1) Indirect manufacturing costs should be allocated equally to each job.

2) Kaizen budgeting does NOT make sense for cost centers.

3) Engineered costs result from a cause-and-effect relationship between the cost driver

output and the resources used to produce that output.

4) Process-costing systems using standard costs record standard direct material costs in

Direct Materials Control and standard conversion costs in Conversion Costs Control.

5) The accrual accounting rate-of-return method has a significant weakness for use in

making capital budgeting decisions because it does NOT track cash flows and it ignores

the time value of money.

6) The flexible-budget variance is the difference between an actual result and the

flexible-budget amount based on the level of output actually achieved in the budget

period.

7) The technical considerations of budgeting encourage managers and other employees

to strive for achieving the goals of the organization.

8) When actual revenues exceed budgeted revenues, a favorable variance arises.

9) Value engineering cannot decrease value-added costs.

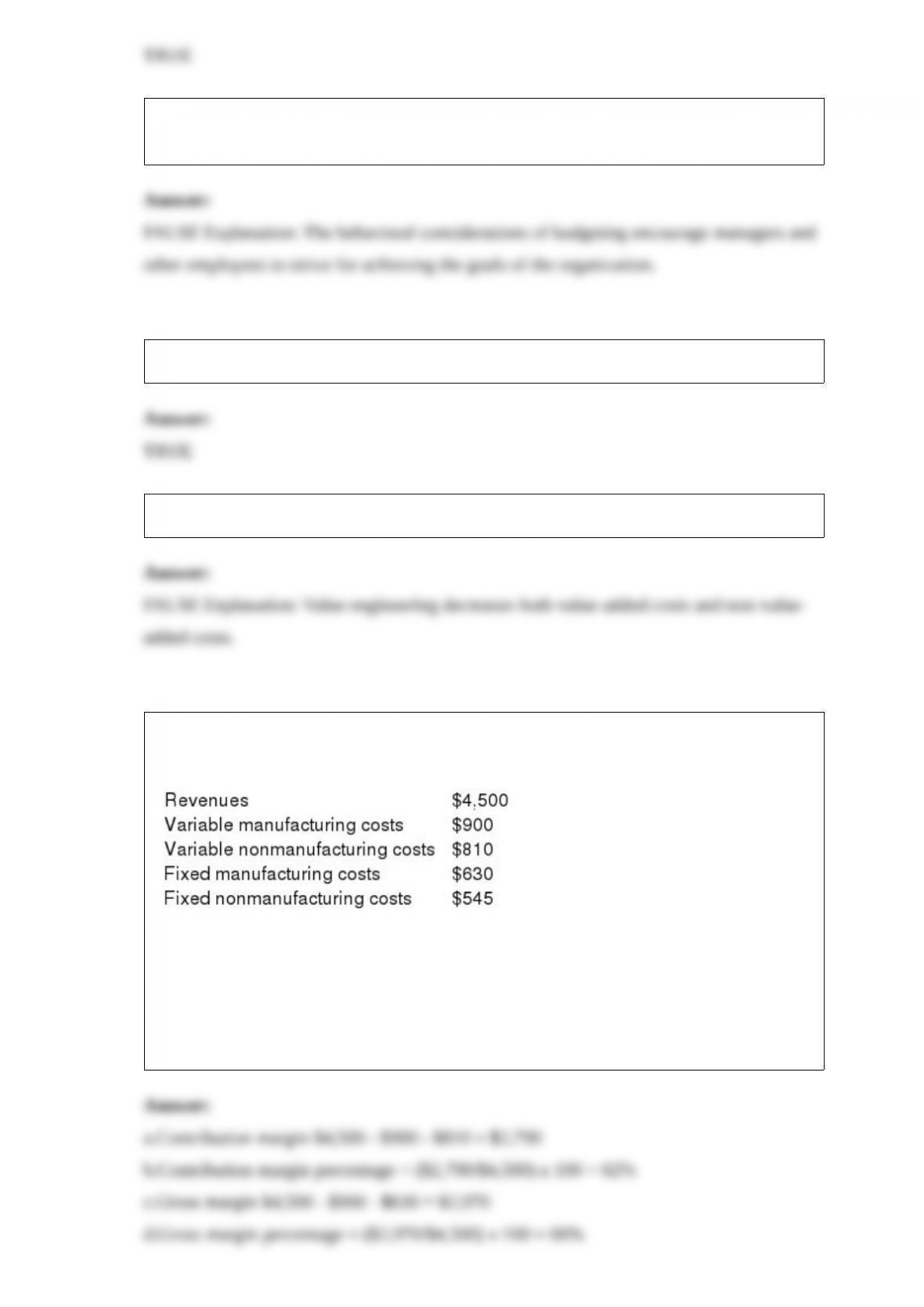

10) Arthur’s Plumbing reported the following:

Required:

a.Compute contribution margin.

b.Compute contribution margin percentage.

c.Compute gross margin.

d.Compute gross margin percentage.

e.Compute operating income.

