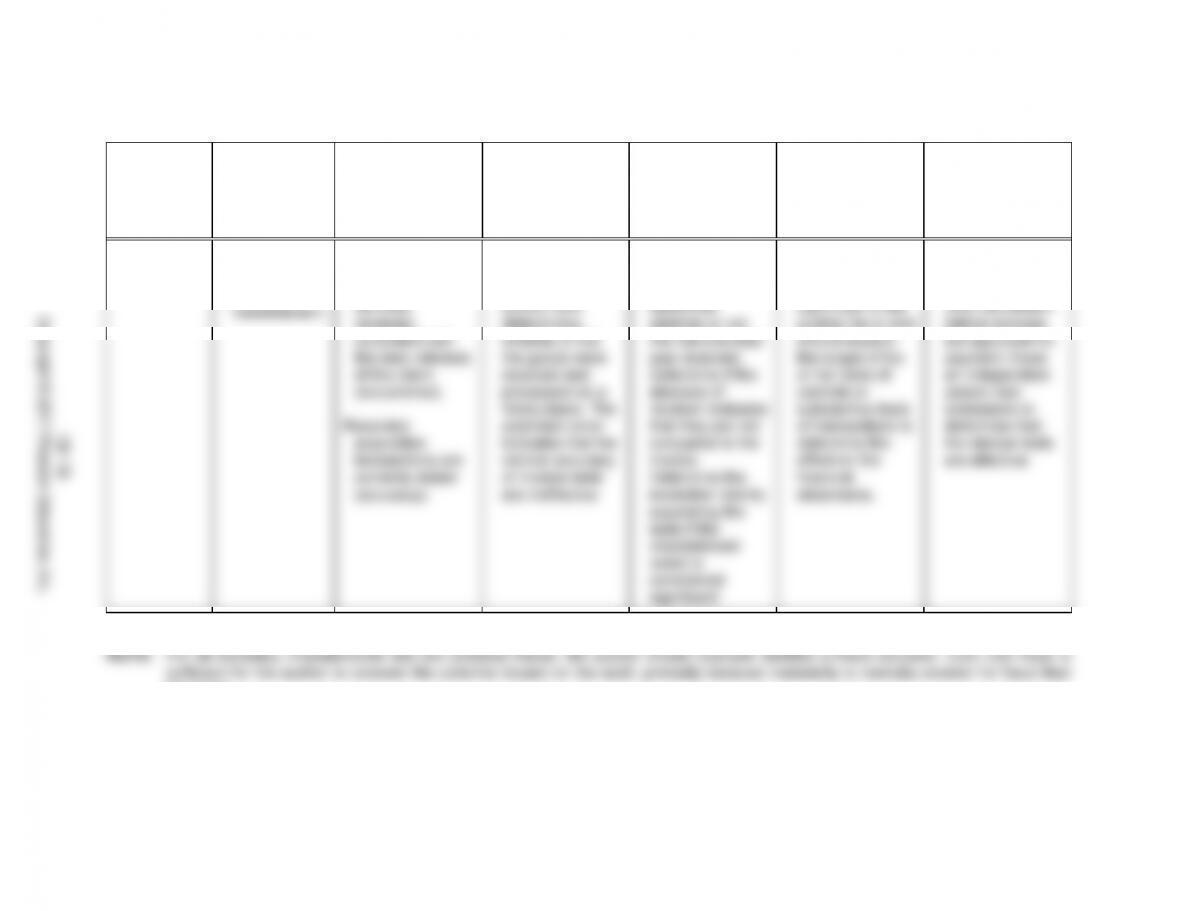

18–20

AUDIT

PROCEDURE

a.

TYPE OF

EVIDENCE

b.

TRANSACTION AUDIT

OBJECTIVE

c.

