14–11

14–23 (continued)

4. a. Online sales are recorded in the sales system (Completeness).

b. Review online sales system documentation and make

c. Online sales may not be recorded in the sales account,

which would understate sales.

journal.

5. a. Recorded sales are billed using approved prices (Accuracy).

b. Obtain a list of pre–approved unit prices in the master file.

master file.

c. Sales transactions could be recorded using incorrect amounts.

d. Compare a sample of prices on a sample of sales invoices

6. a. Recorded sales are for the correct amounts (Accuracy).

is documentation of the independent verification.

c. Sales could be misstated because they are recorded at

inaccurate amounts.

the sales amount.

7. a. Recorded sales are for shipments actually made (Occurrence).

b. Review systems documentation and make inquiries of

transaction is rejected.

c. Sales could be recorded even though goods have not been

shipped to customers, which overstates sales.

entries.

14–12

14–23 (continued)

8. a. Sales transactions are correctly included in the accounts

receivable master file and are correctly summarized (Posting

and Summarization).

receivable.

c. The accounts receivable master file does not reflect

transactions that are included in the ending accounts

receivable general ledger balance.

in the accounts receivable master file.

9. a. All cash sales are recorded (Completeness).

b. Inquire about duties for individuals responsible for cash

collections and observe whether they have access to

accounting or shipping functions.

