Extensive professional development is necessary for auditors doing governmental

audits.

In process cost systems, costs are accumulated by individual jobs.

The auditor must perform substantive tests related to assertions deemed to have

significant risks.

Because of the high cost of tests of details of balances, auditors do not perform this

type of testing unless fraud is suspected.

Because they operate the business on a daily basis, a company’s management knows

more about the company’s transactions and related assets, liabilities, and equity than the

auditors.

One unique characteristic of the capital acquisition and repayment cycle is that

relatively few transactions affect the account balances, but each transaction is often

highly material in amount.

Obtaining an understanding of the entity and its environment is part of the analytical

procedures phase of the audit.

Auditors focus on determining whether recorded information properly reflects the

economic events that occurred during the accounting period.

Recording an acquisition of a fixed asset at an improper amount affects the balance

sheet until the company disposes of the asset, but the income statement is not affected.

If the misstatement in a population is larger then tolerable misstatement without

considering sampling error, the population will be considered unacceptable.

When an auditor has reduced assessed control risk based on tests of controls, he or she

may then reduce the extent to which the accuracy of the financial statement information

directly related to those controls must be supported through the accumulation of

evidence using substantive tests.

In practice, auditors do not know whether a sample is representative, even after all

testing is complete.

In a standard inquiry to the client’s attorney letter, the attorney is requested to

communicate about contingencies up to the balance sheet date.

The “rights “aspect of the “rights and obligations” objective is not applicable to

liabilities.

A confirmation is a type of audit evidence.

The adequacy of internal controls over the physical count of inventory is one of the key

determinants of the amount of time needed to test inventory.

If all transaction-related audit objectives are met, the auditor does not need to perform

substantive test of balances to meet the realizable value audit objective.

The Sarbanes-Oxley Act of 2002 makes destruction of audit documentation punishable

by up to 10 years in prison.

In the analysis of expense accounts, the auditor verifies transactions in specific accounts

to determine whether the transactions are properly classified and accurately recorded.

Payroll checks should be distributed by someone independent of the payroll and

timekeeping functions.

The 1136 Tenants case was a criminal case concerning a CPA’s failure to uncover fraud

during a financial statement audit.

Auditing standards recommend that auditors observe physical inventory counts by the

client.

The use of positive assurance is appropriate in a review attestation report.

A document received from the vendor indicating such things as the description and

quantity of goods and services received, price including freight, cash discount terms,

and date of billing is called the voucher.

In difference estimation sampling, the confidence limits are calculated by combining

the point estimate of the total misstatements and the computed precision interval at the

desired confidence level.

Presentation and disclosure objectives are primarily addressed in the tests of details of

balances phase of the audit.

Controls that are applied throughout the accounting period must be tested both at an

interim date and then again on the balance sheet date.

The primary purpose of a management consulting engagement is to generate a

recommendation to management.

When using audit sampling for tests of details of balances, the acceptable risk of

overreliance must be determined.

Membership in the AICPA is mandatory for all licensed practicing CPAs.

If the total misstatement of an account is known, a sampling error still needs to be

determined.

Materiality is essential when an auditor considers his/her determination of the

appropriate report for a given set of circumstances.

Which is usually included in an engagement letter?

A)

B)

C)

D)

________ is an automated fraud detection tool offered by most banks.

A) Positive pay

B) A bank confirmation

C) Fraud buster

D) Check matching

When performing the tests of details of balances for expense accounts, ________ is

(are) generally not necessary.

A) extensive additional testing

B) analytical procedures

C) tests of controls

D) substantive tests of transactions

In comparing management fraud with employee fraud, the auditor’s risk of failing to

discover the fraud is

A) greater for management fraud because managers are inherently more deceptive than

employees.

B) greater for management fraud because of management’s ability to override existing

internal controls.

C) greater for employee fraud because of the higher crime rate among blue collar

workers.

D) greater for employee fraud because of the larger number of employees in the

organization.

Determine which of the following is most correct statement regarding the reliability of

audit evidence.

A) Information that is indirectly obtained from external sources is the most reliable

audit evidence.

B) Reliability of audit evidence is dependent upon the evidence being subjective.

C) Reliability of evidence refers to the amount of evidence obtained.

D) If internal controls are effective, evidence obtained is more reliable than when the

controls are not effective.

Under the AICPA independence rules, the auditor

A) is prohibited from performing a company’s audit and installing and designing the

client’s new information system.

