6-1

SOLUTION

1.

Increase in Costs for the Year

Assume Trendy uses New Dye

Units to dye

60,000

Cost differential ($1.25 – $0.40) per ounce × 3 ounces

× $2.55

Increase in costs

$153,000

Because the fine is only $120,000, Trendy would be financially better off by not switching.

1. If Trendy switches to the new dye, costs will increase by $153,000.

If Trendy implements Kaizen costing, costs will be reduced as follows:

Original monthly costs

Input

Unit cost

Number of units

Total cost

Annual cost

Fabric

$7.00

6,000*

$42,000

$504,000

Labor

$3.50

6,000*

21,000

252,000

Total

$63,000

$756,000

* (12,000 + 60,000)/12 months = 6,000 units

Monthly decrease in costs

Fabric

Labor cost

Month 1

$ 42,000

Month 1

$ 21,000

Month 2

41,580

Month 2

20,790

Month 3

41,164

Month 3

20,582

Month 4

40,753

Month 4

20,376

Month 5

40,345

Month 5

20,173

Month 6

39,942

Month 6

19,971

Month 7

39,542

Month 7

19,771

Month 8

39,147

Month 8

19,573

Month 9

38,755

Month 9

19,378

Month 10

38,368

Month 10

19,184

Month 11

37,984

Month 11

18,992

Month 12

37,604

Month 12

18,802

$477,184

$238,592

$715,776

TOTAL

Difference between costs with and without Kaizen improvements

($756,000 – $715,776)

$ 40,224

This means costs increase a net amount of $153,000 – 40,224 = $112,776

6-2

3. Reduction in materials can be accomplished by reducing waste and scrap. Reduction in

direct labor can be accomplished by improving the efficiency of operations and decreasing down

time. Employees who make and dye the T-shirts may have suggestions for ways to do their

jobs more efficiently. For instance, employees may recommend process changes that reduce idle

time, setup time, and scrap. To motivate workers to improve efficiency, many companies have

set up programs that share productivity gains with the workers. Trendy must be careful that

productivity improvements and cost reductions do not in any way compromise product quality.

