Archives

978-0134065823 Chapter 1 Solution Manual Part 1

Copyright © 2017 Pearson Education, Inc. Chapter 1 The Demand for Audit and Other Assurance Services Concept Checks P. 8 1. To do an audit, there must be information in a verifiable form and some standards (criteria) by which […]

978-0134065823 Chapter 1 Solution Manual Part 2

1-8 1-17 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The services provided by Consumers Union and assurance services provided by CPA firms are designed to improve the quality of information […]

978-0134065823 Chapter 10 Solution Manual Part 1

10-1 Chapter 10 Assessing and Responding to Fraud Risks Concept Checks P. 311 1. The three conditions of fraud referred to as the “fraud triangle” are (1) Incentives/Pressures; (2) Opportunities; and (3) Attitudes/Rationalization. Incentives/Pressures are incentives of management or […]

978-0134065823 Chapter 10 Solution Manual Part 2

10–11 10-26 (continued) whether an audit performed in accordance with auditing standards should have uncovered the fraud. The auditor is not required to search for immaterial fraudulent transactions; however, the auditor is required to follow up when one is discovered. […]

978-0134065823 Chapter 10 Solution Manual Part 3

10–21 10-34 (continued) 7. a. Sales may be fictitiously recorded before any goods were shipped. b. Sales and accounts receivable. c. Recorded amounts meet the criteria for revenue recognition (occurrence). 8. a. Fictitious sales transactions may have been entered to […]

978-0134065823 Chapter 11 Solution Manual Part 1

11-1 Chapter 11 Internal Control and COSO Framework Concept Checks P. 339 1. Management typically has three broad objectives in designing effective internal controls. 1. Reliability of Reporting While this objective relates to both external and internal reporting, we […]

978-0134065823 Chapter 11 Solution Manual Part 2

11–11 Copyright © 2017 Pearson Education, Inc. 11–25 1. a. Adequate documents and records, and independent checks on performance. b. Transactions are recorded on the correct dates (cutoff). c. Carefully coordinate the physical count of inventory on the 2. a. […]

978-0134065823 Chapter 12 Solution Manual Part 1

12-1 Chapter 12 Assessing Control Risk and Reporting on Internal Controls Concept Checks P. 381 1. As illustrated by Figure 12–1, there are four phases in the process of understanding internal control and assessing control risk. In the first phase […]

978-0134065823 Chapter 12 Solution Manual Part 2

12-11 12–21 (continued) system. She must obtain an understanding of internal control to determine whether it is possible to conduct an audit at all. Auditing standards require, at a minimum, an understanding of internal control. The auditor must understand the […]

978-0134065823 Chapter 12 Solution Manual Part 3

12-21 12–28 (continued) 4. Access the client’s electronic inventory master file and list all items or parts of which the quantity on hand seems excessive in relation to quantity used or sold during the year. This list provides data for […]

978-0134065823 Chapter 12 Solution Manual Part 4

12-31 12–35 (continued) Establish standardized programming procedures and have Melinda review changed programs for compliance with those procedures. Melinda should reconcile the Job Processed Log to the job schedule developed by her.Melinda should assign or at least approve […]

978-0134065823 Chapter 13 Solution Manual Part 1

13-1 Chapter 13 Overall Audit Strategy and Audit Program Concept Checks P. 419 1. The five types of tests auditors use to determine whether financial statements are fairly stated include the following: Risk assessment procedures Tests of […]

978-0134065823 Chapter 13 Solution Manual Part 2

Copyright © 2017 Pearson Education, Inc. 13–26 a. TRANSACTION–RELATED AUDIT OBJECTIVE b. TEST OF CONTROL PROCEDURE c. SUBSTANTIVE TEST 1. Recorded transactions exist, recorded transactions are stated at the correct amounts, and transactions are properly classified. (Occurrence, Accuracy, and Classification) […]

978-0134065823 Chapter 13 Solution Manual Part 3

13–17 13–32 (continued) Parts 7, 9, and 1 are all a part of planning and are therefore done early. These are in the sequence shown in Chapter 8. As part of planning the audit, the auditor obtains an understanding of […]

978-0134065823 Chapter 14 Solution Manual Part 1

14-1 Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Concept Checks P. 452 1. a. The customer order is a request from the customer indicating the quantity and the description […]

978-0134065823 Chapter 14 Solution Manual Part 2

14–11 14–23 (continued) 4. a. Online sales are recorded in the sales system (Completeness). b. Review online sales system documentation and make inquiries of client personnel to determine that the automatic interface is a part of the system design. Enter […]

978-0134065823 Chapter 14 Solution Manual Part 3

14–21 14–30 POSSIBLE ERROR OR FRAUD CONTROL 1. Customer checks are properly credited to customer accounts and are properly deposited, but errors are made in recording receipts in the cash receipts journal. g. An employee, other than the bookkeeper, periodically […]

978-0134065823 Chapter 14 Solution Manual Part 4

14–30 14–34 (continued) d. TRANSACTION– RELATED AUDIT OBJECTIVE SUBSTANTIVE TEST OF TRANSACTIONS AUDIT PROCEDURES 1. Recorded sales occurred. Select a sample of sales from sales journal and examine customer’s purchase order, sales order form, and bill of lading to determine […]

978-0134065823 Chapter 15 Solution Manual Part 1

15-1 Chapter 15 Audit Sampling for Tests of Controls and Substantive Tests of Transactions Concept Checks P. 489 1. A representative sample is one in which the characteristics of interest for the sample are approximately the same as for […]

978-0134065823 Chapter 15 Solution Manual Part 2

15-11 15–28 (continued) 2. Test time delay between warehouse removal slip date and billing date for timeliness of billing. (Timing) 3. Trace entries into perpetual inventory records to determine that inventory is properly relieved for shipments. (Posting and summarization) e. […]

978-0134065823 Chapter 15 Solution Manual Part 3

15-20 15–34 (continued) INVOICE NUMBER EXCEPTION ANALYSIS 6810 Confirm the account balances to the customers; examine the reduction in the perpetual inventory records. 7625 Trace the amount to the sales journal and accounts receivable master file; examine the shipping document […]

978-0134065823 Chapter 16 Solution Manual Part 1

16-1 Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Concept Checks P. 537 1. Auditors perform substantive analytical procedures for the entire sales and collection cycle, including accounts receivable. This is necessary because of […]

978-0134065823 Chapter 16 Solution Manual Part 2

16–11 16–17 (continued) of controls based upon the selection of the significant controls. The auditor would then perform the tests of the significant controls to determine the effectiveness ofthe controls and to plan the substantive tests that are necessary based […]

978-0134065823 Chapter 16 Solution Manual Part 3

16–21 16–30 (continued) d. When no response is received to the second request for positive confirmation, the auditor should use alternative procedures. These normally include examination of the customer’s remittance advice and related cash receipt. This is often a simple […]

978-0134065823 Chapter 16 Solution Manual Part 4

16–28 16–36 (continued) c. The auditor would likely deem that the risks of material misstatement related to all of the transaction–related audit objective for sales and cash receipts transactions as significant risks due to the deficiencies in internal control and […]