14–24

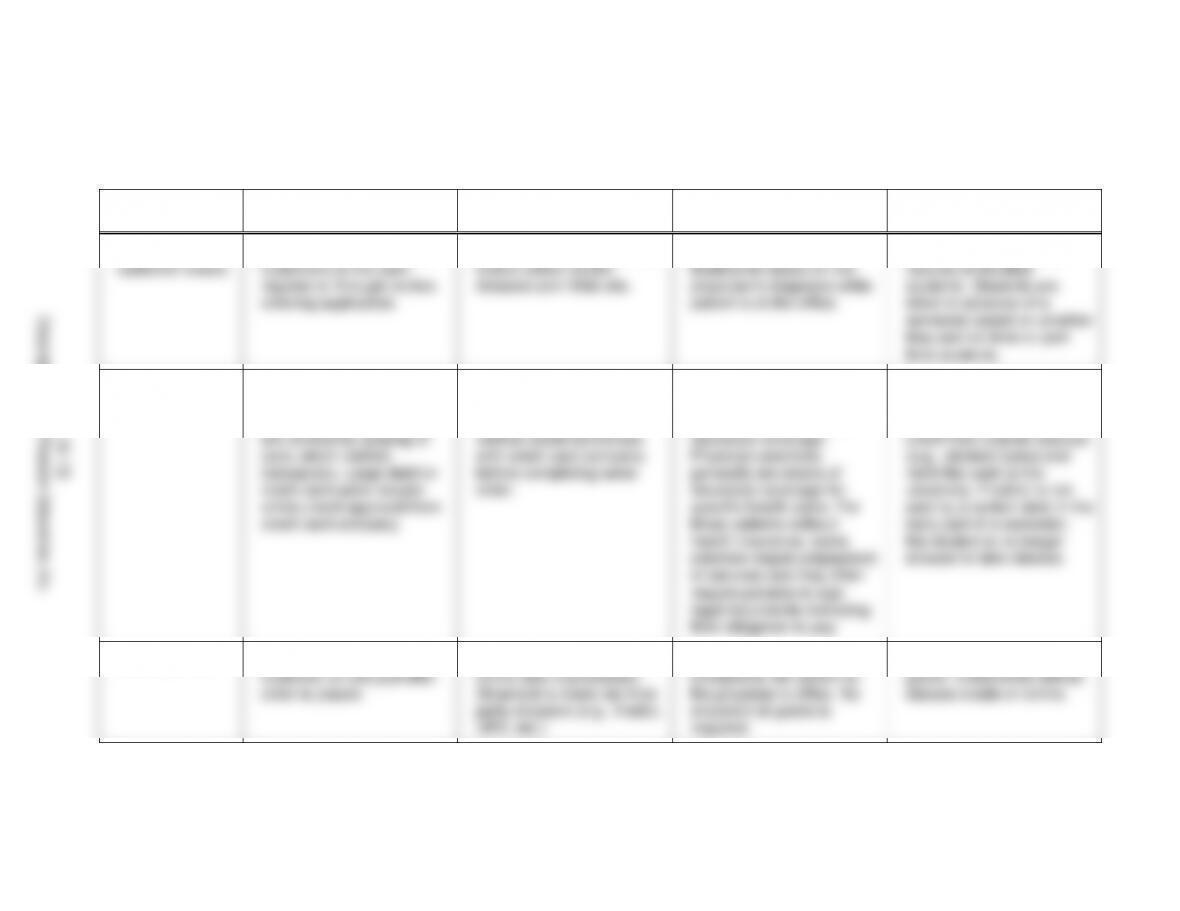

a.

Business

Function

Starbucks

Amazon

Physician Practice

University

Processing

customer orders

Baristas receive orders from

customers at the cash

register or through on–line

ordering application.

Customers shop and process

orders online via the

Amazon.com Web site.

Physicians provide medical

treatments based on the

physician’s diagnosis while

patient is at the office.

University registrars have

records of enrolled

students. Students are

billed in advance of a

they are full–time or part–

time students.

Granting credit

No credit approval is

required for cash sales.

Debit or credit card sales

are verified by swiping of

card, which verifies

transaction. Large debit or

credit card sales require

online credit approval from

credit card company.

Customers make purchases

via debit or credit cards.

The Amazon system

verifies credit worthiness

with credit card company

before completing sales

order.

Before services are provided,

patients must present

documentation of health

insurance coverage.

Physician practices

generally are aware of

insurance coverage for

specific health plans. For

those patients without

health insurance, some

practices require prepayment

of services and they often

require patients to sign

legal documents indicating

their obligation to pay.

Many universities do not

grant credit for tuition.

Rather, students seek

credit from outside sources

(e.g., student loans) and

remit the cash to the

university. If tuition is not

paid by a certain date in the

early part of a semester,

the student is no longer

allowed to take classes.

Shipping goods

Goods are delivered to

customer on site just after

order is placed.

Goods are shipped after the

online sale is processed.

Shipment is made via third–

party shippers (e.g., FedEx,

UPS, etc.).

Medical services are

provided to the patient at

the physician’s office. No

shipment of goods is

required.

There is no shipment of

goods. Universities deliver

classes onsite or online.

14–13

Copyright © 2017 Pearson Education, Inc.