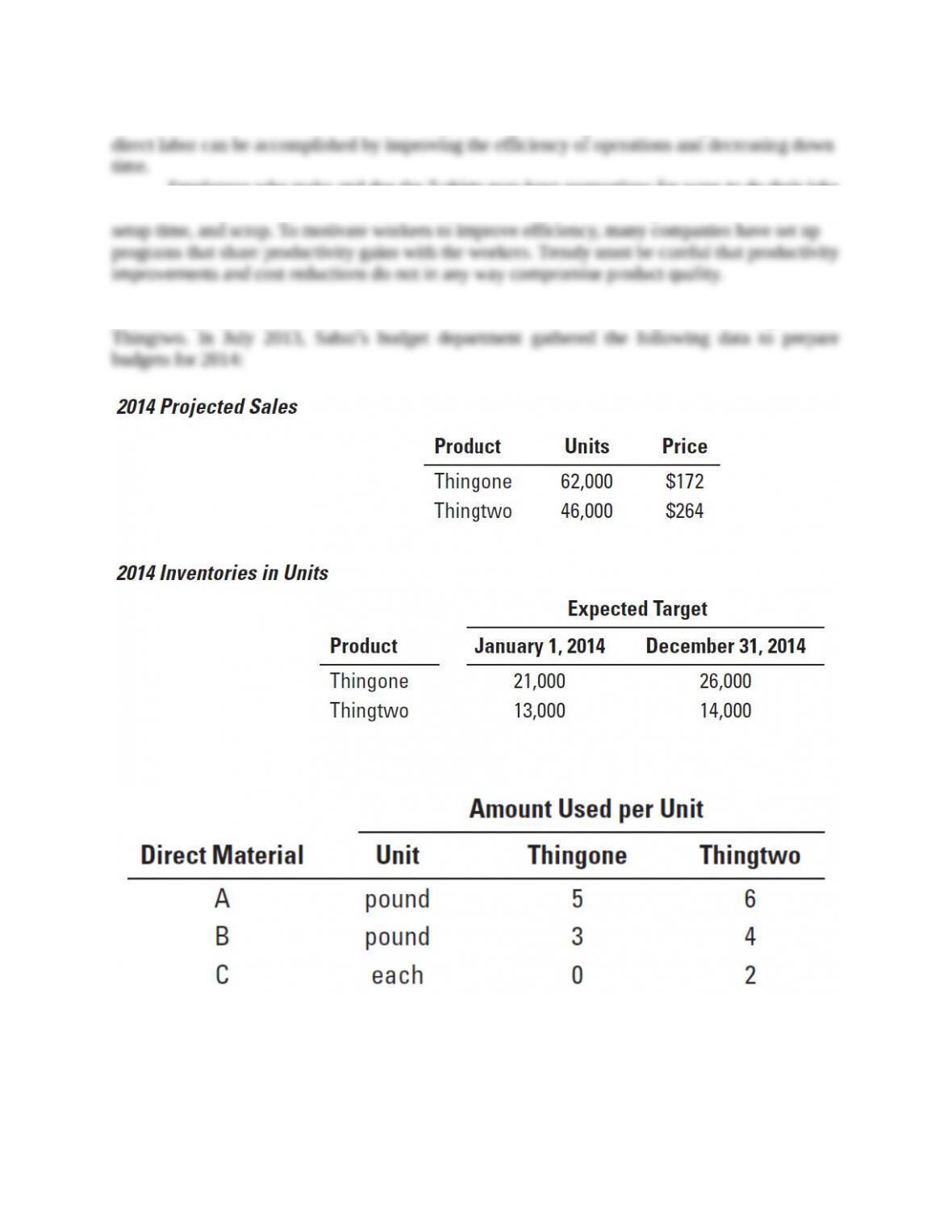

(CPA, adapted) The Sabat Corporation manufactures and sells two products: Thingone and

Thingtwo. In July 2013, Sabat’s budget department gathered the following data to prepare budgets

for 2014:

The following direct materials are used in the two products:

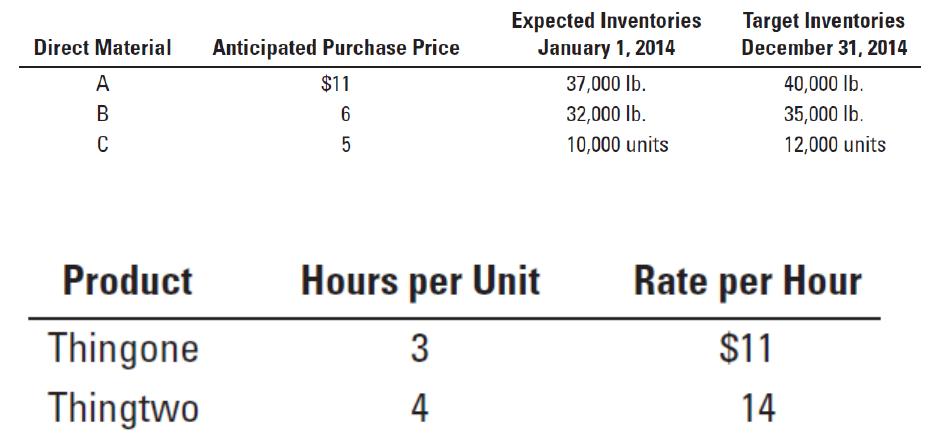

Projected data for 2014 for direct materials are:

6-3

Projected direct manufacturing labor requirements and rates for 2014 are:

Manufacturing overhead is allocated at the rate of $19 per direct manufacturing labor-hour.

Based on the preceding projections and budget requirements for Thingone and Thingtwo, prepare

the following budgets for 2014:

Required:

1. Revenues budget (in dollars)

2. What questions might the CEO ask the marketing manager when reviewing the revenues

budget? Explain briefly.