978-0134065823 Chapter 17 Solution Manual Part 1

17-1 Chapter 17 Audit Sampling for Tests of Details of Balances Concept Checks P. 575 1. The steps in nonstatistical sampling for tests of details of balances and for tests of controls are almost identical, as illustrated in the […]

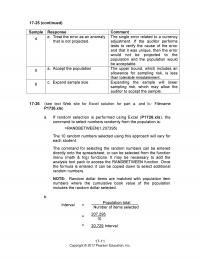

978-0134065823 Chapter 17 Solution Manual Part 2

17–11 17–25 (continued) Sample Response Comment 4 e. Treat the error as an anomaly that is not projected. The single error related to a currency adjustment. If the auditor performs tests to verify the cause of the error and that […]

978-0134065823 Chapter 17 Solution Manual Part 3

17–31 (continued) b. Determination of ARIA – Note that there are many ways to estimate ARIA. One method is as follows: ARIA = AAR / (IR x CR x APR) = .05 / [1.0 x .8 x (1 – .6)] […]

978-0134065823 Chapter 18 Solution Manual Part 1

18-1 Chapter 18 Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable Concept Checks P. 616 1. There are several balance sheet and income statement accounts related to the acquisition and […]

978-0134065823 Chapter 18 Solution Manual Part 2

Copyright © 2017 Pearson Education, Inc. 18–20 AUDIT PROCEDURE a. TYPE OF EVIDENCE b. TRANSACTION AUDIT OBJECTIVE c. TEST OF CONTROL OR SUBSTANTIVE TEST OF TRANSACTION 1.a. Inspection Recorded acquisitions and payments are for goods and services received, consistent with […]

978-0134065823 Chapter 18 Solution Manual Part 3

Copyright © 2017 Pearson Education, Inc. 18–24 (continued) MISSTATEMENT a. TRANSACTION– RELATED AUDIT OBJECTIVE NOT MET b. PREVENTIVE CONTROL c. SUBSTANTIVE PROCEDURE 4 Acquisition transactions are properly classified (classification). Account distributions are reviewed by a responsible individual prior to entry […]

978-0134065823 Chapter 18 Solution Manual Part 4

Copyright © 2017 Pearson Education, Inc. 18–28 (continued) a. BERGERON INTERNAL CONTROLS b. TRANSACTION– RELATED AUDIT OBJECTIVE(S) c. TEST OF CONTROLS 11. Controller reconciles on a monthly basis the accounts payable listing to the accounts payable general ledger account. Controller […]

978-0134065823 Chapter 19 Solution Manual Part 1

19-1 Chapter 19 Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts Concept Checks P. 645 1. The reason for the emphasis on current period acquisitions in auditing property, plant, and equipment is that there […]

978-0134065823 Chapter 19 Solution Manual Part 2

19–11 19–25 a. Both U.S. GAAP and IFRS standards generally contain similar requirements for assessing the impairment of assets, including goodwill. Both standards require the testing of goodwill for impairment at least annually, or more frequently if there are indications […]

978-0134065823 Chapter 19 Solution Manual Part 3

19–17 19–27 (continued) 4. The paving and fencing are land improvements and should be depreciated over their useful lives. Land improvements (may be $50,000 combined with buildings account — buildings and improvements) Land $50,000 To correct initial recording of paving […]

978-0134065823 Chapter 2 Solution Manual

2-1 Chapter 2 The CPA Profession Concept Checks P. 28 1. The four major services that CPAs provide are: a. Audit and assurance services Assurance services are independent professional services that improve the quality of information for decision makers. […]

978-0134065823 Chapter 20 Solution Manual Part 1

20-1 Chapter 20 Audit of the Payroll and Personnel Cycle Concept Checks P. 666 1. Transactions for the payroll and personnel cycle are generally far more significant than for payroll–related balance sheet accounts because entities pay payroll related expenses […]

978-0134065823 Chapter 20 Solution Manual Part 2

20–24 A flowchart of steps for each type of test is given below (requirements a., b., and c.): TESTS OF CONTROLS OR SUBSTANTIVE TESTS OF TRANSACTIONS TESTS OF DETAILS OF BALANCES 5 4 2 7 9 8 6 3 1 […]

978-0134065823 Chapter 21 Solution Manual Part 1

21-1 Chapter 21 Audit of the Inventory and Warehousing Cycle Concept Checks P. 694 1. Inventory is often the most difficult and time consuming part of many audit engagements because: 1. Inventory is generally a major item on the […]

978-0134065823 Chapter 21 Solution Manual Part 2

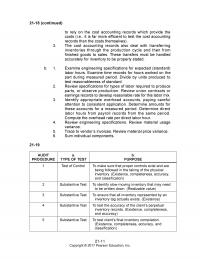

21–11 21–18 (continued) to rely on the cost accounting records which provide the costs (i.e., it is far more efficient to test the cost accounting records than the costs themselves). 3. The cost accounting records also deal with transferring inventories […]

978-0134065823 Chapter 21 Solution Manual Part 3

21–25 (continued) CLIENT a. ISSUES TO CONSIDER b. LOCATIONS TO VISIT c. POTENTIAL RISKS OF MATERIAL MISSTATEMENT d. AUDITOR RESPONSES TO RISKS 4. Food Giant Three–fourths of the inventory balance is located at the five independent storage warehouses. There is […]

978-0134065823 Chapter 22 Solution Manual Part 1

22-1 Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Concept Checks P. 720 1. The characteristics of the liability accounts in the capital acquisition and repayment cycle that result in a different auditing approach than the approach […]

978-0134065823 Chapter 22 Solution Manual Part 2

22–11 22–23 (continued) c. Procedure 2 is not necessary in light of procedure 3. They both perform the same function and the confirmation is from an independent source. The sample sizes for the procedures are probably appropriate, considering the deficiencies […]

978-0134065823 Chapter 23 Solution Manual Part 1

23-1 Chapter 23 Audit of Cash and Financial Instruments Concept Checks P. 748 1. The appropriate tests for the ending balance in the cash accounts depend heavily on the initial assessment of control risk, tests of controls, and substantive […]

978-0134065823 Chapter 23 Solution Manual Part 2

23-11 23–19 (continued) c. RECONCILING ITEM AUDIT PROCEDURE 1. Deposits in transit Trace to duplicate deposit slip and entry on cutoff bank statement. 2. Erroneous check Examine correction notice in August charge received from bank. 3. Outstanding checks Obtain cutoff […]

978-0134065823 Chapter 24 Solution Manual Part 1

24-1 Chapter 24 Completing the Audit Concept Checks P. 776 1. The auditor is particularly concerned with whether management has disclosed all required information (completeness objective for presentation and disclosure). Auditors often use a disclosure checklist to determine that […]

978-0134065823 Chapter 24 Solution Manual Part 2

24–11 24–22 (continued) d. The search for unknown commitments is typically performed as part of individual audit areas. Three examples of procedures Johnson is likely to perform for the purpose of uncovering commitments are: As part of the audit […]

978-0134065823 Chapter 25 Solution Manual Part 1

25-1 Chapter 25 Other Assurance Services Concept Checks P. 807 1. Preparation is defined in SSARS as a service where the CPA is engaged by the client to prepare or assist in preparing financial statements, but the CPA does […]

