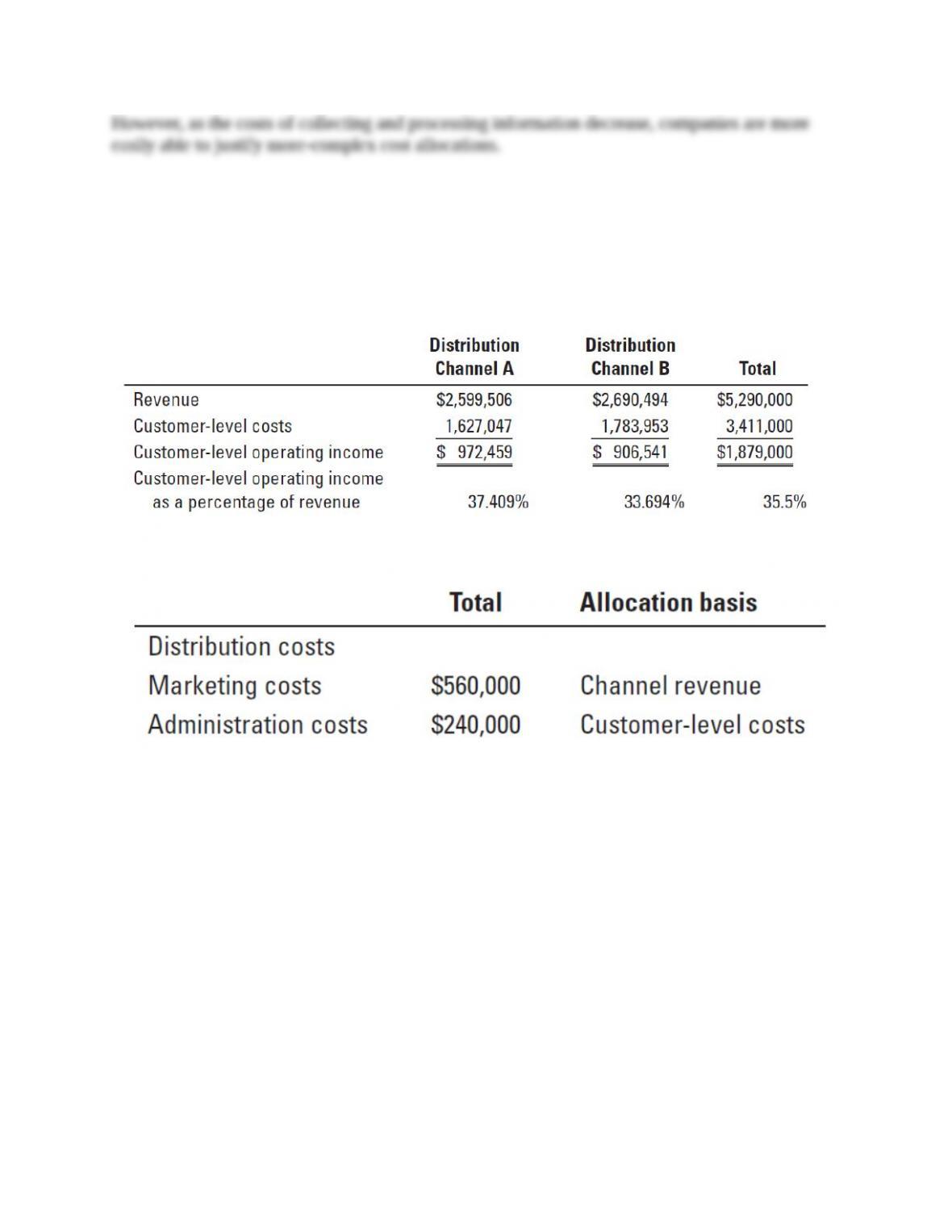

Distribution

Channel A

Distribution

Channel B

Total

Revenue

$2,599,506

$2,690,494

$5,290,000

Customer-level costs

1,627,047

1,783,953

3,411,000

Customer-level operating income

Distribution costs

972,459

906,541

1,879,000

Marketing costs1

275,184

284,816

560,000

Administration costs2

114,480

125,520

240,000

Allocated distribution costs

389,664

410,336

800,000

Distribution-channel operating

income after allocating

distribution costs

582,795

496,205

1,079,000

Allocated corporate costs

440,000

500,000

940,000

Fully allocated distribution

channel operating income

$ 142,795

$ (3,795)

$ 139,000

Distribution-channel operating

income as a percentage of

revenue

5.5%

0.14%

2.6%

1$560,000 × ($2,599,506 ÷ $5,290,000; $2,690,494 ÷ $5,290,000)

2$240,000 × ($1,627,047 ÷ $3,411,000; $1,783,953 ÷ $3,411,000)

2. Basic Boards should not close down any distribution channel. Distribution Channel B

shows a loss, but if the company was to close down this channel, it would not save any corporate

costs. Basic Boards would then forgo the operating income of $496,205 but not save any costs.