TEST OF

CONTROL OR

SUBSTANTIVE

TEST OF

TRANSACTION

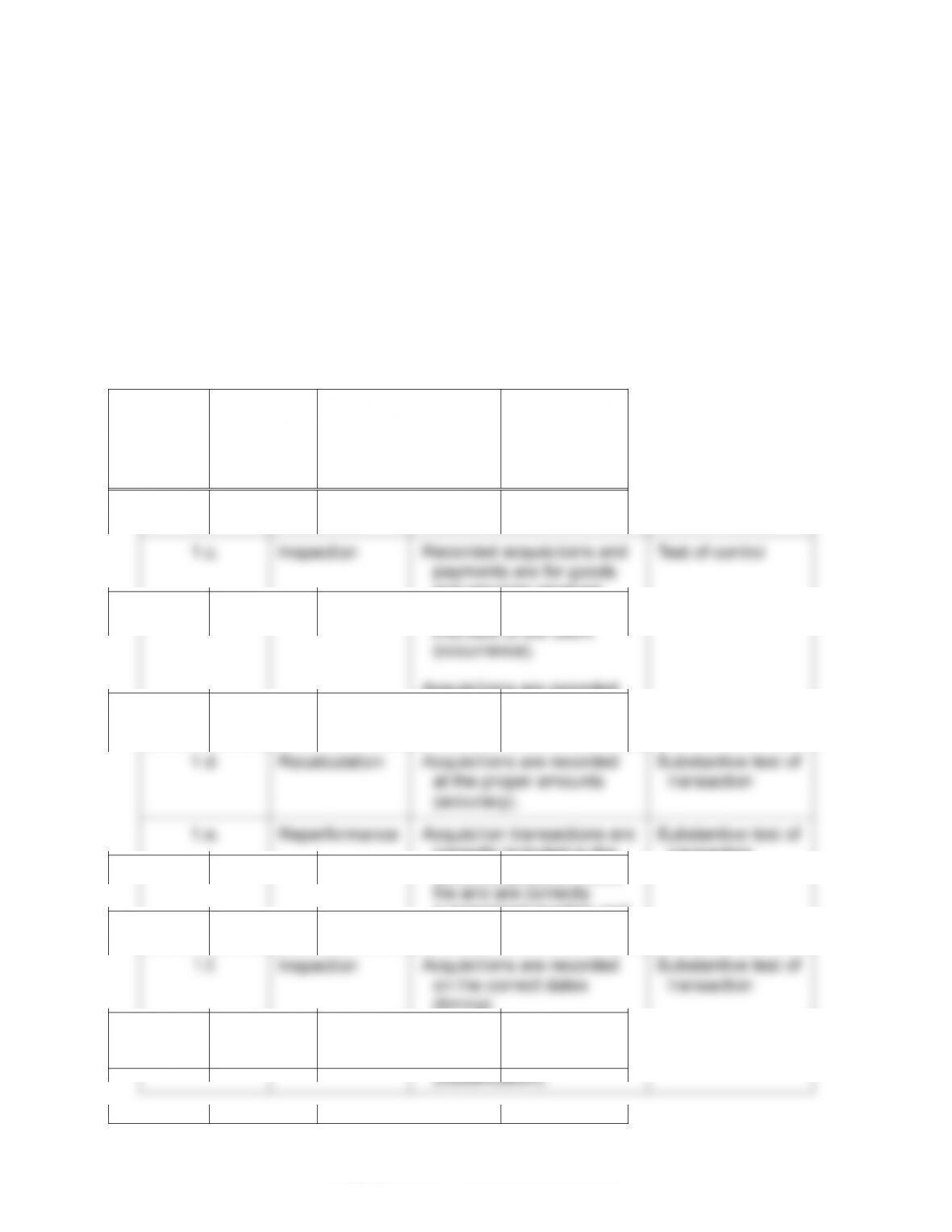

1.a.

Inspection

Recorded acquisitions and

payments are for goods

and services received,

consistent with the best

interests of the client

(occurrence).

Test of control

1.b.

Inspection

Recorded acquisitions and

payments are for goods

and services received,

consistent with the best

interests of the client

(occurrence).

Test of control

1.c.

Inspection

Recorded acquisitions and

payments are for goods

and services received,

consistent with the best

interests of the client

(occurrence).

Acquisitions are recorded

at the proper amounts

(accuracy).

Test of control

1.d.

Recalculation

Acquisitions are recorded

at the proper amounts

(accuracy).

Substantive test of

transaction

1.e.