978-0134065823 Chapter 25 Solution Manual Part 2

25-11 25–24 (continued) d. Additional procedures should be performed when the accountant believes, based on the information obtained through inquiry and analytical procedures, that the financial statements may be materially misstated. Examples where this could be the case are: ■ […]

978-0134065823 Chapter 26 Solution Manual Part 1

26-1 Chapter 26 Internal and Governmental Financial Auditing and Operational Auditing Concept Checks P. 832 1. Internal auditors who perform financial auditing are responsible for evaluating whether their company’s internal controls are designed and operating effectively and whether the […]

978-0134065823 Chapter 26 Solution Manual Part 2

26-9 26–21 (continued) c. The following certifications are available: 1. CIA (Certified Internal Auditor) 2. CCSA (Certification in Control Self–Assessment) 3. CFSA (Certified Financial Services Auditor) 4. CGAP (Certified Government Auditing Professional) 5. CRMA (Certification in Risk Management Assurance) 6. […]

978-0134065823 Chapter 3 Solution Manual Part 1

3-1 Chapter 3 Audit Reports Concept Checks P. 57 1. The standard unmodified opinion audit report for a nonpublic entity contains the following eight parts: 1. Report title: Auditing standards require that the report be titled and that the […]

978-0134065823 Chapter 3 Solution Manual Part 2

3-11 3–24 (continued) 6. There is no separate scope paragraph that describes what an audit is. 7. The audit was made in accordance with auditing standards generally accepted in the United States of America rather than generally accepted accounting standards. […]

978-0134065823 Chapter 4 Solution Manual Part 1

4-1 Chapter 4 Professional Ethics Concept Checks P. 85 1. The following is the six-step approach to resolving an ethical dilemma: 1. Obtain the relevant facts. 2. Identify the ethical issues from the facts. 3. Determine who is affected […]

978-0134065823 Chapter 4 Solution Manual Part 2

4-24 (continued) (a) POTENTIAL THREATS TO INDEPENDENCE (b) POSSIBLE SAFEGUARDS? (c) RULES OF CONDUCT VIOLATED? (d) APPROPRIATE ACTION? 1. The ability to purchase a car at a substantial discount due to Marie’s long-standing audit service may cause Marie to be […]

978-0134065823 Chapter 4 Solution Manual Part 3

4-17 4-27 (continued) c. Section 1.320.030.03 indicates that new legislation or evolution of a new form of business transaction are examples of unusual circumstances that may justify a departure from the Accounting Principles Rule. An unusual degree of materiality and […]

978-0134065823 Chapter 5 Solution Manual Part 1

5-1 Chapter 5 Legal Liability Concept Checks P. 118 1. Several factors that have affected the increased number of lawsuits against CPAs are: The growing awareness of the responsibilities of public accountants on the part of users of […]

978-0134065823 Chapter 5 Solution Manual Part 2

5-8 5–19 (continued) 3. Given that the auditors were able to satisfy themselves through alternative procedures that the inventory existed as of the end of the year, their behavior in this instance would be considered nonnegligent. 4. The facts in […]

978-0134065823 Chapter 6 Solution Manual Part 1

6-1 Chapter 6 Audit Responsibilities and Objectives Concept Checks P. 152 1. It is management’s responsibility to adopt sound accounting policies, maintain adequate internal control, and make fair representations in the financial statements. The auditor’s responsibility is to conduct […]

978-0134065823 Chapter 6 Solution Manual Part 2

6-11 6–26 (continued) The auditor normally assesses the likelihood of material misappropriation of assets as a part of understanding the entity’s internal control and assessing control risk. Audit evidence should be expanded when the auditor finds an absence of adequate […]

978-0134065823 Chapter 7 Solution Manual Part 1

7-1 Chapter 7 Audit Evidence Concept Checks P. 192 1. Following are six characteristics that determine reliability of evidence and an example of each. FACTOR DETERMINING RELIABILITY EXAMPLE OF RELIABLE EVIDENCE Independence of provider Confirmation of a bank balance […]

978-0134065823 Chapter 7 Solution Manual Part 2

7-27 (continued) ACCOUNT NAME FROM WHOM CONFIRMED INFORMATION TO BE CONFIRMED NOTES RECEIVABLE A selected sample of notes receivable outstanding at the balance sheet date. If a note receivable was written off during the year, the balance written off should […]

978-0134065823 Chapter 7 Solution Manual Part 3

7-35 Here are expected values for each account except sales and the calculated difference between the expected value and actual recorded balance: ACCOUNT EXPECTED VALUE DIFFERENCE IN EXPECTED AND RECORDED REASONING TO SUPPORT EXPECTED VALUE Executive salaries $563,348 ($546,940 x […]

978-0134065823 Chapter 8 Solution Manual Part 1

8-1 Chapter 8 Audit Planning and Materiality Concept Checks P. 234 1. The eight major steps in planning audits are: 1. Accept client and perform initial planning 2. Understand the client’s business and industry 3. Perform preliminary analytical procedures […]

978-0134065823 Chapter 8 Solution Manual Part 2

8-11 Discussion Questions And Problems 8–29 AUDIT ACTIVITIES RELATED PLANNING PROCEDURE 1. Review accounting principles unique to the client’s industry. (2) Understand the client’s business and industry 2. Determine the likely users of the financial statements. (1) Accept client […]

978-0134065823 Chapter 8 Solution Manual Part 3

8-21 8–38 (continued) d. By allocating 75% of the preliminary estimate to accounts receivable, inventories, and accounts payable, there is far less materiality to be allocated to all other accounts. Given the total dollar value of those accounts, this may […]

978-0134065823 Chapter 8 Solution Manual Part 4

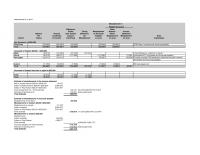

8-28 8-40 (continued) (part of requirement e.) Pinnacle Manufacturing Company Income Statement – Welburn Division For the Year Ended December 31 2016 $ Value 2016 % of Div. Sales 2015 $ Value 2015 % of Div. Sales 2014 $ Value […]

978-0134065823 Chapter 9 Solution Manual Part 1

9-1 Chapter 9 Assessing the Risk of Material Misstatement Concept Checks P. 268 1. The risk of material misstatement exists at two levels: the overall financial statement level and at the assertion level for classes of transactions, account balances, […]

978-0134065823 Chapter 9 Solution Manual Part 2

9-11 9–30 (continued) assessment, the auditor should revise the risk assessment and modify planned audit procedures or perform additional procedures in response to the revised risk assessments. 9–31 a. Several of the recent developments at Highland Bank and Trust may […]

978-0134065823 Chapter 9 Solution Manual Part 3

9-20 9–39 (continued) Bank Loan Payable It seems somewhat strange for the Company to have an outstanding balance on its bank loan payable at the end of 2016 given its excellent operating results. This may be attributable to the growth […]

978-0134065823 P1237 Excel

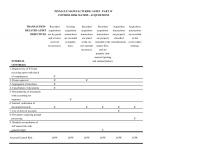

PINNACLE MANUFACTURING AUDIT – PART IV CONTROL RISK MATRIX – ACQUISITIONS TRANSACTION- Recorded Existing Recorded Recorded Acquisition Acquisition RELATED AUDIT acquisitions acquisition acquisition acquisition transactions transactions OBJECTIVES are for goods transactions transactions transactions are properly are recorded and services are […]