3. Production budget (in units)

4. Direct material purchases budget (in quantities)

5. Direct material purchases budget (in dollars)

6. Direct manufacturing labor budget (in dollars)

7. Budgeted finished goods inventory at December 31, 2014 (in dollars)

8. What questions might the CEO ask the production manager when reviewing the production,

direct materials, and direct manufacturing labor budgets?

9. How does preparing a budget help Sabat Corporation’s top management better manage the

company?

SOLUTION

This is a routine budgeting problem. The key to its solution is to compute the correct quantities of

finished goods and direct materials. Use the following general formula:

( )

Budgeted production

or purchases

=

( )

Target ending

inventory

+

( )

Budgeted sales or

materials used

–

( )

Beginning

inventory

1. Sabat Corporation

Revenues Budget for 2014

Units Price Total

Thingone 62,000 $172 $10,664,000

Thingtwo 46,000 264 12,144,000

Budgeted revenues $22,808,000

2. The CEO would want to probe if the revenue budget is sufficiently stretched. Is the revenue

growing faster than the market? Should the company increase marketing and advertising spending

to grow sales? Would increasing the sales force or giving salespersons stronger incentives result

in higher sales?

3. Sabat Corporation

Production Budget (in units) for 2014

Thingone

Thingtwo

Budgeted sales in units

62,000

46,000

Add target finished goods inventories,

December 31, 2014

26,000

14,000

Total requirements

88,000

60,000

Deduct finished goods inventories,

January 1, 2014

21,000

13,000

Units to be produced

67,000

47,000

4. Sabat Corporation

Direct Materials Purchases Budget (in quantities) for 2014

Direct Materials

A

B

C

Direct materials to be used in production

• Thingone (budgeted production of 67,000

units times 5 lbs. of A, 3 lbs. of B)

335,000

201,000

—

• Thingtwo (budgeted production of 47,000

units times 6 lbs. of A, 4 lbs. of B, 2 lb. of C)

282,000

188,000

94,000

Total

617,000

389,000

94,000

Add target ending inventories, December 31, 2014

40,000

35,000

12,000

Total requirements in units

657,000

424,000

106,000

Deduct beginning inventories, January 1, 2012

37,000

32,000

10,000

Direct materials to be purchased (units)

620,000

392,000

96,000

5. Sabat Corporation

Direct Materials Purchases Budget (in dollars) for 2014

Budgeted

Expected

Purchases

Purchase

(Units)

Price per unit

Total

Direct material A

620,000

$11

$6,820,000

Direct material B

392,000

6

2,352,000

6-5

Direct material C

96,000

5

480,000

Budgeted purchases

$9,652,000

6. Sabat Corporation

Direct Manufacturing Labor Budget (in dollars) for 2014

Direct

Budgeted

Manufacturing

Rate

Production

Labor-Hours

Total

per

(Units)

per Unit

Hours

Hour

Total

Thingone

67,000

3

201,000

$11

$2,211,000

Thingtwo

47,000

4

188,000

14

2,632,000

Total

$4,843,000

7. Sabat Corporation

Budgeted Finished Goods Inventory

at December 31, 2014

Thingone:

Direct materials costs:

A, 5 pounds × $11 $55

B, 3 pounds × $6 18 $ 73

Direct manufacturing labor costs,

3 hours × $11 33

Manufacturing overhead costs at $19 per direct

manufacturing labor-hour (3 hours × $19) 57

Budgeted manufacturing costs per unit $163

Finished goods inventory of Thingone

$163 × 26,000 units $4,238,000

Thingtwo:

Direct materials costs:

A, 6 pounds × $11 $66

B, 4 pounds × $6 24

C, 2 each × $5 10 $100

Direct manufacturing labor costs,

4 hours × $14 56

Manufacturing overhead costs at $19 per direct

manufacturing labor-hour (4 hours × $19) 76

Budgeted manufacturing costs per unit $232

Finished goods inventory of Thingtwo

$232 × 14,000 units 3,248,000

Budgeted finished goods inventory, December 31, 2014 $7,486,000

8. The CEO would want to ask the production manager why the target ending inventories

have increased. Could production be more closely tailored to demand? Could the efficiency and

productivity of direct materials and direct manufacturing labor be increased? Could direct

materials inventory be reduced?

