12-11

12–21 (continued)

system. She must obtain an understanding of internal control to

determine whether it is possible to conduct an audit at all. Auditing

standards require, at a minimum, an understanding of internal

control.

The auditor must understand the control environment and

the flow of transactions. It is not necessary, however, for the

c. Collier’s approach is not acceptable when auditing either a public

or nonpublic company. Collier must obtain an understanding of

internal controls over financial reporting in all audits. When the

auditor assesses control risk below the maximum, which is

companies.

d. While Pherson’s approach includes procedures similar to those

that would be performed to obtain an understanding of internal

controls, if Pherson is auditing a public company, he may need to

for accelerated filer public companies.

12–22 1. a. Supplying the receiving department with electronic

access to the purchase order is regarded as a

deficiency in that the department may be less careful

be received.

The failure to have the storekeeper receipt for the

materials when they are sent to him or her from the

receiving department or to tie in the items placed in

storage with the acquisition constitutes a deficiency

12-12

12–22 (continued)

stores department might fraudulently convert some

of the materials and because of the lack of a

record of responsibility, the company would be

unable to determine which department was

responsible.

inventory actually received and recorded.

The failure to isolate responsibility for shortages also

increases the likelihood of obsolescence in that

employees are likely to be less concerned when they

the goods.

2. a. The payroll checks should not be returned to the

computer department supervisor but should be

part in generating the payroll data.

There is a lack of internal verification of the hours,

rates, extensions, or employees by above.

There may be misstatements in hours, rates,

extensions, and the existence of nonworking

employees.

person and not returned to Strode.

Internal verification of that information by Webber or

someone else.

12-13

12–22 (continued)

3. a. The bank statement and cancelled checks should not be

disbursements or inflate other reported disbursement

amounts.

c. Have all bank statements sent directly to the home office

testing of IT security and software changes that might be

necessary in the current year audit due to the auditor’s reliance on

them to prevent changes to the underlying automated

reconciliation control.

year’s audit.

3. Testing is required in the December 31, 2016, audit because the

control is designed to mitigate a significant risk. Controls that

4. Testing is required in the December 31, 2016, audit because the

year.

5. No testing is required in the December 31, 2016, audit because

the auditor has determined that the automated controls have not

been changed since the prior year. The auditor obtains

12-14

12–23 (continued)

extent of testing of IT security and software changes that might be

12–24 The following are deficiencies of internal control, by transaction–related

audit objective.

Occurrence

The receiving report is not sent to the stores department. A copy

of the receiving report should be sent from the receiving room

directly to the stores department with the materials received. The

The controller should not be responsible for cash disbursements.

The cash disbursement function should be the responsibility of the

The purchase requisition is not approved. The purchase

requisition should be approved by a responsible person in the

stores department. The approval should be indicated on the

Preliminary review should be made before preparing purchase

orders. Prior to preparation of the purchase order, the purchase

Completeness

Purchase orders and purchase requisitions should not be

combined and filed with the unmatched purchase requisitions, in

There is no indication of control over vouchers in the accounts

payable department. A record of all vouchers submitted to the

12-15

12–24 (continued)

There is no indication of any control over prenumbered

Accuracy

Purchase requisitions and purchase orders are not compared in

the stores department. Although purchase orders are attached to

that:

a. Prices are reasonable;

b. The quality of the materials ordered is acceptable;

c. Delivery dates are in accordance with company needs;

Because the requisitioner will be charged for the materials

The purchase office does not review the invoice prior to

processing approval. The purchase office should review the

vendor’s invoice for overall accuracy and completeness,

The copy of the purchase order sent to the receiving room

generally should not show quantities ordered, thus forcing the

There is no indication of control over dollar amounts on vouchers.