978-0134065823 P1435a Excel

# a. Key Internal Control b. Transaction Related Audit Objectives c. Test of Control d. Substantive Test of Transaction 1. Segregation of the purchasing, receiving, and cash disbursements functions. Recorded acquisitions are for goods and services actually received (occurrence). Discuss […]

978-0134065823 P1435b Excel

Acquisitions Substantive Tests of Transactions More than one audit procedure is listed for certain objectives even though the requirement is for only one procedure. Transaction-Related Audit Objective Substantive Audit Procedures Occurrence Compare prices on vendor invoices with approved price limits […]

978-0134065823 P1527 Excel

PROBLEM 15-27 GENERATION OF RANDOM SAMPLES SALES BILL OF INVOICE LADING CUSTOMER RANGE 1 – 18221 – Pg. 1-20 8274 29427 Ln. 1-50 SAMPLE ITEM 13975 24066 7 – 8 26585 18874 18 –17 31306 28176 6 – 38 4792 […]

978-0134065823 P1528 Excel

PROBLEM 15-28 COMPUTER GENERATION OF RANDOM NUMBERS Illustration of first 10 sample items: 33394 19128 17152 25100 14682 12481 13824 17406 22138 30950

978-0134065823 P1537 Excel

Client: Pinnacle Manufacturing Audit Area: Tests of Controls and Substantive Test of Transactions–Acquisitions. Define the Objective(s): Examine vendors’ invoices, receiving reports, purchase orders, and other related documents to determine whether the system has functioned as intended and as described in […]

978-0134065823 P1637 Excel

requirements d, e, and f Misstatement in Related Accounts Difference: Other Books Timing Misstatement Balance Income Balance Amount Over (Under) Difference: in Accounts Sheet Statement Per Confirmed Amount No Payable Misstatement Misstatement Brief Vendor Books by Vendor Confirmed Misstatement o/s […]

978-0134065823 P1724 Excel

Recorded Confirmation Value Response Misstatement Acct. 147 24,692$ 22,486$ 2,206$ Pricing error Acct. 228 183,219 157,216 26,003 Cutoff error Acct. 278 7,546 5,546 – Timing difference Acct. 497 15,319 – – Timing difference Acct. 564 8,397 7,858 539 Error in […]

978-0134065823 P1726 Excel

PROBLEM 17-26 COMPUTER GENERATION OF RANDOM NUMBERS Selection of 10 sample items: 204229 153774 189978 120315 140353 85371 68657 196629 105030 78612 PROBLEM 17-26 SYSTEMATIC SELECTION OF NUMBERS Population 207295 Sample size 10 Start = 1857 11857 222,586 343,315 464,044 […]

978-0134065823 P1727 Excel

1 $2,728.00 $2,498.00 $230.00 0.084 3 3,890.00 1,190.00 2,700.00 0.694 4 815.00 785.00 30.00 0.037 6 3,215.00 3,190.00 25.00 0.008 Totals $10,648.00 $7,663.00 $2,985.00 (a) (b) ( c = a x b) (d) (e = c x d) TAINTING INTERVAL […]

978-0134065823 P1730 Excel

STATISTICAL CALCULATIONS – INVENTORY SAMPLE ITEM VALUES: Misstatement Item Audit Book Misstatement Amount No. Value Value Amount Squared 1 812.50 740.50 -72.00 5184.00 2 12.50 78.20 65.70 4316.49 3 10.00 51.10 41.10 1689.21 4 25.40 61.50 36.10 1303.21 5 600.10 […]

978-0134065823 P1731 Excel

SOLUTION TO CASE 17-31 Note: The random numbers in column C were set using the RANDBETWEEN function. Because the numbers change, the original formulas no longer appear on this file. GENERATION ORDER ASCENDING ORDER Sample Dollar Sample Dollar Item No. […]

978-0134065823 P1732 Excel

NONSTATISTICAL SAMPLING EVALUATION WORKSHEET CLIENT AND YEAR-END: Danforth Paper Company PREPARED BY AND DATE: REVIEWED BY AND DATE: A/R RECORDED BALANCE: $2,760,000 RECORDED BALANCE OF ACCOUNTS AUDITED 100% $465,000 RECORDED BALANCE OF ACCOUNTS TO BE SAMPLED: $2,295,000 TOLERABLE MISSTATEMENT $100,000 […]

978-0134065823 P1830 Excel

WARD PUBLISHING COMPANY SECTION V – ATTRIBUTES SAMPLING TABLES SAMPLING DATA SHEET TO DETERMINE SAMPLE SIZE USING A 5 PERCENT ARO Planned Audit Actual Results TER Initial EPER 2345678910 Sample Sample Excep– Exception ——– — — — — — — […]

978-0134065823 P2126 Excel

ALADDIN PRODUCTS SUPPLY COMPANY RATIO CALCULATIONS Part a. DATA ENTRY AREA: 2016 2015 2014 2013 Sales 92,800,000 86,800,000 78,400,000 69,600,000 Cost of sales 68,400,000 67,200,000 60,800,000 54,000,000 Beginning inventory 9,200,000 8,400,000 7,600,000 6,000,000 Ending inventory 11,600,000 9,200,000 8,400,000 7,600,000 RESULTS […]

978-0134065823 P2130 Excel

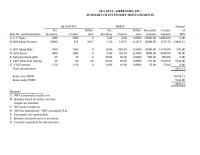

SEA GULL AIRFRAMES, INC. SUMMARY OF INVENTORY MISSTATEMENTS QUANTITY PRICE Amount Per Differ- Per Differ- Recorded Correct of Item No. and Description Inventory Correct ence Inventory Correct ence Amount Amount M/S A. L37 Spars 3000 3000 0 8.00 8.00 0.0000 […]

978-0134065823 P2429 Excel

Item Total Amount Current Assets Noncurrent Assets Current Liabilities Noncurrent Liabilities Income Before Tax 1 125000 (125,000) 125,000 2 85,000 (85,000) 60,000 (25,000) 3 44,000 (44,000) (44,000) 4 52,000 52,000 52,000 5 43,000 0 6 Not known 0 0 (129,000) […]

978-0134065823 P735 Excel

MOREHEAD TECHNOLOGIES ANALYTICAL PROCEDURES Audited Balance Preliminary Balance Difference in expected Account 10/31/2015 10/31/2016 Expected Value recorded amounts Reasoning for Expected Value Sales 51,316,234 57,474,182 Executive salaries 546,940 615,970 563,348 -9.34% Executives received 3% raise November 1, 2015. Factory hourly […]

978-0134065823 P737 Excel

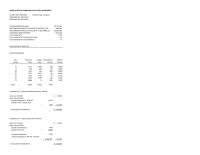

VANDERVOORT COMPANY Schedule N-1 Date A/C #110 – NOTES RECEIVABLE Prepared by JD 01/21/17 12/31/16 Approved by PP 02/15/17 Account #110 – Notes Receivable Interest Date Interest Made/ Rate/ Face Value of Balance Balance Receivable Receivable Maker Due Date Paid […]