Reperformance

Acquisition transactions are

correctly included in the

accounts payable master

file and are correctly

summarized (posting and

summarization).

Substantive test of

transaction

1.f.

Inspection

Acquisitions are recorded

on the correct dates

(timing).

Substantive test of

transaction

1.g.

Inspection

Acquisition transactions are

properly classified

(classification).

Substantive test of

transaction

18–20 (continued)

AUDIT

PROCEDURE

a.

TYPE OF

EVIDENCE

b.

TRANSACTION AUDIT

OBJECTIVE

c.

TEST OF

CONTROL OR

SUBSTANTIVE

TEST OF

TRANSACTION

2.

Inquiry

Recorded acquisitions and

payments are for goods

and services received,

consistent with the best

interests of the client

(occurrence).

Acquisitions are recorded at

the proper amounts

(accuracy).

Acquisitions are recorded

on the correct dates

(timing).

Test of control

3.

Analytical

procedure

Recorded acquisitions and

payments are for goods

and services received,

consistent with the best

interests of the client

(occurrence).

Acquisitions are recorded at

the proper amounts

(accuracy).

Substantive test of

transaction

4.

Recalculation

Acquisition transactions are

correctly included in the

accounts payable master

file and are correctly

summarized (posting and

summarization).

Substantive test of

transaction

5.

Inspection

Existing acquisitions are

recorded (completeness).

Substantive test of

transaction

18–21 a. Here are advantages for purchasing raw material jewelry items

online through supplier Web sites:

18-13

18–21 (continued)

Faster Delivery of Purchases. Because Donnen Designs

purchasing agents may be able to purchase raw material

More Product Information. Most jewelry suppliers post

pictures of the products for sale on the Internet. Thus, Donnen

b. Here are potential risks associated with online purchases of raw

material jewelry items:

Unauthorized Purchases Using Donnen Credit Cards. Given

that all online sales must be made using a company credit

cards but shipped to purchasing agent addresses.

Privacy Protection for Donnen Credit Cards. Because the

Inconsistent Product Quality. Because Donnen purchasing

agents will be buying products from a wide variety of new

Reliability of Supplier. Because Donnen purchasing agents

will be buying products from a wide variety of new vendors,

c. The primary advantage of allowing Donnen Designs purchasing

agents to acquire products using company credit cards is that the

d. The primary advantages of restricting purchases to only those

that can be paid by company check are that it (1) decreases the

18-14

18–21 (continued)

e. Suggested internal controls:

(1) To prevent purchasing agents from making unauthorized

purchases of non–jewelry items using Donnen credit cards,

the company could:

Request through the credit card agency that only

selected types of products are authorized for purchase

(2) To prevent purchasing agents from ordering jewelry items for

shipment to an agent’s home address, the company could:

Send all credit card billing statements directly to

accounting for reconciliation to receiving reports.

(3) To prevent a buildup of unused credits with online vendors

for returned goods, the company could:

Only allow purchases from selected online vendors

whose policies indicate that products may be returned

for credit to the credit card account.

18–22 a. The employees in this large government agency were purchasing

expensive items such as appliances, electronics, and even

vehicles, for themselves using agency funds. The fraud was

18-15

18–22 (continued)

An understaffed internal audit function

The agency had a reactive approach to fraud detection and

prevention rather than a proactive approach

The incentives of the agency employees to commit fraud included

the following:

The agency would lose any budget money that was not spent

by the end of the year, so this provided an incentive for

b. Data analytics can be used to detect fraud by enabling the auditor

to analyze large datasets more easily and to drill down into the

data. The auditor can easily disaggregate purchases by month, by

c. A fraud examiner could perform the following comparisons in order

to detect fraud related to a particular vendor:

Calculate year–to–year percentage changes in total purchases

from each vendor.

