Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

22-1

Chapter 22

Concept Checks

P. 720

1. The characteristics of the liability accounts in the capital acquisition and

repayment cycle that result in a different auditing approach than the

There is a legal relationship between the client entity and the

holder of the stock, bond, or similar ownership document.

and debt and equity.

2. The most important controls the auditor should be concerned about in the

audit of notes payable are:

The proper authorization for the issuance of new notes (or

renewals) to insure that the company is not being committed to debt

arrangements that are not authorized.

Controls over the repayment of principal and interest to insure that

P. 727

1. The primary objectives in the audit of owners’ equity accounts are to

determine whether:

a. The internal controls over capital stock and related dividends are

adequate.

the following six transaction-related audit objectives:

Occurrence

Completeness

Accuracy

22-2

Concept Check, P. 727 (continued)

following balance-related audit objectives:

Detail tie-in

Existence

objectives:

Occurrence and Rights and Obligations

Completeness

2. The duties of a stock registrar are to make sure that stock is issued by a

corporation in accordance with the capital authorization of the board of

and in some cases, disburse cash dividends to shareholders.

The use of the services of a stock registrar improves the effectiveness

the hands of an independent organization.

Review Questions

balance sheets are:

1. Notes payable

These liabilities have the following characteristics in common:

transaction is often highly material in amount.

2. The exclusion of a single transaction could be material in itself.

22-3

22-1 (continued)

4. There is a direct relationship between interest and dividend accounts

and debt and equity.

These liabilities differ in what they represent and the nature of their respective

liabilities.

same time, the likelihood of omitting a note from notes payable for which

interest has been paid is minimized. When there are a large number of notes or

22-3 The most important analytical procedures used to verify notes payable

to uncover unrecorded notes payable are:

1. Examine the notes paid after year-end to determine whether they

2. Obtain a standard bank confirmation that includes specific reference

the bank account by the bank.

4. Obtain confirmation from creditors who have held notes from the

6. Review the minutes of the board of directors for authorized but

unrecorded notes.

22-4

22-5 The primary purpose of analyzing interest expense is to uncover a

payment to a creditor who is not included on the notes payable schedule. The

primary considerations the auditor should keep in mind when doing the analysis

are:

22-6 The tests of controls and substantive tests of transactions for liability

accounts in the capital acquisition and repayment cycle consists of tests of the

controls and substantive tests over the payment of principal and interest and

the issuance of new notes or other liabilities, whereas the tests of details of

22-7 Four types of restrictions long-term creditors often put on companies in

granting them a loan are:

1. Financial ratio restrictions

The auditor can find out about these restrictions by examining the

loan agreement and related correspondence associated with the loan, and

22-8 Although the corporate charter and bylaws are legal documents, their

legal nature is not being judged by the auditor. They are being used only to

22-9 The major internal controls over owners’ equity are:

1. Proper authorization of transactions

2. Proper record keeping

22-5

22-10 The audit of owners’ equity for a closely held corporation differs from

that for a publicly held corporation in that the amount of time spent in verifying

owners’ equity in a closely held corporation is usually minimal because of the

The audits are not significantly different in regard to whether the

transactions in the equity accounts are properly authorized and recorded and

22-12 Because it is important to verify that properly authorized dividends have

been paid to owners of stock as of the dividend record date, a comparison of a

random sample of cancelled dividend checks to a dividend list prepared by

management would be inadequate. Such an audit step is useless unless the

to valid shareholders.

22-13 If a transfer agent disburses dividends for a client, the total dividends

declared can be verified by tracing the amount to a cash disbursement entry to

used.

22-14 The major emphasis in auditing the retained earnings account should

be on the recorded changes that have taken place during the year, such as net

earnings for the year; dividends declared; prior period adjustments; extraordinary

authorization and accuracy of the underlying transactions.

22-15 For auditing owners’ equity and calculating earnings per share, it is

standards.