978-0134065823 P832 Excel

2016 2015 2014 2013 Sales (000) 14,211$ 12,916$ 11,462$ 10,351$ Cost of sales (000) 9,223 8,266 7,313 6,573 Gross margin 4,988$ 4,650$ 4,149$ 3,778$ Percent 35.1% 36.0% 36.2% 36.5% Drug Nondrug Drug Nondrug Industry Sales Sales COS COS GM 2016 […]

978-0134065823 P939a Excel

Stanton Enterprises Worksheet 9-39A Determination of Materiality and Allocation to the Accounts 12/31/2016 DETERMINATION OF MATERIALITY: Income before taxes $8,004,277 Possible adustments – estimated. See Worksheet 9-39B: Increase allowance for uncollectible accounts (220,000) Increase to equal same % of trade […]

978-0134065823 P939b Excel

Stanton Enterprises Worksheet 9-39B Analysis of Financial Statements and Audit Planning Worksheet 12/31/2016 BALANCE SHEET Preliminary Audited % 12/31/16 % 12/31/15 %Change Cash $243,689 1.4 $133,981 1.1 81.9 Trade accounts receivable 3,544,009 19.7 2,224,921 17.7 59.3 Allowance for uncollectible accounts […]

AC 28268

When communicating with the audit committee and management, A) only material fraud and illegal acts are required by auditing standards to be communicated. B) all internal control deficiencies are required by auditing standards to be communicated. C) the communications should […]

AC 34107

Extensive professional development is necessary for auditors doing governmental audits. In process cost systems, costs are accumulated by individual jobs. Answer: FALSE The auditor must perform substantive tests related to assertions deemed to have significant risks. Answer: TRUE Because of […]

AC 50854

While there is no professional requirement to do so on audit engagements, CPAs frequently issue a formal “management” letter to clients. The primary purpose of this letter is to provide A) evidence indicating whether the auditor is reasonably certain that […]

AC 78893

A high detection risk equates to a low amount of audit evidence needed. CPA firms are required to be independent when performing any professional service. Answer: FALSE For each significant internal control deficiency identified by the auditor, he or she […]

AC 83164

The last paragraph of the accountant’s review report A) details the responsibilities of management. B) details the responsibilities of the accountant. C) expresses limited assurance in the form of negative assurance. D) lists the analytical procedures performed. Audit procedures designed […]

AC 84238

Professional skepticism must be maintained only if the auditor suspects fraud. Auditors use trends in the accounts receivable turnover ratio to assess the reasonableness of the company’s credit policies. Answer: FALSE Section 404 of the Sarbanes-Oxley Act requires public companies […]

Acc 26913

When errors are found in a sample, auditors in practice generally make the assumption A) that the population errors cannot be determined. B) that the population errors are larger than the sample errors. C) that the population errors are smaller […]

ACC 27725

Staff assigned to an audit engagement must be knowledgeable about the client’s industry. Current professional standards prohibit accountants from performing engagements to review forecasts or projections. Answer: TRUE It is common to use a combination of positive and negative confirmations […]

Acc 27782

Current professional auditing standards require the performance of analytical procedures during the planning and completion phases of the audit. Depreciation amounts are determined by exchange transactions with outside parties. Answer: FALSE International Standards on Auditing are issued by the International […]

ACC 48333

Which of the following is not a term related to evaluating results in audit sampling until after a sample is tested and evaluated? A) sample exception rate B) estimated population exception rate C) computed upper exception rate D) exception Some […]

ACC 54373

The auditors ultimate substantive tests depend on the relative effectiveness of internal controls related to accounts payable. For sales, the completeness transaction-related audit objective affects the existence balance-related audit objective. Answer: FALSE Auditors seldom expect to find misstatements when testing […]

ACC 60730

To determine if significant internal control deficiencies are material weaknesses, they must be evaluated on their A) B) C) D) Which of the following includes all payroll transactions processed by the accounting system for a given period of time? A) […]

Acc 64373

Significant risks often relate to routine transactions. Significant changes in the industry may increase the risk of material misstatement at the assertion level. Answer: FALSE The cash account is not part of the acquisitions and payment cycle. Answer: FALSE To […]

Acc 70608

Substantive analytical procedures performed during the testing phase of the audit A) are required under generally accepted auditing standards. B) are always done independently from other audit procedures. C) are used as a substantive test in support of account balances. […]

Acc 76789

Which of the following is a true statement regarding CPAs’ liability? A) The amounts assessed under joint and several liability will not differ significantly from the amounts assessed under separate and proportionate liability. B) When lawsuits are brought under the […]

ACC 82513

Both SEC rules and the Sarbanes-Oxley Act prohibit auditors from providing bookkeeping services to their public company audit clients. All owners of a CPA firm must be CPAs who are qualified to practice. Answer: FALSE[/cpmembership] Errors are usually more difficult […]

ACC 86947

The letter of representation obtained from an audit client should be A) dated as of the end of the period under audit. B) dated as of the audit report date. C) dated as of any date decided upon by the […]

Acc 91836

A type of positive confirmation known as a blank confirmation A) requests the recipient to fill in the amount of the balance. B) is considered less reliable than the regular positive confirmation. C) generates as high a response rate as […]

ACC 95604

The sum of the tolerable exception rate and the estimated population exception rate is the precision of the initial sample estimate. Operational audits are often categorized as functional, organizational, or special assignments. Answer: TRUE Subsequent events represent events that occasionally […]

ACC 96926

A major consideration in audit staffing is the need for continuity from year to year. As the impact from noncompliance is further removed from affecting the financial statements, the less likely the auditor is to become aware of or recognize […]

Accounting 58765

The computer file used for recording payroll transactions for each employee and maintaining total wages paid for the year to date is the A) payroll transaction file. B) payroll master file. C) payroll bank account reconciliation. D) payroll tax returns. […]

Accounting 62464

The risk of material misstatement refers to A) control risk and acceptable audit risk. B) inherent risk. C) the combination of inherent risk and control risk. D) inherent risk and audit risk. Which of the following services is not prohibited […]

Accounting Chapter 1 Which of the following can be used as a criteria for evaluating

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 1 The Demand for Audit and Other Assurance Services 1.1 Learning Objective 1-1 1) In the auditing process A) the types and amounts of evidence remain constant […]

Accounting Chapter 10 Ineffective Board Director Audit Committee Oversight Over financial

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 10 Fraud Auditing 10.1 Learning Objective 10-1 1) Which of the following best defines fraud in a financial statement auditing context? A) Fraud is an unintentional misstatement […]

Accounting Chapter 10 the auditor should obtain an understanding of the internal

Copyright © 2017 Pearson Education, Inc. 17) For significant risks, including fraud risks, the auditor should obtain an understanding of the internal controls related to the risks. Answer: TRUE Terms: Significant risk Diff: Moderate Objective: LO 10-3 AACSB: Reflective thinking […]

Accounting Chapter 11 Control activities are a subcomponent of the information and communication

Copyright © 2017 Pearson Education, Inc. 30) Control activities are a subcomponent of the information and communication component of internal control. Answer: FALSE Terms: Internal control components Diff: Easy Objective: LO 11-3 AACSB: Reflective thinking 31) Adequate documents and records […]

Accounting Chapter 11 Which of the following is not one of the three primary objectives of effective