If there are multiple employees making purchases, calculate the

percentage of purchases made by each employee to each

If there is a spending limit, or a limit on the purchases that can

be made without a purchase order or supervisor approval,

18–23

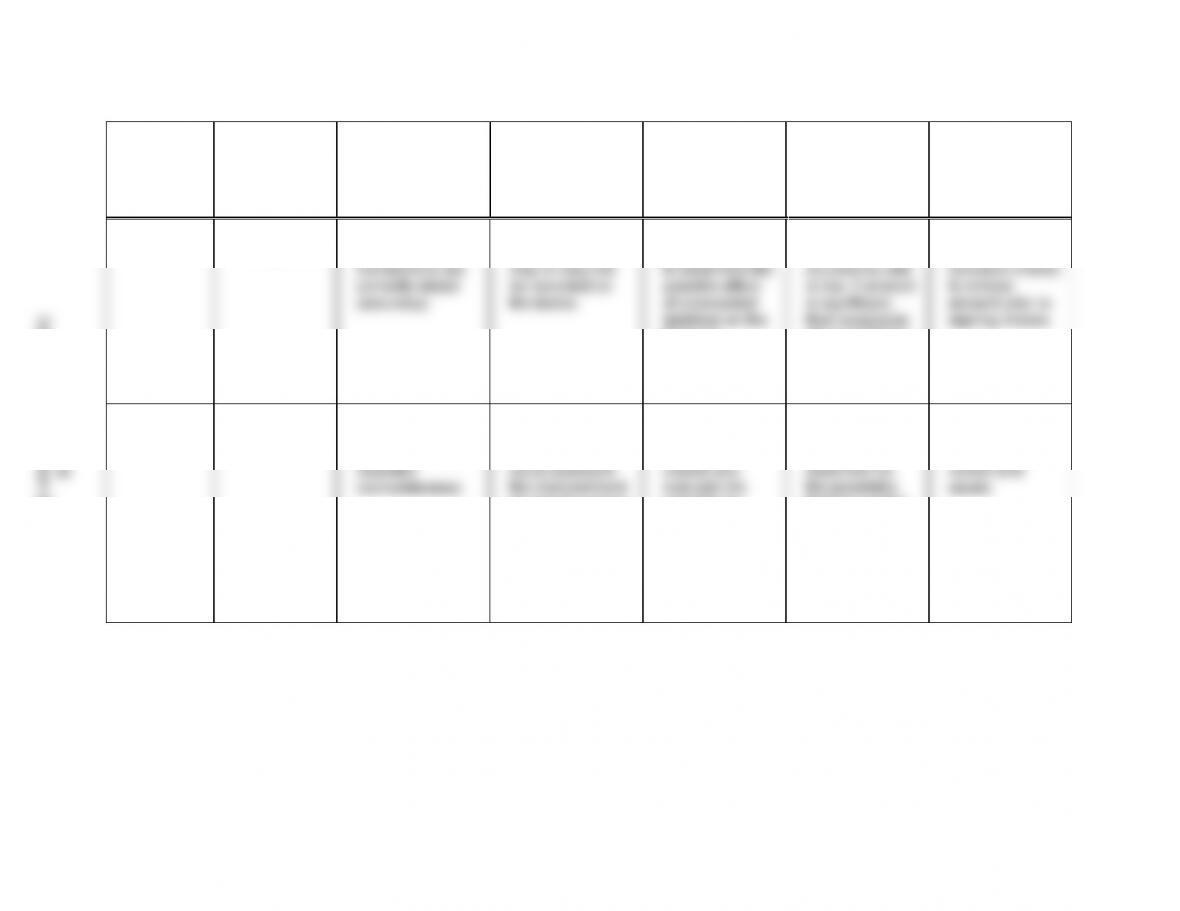

EXCEPTION

a.

TYPE OF

EXCEPTION

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE

NOT MET

c.

AUDIT

IMPORTANCE

d.

FOLLOW–UP

e.

EFFECT

ON AUDIT

f.

PREVENTIVE

CONTROLS

1

Monetary

misstatement

Recorded cash

disbursement

transactions are

correctly stated

(accuracy).

Results in $100

liability, which

may or may not

be recorded on

the books.

Investigate the

exception rate

to determine the

possible effect

of unrecorded

financial

statements.

Probably none,

since

occurrence rate

is low. If amount

is significant,

of reconciliation

of vendor

statements may

be appropriate.

An independent

person should

compare checks

to invoice

amount prior to

2

Control

deviation

Existing cash

disbursement

transactions are

recorded

(completeness).