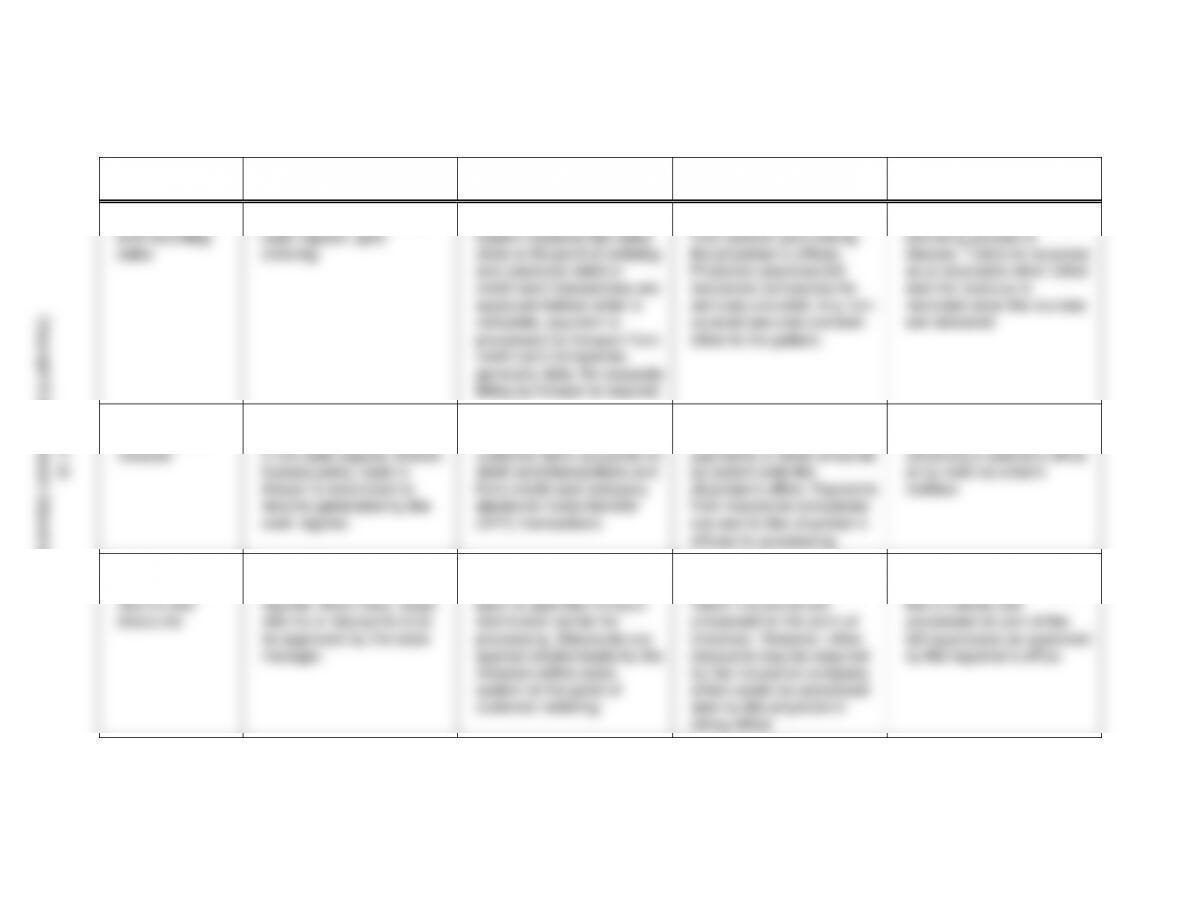

14–24 (continued)

Business

Function

Starbucks

Amazon

Physician Practice

University

Billing customers

and recording

sales

All sales are entered in the

cash register upon

ordering.

The Amazon online sales

system captures the sales

order at the point of ordering

and customer debit or

credit card transactions are

approved before order is

complete; payment is

processed by Amazon from

credit card companies,

generally daily. No separate

billing by Amazon is required.

Co–payments are collected

from patient upon exiting

the physician’s offices.

Physician practices bill

insurance companies for

services provided. Any non–

covered services are later

billed to the patient.

Tuition is billed in advance of

providing access to

classes. Tuition is recorded

as a receivable when billed

and the revenue is

recorded once the courses

are delivered.

Processing and

recording cash

receipts

Cash is collected as order is

placed and cash is entered

in the cash register drawer.

Subsequently, cash in

drawer is reconciled to

records generated by the

cash register.

Cash is received

electronically from

customer bank accounts for

debit card transactions and

from credit card company

electronic funds transfer

(EFT) transactions.

A cashier at the physician’s

office collects any co–

payments or other amounts

as patient exits the

physician’s office. Payments

from insurance companies

are sent to the physician’s

offices for processing.

Tuition payments are

typically received at the

university’s cashier’s office

or by mail via a bank

lockbox.

Processing and

recording sales

returns and

discounts

Returns or discounts are

recorded using the cash

register. Most likely, larger

returns or discounts must

be approved by the store

manager.

Customers must ship

merchandise for return

back to specified Amazon

distribution center for

processing. Discounts are

applied electronically by the

Amazon online sales

system at the point of

customer ordering.

Generally, pre–negotiated

discounts associated with

health insurance are

processed at the point of

checkout. However, other

discounts may be required

by the insurance company,

which would be processed

later by the physician’s

billing office.

Any tuition waivers or

scholarships provided by

the university are

processed as part of the

billing process as approved

by the registrar’s office.

14–14

Copyright © 2017 Pearson Education, Inc.