6-6

9. Preparing a budget helps Saadi Corporation manage costs based on revenues and production

needs, look for opportunities to increase efficiencies, reduce costs, particularly in areas where costs

are high, coordinate and communicate across different parts of the organization, create a

framework for judging performance and facilitating learning, and motivate managers and

employees to achieve “stretch” targets of higher revenues and lower costs.

This is a routine budgeting problem. The key to its solution is to compute the correct quantities of

finished goods and direct materials. Use the following general formula:

( )

Budgeted production

or purchases

=

( )

Target ending

inventory

+

( )

Budgeted sales or

materials used

–

( )

Beginning

inventory

6-33 (30 min.) Budgeted income statement.

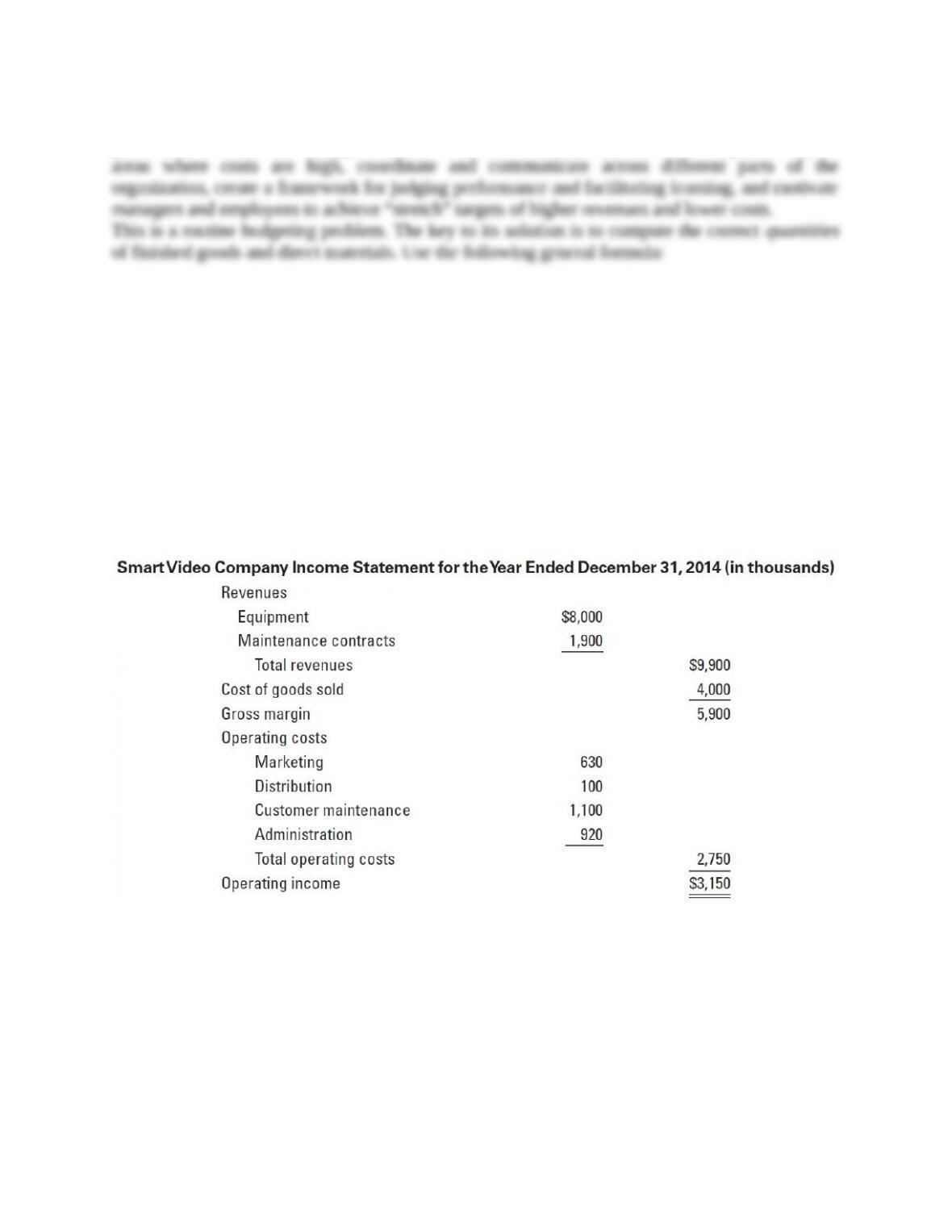

(CMA, adapted) Smart Video Company is a manufacturer of videoconferencing products.

Maintaining the videoconferencing equipment is an important area of customer satisfaction. A

recent downturn in the computer industry has caused the videoconferencing equipment segment

to suffer, leading to a decline in Smart Video’s financial performance. The following income

statement shows results for 2014:

Smart Video’s management team is preparing the 2015 budget and is studying the following

information:

1. Selling prices of equipment are expected to increase by 10% as the economic recovery begins.

The selling price of each maintenance contract is expected to remain unchanged from 2014.

2. Equipment sales in units are expected to increase by 6%, with a corresponding 6% growth in

units of maintenance contracts.

3. Cost of each unit sold is expected to increase by 5% to pay for the necessary technology and

quality improvements.

4. Marketing costs are expected to increase by $290,000, but administration costs are expected to

remain at 2014 levels.

6-7