B) does not need to document the understanding and willingness of the client to

perform all management functions associated with the nonaudit service.

C) is prohibited from doing any bookkeeping services for the client if performing the

audit.

D) must follow the more restrictive SEC independence rules when dealing with a public

company.

Determining that the footnote disclosures related to long-term debt are accurate is an

example of the ________ audit objective.

A) occurrence

B) completeness

C) presentation and disclosure

D) classification and understandability

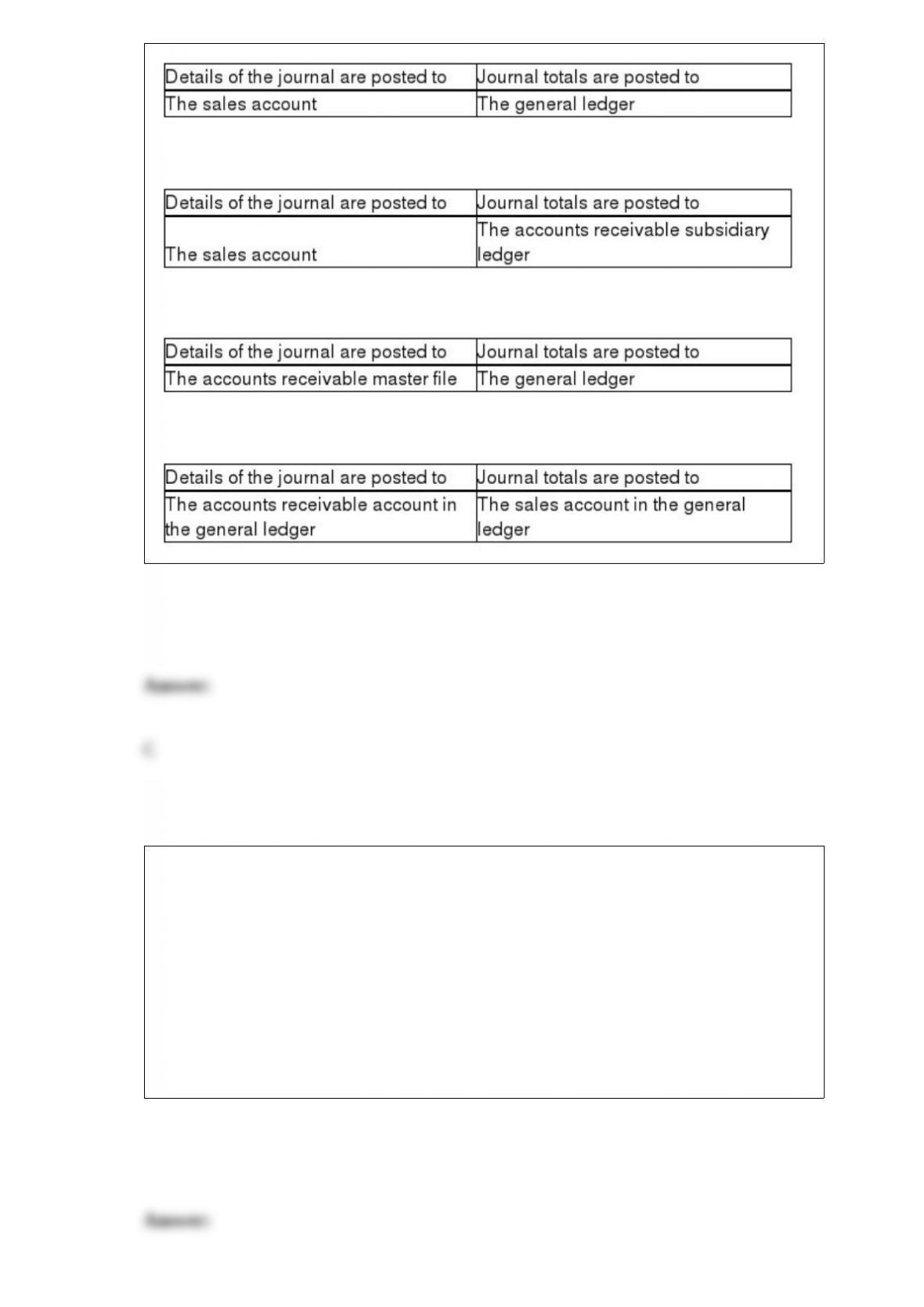

When posting items sold on account from the sales journal

A)

B)

C)

D)

Which of the following management assertions is not associated with classes of

transactions and events?