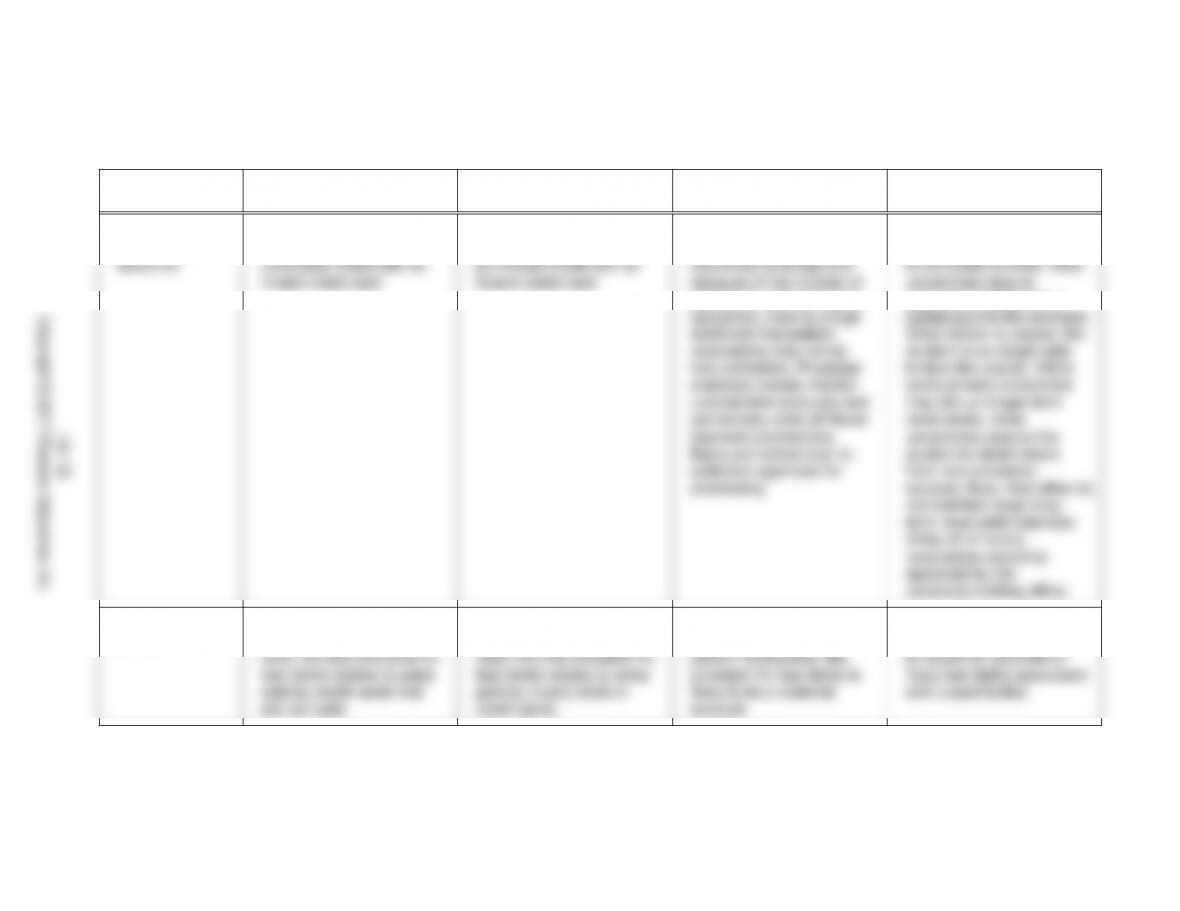

14–24 (continued)

Business

Function

Starbucks

Amazon

Physician Practice

University

Writing off

uncollectible

accounts

The only uncollectible

accounts relate to

purchases made with an

invalid credit card.

The only uncollectible

accounts relate to

purchases made with an

invalid credit card.

Because of the complexities

surrounding health

insurance coverage and

because of the number of

individuals without health

likelihood that patient

receivables may not be

fully collectible. Physician

practices closely monitor

uncollectible accounts and

periodically write–off those

deemed uncollectible.

Many are turned over to

collection agencies for

processing.

If tuition is not paid in full, the

student generally is unable

to complete courses. Most

universities require

payment in full before a

When tuition is unpaid, the

student is no longer able

to take the course. While

some private universities

may set up longer–term

receivables, most

universities require the

student to obtain loans

from non–university

sources; thus, they often do

not maintain large long–

term receivable balances.