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 11 Internal Control and COSO Framework 11.1 Learning Objective 11-1 1) Which of the following is not one of the three primary objectives of effective internal control? […]

Accounting Chapter 12 A narrative should describe the disposition of every document and record

Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 12 Assessing Control Risk and Reporting on Internal Controls 12.1 Learning Objective 12-1 1) When the auditor attempts to understand the operation of the accounting system by tracing a few transactions through the […]

Accounting Chapter 12 If When Obtaining Understanding Control Activities Relatively

Copyright © 2017 Pearson Education, Inc. 9) When a client uses a service center for processing transactions, A) the auditor can assume that the controls are adequate because it is an independent enterprise. B) auditing standards require the auditor to […]

Accounting Chapter 13 Tests of controls provide evidence about the likelihood for misstatements

Copyright © 2017 Pearson Education, Inc. 23) Tests of controls provide evidence about the likelihood for misstatements in a client’s financial statements. Answer: TRUE Terms: Tests of controls; Misstatements in client’s financial statements Diff: Easy Objective: LO 13-2 AACSB: Reflective […]

Accounting Chapter 13 Which of the following further audit procedures are used to determine whether

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 13 Overall Audit Strategy and Audit Program 13.1 Learning Objective 13-1 1) Shown below (1 through 5) are the five types of tests which auditors use to […]

Accounting Chapter 14 List Below The Classes of Transactions That You

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions 14.1 Learning Objective 14-1 1) Which of the following is an […]

Accounting Chapter 14 Transaction related Audit Objectives For Credit Memos And

Copyright © 2017 Pearson Education, Inc. 13) In many audits of sales transactions substantive tests of transactions can be reduced in determining the completeness objective because A) understatements of assets and income are a greater concern than overstatements. B) overstatements […]

Accounting Chapter 15 An auditor can increase the likelihood that a sample is representative

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 15 Audit Sampling for Tests of Controls and Substantive Tests of Transactions 15.1 Learning Objective 15-1 1) A sample in which the characteristics of the sample are […]

Accounting Chapter 15 Ter Than For High Ter answer A terms Tolerable

Copyright © 2017 Pearson Education, Inc. 15.5 Learning Objective 15-5 1) The risk which the auditor is willing to take in accepting a control as being effective when the true population exception rate is greater than a tolerable rate is […]

Accounting Chapter 16 For cash receipts, the occurrence transaction-related audit objective

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable 16.1 Learning Objective 16-1 1) The two primary classes of transactions in the sales and […]

Accounting Chapter 16 The net realizable value of accounts receivable is equal to

Copyright © 2017 Pearson Education, Inc. 33) The net realizable value of accounts receivable is equal to: A) gross accounts receivable less allowance for uncollectible accounts. B) gross accounts receivable less bad debt expense. C) gross accounts receivable less returns […]

Accounting Chapter 17 An increased sample size will always cause the population to be accepted

Copyright © 2017 Pearson Education, Inc. 53) An increased sample size will always cause the population to be accepted. Answer: FALSE Terms: Sample size and analyzing exceptions Diff: Moderate Objective: LO 17-2 AACSB: Reflective thinking 54) When using audit sampling […]

Accounting Chapter 17 When selecting a sample size for substantive tests of balances

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 17 Audit Sampling for Tests of Details of Balances 17.1 Learning Objective 17-1 1) Both sampling and nonsampling risks are associated with A) Tests of controls. Substantive […]

Accounting Chapter 18 D terms Accounts Payable Cutoff Physical Inventory Before

Copyright © 2017 Pearson Education, Inc. 31) Discuss the key internal controls that should be present in the processing purchase orders function in the acquisitions and payment cycle. Answer: Proper authorization for acquisitions ensures that the goods and services acquired […]

Accounting Chapter 18 The Personnel The Receiving Department Should Independent

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 18 Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable 18.1 Learning Objective 18-1 1) The overall objective in […]

Accounting Chapter 19 Property, plant, and equipment is normally audited in a different manner

Copyright © 2017 Pearson Education, Inc. 44) Property, plant, and equipment is normally audited in a different manner than current asset accounts. State three reasons why this is so, and discuss the differences in how property, plant, and equipment is […]

Accounting Chapter 19 Which is not one of the tests that would be used in

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 19 Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts 19.1 Learning Objective 19-1 1) Which of the following accounts is not associated […]

Accounting Chapter 2 The legal right to perform audits is granted to a CPA firm

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 2 The CPA Profession 2.1 Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of A) each state. […]

Accounting Chapter 2 Which of the following is a true statement regarding auditing

15 6) Which of the following is a true statement regarding auditing standards? A) Prior to the passage of Sarbanes-Oxley, the FASB established auditing principles for U.S. public companies. B) PCAOB auditing standards are applicable to entities outside the U.S. […]

Accounting Chapter 20 Auditors may extend their tests of payroll in which of the following

Copyright © 2017 Pearson Education, Inc. 26) Auditors may extend their tests of payroll in which of the following circumstances? A) Payroll materially affects the valuation of inventory. The auditor is concerned there may be nonexistent employees on the payroll. […]

Accounting Chapter 20 Which of the following statements about the payroll and personnel cycle

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 20 Audit of the Payroll and Personnel Cycle 20.1 Learning Objective 20-1 1) Which of the following statements about the payroll and personnel cycle is correct? A) […]

Accounting Chapter 21 It is frequently possible to test the physical inventory prior

Copyright © 2017 Pearson Education, Inc. 7) It is frequently possible to test the physical inventory prior to the balance sheet date when A) the perpetual inventory records are accurate and related controls operate effectively. B) year-end sales are small. […]

Accounting Chapter 21 Receipt of ordered materials by the receiving department will generate

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 21 Audit of the Inventory and Warehousing Cycle 21.1 Learning Objective 21-1 1) Receipt of ordered materials by the receiving department will generate the completion of a […]

Accounting Chapter 22 Which of the following owners’ equity transactions usually require

Copyright © 2017 Pearson Education, Inc. 2) Which of the following owners’ equity transactions usually require specific authorization from a company’s board of directors? A) Repurchase of common stock Issuance of common stock Declaration of dividends Yes Yes Yes B) […]

Accounting Chapter 22 Which of the following statements is correct regarding the capital acquisition

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 22 Audit of the Capital Acquisition and Repayment Cycle 22.1 Learning Objective 22-1 1) Which of the following statements is correct regarding the capital acquisition and payment […]

Accounting Chapter 23 A major consideration in the audit of the general cash balance is the

Copyright © 2017 Pearson Education, Inc. 3) A proof of cash represents A) a test of controls and substantive test of transactions. B) a substantive test of transactions. C) a substantive test of transactions and test of details of balances. […]

Accounting Chapter 23 Describe each of the major types of cash accounts maintained by business

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 23 Audit of Cash and Financial Instruments 23.1 Learning Objective 23-1 1) Which of the following is not a “cash equivalent”? A) time deposits B) certificates of […]

Accounting Chapter 24 Accounting Standards Describe Three Levels Likelihood Occurrence

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 24 Completing the Audit 24.1 Learning Objective 24-1 1) Auditors often integrate procedures for presentation and disclosure objectives with A) Tests for transaction-related objectives Tests for balance-related […]