The check may not

actually have

been voided. It

could represent

the disbursement

of cash if a check

was prepared.

Determine

company policy

for voided

checks and

evaluate the

potential for

unrecorded

checks.

Auditor should

examine the

bank cutoff

statement for

the possibility

that the voided

check and other

checks may

have been

issued and

cashed but not

recorded.

Require that all

voided checks

be properly

voided and

saved.

18–16

Copyright © 2017 Pearson Education, Inc.

18–23 (continued)

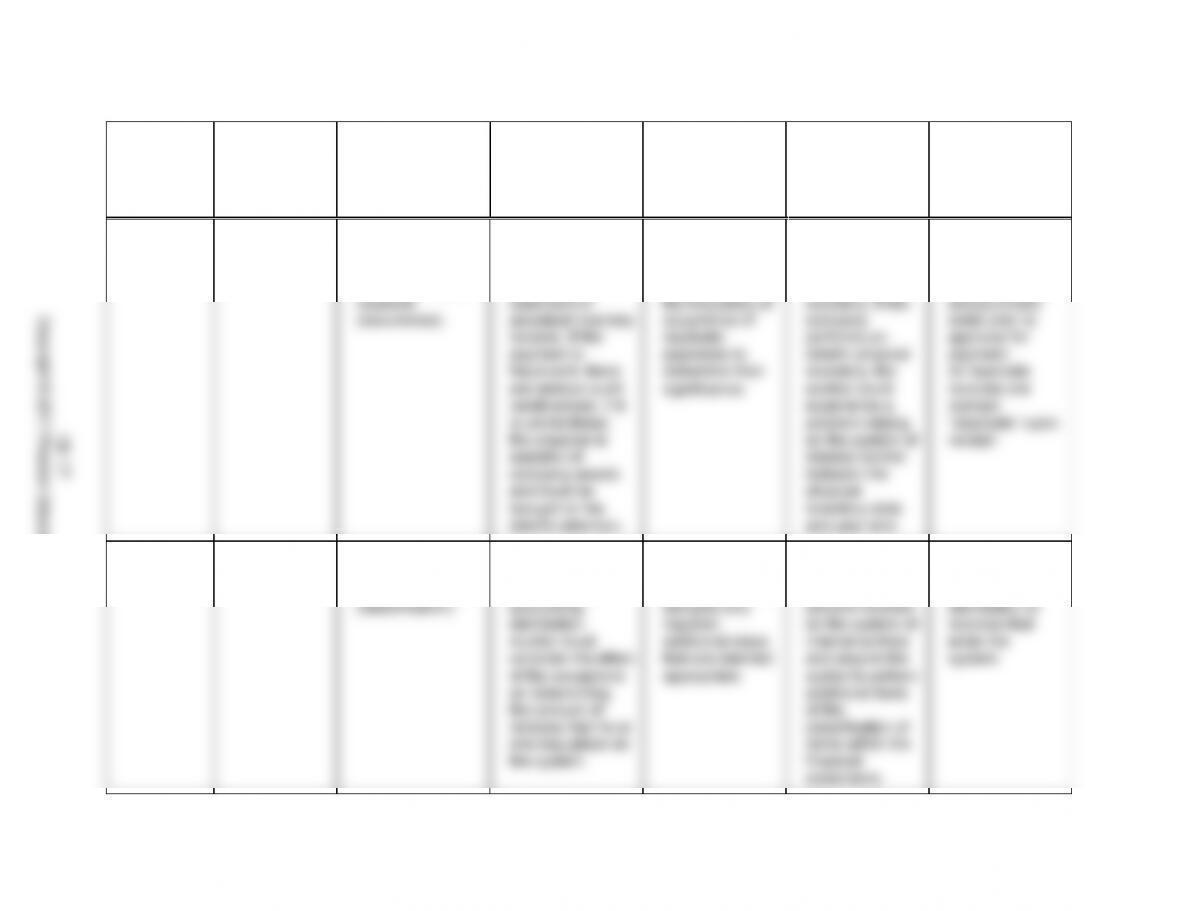

EXCEPTION

a.

TYPE OF

EXCEPTION

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE

NOT MET

c.

AUDIT

IMPORTANCE

d.