Write–off of tuition

receivables would be

Providing for bad

Because most sales are

Because most sales are

Because of the high

The university’s accounting

14–15

Copyright © 2017 Pearson Education, Inc.

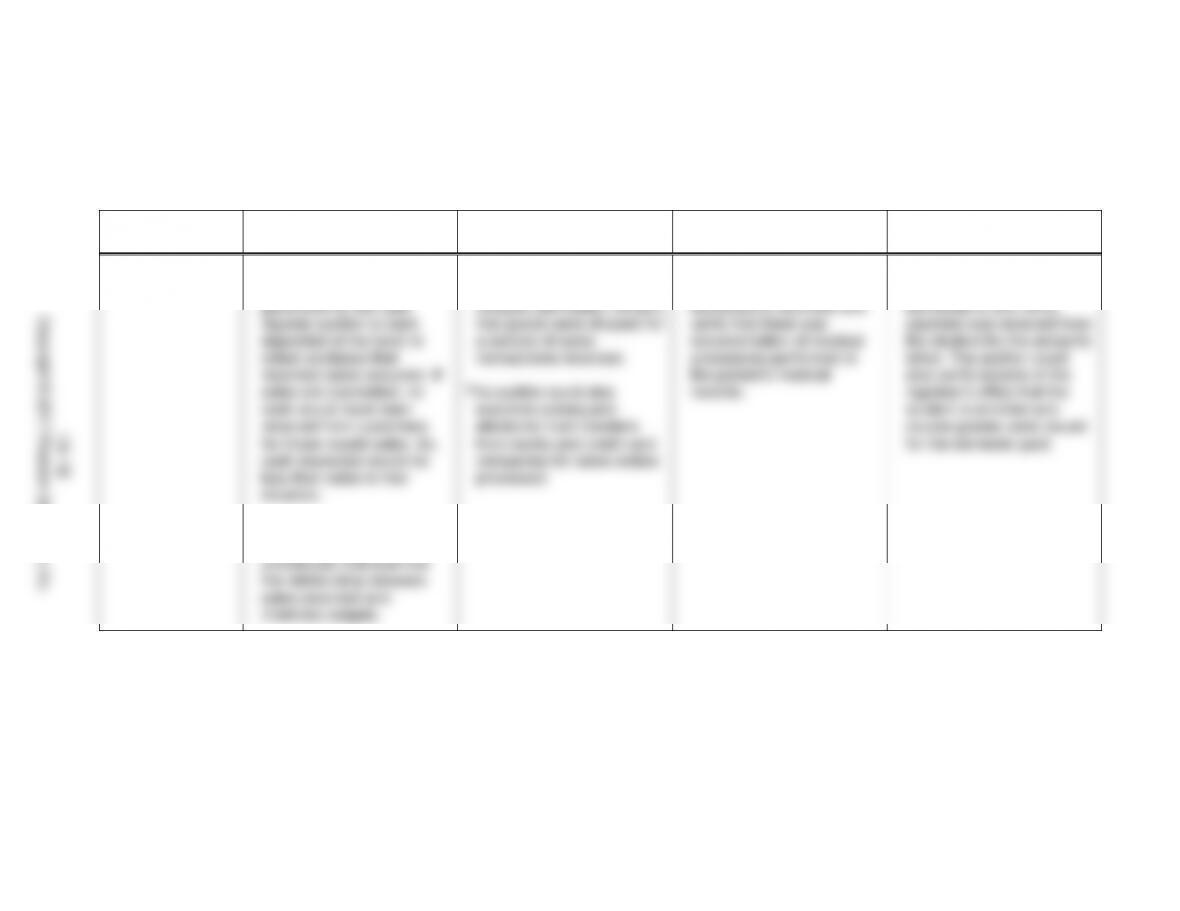

14–24 (continued)

b.

Transaction

Objective

Starbucks

Amazon

Physician Practice

University

Occurrence of

sales

The auditor would likely

reconcile sales records

generated by the cash

register system to cash

deposited at the bank to

obtain evidence that

recorded sales occurred. If

sales are overstated, no

cash would have been

received from customers

for those invalid sales. So,

cash deposited would be

less than sales in that

situation.