Accounting Chapter 24 Analytic Thinking The Auditors Responsibility With Respect

Copyright © 2017 Pearson Education, Inc. 3) Whenever subsequent events are used to evaluate the amounts included in the statements, care must be taken to distinguish between conditions that existed at the balance sheet date and those that come into […]

Accounting Chapter 24 Which The Following Statements Correct a Letter

Copyright © 2017 Pearson Education, Inc. 14) Which of the following statements is correct? A) A letter of representation is documentation of management’s acceptance of responsibility for the financial statements and is deemed to be reliable evidence. B) A letter […]

Accounting Chapter 25 CPAS Are Attesting The Accuracy The Prospective

Copyright © 2017 Pearson Education, Inc. 13) An agreed-upon procedures engagement is one in which A) the CPA and management agree that procedures will be applied to all accounts and circumstances. B) the CPA and management agree that procedures will […]

Accounting Chapter 25 Typically This Type Statement Used primarily For Management

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 25 Other Assurance Services 25.1 Learning Objective 25-1 1) The standards for preparation, compilation, and review engagements of financial statements are the A) AICPA’s Code of Professional […]

Accounting Chapter 26 False terms International Standards For The Professional Practice

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 26 Internal and Governmental Financial Auditing and Operational Auditing 26.1 Learning Objective 26-1 1) Internal auditors are expected to add value to the organization through improved operational […]

Accounting Chapter 26 Special Assignments Special Assignment Audits Arise The

Copyright © 2017 Pearson Education, Inc. 2) Which of the following is not one of the major differences between financial and operational auditing? A) The financial audit is oriented to the past, but an operational audit concerns performance for the […]

Accounting Chapter 3 Management Discloses The Notes The Financial statements

53 19) Smith and Jones, CPAs, audited the consolidated financial statements of Concord Inc. and all but one of its subsidiaries for the year ended September 30, 2016 and are expressing an unqualified opinion on the financials presented as a […]

Accounting Chapter 3 No reference is made in the auditor’s report to other auditors who

Copyright © 2017 Pearson Education, Inc. 7) When there is uncertainty about a company’s ability to continue as a going concern, the auditor’s concern is the possibility that the client may not be able to continue its operations or meet […]

Accounting Chapter 3 The appropriate audit report date for a standard unmodified opinion

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 3 Audit Reports 3.1 Learning Objective 3-1 1) Which of the following is a correct statement regarding the standard unmodified opinion audit report? A) The format of […]

Accounting Chapter 3 The Receivable Significantly Material in Relation The Financial

Copyright © 2017 Pearson Education, Inc. 3) When comparing misstatements with a measurement base, the auditor must consider the pervasiveness of the misstatement. Of the following examples, the most pervasive misstatement is a(n) A) understatement of inventory. B) understatement of […]

Accounting Chapter 4 Jernigan Corporation For The Year Ended December

Copyright © 2017 Pearson Education, Inc. 13) Which of the following represents all of the ways a CPA firm can be organized? A) proprietorships and partnerships B) proprietorships, partnerships, and professional corporations C) proprietorships, general partnerships, general corporations, professional corporations, […]

Accounting Chapter 4 Scope And Nature Services Member Public Practice

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 4 Professional Ethics 4.1 Learning Objective 4-1 1) Ethics are A) needed in the professions, but is not needed for society in general. B) a set of […]

Accounting Chapter 4 Which of the following circumstances impairs an auditor’s independence

Copyright © 2017 Pearson Education, Inc. 24) A CPA’s financial interests in nonclients may have an effect on independence if the nonclients are investors in or investees of the client. Which situation would not impair a CPA’s independence? A) The […]

Accounting Chapter 5 Reflective Thinking One Significant Result The Escott

Copyright © 2017 Pearson Education, Inc. 2) Which of the following auditor’s defenses usually means nonreliance on the financial statements by the user? A) lack of duty B) non negligent performance C) absence of causal connections D) contributory negligence Answer: […]

Accounting Chapter 5 Some States Not Distinguish Between Ordinary and Gross

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 5 Legal Liability 5.1 Learning Objective 5-1 1) Which of the following factors does not contribute to the number of lawsuits against auditors? A) large civil court […]

Accounting Chapter 6 all of which are tests of transactions associated with the audit of

Copyright © 2017 Pearson Education, Inc. 7) Below are five audit procedures, all of which are tests of transactions associated with the audit of the acquisition and payment cycle. Also below are the six general transaction-related audit objectives and the […]

Accounting Chapter 6 Generally The Auditor Under Obligation Notify Parties

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 6 Audit Responsibilities and Objectives 6.1 Learning Objective 6-1 1) The objective of an audit of the financial statements is an expression of an opinion on A) […]

Accounting Chapter 6 Which of the following is not a step in the professional judgment

Copyright © 2017 Pearson Education, Inc. 2) Which of the following is not a step in the professional judgment process? A) make the decision B) perform the analysis C) determine the type of audit opinion D) review and document the […]

Accounting Chapter 7 State the three phases of the audit where analytical procedures can be

Copyright © 2017 Pearson Education, Inc. 8) Auditors compare client data with A) industry data. B) client-determined expected results. C) similar prior-period data. D) all of the above. Answer: D Terms: Analytical procedures Diff: Easy Objective: LO 7-5 AACSB: Reflective […]

Accounting Chapter 7 When the auditor scans the sales journal looking for large and unusual

21 24) When the auditor scans the sales journal looking for large and unusual transactions, he is gathering what type of evidence? A) inspection B) recalculation C) physical examination D) analytical procedures Answer: D Terms: Types of audit evidence; analytical […]

Accounting Chapter 7 Which of the following is an accurate statement regarding audit evidence

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 7 Audit Evidence 7.1 Learning Objective 7-1 1) Which of the following is an accurate statement regarding audit evidence? A) Responses to the auditor’s questions by client […]

Accounting Chapter 8 A measure of how willing the auditor is to accept that the financial statements

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 8 Audit Planning and Analytical Procedures 8.1 Learning Objective 8-1 1) A measure of how willing the auditor is to accept that the financial statements may be […]

Accounting Chapter 8 Preliminary Materiality Should Allocated Income Statement Accounts

Copyright © 2017 Pearson Education, Inc. 9) The five steps in applying materiality are listed below in random order. 1. Estimate the combined misstatement. 2. Estimate the total misstatement in the segment. 3. Set materiality for the financial statements as […]

Accounting Chapter 8 What Are These Reasons answer The Three Reasons

Copyright © 2017 Pearson Education, Inc. 39) An engagement letter establishes a clear understanding of the terms of the engagement between the client and the auditor. Answer: TRUE Terms: Engagement letter Diff: Easy Objective: LO 8-2 AACSB: Reflective thinking 40) […]

Accounting Chapter 9 Which of the following would not increase the risks of material

Copyright © 2017 Pearson Education, Inc. Auditing and Assurance Services, 16e (Arens/Elder/Beasley) Chapter 9 Materiality and Risk 9.1 Learning Objective 9-1 1) Which of the following would not increase the risks of material misstatement at the overall financial statement level? […]