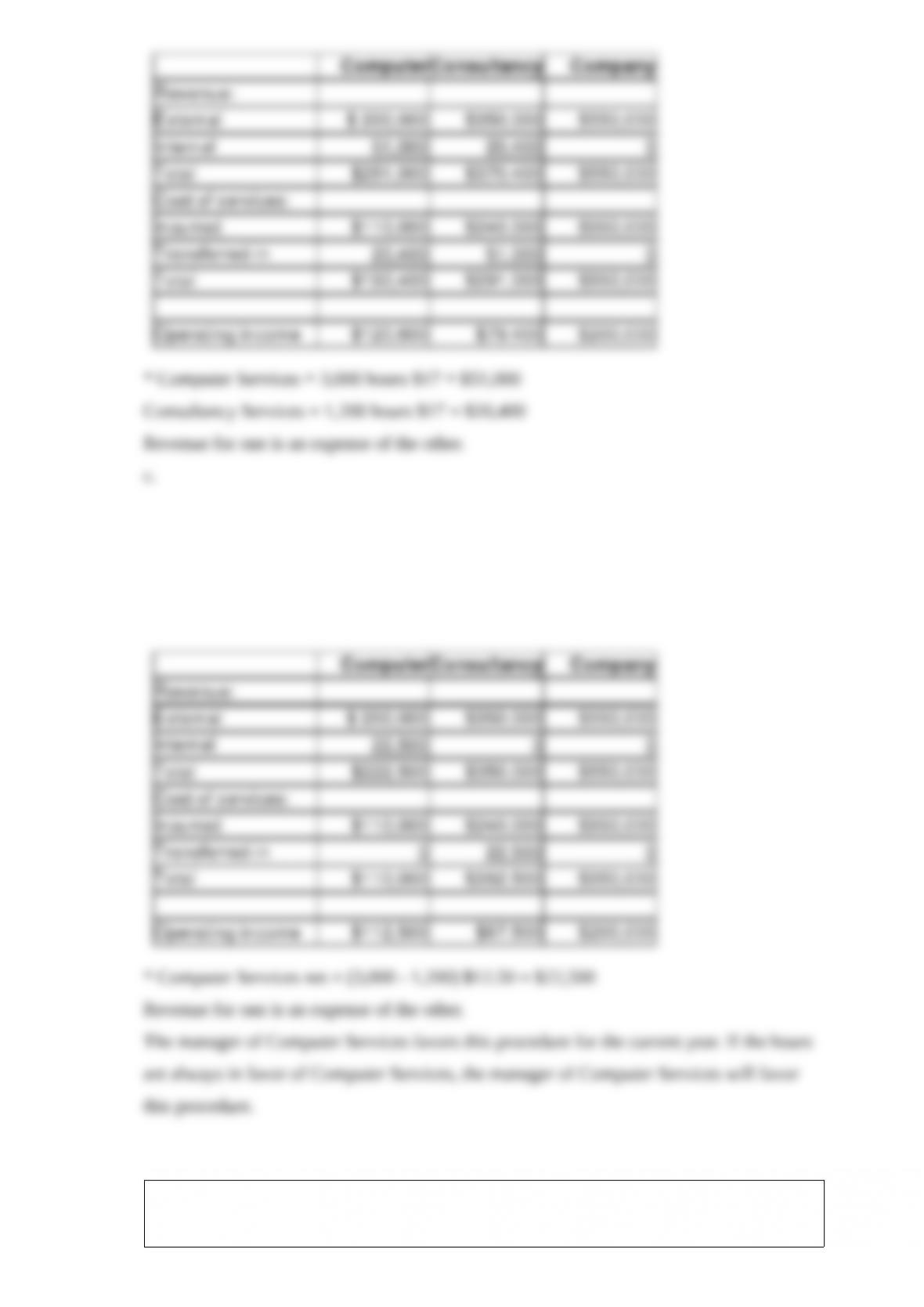

11) DesMoines Valley Company has two divisions, Computer Services and Consultancy

Services. In addition to their external customers, each division performs work for the