A) occurrence

B) classification

C) accuracy

D) rights and obligations

Pricing manufactured inventory is difficult. Auditors must evaluate the method of

allocating manufacturing overhead for all but which of the following?

A) reasonableness

B) computational correctness

C) compliance with generally accepted auditing standards

D) consistency

The most important means of verifying account balances in the payroll and personnel

cycle are

A) tests of controls and substantive tests of transactions.

B) analytical procedures and tests of controls.

C) analytical procedures and substantive tests of transactions.

D) tests of controls and tests of details of balances.

When the client fails to make adequate disclosure in the body of the statements or in the

related footnotes, it is the responsibility of the auditor to

A) inform the reader that disclosure is not adequate, and to issue an adverse opinion.

B) inform the reader that disclosure is not adequate, and to issue a qualified opinion.

C) present the information in the audit report and issue an unqualified or qualified

opinion.

D) present the information in the audit report and to issue a qualified or an adverse

opinion.

Fraudulent financial reporting is most likely to be committed by whom?

A) line employees of the company

B) outside members of the company’s board of directors

C) company management

D) the company’s auditors

Before goods are shipped on account, a properly authorized person must

A) prepare the sales invoice.

B) approve the journal entry.

C) approve the customer’s credit.

D) verify that the unit price is accurate.

Company management is often under pressure to increase revenue and/or net income.

One approach is to use a “bill and hold” arrangement. This is an example of which of

the following?

A) significant accounting estimates

B) fictitious revenue recorded

C) premature revenue recognized

D) alteration of cutoff documents

What category of audit report will be issued if the auditor concludes that the financial

statements are not fairly presented?

A) disclaimer

B) qualified

C) standard unmodified opinion

D) adverse

________ means that a person acts according to conscience, regardless of the situation.

A) Caring

B) Fairness

C) Integrity

D) Respect

The relationship of tolerable exception rate (TER) to sample size is

A) direct (larger TER = larger sample).

B) inverse (larger TER = smaller sample).

C) variable (sometimes larger, sometimes smaller).

D) not determinable.

When assessing the risk for fraud, the auditor must be cognizant of the fact that

A) the existence of fraud risk factors means fraud exists.

B) analytical procedures must be performed on revenue accounts.

C) horizontal analysis is not useful in helping to determine unusual financial statement

relationships.

D) the auditor cannot make inquiries about fraud to company personnel who have no

financial statement responsibilities.

The major conclusion of the 1931 Ultramares case was that

A) ordinary negligence is insufficient for liability to third parties.

B) third parties must file criminal charges, not civil charges, against the auditor.

C) fraud or gross negligence is sufficient for liability to third parties.

D) auditors have no liabilities to third parties.

Which of the following is a correct statement regarding materiality?

A) There are well-defined guidelines that enable auditors to determine if something is

material.

B) Misstatements must be compared with some benchmark before a decision can be

made about the materiality level of the failure of a company to follow GAAP.

C) Pervasiveness is not considered when comparing potential misstatements with a base

or benchmark.

D) To evaluate overall materiality, the auditor does not combine all unadjusted

misstatements.

When reviewing the controls and procedures in the acquisition and payment cycle,

A) companies cannot record the liability for the acquisition until the invoice is received

from the vendor.

B) the purchasing department has the responsibility for verifying for appropriateness of

the acquisition.

C) personnel who record the acquisitions should not have access to cash or other assets.

D) the accounts payable department should account for all receiving reports to assure

that the occurrence objective is satisfied.

When allocating performance materiality,

A) it is easy to predict in advance which accounts are most likely to be misstated.

B) only overstatements need to be considered.

C) professional judgment is critical.

D) the sum of all the performance materiality levels cannot exceed the preliminary

judgment about materiality.

If no material differences are found using analytical procedures, and the auditor

concludes that misstatements are not likely to have occurred,

A) other substantive tests may be reduced.

B) it will be necessary to increase the tests of balances.

C) it will not be necessary to perform tests of balances.

D) it will be necessary to increase the tests of transactions.

The service auditor’s Type 2 report contains

A) an opinion on the reasonableness of the financial statements.

B) the two opinions about the description and suitability of the design of controls that

are issued in a Type 1 report plus an additional opinion about the operating

effectiveness of controls throughout the period.

C) an opinion only on the operating effectiveness of the controls.

D) an opinion on the service company’s website.

Another term for misappropriation of assets is

A) management fraud.