Accounts payable personnel should prepare and maintain control

Note: Classification, timing, and posting and summarization are

12-16

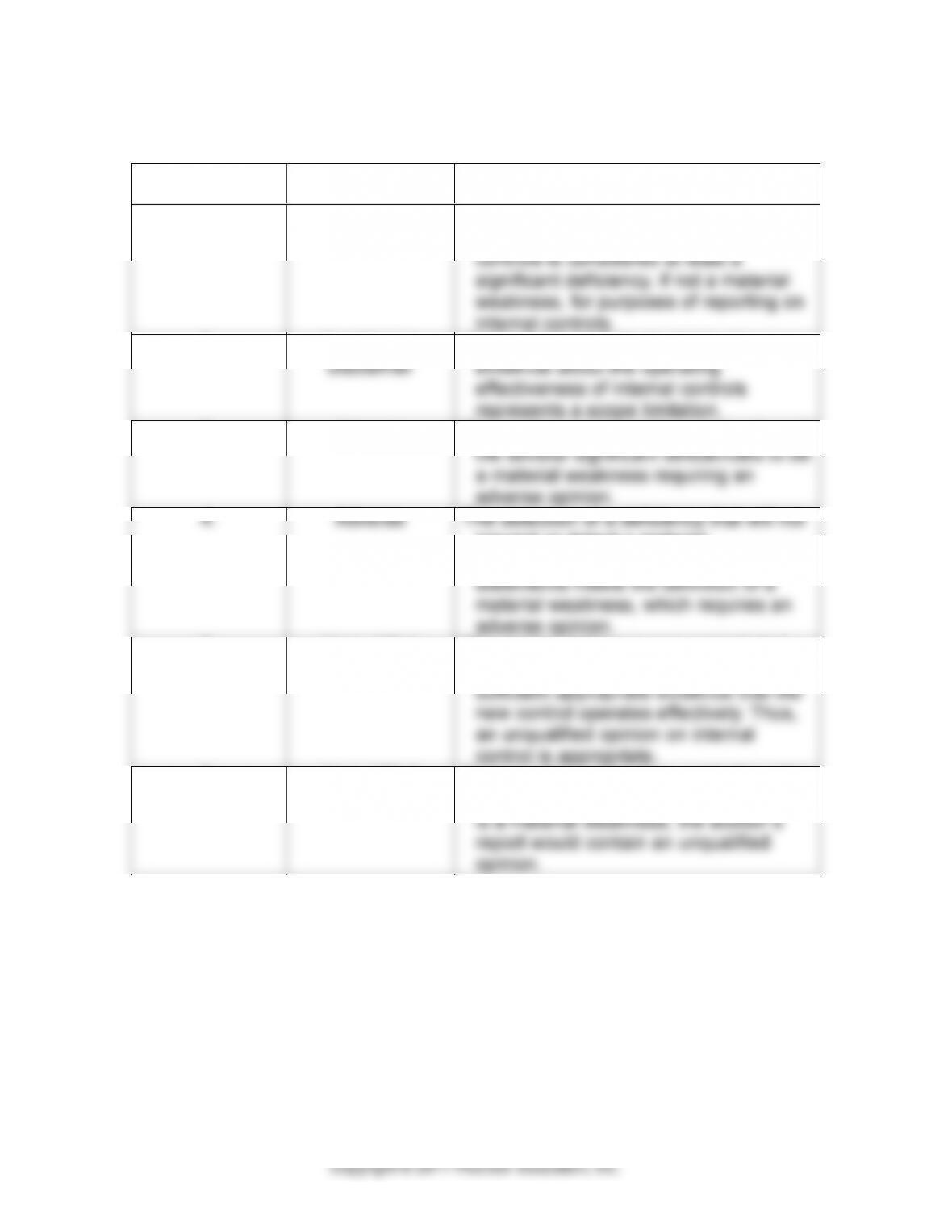

12–25 Following are the appropriate reporting formats for the six independent

situations:

INDEPENDENT

SITUATION

APPROPRIATE

AUDIT REPORT

REASON FOR REPORT

1.

Adverse

The presence of a material misstatement

not detected by the company’s internal

controls is considered at least a

significant deficiency, if not a material

weakness, for purposes of reporting on

internal controls.

2.

Qualified or

disclaimer

The auditor’s inability to obtain any

evidence about the operating

effectiveness of internal controls

represents a scope limitation.

3.

Adverse

The auditor considers the combination of

the several significant deficiencies to be

a material weakness requiring an

adverse opinion.

4.

Adverse

The detection of a deficiency that will not

prevent or detect a material

misstatement in the financial

statements meets the definition of a

material weakness, which requires an

adverse opinion.