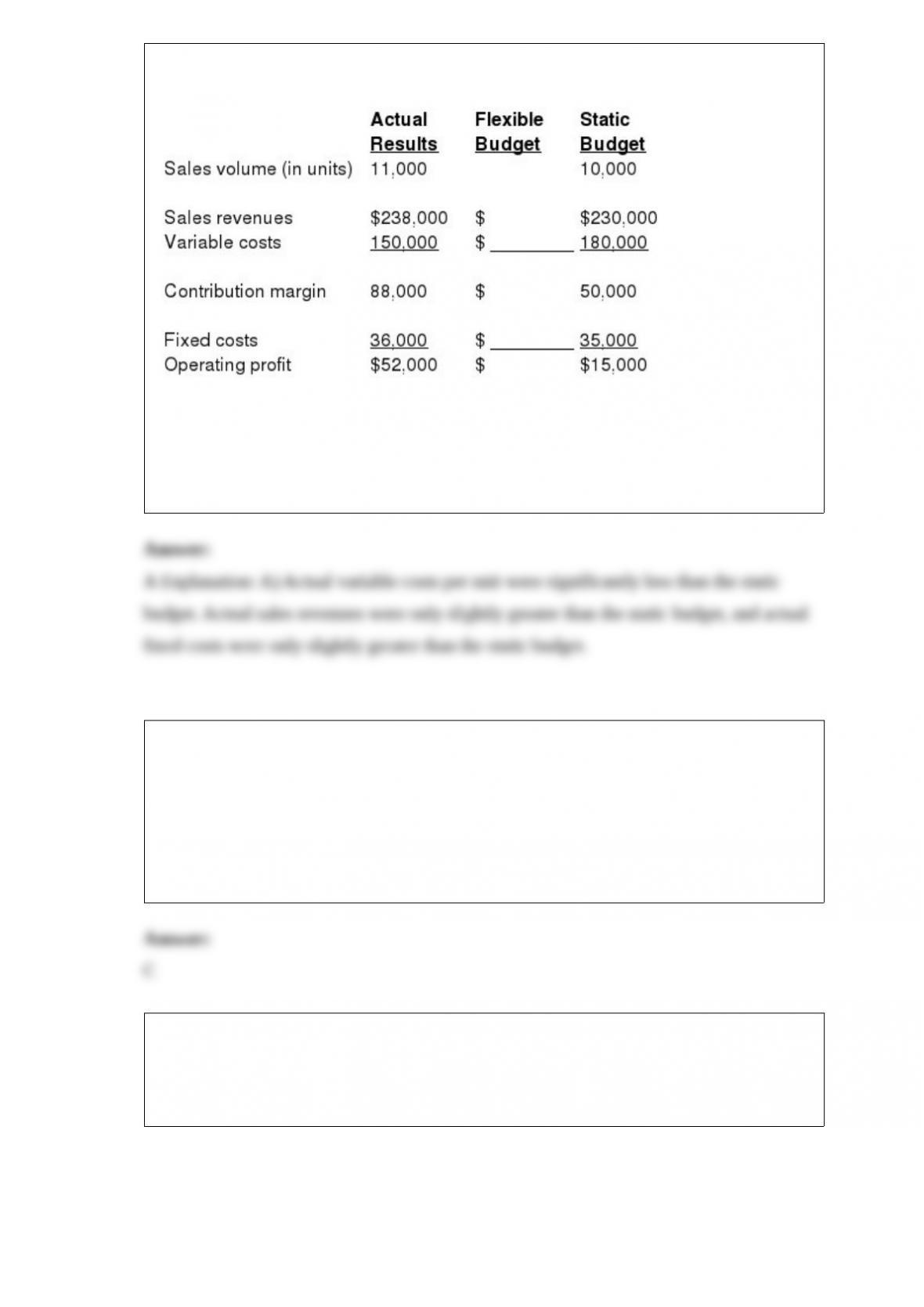

other division. The external fees earned by each division in 20X5 were $200,000 for

Computer Services and $350,000 for Consultancy Services. Computer Services worked

3,000 hours for Consultancy Services, who, in turn, worked 1,200 hours for Computer

Services. The total costs of external services performed by Computer Services were

$110,000 and $240,000 by Consultancy Services.

Required:

a.Determine the operating income for each division and for the company as a whole if

the transfer price from Computer Services to Consultancy Services is $15 per hour and

the transfer price from Consultancy Services to Computer Services is $12.50 per hour.

b.Determine the operating income for each division and for the company as a whole if

the transfer price between divisions is $17 per hour.

c.What are the operating income results for each division and for the company as a

whole if the two divisions net the hours worked for each other and charge $12.50 per

hour for the one with the excess? Which division manager prefers this arrangement?

12) Soft Cushion Company is highly decentralized. Each division is empowered to

make its own sales decisions. The Assembly Division can purchase stuffing, a key

component, from the Production Division or from external suppliers. The Production

Division has been the major supplier of stuffing in recent years. The Assembly Division

has announced that two external suppliers will be used to purchase the stuffing at $20

per pound for the next year. The Production Division recently increased its unit price to

$40. The manager of the Production Division presented the following information

variable cost $32 and fixed cost $8 to top management in order to attempt to force the

Assembly Division to purchase the stuffing internally. The Assembly Division

purchases 20,000 pounds of stuffing per month.

What would be the monthly operating advantage (disadvantage) of purchasing the

goods internally, assuming the external supplier increased its price to $50 per pound and