Multiple Choice Questions From CPA Examinations

22-16 a. (1) b. (2) c. (3)

22-17 a. (4) b. (1) c. (1)

22-18 a. (3) b. (1) c. (3)

Discussion Questions and Problems

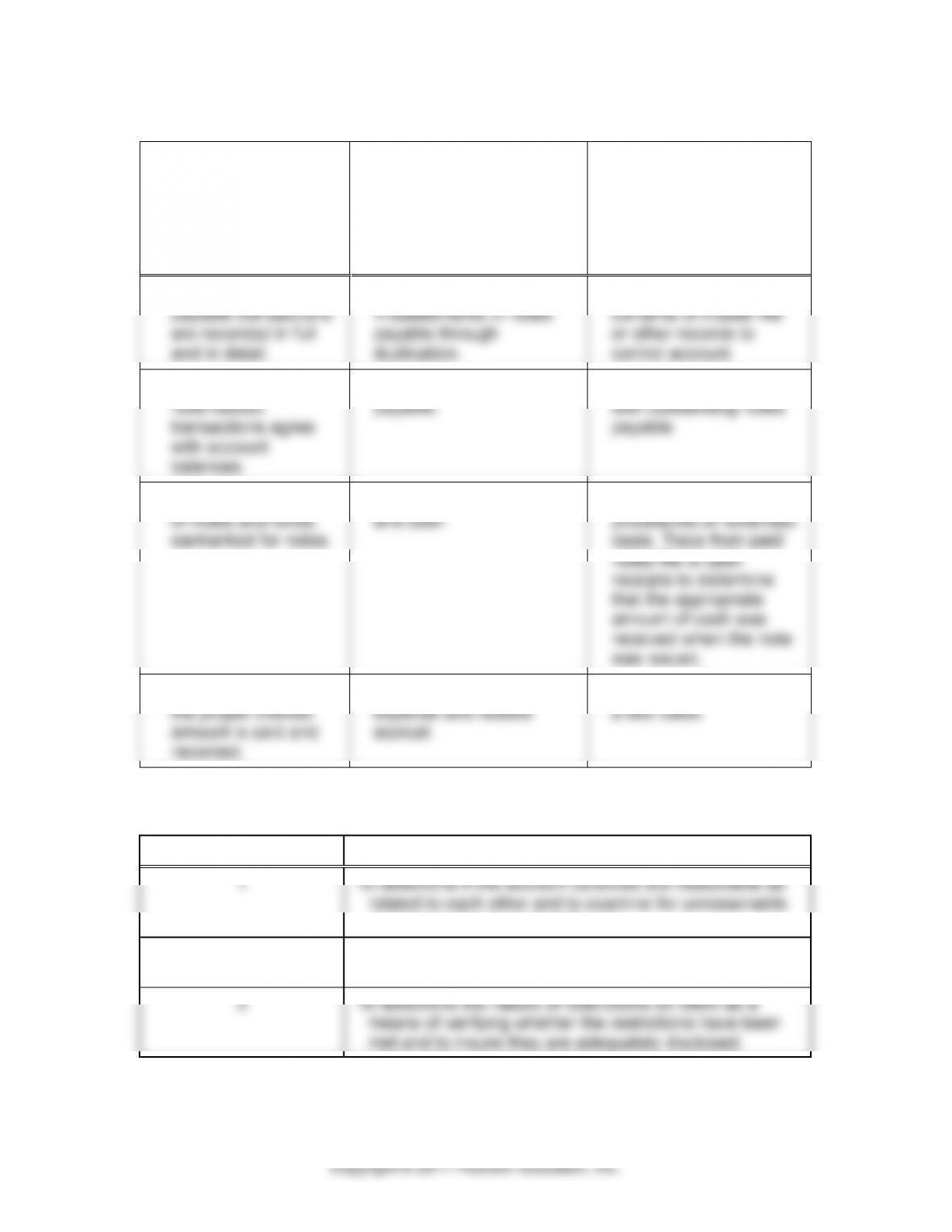

22-19

a.

PURPOSE OF

CONTROL

b.

POTENTIAL FINANCIAL

STATEMENT

MISSTATEMENT

c.

AUDIT PROCEDURE

TO DETERMINE

EXISTENCE

OF MATERIAL

MISSTATEMENT

1. To insure that all

note liabilities are

actual liabilities of

the company.

Loss of assets through

payment of excess

interest rates or the

diversion of cash to

unauthorized persons.

Examine note request

forms for proper

authorization and

discuss terms of note

with appropriate

management

personnel.

2. To insure that notes

are not paid more

than once.

Loss of cash.