5.

Unqualified

The control deficiency was remediated

and the auditor was able to obtain

sufficient appropriate evidence that the

new control operates effectively. Thus,

an unqualified opinion on internal

control is appropriate.

6.

Unqualified

Because the auditor does not believe the

significant deficiency in internal control

is a material weakness, the auditor’s

report would contain an unqualified

opinion.

12-17

12–26 a. The important controls and related sales transaction–related audit

objectives are:

CONTROL

SALES TRANSACTION–RELATED

AUDIT OBJECTIVE

1. Use of prenumbered sales

orders

Existing sales transactions are recorded

2. Segregated approval of sales by

credit department; customer

purchase orders are attached to

sales orders; approval is noted

on form

Recorded sales are for shipments made to

existing customers

3. Segregated entry of approved

sales orders

Recorded sales are for shipments made to

existing customers

Recorded sales are posted to correct

customer account

Prices are entered using an

approved price list

Recorded sales are at the correct price

Sales invoices are prepared from

the data file created from sales

order entry; hash totals are

generated and used; sales

invoices are prenumbered;

control totals are reconciled by

an independent person

Recorded sales are for shipments made to

existing customers

Existing sales transactions are recorded

Recorded sales are at the correct amount

Sales transactions are properly included in

the master files

4. & 5. Bills of lading are produced

with sales invoices and

eventually filed with the sales

invoice in numerical order;

differences in quantities are

corrected and transaction

amounts are adjusted

Existing sales transactions are recorded

Recorded sales are for the correct quantity

of goods shipped

6. Hash totals of daily processing

matched to hash and control

totals generated by independent

person

Existing sales transactions are recorded.

Recorded transactions are for shipments

made to existing customers

12-18

12–26 (continued)

1. Account for the sequence of prenumbered sales order forms.

orders from customers.

appears on all sales order forms.

4. Account for the sequence of prenumbered sales invoices.

invoices and are in agreement therewith.

6. Determine that the price list used by the billing clerk has

7. Ascertain that the sales invoices are in agreement with the

Among the audit procedures to be applied to the data file are the

following:

1. Verify the company’s predetermined “hash” totals and control

2. Compare totals and see that they reconcile.

3. Arrange for a tabulating run to be made of selected test

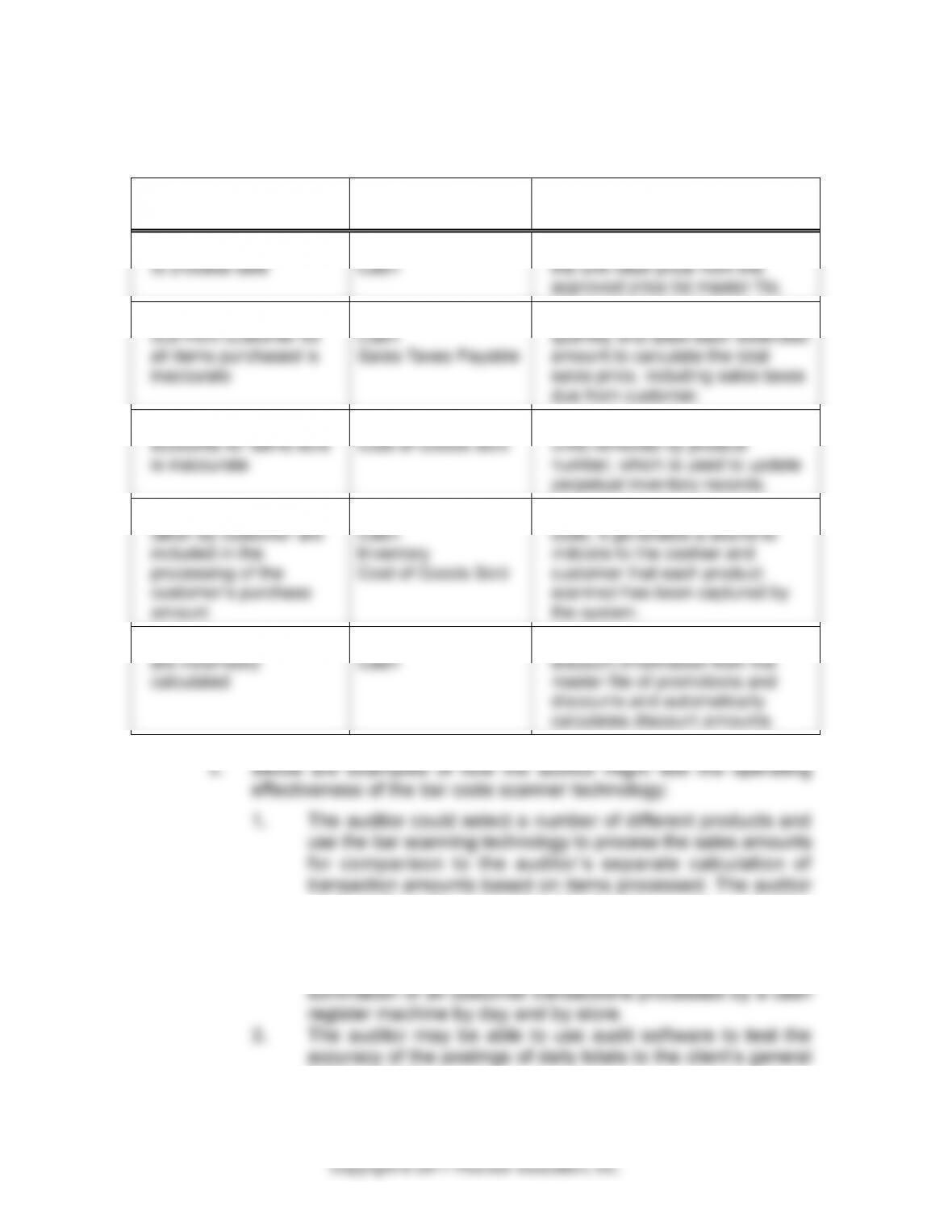

12–27 a. The use in grocery stores of bar code scanning technologies impacts

a number of financial statement accounts for a grocery. The bar

code scanner is used to retrieve unit prices for each product

scanned, which is then used to calculate the amount to be posted

to the Revenue, Sales Tax Payable, and Cash accounts (and any

overnight Receivable accounts related to sales paid by debit and

12–27 (continued)

b.

Risks Inherent to

Sales Processing

Accounts Affected

How Bar Scanning

Technologies Help Reduce Risk

Wrong unit price is used

to process sale

Revenues

Cash

The system automatically retrieves

the unit retail price from the

approved price list master file.

Calculation of amounts

due from customer for

all items purchased is

inaccurate

Revenues

Cash

Sales Taxes Payable

The system extends price times

quantity and adds each extended

amount to calculate the total

sales price, including sales taxes

due from customer.

Reduction in inventory

accounts for items sold

is inaccurate

Inventory

Cost of Goods Sold

The system tracks the number of

units removed by product

number, which is used to update

perpetual inventory records.

Not all inventory items

taken by customer are

included in the

processing of the

customer’s purchase

amount

Revenues

Cash

Inventory

Cost of Goods Sold

As the system reads each bar

code, it generates a sound to

indicate to the cashier and

customer that each product

scanned has been captured by

the system.

Coupons and discounts

are incorrectly

calculated

Sales Discounts

Cash

The system retrieves coupon and

discount information from the

master file of promotions and

discounts and automatically

calculates discount amounts.

could perform the same kind of test using coupons and other

discount programs.

2. The auditor may be able to use audit software to test the

accuracy of individual customer transactions and to test the

ledger system.

12-20

12–27 (continued)

prices, etc.).

5. The auditor may be able to use audit software to identify

the most recent date of the most recent date of sale by

the auditor’s desktop or laptop computer. Other generalized audit

software exists that contain programs that create or generate

other programs, programs that modify themselves to perform

requested functions, or skeletal frameworks of programs that must

be completed by the user.

machine–readable files in a format specified by the auditor.

b. Ways in which a generalized audit software package can be used

to assist in the audit of inventory of Boos & Baumkirchner, Inc.,

include the following:

cards or the electronic inventory master file. Exclude from

the population items with a high unit cost or total value that

have already been selected for test counting.

3. Access the client’s electronic inventory master file and list

data for determining possible obsolescence.