the Production Division is able to utilize the facilities for other operations, resulting in a

monthly cash-operating savings of $30 per pound?

A) $1,000,000

B) $360,000

C) $(240,000)

D) $(400,000)

13) Management accounting information typically includes ________.

A) tabulated results of customer satisfaction surveys

B) the cost of producing a product

C) the percentage of units produced that are defective

D) All of these answers are correct.

14) Query Company sells pillows for $25.00 each. The manufacturing cost, all variable,

is $10 per pillow. The company is planning on renting an exhibition booth for both

display and selling purposes at the annual crafts and art convention. The convention

coordinator allows three options for each participating company. They are:

1.paying a fixed booth fee of $5,010, or

2.paying an $4,000 fee plus 10% of revenue made at the convention, or

3.paying 20% of revenue made at the convention.

Required:

a.Compute the breakeven sales in pillows of each option.

b.Which option should Query Company choose, assuming sales are expected to be 800

pillows?

15) Midend’s Camera Shop has prepared the following flexible budget for September

and is in the process of interpreting the variances. F denotes a favorable variance and U

denotes an unfavorable variance.

The explanation that lower-quality materials were purchased is most likely for

________.

A) Material A

B) Material B

C) Material C

D) both Material A and C

16) If total payroll processing costs of $64,000 are allocated on the basis of number of

employees, the amount allocated to the Large Department would be ________.

A) $18,400

B) $19,200

C) $17,800

D) $19,400

17) Nancy Company has budgeted sales of $300,000 with the following budgeted costs:

Compute the average markup percentage for setting prices as a percentage of:

a.The full cost of the product

b.The variable cost of the product

c.Variable manufacturing costs

d.Total manufacturing costs

18) An experience curve ________.