B) collusion.

C) employee fraud.

D) illegal acts.

The procedures used to test the effectiveness of the internal controls are known as

A) tests of transactions.

B) tests of controls.

C) substantive analytical procedures.

D) control risk.

The auditor has no responsibility to plan and perform the audit to obtain reasonable

assurance that misstatements that are not ________ are detected.

A) important to the financial statements

B) statistically significant to the financial statements

C) material to the financial statements

D) identified by the client

Which of the following best describes an entity’s accounting information and

communication system?

A)

B)

C)

D)

An attorney is aware of a violation of a patent agreement that could result in a

significant loss to the client if it were known. This is an example of a(n)

A) commitment.

B) unasserted claim.

C) pending litigation.

D) subsequent event.

Discuss the internal controls related to owners’ equity that are of concern to the auditor.

Discuss three major factors that have contributed to the recent increase in the number of

lawsuits against auditors and the size of awards to plaintiffs.

What two steps must an auditor take if they have reservations about the audit client

continuing as a going concern?

There are three stages of the audit in which analytical procedures are performed.

Identify each of these three stages and, for each stage, discuss the purpose of

performing analytical procedures in that stage. Also indicate in which stage(s)

analytical procedures are required by current professional auditing standards.

In addition to attestation and assurance services, CPA firms provide other services to

their clients. List three of these services.