Allocating corporate costs to the distribution channels gives the misleading impression that

potential cost savings from closing down a channel are greater than the likely amount. Of course,

the overall profitability of Basic Boards is very low (2.6%), so Basic Boards should carefully

examine all its costs to see where it might be able to achieve cost savings.

3. I would allocate corporate costs to distribution channels. One important advantage of

doing so is that the full costs of supporting the sales of products to customers in a distribution

channel are included when determining customer-level profitability. In the long run, distribution

channels must be profitable on a full-cost basis if the company is to be profitable.

Another advantage of allocating corporate costs to distribution channels is to encourage

distribution-channel managers to set long-run prices to cover the costs of all resources used to

produce and sell products to customers. Full-cost allocation reduces the temptation for

companies to cut prices to simply cover partial (or variable) costs.

Allocating corporate costs will motivate managers of the distribution channels to examine

how corporate costs are planned and controlled. The distribution-channel managers will want to

understand whether these costs are providing them benefits in line with their costs. For example,

are corporate costs supporting better distribution of products to customers?

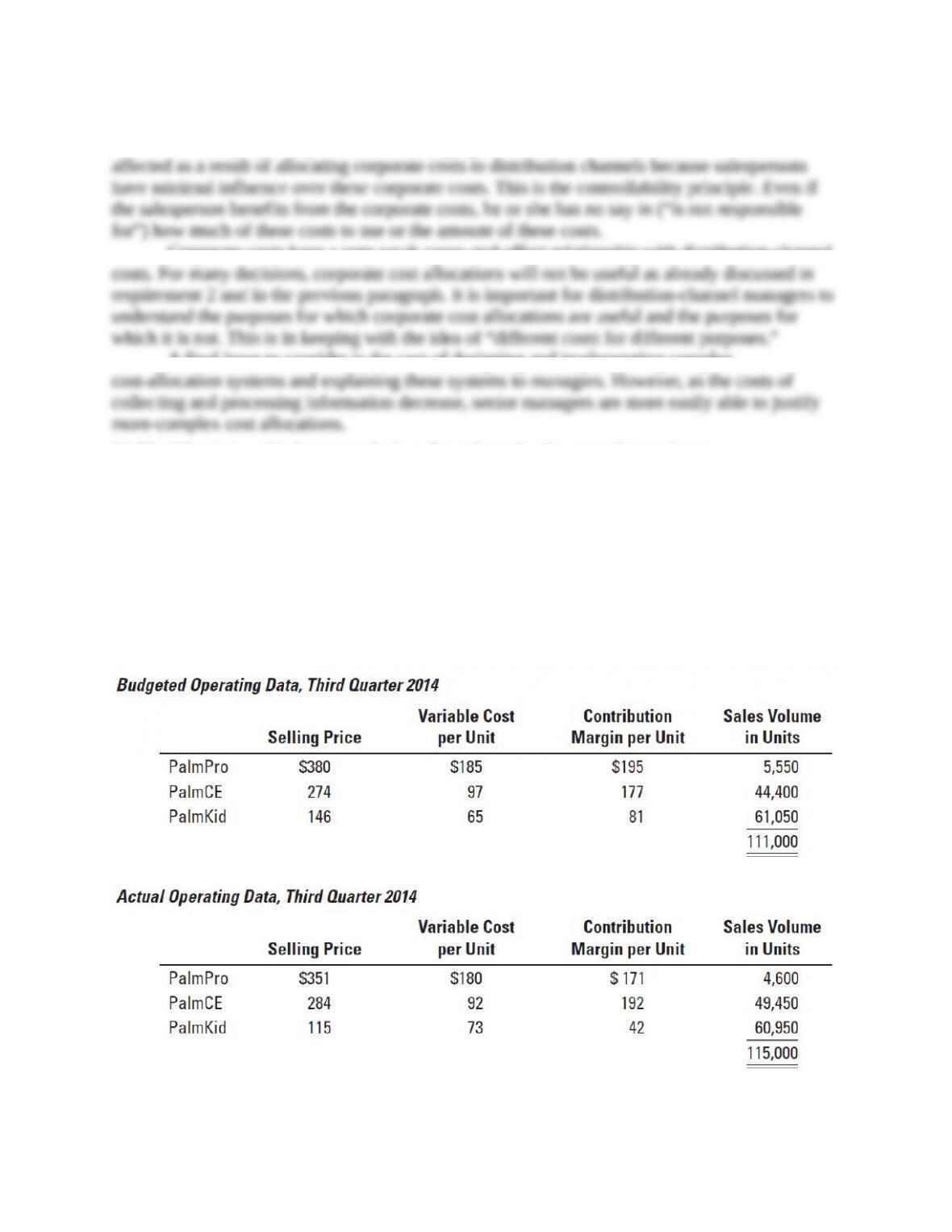

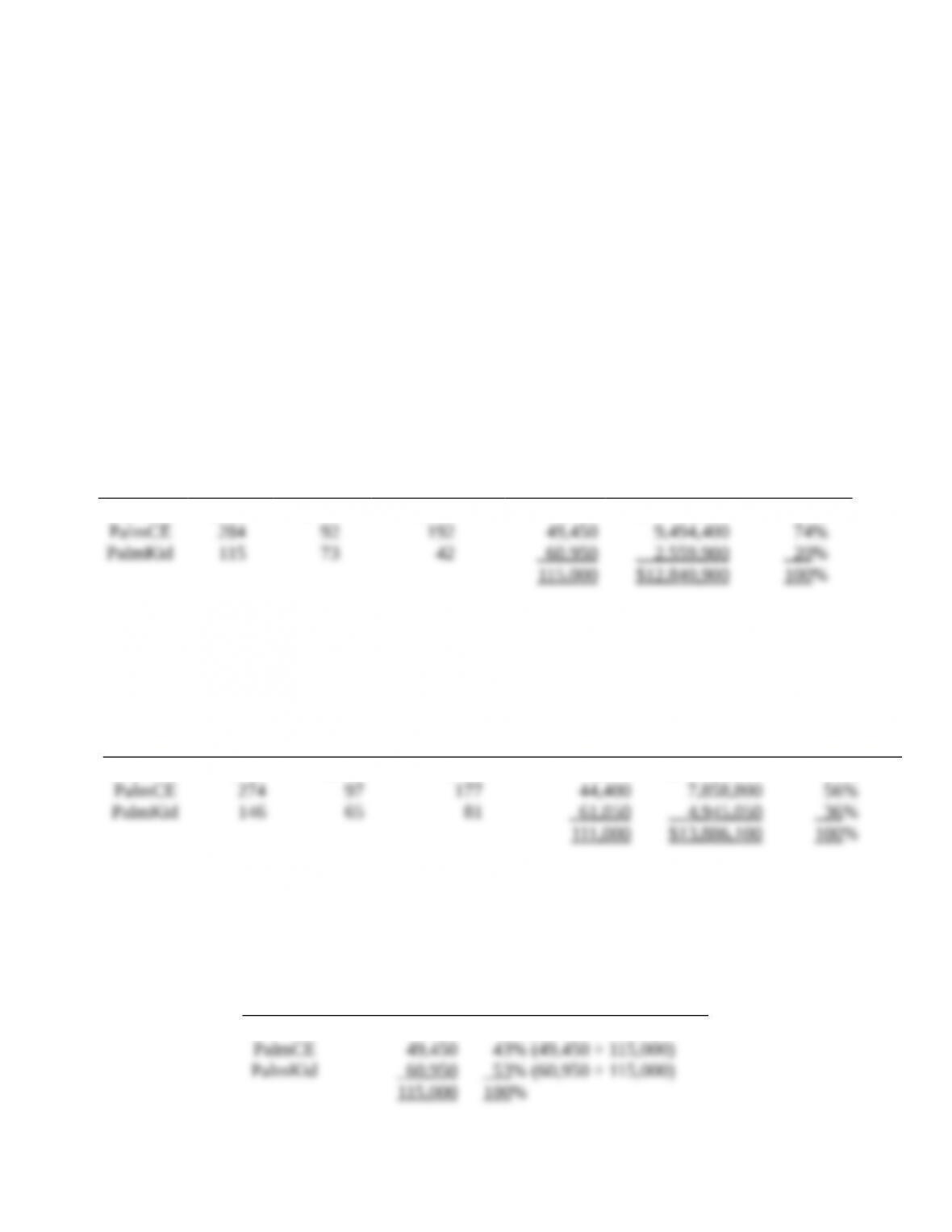

=

500,000 (–0.02) $125.10

=

$1,251,000 U

Market-size

variance

=

Actual Budgeted

market size market size

in units in units

−

Budgeted

Budgeted contribution margin

market per composite unit

share for budgeted mix

=

(500,000 – 444,000) 0.25 $125.10

=

56,000 0.25 $125.10

=

$1,751,400 F

Solution Exhibit 14-37 presents the market-share variance, the market-size variance, and the sales-

quantity variance for the third quarter 2014.