A) is a narrower application of the learning curve

B) measures the decline in cost per unit as production decreases for various value-chain

functions such as marketing as production increases

C) only measures the decline in labor-hours per unit as units produced increases

D) measures the increase in cost per unit as productivity increases

19) A “what-if” technique that examines how a result will change if the original

predicted data are NOT achieved or if an underlying assumption changes is called

________.

A) sensitivity analysis

B) net present value analysis

C) internal rate-of-return analysis

D) adjusted rate-of-return analysis

20) The cost function y = 10,000 + 3X ________.

A) represents a mixed cost

B) will intersect the y-axis at 3

C) has a slope coefficient of 10,000

D) is a curved line

21) Just-in-time purchasing requires ________.

A) larger and less frequent purchase orders

B) smaller and less frequent purchase orders

C) smaller and more frequent purchase orders

D) larger and more frequent purchase orders

22) At a volume of 8,000 units, Pwerson Company incurred $32,000 in factory

overhead costs, including $12,000 in fixed costs. If volume increases to 9,000 units and

both 8,000 units and 9,000 units are within the relevant range, then the company would

expect to incur total factory overhead costs of:

A) $22,500

B) $32,000

C) $34,500

D) $20,000

23) Jupiter Corporation incurred fixed manufacturing costs of $16,000 during 2015.

Other information for 2015 includes:

The budgeted denominator level is 2,000 units.

Units produced total 2,200 units.

Units sold total 1,900 units.

Variable cost per unit is $4.

Beginning inventory is zero.

The fixed manufacturing cost rate is based on the budgeted denominator level.

Under variable costing, the fixed manufacturing costs expensed on the income

statement (excluding adjustments for variances) total ________.

A) $16,000

B) $15,200

C) $14,400

D) 0

24) Sales total $400,000 when variable costs total $300,000 and fixed costs total

$50,000. The breakeven point in sales dollars is ________.

A) $200,000

B) $120,000

C) $170,000

D) $210,000

25) The actual information pertains to the third quarter. As part of the budgeting

process, the Duck Decoy Department of Paralith Incorporated had developed the

following static budget for the third quarter. Duck Decoy is in the process of preparing

the flexible budget and understanding the results.

The primary reason for high actual operating profits was ________.

A) the variable-cost variance

B) increased fixed costs

C) flexible budget variance for revenues

D) lower sales volume than planned

26) The fundamental rethinking and redesign of business processes to achieve

improvements in critical measures of performance, such as cost, quality, service, speed,

and customer satisfaction is ________.