Accounting Chapter 9 Inherent Risk Dependent Upon The Strengths Clients

Copyright © 2017 Pearson Education, Inc. 24) Using your knowledge of the relationships among acceptable audit risk, inherent risk, control risk, planned detection risk, performance materiality, and planned evidence, state the effect on planned evidence (increase or decrease) of changing […]

ACCT 10957

An auditor must evaluate a specialist’s professional qualifications and understand the objectives of the specialist’s work. The starting point for the verification of the balance in the general bank account is to obtain a bank cut-off statement. Answer: FALSE When […]

ACCT 13240

Which one of the following duties should not be assigned the purchases department? A) finding the lowest cost vendor B) reviewing vendors’ catalog descriptions and prices for standardized items C) designing the purchase order form D) authorizing the acquisition of […]

Acct 17675

The estimated unpaid obligations for services or benefits that have been received before the balance sheet date are A) accounts payable. B) accounts receivable. C) unearned liabilities. D) accrued liabilities. Which ratio is computed by dividing operating income by net […]

ACCT 18835

All known related parties must be identified and included in the auditor’s permanent files related to the client. Auditing standards require the auditor’s assessment of going concern issues. Answer: TRUE When performing substantive analytical procedures for notes payable, if actual […]

Acct 26976

Several factors influence the auditor’s choice of the types of tests to select, including A) the availability of the types of evidence. B) the relative costs of each type of test. C) the effectiveness of the internal controls. D) all […]

ACCT 28413

A primary concern in reporting on a comprehensive basis is to make sure that the statements clearly indicate that they are prepared on a basis other than GAAP. Cutoff for acquisitions of insurance is normally not a significant problem for […]

ACCT 32503

The bank reconciliation A) must be done on a daily basis if the client uses electronic banking. B) should be performed by someone independent of the handling or recording of cash receipts. C) should be performed by someone who handles […]

ACCT 35231

Fraud is more prevalent in large businesses than small businesses and not-for-profit organizations. Statutory laws are laws that have been developed through court decisions rather than through the U.S. Congress and other governmental units. Answer: FALSE Sales returns and allowances […]

ACCT 43512

In testing acquisitions the auditor needs to understand the appropriate accounting guidance related to acquisition accounting. Which of the following is not an accounting consideration for the auditor as regards to acquisition cost? A) inclusion of material transportation and installation […]

Acct 45052

When analytical procedures reveal unusual fluctuations in an account balance, the auditor will probably perform fewer tests of details for that account and increase the tests of controls related to the account. Companies using e-commerce systems to transact business electronically […]

Acct 50917

After the accrual and property tax expense for each piece of property has been recalculated, the totals are added and compared with the general ledger. Deviation refers to a departure from prescribed controls or amounts that are not monetarily correct. […]

Acct 51027

Which of the following statements is correct regarding the audit of inventory cost accounting? A) Cost accounting systems and controls are the same for all manufacturing companies. B) All companies that have work-in-process must use a perpetual inventory system. C) […]

ACCT 58302

When a successor auditor requests information from a company’s previous auditor, and there are legal problems or disputes between the client and the predecessor auditor, the predecessor auditor’s response to the new auditor may be limited to stating that no […]

ACCT 61841

Statistical sampling eliminates any professional judgment for the auditor. In the scope paragraph of the audit report issued for financial statements of a nonpublic company, the auditor expresses an opinion about the internal controls of the company. Answer: FALSE According […]

Acct 63847

If an auditor concludes there are contingent liabilities, then he or she must evaluate the A) B) C) D) The auditor must gather sufficient and appropriate evidence during the course of the audit. Sufficient evidence must A) be well documented […]

ACCT 69617

The primary concern in determining whether retained earnings is correctly disclosed on the balance sheet is A) correct calculation of the net income or loss for the year. B) correct calculation of dividend payments for the year. C) whether prior-period […]

Acct 71662

If, when obtaining an understanding of control activities of a relatively small client, the auditor identified no control activities, the auditor would probably set a high assessment of control risk. Depreciation expense is normally verified as a part of tests […]

ACCT 72465

The ________ is helpful in preventing classification errors if it accurately describes which type of transaction should be in each account. A) general ledger B) general journal C) trial balance D) chart of accounts Interpretations of the rules regarding independence […]

Acct 77254

Which of the following subsequent events is most likely to result in an adjustment to a company’s financial statements? A) merger or acquisition activities B) bankruptcy (due to deteriorating financial condition) of a customer with an outstanding accounts receivable balance […]

ACT 50809

Determining if the financial instruments included in the schedule of investment activity at year-end are stated at appropriate amounts in accordance with accounting standards is the balance-related audit objective of A) materiality. B) realizable value. C) consistency. D) classification. When […]

ACT 51798

What is the best reason that standards prohibit accepting an engagement on a projection for general use? A) The CPA’s procedures would violate SSARS. B) Reports on projections are not well understood by the general public. C) Underlying hypothetical assumptions […]

ACT 58284

The auditors determine which disclosures must be presented in the financial statements. The phrase “Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material error” is included […]

ACT 67094

Which of the following is a reason that the auditors may change the preliminary judgment about materiality? A) The auditors decide that the preliminary judgment was too large. B) The auditors decide that the preliminary judgment was too small. C) […]

ACT 73889

Auditing standards indicate that reasonable assurance is a moderate, but not absolute, level of assurance that the financial statements are free of material misstatement. LANs link equipment within a single or small cluster of buildings and are used within a […]

ACT 80381

Because they spend all their time within one company, internal auditors have much greater knowledge about the company’s operations and internal controls then external auditors. If the preliminary judgment of materiality increases, the amount of audit evidence required will decrease. […]

MET MG 12800

An individual who is not party to the contract between a CPA and the client, but who is known by both and is intended to receive certain benefits from the contract is known as A) a third party. B) a […]

MET MG 31155

Auditing standards require that the auditor evaluate whether there is a substantial doubt about a client’s ability to continue as a going concern for at least A) one quarter beyond the balance sheet date. B) one quarter beyond the date […]

MET MG 35134

The objective of the audit of financial statements by an independent auditor is to verify that the financial statements are free of misstatements and accurately represent the company’s financial position and results of operations. Analytical procedures may be used to […]

MET MG 57721

When customers purchase goods by credit card, the issuer of the credit card uses EFT to transfer funds into the company’s bank account. The three most important audit objectives for cash are accuracy, existence, and classification. Answer: FALSE Auditing standards […]

SMG AC 23214

The auditor’s tests for proper cutoff of current year acquisitions of property, plant, and equipment are usually done as part of accounts payable cutoff tests. Auditors are allowed to have an indirect financial interest in an audit client, such as […]

SMG AC 29276

When assessing the risk of material misstatements in the financial statements, A) inadequate internal control procedures will mitigate client business risk. B) GAAS specifies in detail how much and what types of evidence the auditor needs to obtain. C) company […]

SMG AC 43220

When determining whether independence is impaired because of an ownership interest in a client company, materiality will affect ownership A) in all circumstances. B) only for direct ownership. C) only for indirect ownership. D) under no circumstances. An example of […]

SMG AC 43233

Match six of the terms (a-l) with the definitions provided below (1-6): a. acceptable risk of incorrect acceptance b. acceptable risk of incorrect rejection c. difference estimation d. misstatement bounds e. monetary unit sampling f. mean-per-unit estimation g. point estimate […]