Examine outstanding

notes and paid notes

for similarities and the

potential for reusing the

notes.

22-19 (continued)

a.

PURPOSE OF

CONTROL

b.

POTENTIAL FINANCIAL

STATEMENT

MISSTATEMENT

c.

AUDIT PROCEDURE

TO DETERMINE

EXISTENCE

OF MATERIAL

MISSTATEMENT

3. To insure that notes

payable transactions

are recorded in full

and in detail.

Improper disclosure or

misstatements in notes

payable through

duplication.

Reconcile detailed

contents of master file

or other records to

control account.

4. To insure that all

note-related

transactions agree

with account

balances.

Misstatement of notes

payable.

Reconcile master file

with outstanding notes

payable.

5. To prevent misuse

of notes and funds

earmarked for notes.

Misstatement of liabilities

and cash.

Perform all substantive

procedures on extended

basis. Trace from paid

notes file to cash

receipts to determine

that the appropriate

amount of cash was

received when the note

was issued.

6. To insure that only

the proper interest

amount is paid and

recorded.

Misstatement of interest

expense and related

accrual.

Recompute interest on

a test basis.

22-20 a.

AUDIT PROCEDURE

PURPOSE

1

To determine if the account balances are reasonable as

related to each other and to examine for unreasonable

changes in the account balances.

2

To obtain independent confirmation of bond

indebtedness and collateral.

3

To determine the nature of restrictions on client as a

means of verifying whether the restrictions have been

met and to insure they are adequately disclosed.

22-8

22-20 (continued)

AUDIT PROCEDURE

PURPOSE

4

To insure that the bonds are not subject to unnecessary

early retirement by bondholders and that proper

disclosures are made.

5

To determine if the calculations are correct and accounts

are accurate.

indenture agreement:

1. Restrictions on payment of dividends

2. Convertibility provisions

met by the following procedures:

1. Audit of payments of dividends

2. Determine if the appropriate stock authorizations are adequate

verified. The monthly premium or discount is then calculated and

multiplied by the number of months still outstanding.

e. The following information should be requested from the bondholder

in the confirmation of bonds payable:

1. Amount of bond

2. Maturity date

3. Interest rate

22-9

22-21

AUDIT PROCEDURE

PRESENTATION AND

DISCLOSURE-RELATED OBJECTIVE

1

Completeness

2

Classification and understandability

3

Accuracy and valuation

4

Occurrence and rights and obligations

5

Classification and understandability

22-22 a. The amounts listed for each type of long-term debt in the beginning

balance column would be verified by examining the ending audited

documenting board of director approval. The auditor would also

verify whether cash was received and deposited in company cash

accounts if the debt was tied to cash financing. For some types

of long-term debt, such as a mortgage, the company would not

c. To obtain evidence about the items in the payments column, the

auditor would review the related debt contract to determine if the

amounts paid are reasonable. The auditor would also verify that

the payment amounts agree with cash disbursement records and

d. The auditor would verify the mathematical accuracy of the summation

of the beginning balances plus additions less payments to ensure it

crossfoots to the ending balance for each long-term debt category

listed on the schedule. The auditor would also recalculate the

the ending balance with the noteholder.

22-10

22-22 (continued)

agreement.

f. The auditor could use the information in the schedule to develop a

substantive analytical procedure related to interest expense. The

auditor could calculate an average long-term debt balance for

of the debt agreements, the interest payment due dates and

interest rates to determine the appropriate period of time for which

interest expense requires accrual. For example, the debt agreement

for the convertible debentures may indicate that interest is due

($131,250) requires accrual as of December 31, 2016 ($10,000,000

times 5.25% divided by 4 = $131,250). That expectation would

be compared to the amount recorded in the general ledger as

accrued interest for that debt type. The auditor would also need to

determine that prior interest payments have been made and

22-23 a. The emphasis in the verification of notes payable in this situation

should be in determining whether all existing notes are included in

the client’s records. The four audit procedures listed do not satisfy

this emphasis.

b.

AUDIT

PROCEDURE

PURPOSE

1

To determine if the notes payable list reconciles to the general

ledger.

2

To determine if the notes payable on the list are correctly

recorded and disclosed.

3

To verify that all recorded notes payable are properly recorded

and disclosed.

4

To insure that interest expense is properly recorded on the

books.