The auditor may perform

substantive analytical

procedures that examine

the relationship between

sales recorded and

inventory usages.

The auditor could inspect

documentation from the

Amazon distribution centers

that goods were shipped for

a sample of sales

transactions recorded.

The auditor could also

examine subsequent

electronic fund transfers

from banks and credit card

companies for sales orders

processed.

The auditor could select a

sample of patient revenue

transactions recorded and

verify that there was

documentation of medical

procedures performed in

the patient’s medical

records.

The auditor could select a

sample of tuition revenue

transactions and verify

payment was received from

the student for the amounts

billed. The auditor could

also verify records in the

registrar’s office that the

student is enrolled and

course grades were issued

for the semester paid.

14–16

Copyright © 2017 Pearson Education, Inc.

14–17

14–24 (continued)

c. Physician offices and universities would generally not have sales

return activities. While Starbucks may receive returns for some

d. Starbucks and Amazon most likely would not have a large volume

14–25

1. a. Test of control

(Completeness)

(2) Cash receipts are recorded on the correct dates.

(Timing)

c. Observation or inspection

2. a. Substantive test of transactions

b. (1) Recorded receipts are for funds actually received by

the company. (Occurrence)

(Completeness)

(3) Cash receipts are deposited at the amount received.

(Accuracy)

(Timing)

c. Inspection

3. a. Test of control

b. Existing sales transactions are recorded. (Completeness)

c. Inspection

4. a. Test of control

customers. (Occurrence)

c. Inspection

5. a. Substantive test of transactions

14–18

14–25 (continued)

6. a. Substantive test of transactions

and summarization)

c. Reperformance

7. a. Test of control

(Occurrence)

c. Inspection

14–26

POSSIBLE ERROR OR FRAUD

CONTROL

1. Goods are removed from inventory

for unauthorized orders.

f. Approved sales orders are required

for goods to be released from

warehouse.

2. Credit sales are made to customers

with unsatisfactory credit ratings.

a. Customer orders are compared with

an approved customer list.

3. Invoices are sent to co–participants

in a fraudulent scheme, and sales

are recorded for fictitious

transactions.

i. Sales invoices are compared with

shipping documents and approved

customer orders before invoices are

mailed.

4. Good shipped to customers do not

agree with goods ordered by

customers.

h. Shipping clerks compare goods

received from warehouse with

approved sales orders.

5. Invoices are sent for shipped

goods, but are not recorded in the

sales journal.

k. Daily sales summaries are

compared with control total of

invoices.

6. Invoices are sent for shipped

goods, and are recorded in the

sales journal, but are not posted to

any customer accounts.

j. Control amounts posted to the

accounts receivable ledger are

compared with the control totals of

invoices.

7. Invoices for goods sold are posted

to incorrect customer accounts.

g. Monthly statements are mailed to

customers with outstanding balances.

8. Invoices for goods sold are posted

to incorrect customer accounts.

e. Goods returned for credit are

approved by the supervisor of the

sales department.

14–19

14–27 a. (2) b. (3) c. (4)

14–28

61% involved improper revenue recognition.

b. The two categories of improper revenue recognition are recording of

fictitious revenue, and recording revenues prematurely.

Premature revenue recognition – These frauds involve an actual

sale, but the company recognized some or all of the revenue in a

period before it was earned. For example, a company might

c. The COSO report describes several techniques to overstate revenue.

Conditional sales – In these transactions, the company recorded

Bill and hold sale – In a bill and hold sale, the company billed the

customer for the goods, but they were held by the fraud company and

shipped at a later date.