A) directing

B) controlling

C) reengineering

D) structuring

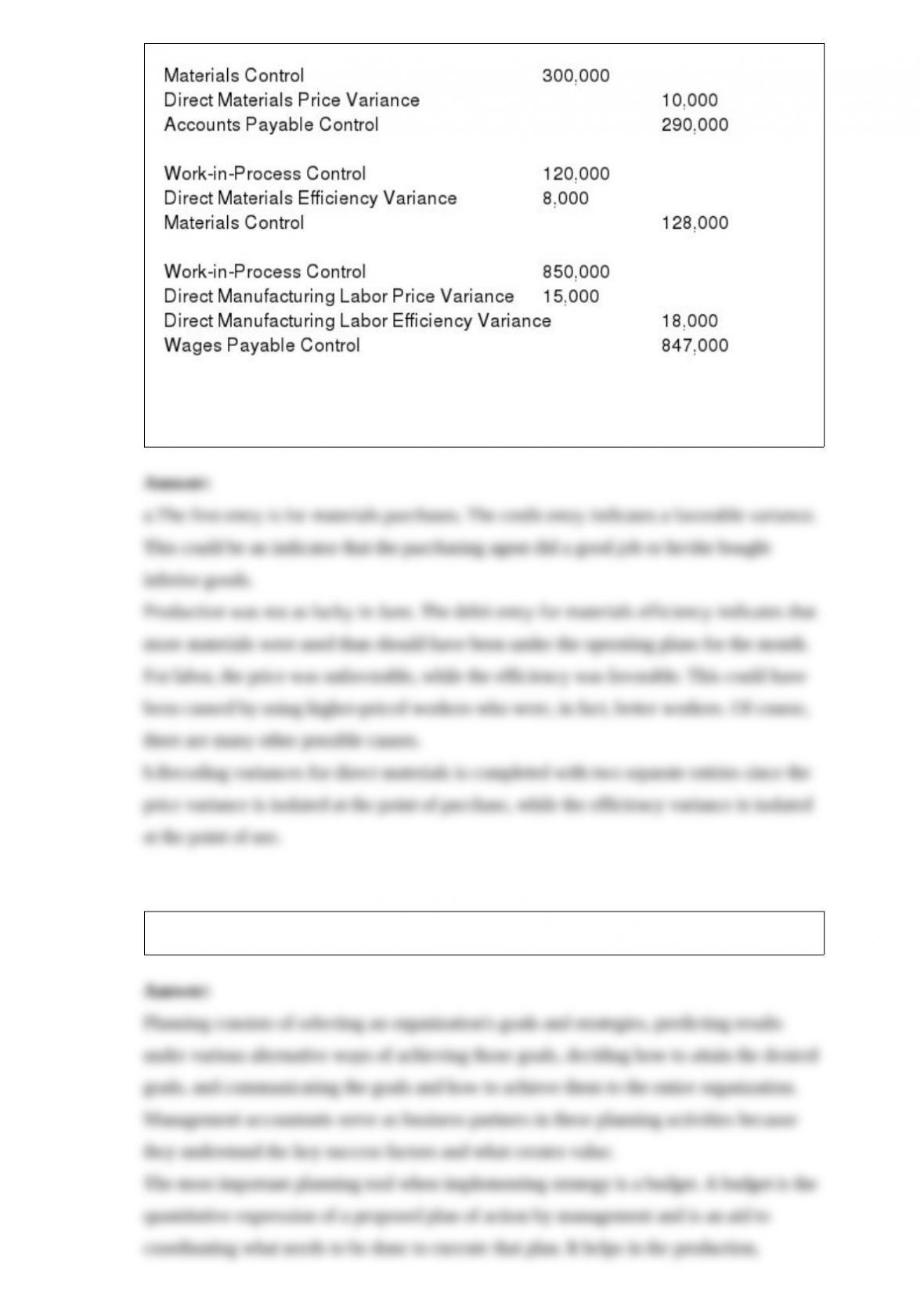

27) Mayberry Company had the following journal entries recorded for the end of June.

Unfortunately, the company’s only accountant quit on July 10 and the president is at a

loss as to the company’s performance for the month of June.

Required:

a.What kind of performance did the company have for June? Explain each variance.

b.Why is Direct Materials given in two entries?

28) What is planning in decision making? Explain how budget helps in planning.

29) List the four standards of ethical conduct for management accountants. For each

standard, give an example that demonstrates compliance with that standard.