5. Distribution costs vary in proportion to the number of units of equipment sold.

6. Two maintenance technicians are to be hired at a total cost of $160,000, which covers wages

and related travel costs. The objective is to improve customer service and shorten response

time.

7. There is no beginning or ending inventory of equipment.

Required:

1. Prepare a budgeted income statement for the year ending December 31, 2015.

2. How well does the budget align with Smart Video’s strategy?

3. How does preparing the budget help Smart Video’s management team better manage the

company?

SOLUTION

1. Smart Video Company

Budgeted Income Statement for 2014

(in thousands)

Revenues

Equipment ($8,000 × 1.06 × 1.10) $9,328

Maintenance contracts ($1,900 × 1.06) 2,014

Total revenues $11,342

Cost of goods sold ($4,000 × 1.06 × 1.05) 4,452

Gross margin 6,890

Operating costs:

Marketing costs ($630 + $290) 920

Distribution costs ($100 × 1.06) 106

Customer maintenance costs ($1,100 + $160) 1,260

Administrative costs 920

Total operating costs 3,206

Operating income $3,684

2. The budget aligns with Videocom’s key strategy of customer satisfaction through

maintaining videoconferencing equipment by hiring maintenance technicians and increasing

costs of customer maintenance by 14.55% ($160,000 ÷ $1,100,000) more than the 6% forecasted

increase in sales.

3. Preparing a budget helps Videocom manage costs based on revenues and production

needs, look for opportunities to increase efficiencies, reduce costs, particularly in areas where

costs are high, coordinate and communicate across different parts of the organization, create a

framework for judging performance and facilitating learning, and motivate managers and

employees to achieve “stretch” targets of higher revenues and lower costs.

6-34 (15 min.) Responsibility of purchasing agent.

6-8

Paula Beane owns a restaurant franchise that is part of a chain of “southern homestyle” restaurants.