14–20

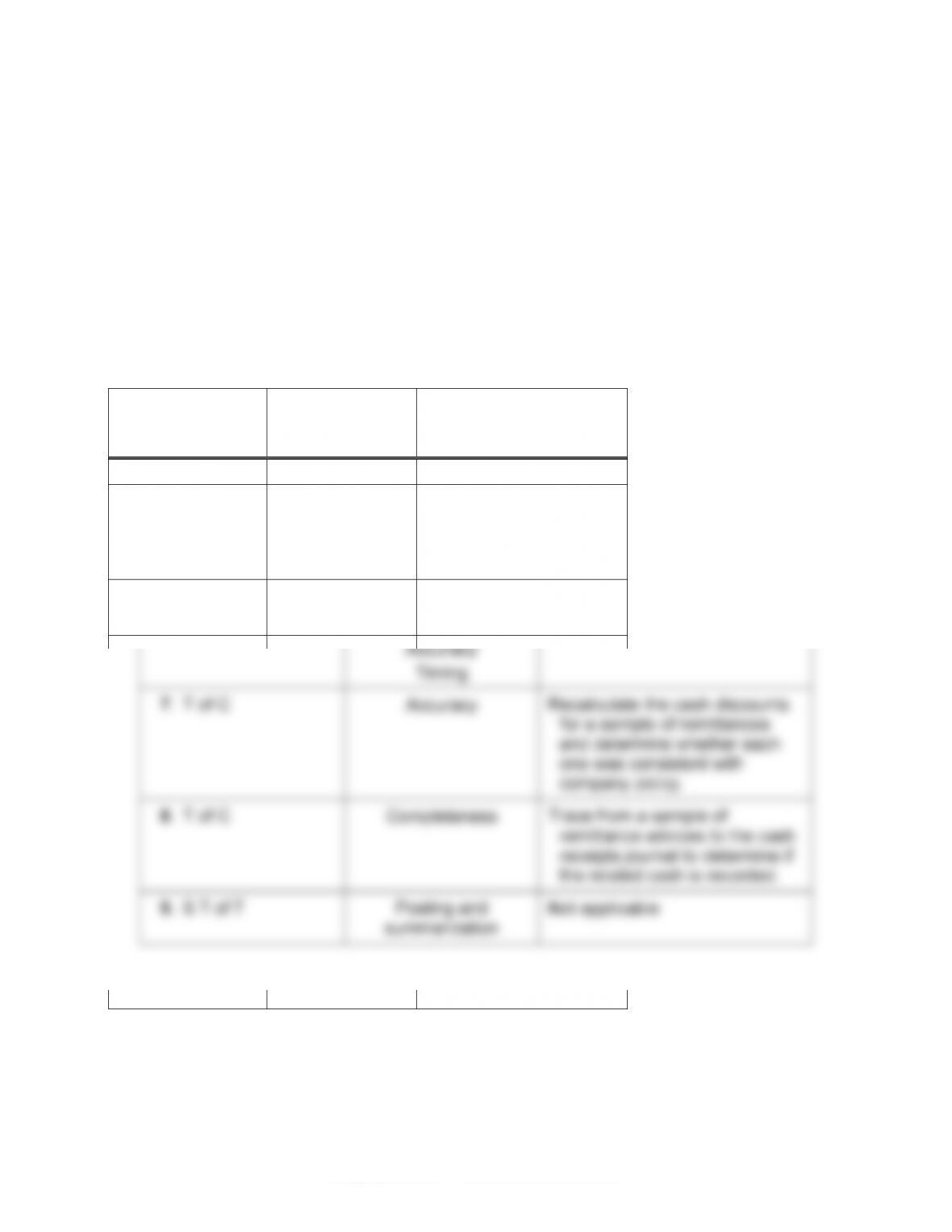

14–29

TEST OF CONTROL

OR SUBSTANTIVE

TEST OF

TRANSACTIONS

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

SUBSTANTIVE TEST

1. S T of T

Classification

Not applicable

2. S T of T

Completeness

Accuracy

Timing

Posting and

summarization

Not applicable

3. T of C

Accuracy

Compare unit selling prices on

duplicate sales invoices to the

approved price list.

4. T of C

Classification

Examine a sample of sales

transactions to determine if

each one is correctly classified

in the sales journal.

5. S T of T

Accuracy

Not applicable

6. S T of T

Occurrence

Completeness

Accuracy

Timing

Not applicable

7. T of C

Accuracy

Recalculate the cash discounts

for a sample of remittances

and determine whether each

one was consistent with

company policy.

8. T of C

Completeness

Trace from a sample of

remittance advices to the cash

receipts journal to determine if

the related cash is recorded.

9. S T of T

Posting and

summarization

Not applicable