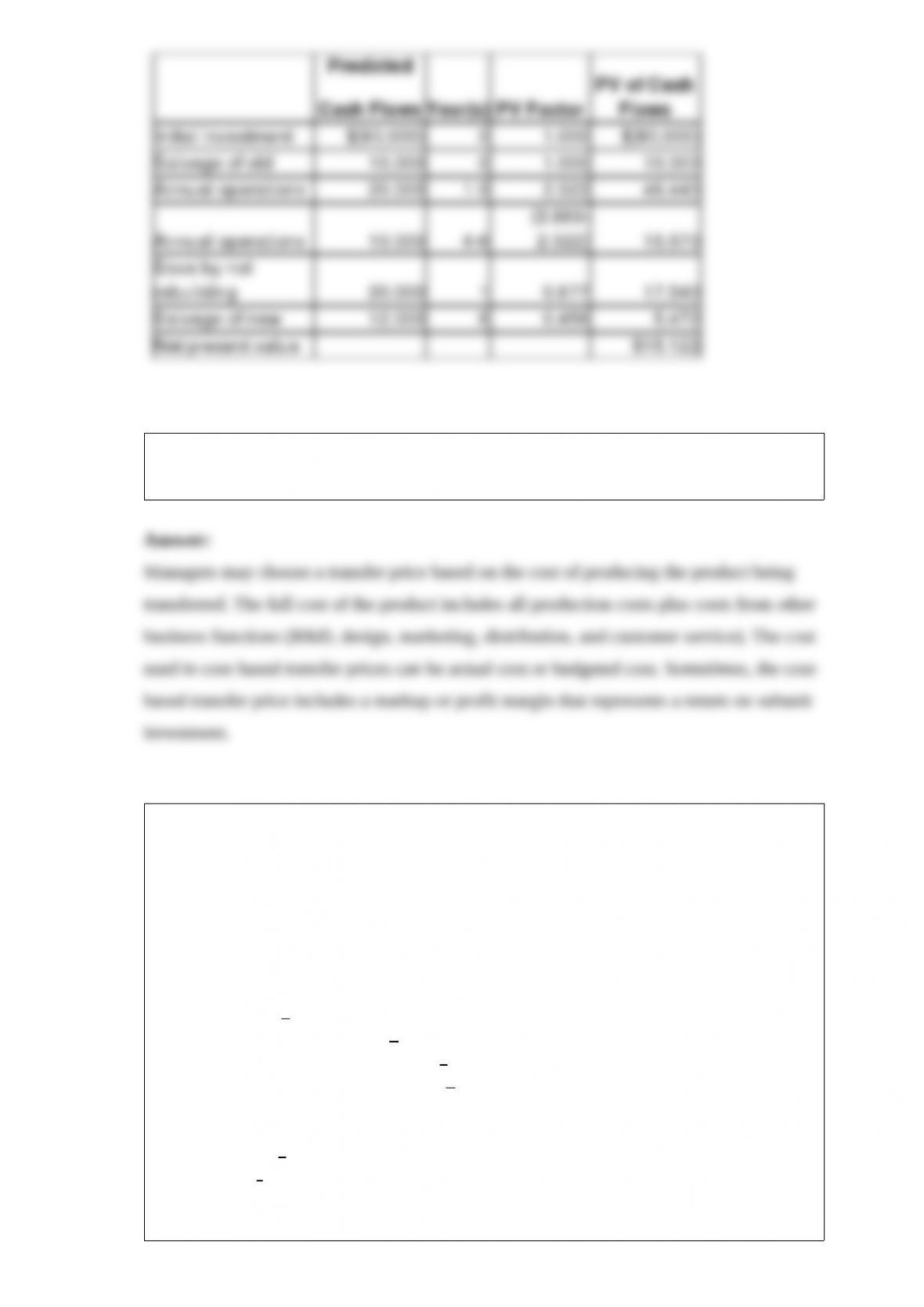

30) ABC Boat Company is interested in replacing a molding machine with a new

improved model. The old machine has a salvage value of $10,000 now and a predicted

salvage value of $4,000 in six years, if rebuilt. If the old machine is kept, it must be

rebuilt in one year at a predicted cost of $20,000.

The new machine costs $80,000 and has a predicted salvage value of $12,000 at the end

of six years. If purchased, the new machine will allow cash savings of $20,000 for each

of the first three years, and $10,000 for each year of its remaining six-year life.

Required:

What is the net present value of purchasing the new machine if the company has a

required rate of return of 14%?

31) How does cost-based transfer price method help managers to determine transfer

prices?

32) Neon Company manufactured 2,500 units during April with a total overhead budget

of $55,000. However, while manufacturing the 2,500 units the microcomputer that

contained the month’s cost information broke down. With the computer out of

commission, the accountant has been unable to complete the variance analysis report.

The information missing from the report is lettered in the following set of data:

Variable overhead:

Standard cost per unit: 1.2 labor hour at $10 per hour

Actual costs: $26,250 for 2,250 hours

Flexible budget: a

Total flexible-budget variance: b

Variable overhead spending variance: c

Variable overhead efficiency variance: d

Fixed overhead:

Budgeted costs: e

Actual costs: f

Flexible-budget variance: $200 favorable

Required:

Compute the missing elements in the report represented by the lettered items.