One of the chain’s popular breakfast items is biscuits and gravy. Central Warehouse makes and

freezes the biscuit dough, which it then sells to the franchise stores where it is thawed and baked

in the individual stores by the cook. Each franchise also has a purchasing agent who orders the

biscuits (and other items) based on expected demand. In March 2015, one of the freezers in Central

Warehouse breaks down and biscuit production is reduced by 25% for 3 days. During those 3 days,

Paula’s franchise runs out of biscuits but demand does not slow down. Paula’s franchise cook,

Betty Baker, sends one of the kitchen helpers to the local grocery store to buy refrigerated ready–

to-bake biscuits. Although the customers are kept happy, the refrigerated biscuits cost Paula’s

franchise three times the cost of the Central Warehouse frozen biscuits, and the franchise loses

money on this item for those 3 days. Paula is angry with the purchasing agent for not ordering

enough biscuits to avoid running out of stock and with Betty for spending too much money on the

replacement biscuits.

Required:

Who is responsible for the cost of the biscuits? At what level is the cost controllable? Do you

agree that Paula should be angry with the purchasing agent? With Betty? Why or why not?

SOLUTION

The cost of the biscuits is usually the responsibility of the purchasing agent, and usually

controllable by the Central Warehouse. However, in this scenario, Betty the cook has taken the

responsibility for the cost of the replacement biscuits from the purchasing agent by making a

purchasing decision. Because Paula holds the purchasing agent responsible for biscuit costs, and

presuming that Betty knew this, Betty should have discussed her decision with the purchasing

agent before sending the kitchen helper to the store.

Paula should not be angry because her employees acted to satisfy the customers on a short-term

emergency basis. Presuming the Central Warehouse does not consistently have problems with

their freezer, there is no way the purchasing agent could foresee the biscuit shortage and plan

accordingly. Also, the problem only lasted three days, which, in the course of the year (or even

the month) will not seriously harm the profits of a restaurant that sells a variety of foods.

However, had they run out of biscuits for three days, this could have long-term implications for

customer satisfaction and customer loyalty, and in the long run could harm profits as customers

find other restaurants at which to eat breakfast.