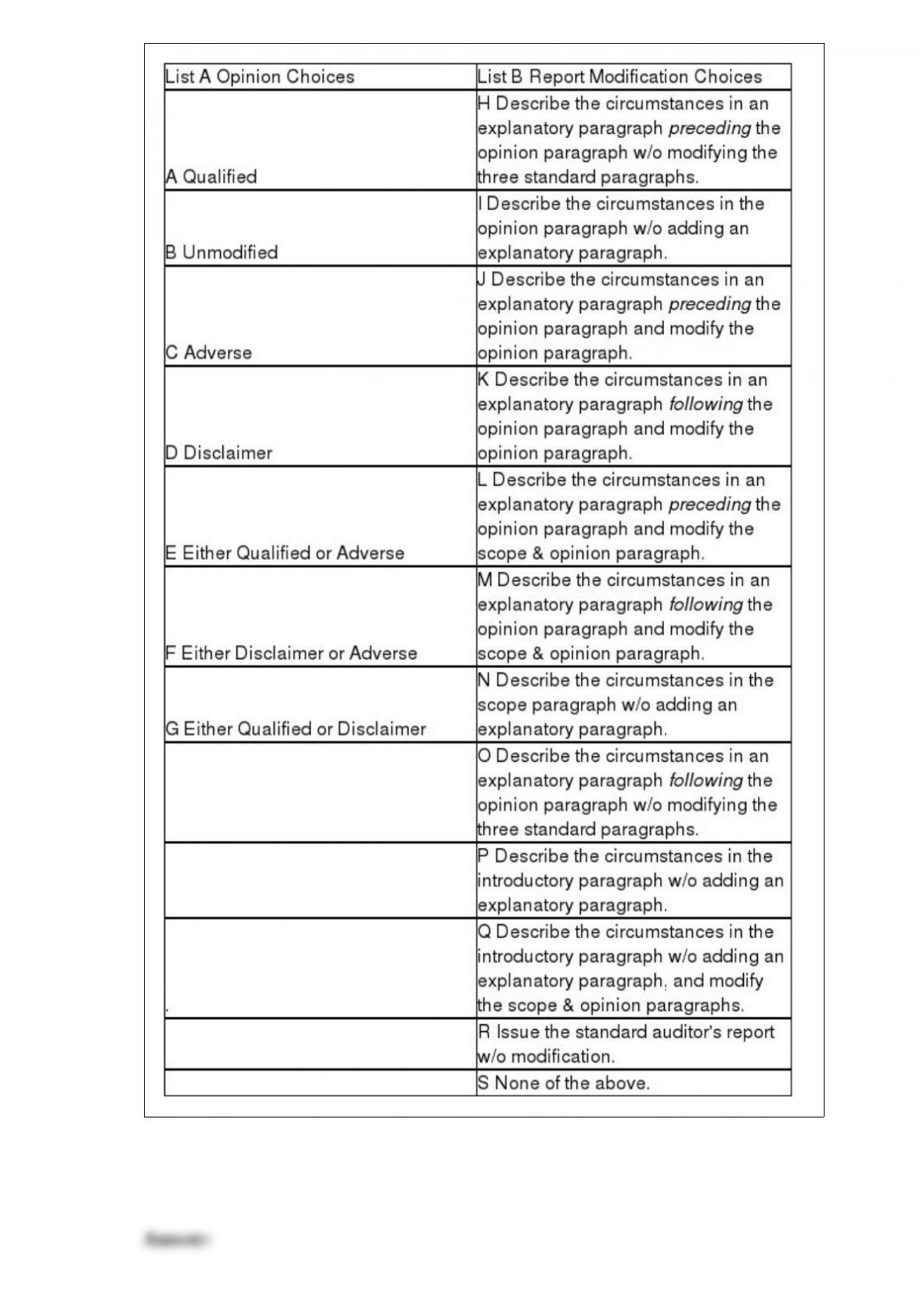

Audit situations 1 through 10 present various independent factual situations an auditor

might encounter in conducting an audit. List A represents the types of opinions the

auditor ordinarily would issue, and List B represents the report modifications (if any)

that would be necessary. For each situation, select one response from List A and one

from List B. Select, as the best answer for each item, the action the auditor normally

would take. Items from either list may be selected once, more than once, or not at all.

Assume the following:

– The auditor is independent

– The auditor previously expressed an unmodified opinion on the prior-year financial

statements unless otherwise noted

– Only single-year (not comparative) statements are presented for the current year

(unless otherwise stated)

– The conditions for an unmodified opinion exist unless contradicted in the factual

scenario

– The conditions stated in the factual scenario are material

– No report modifications are to be made except in response to the factual scenario

Factual Scenario

1. The financial statements present fairly, in all material respects, the financial position,

results of operations, and cash flows in conformity with GAAP.

2. In auditing the Long-Term Investments account, an auditor is unable to obtain

audited financial statements for an investee located in a foreign country. The auditor

concludes that sufficient competent evidential matter regarding this investment cannot

be obtained but it is not pervasive to the financials as a whole.

3. Due to recurring operating losses and working capital deficiencies the auditor has

substantial doubt about an entity’s ability to continue as a going concern for a

reasonable period of time. However, the financial statement disclosures are adequate.

4. The principal auditor decides to refer to the work of another auditor, who audited a

wholly owned subsidiary of the entity and issued an unqualified opinion.

5. An entity issues financial statements that present financial position and results of

operations but omits the related statement of cash flows. Management discloses in the

notes to the financial statements that it does not believe the statement of cash flows to

be useful.

6. An entity changes its depreciation method for production equipment from

straight-line to units of production based on hours of utilization. The auditor concurs

with the change, although it has a material effect on the comparability of the entity’s

financial statements.

7. An entity is a defendant in a lawsuit alleging infringement of certain patent rights.

However, management cannot reasonably estimate the ultimate outcome of the

litigation. The auditor believes that there is a reasonable possibility of a significant

material loss, but the lawsuit is adequately disclosed in the notes to the financial

statements.

8. An entity discloses certain lease obligations in the notes to the financial statements.

The auditor believes that the failure to capitalize these leases is a departure from GAAP.

9. The entity wishes to show comparative financial statements and include the prior

year. However, the prior year financial statements contained a qualification due to an

inappropriate method of GAAP. Accordingly, management corrected the prior year

GAAP deficiency and included the updated numbers in the comparative financials for

the current year.

10. The entity wishes to show comparative financial statements and include the prior

year. However, the prior year financial statements were audited by another auditor who

refuses to reissue his opinion.

When auditing disposals of property, plant, and equipment, the search for unrecorded

disposals is essential. State the four audit procedures frequently used for verifying

disposals.

Auditors often use Generalized Audit Software during their testing of a client’s internal

controls. For the following uses of the software provide a description and an example.

Verify extensions and footings

Print confirmation requests

Compare data on separate files

Discuss the four business functions that result in sales transactions in a typical sales and

collection cycle and, for each function, state the key documents and records involved.

What is an audit of internal control over financial reporting?

Discuss each of the five circumstances when an auditor would issue an unmodified

opinion audit report with an emphasis-of-matter paragraph or nonstandard report

wording.

List the four principles underlying an audit.

What are two factors affecting the complexity of the audit of inventory?

Discuss three audit procedures commonly used to search for contingent liabilities.

The audit of the inventory and warehousing cycle consists of five parts. State the five

parts and, for each part, identify the cycle in which that part is tested by the auditor.