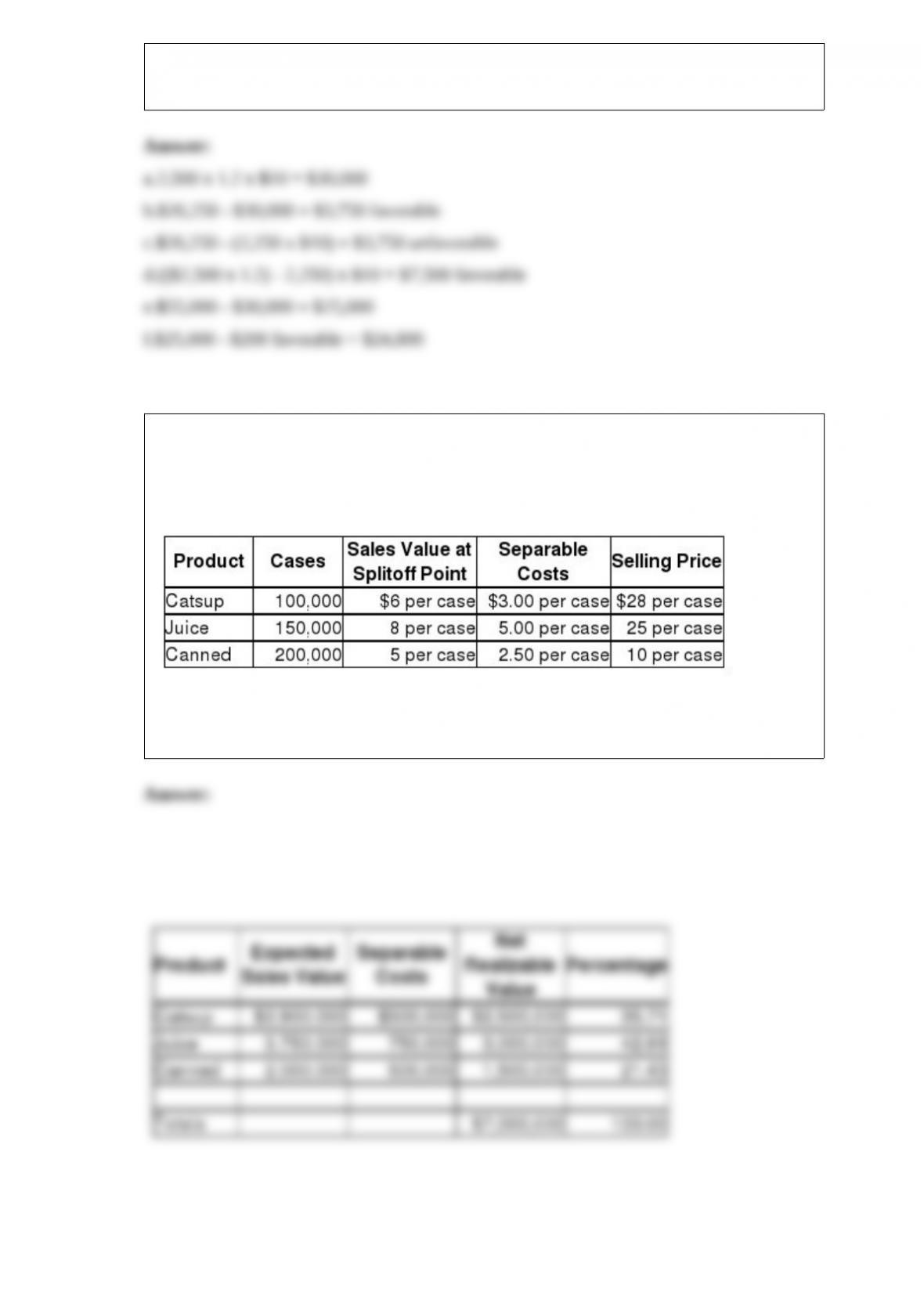

33) Red Sauce Canning Company processes tomatoes into catsup, tomato juice, and

canned tomatoes. During the summer of 20X5, the joint costs of processing the

tomatoes were $420,000. There was no beginning or ending inventories for the summer.

Production and sales value information for the summer is as follows:

Required:

Determine the amount allocated to each product if the estimated net realizable value

method is used, and compute the cost per case for each product.

34) What are the implications of JIT and backflush costing systems for activity-based

costing (ABC) systems?