6-35 (60 min.) Comprehensive problem with ABC costing

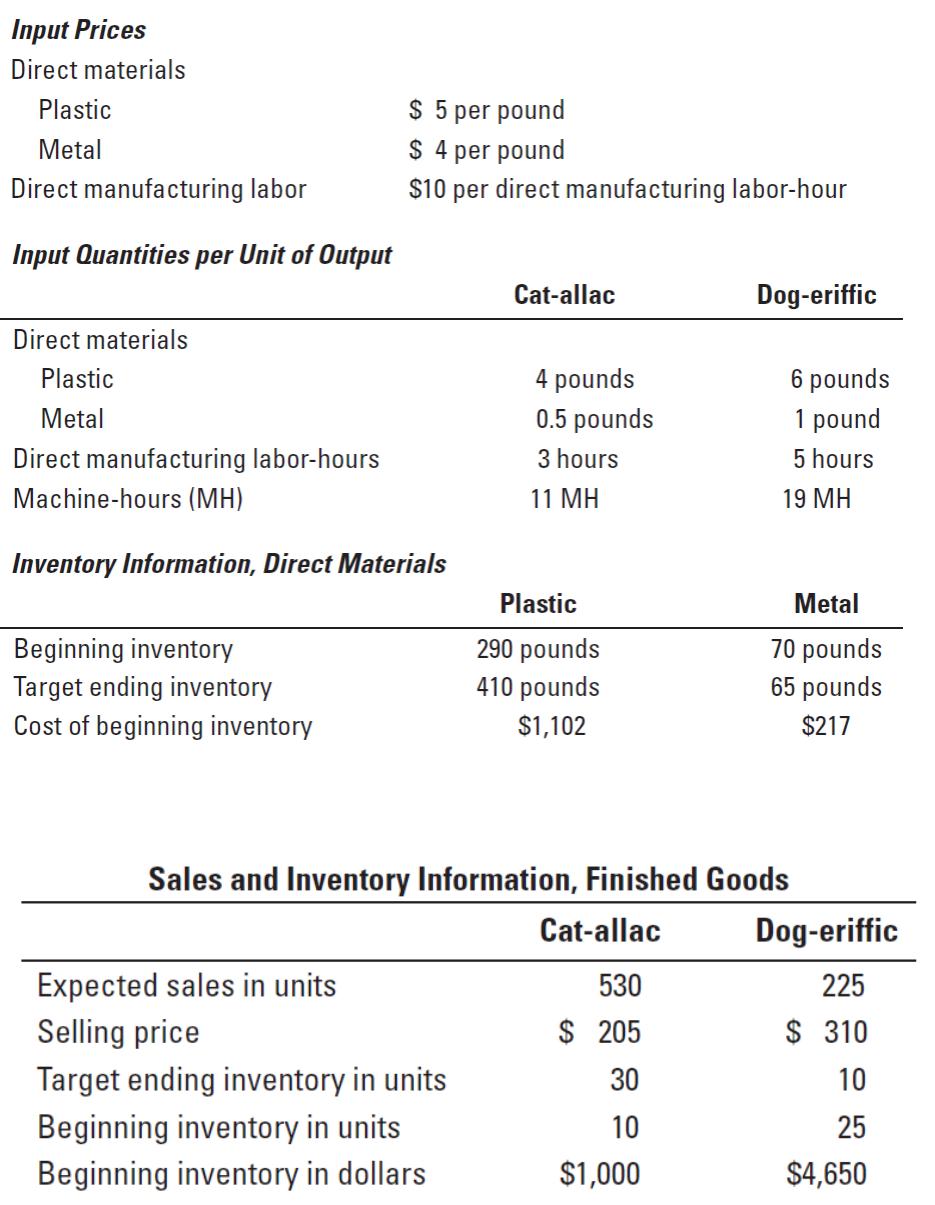

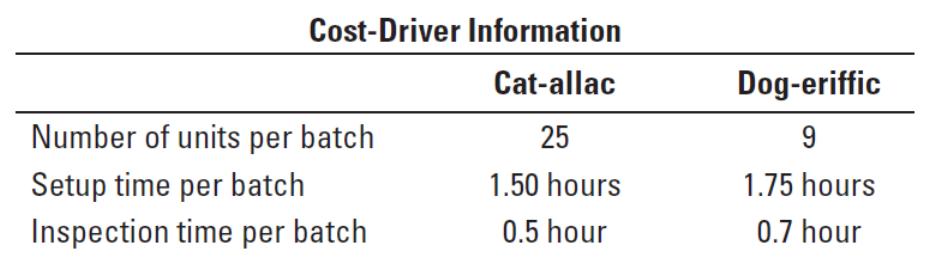

Animal Gear Company makes two pet carriers, the Cat-allac and the Dog-eriffic. They are both

made of plastic with metal doors, but the Cat-allac is smaller. Information for the two products for

the month of April is given in the following tables:

6-9

Animal Gear accounts for direct materials using a FIFO cost flow assumption.

Animal Gear uses a FIFO cost flow assumption for finished goods inventory.

6-10

Animal Gear uses an activity-based costing system and classifies overhead into three activity

pools: Setup, Processing, and Inspection. Activity rates for these activities are $105 per setup-hour,

$10 per machine-hour, and $15 per inspection-hour, respectively. Other information follows:

Nonmanufacturing fixed costs for March equal $32,000, half of which are salaries. Salaries are

expected to increase 5% in April. The only variable nonmanufacturing cost is sales commission,

equal to 1% of sales revenue.

Prepare the following for April:

Required:

1. Revenues budget

2. Production budget in units

3. Direct material usage budget and direct material purchases budget

4. Direct manufacturing labor cost budget

5. Manufacturing overhead cost budgets for each of the three activities

6. Budgeted unit cost of ending finished goods inventory and ending inventories budget

7. Cost of goods sold budget

8. Nonmanufacturing costs budget

9. Budgeted income statement (ignore income taxes)

10. How does preparing the budget help Animal Gear’s management team better manage the

company?