FOLLOW–UP

e.

EFFECT

ON AUDIT

f.

PREVENTIVE

CONTROLS

3

Monetary

misstatement

Recorded cash

disbursements

are for goods and

services actually

received

It could be a

fraudulent

payment or it could

result in an over–

statement of

records. If the

payment is

fraudulent, there

are serious audit

ramifications. If it

is unintentional,

the situation is

wasteful of

company assets

and must be

brought to the

client’s attention.

First determine

whether it is

fraudulent. If

not, investigate

the frequency of

duplicate

payments to

determine their

significance.

The duplicate

payments result

in recording of

nonexistent

inventory. If the

performs an

interim physical

inventory, the

auditor could

experience a

problem relying

on the system of

internal control

between the

physical

inventory date

and year–end.

Invoices must be

matched with

an original

receiving report

and purchase

approval for

payment.

All duplicate

invoices are

marked

“duplicate” upon

receipt.

4

Monetary

misstatement

Acquisition

transactions are

properly classified

(classification).

Indicates that no

one is effectively

reviewing the

accounting

distribution.

Auditor must

consider the effect

Determine the

significance of the

misclassifications

and plan any

required

additional steps

that are deemed

If considered

significant, the

exceptions could

prevent reliance

on the system of

internal controls

and require the

Have someone

review the

account

distribution of

invoices that

enter the

system.

18–17

Copyright © 2017 Pearson Education, Inc.

18–23 (continued)

EXCEPTION

a.

TYPE OF

EXCEPTION

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE

NOT MET

c.

AUDIT

IMPORTANCE

d.

FOLLOW–UP

e.

EFFECT

ON AUDIT

f.

PREVENTIVE

CONTROLS

5

Control

deviation

Recorded

acquisitions and

related cash

disbursements

are for goods

received,

consistent with

the best interests

of the client

(occurrence).

Indicates that the

controller is not

following the

procedure of

initialing

may indicate that

he or she is not

effectively

reviewing

invoices and

other supporting

documents prior

to payment.

Determine whether

or not the

controller is

effectively

reviewing

other supporting

documents.

If determination is

made that

controller does

not review

supporting

audit tests

should be

increased to

determine the

significance of

the deficiency.

A competent

independent

person should

review

supporting

approval of

controller and

test items to

determine

effectiveness of

controller’s

review.

6

Monetary

misstatement

Acquisition

transactions are

recorded on the

correct dates

(timing).

At the date of

the physical

inventory, this

situation will be

critical in that

any items

counted in

physical

inventory and not

recorded in the

acquisitions

journal will cause

an understated

Determine whether

or not this

situation persists

throughout the

year and whether

it is rectified at

physical

inventory date

and year–end.

Require expansion

of purchase

cutoff work

at physical

inventory date

and year–end.

Require that

copies of all

receiving reports

be routed directly

to accounting

and that

accounting

account for

numerical

sequence of

receiving reports

on a regular

basis.

18–18

Copyright © 2017 Pearson Education, Inc.

18–23 (continued)

EXCEPTION

a.

TYPE OF

EXCEPTION

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE

NOT MET

c.

AUDIT

IMPORTANCE

d.

FOLLOW–UP

e.

EFFECT

ON AUDIT

f.

PREVENTIVE

CONTROLS

7

Control

deviation and

Monetary

Recorded

acquisitions are

for goods and

services

received,

consistent with

the best interests

of the client

(occurrence).

Recorded

acquisition

transactions are

correctly stated

(accuracy).

Absence of

receiving reports

prevents the

auditor from

determining

whether or not

the goods were

received and

processed on a

timely basis. The

extension error

indicates that the

clerical accuracy

of invoice tests

are ineffective.

Obtain bill of

lading copy from

vendor to

determine

whether or not

the merchandise

was received.

Determine if the

absence of

receiver indicates

that they are not

compared to the

invoice.

Determine the

exception rate by

expanding the

tests if the

misstatement

noted is

considered

significant.

If either of the

problems is

considered

significant to the

auditor, he or she

should expand

the scope of his

or her tests of

controls or

substantive tests

of transactions to

determine the

effect on the

financial

statements.

Require that

copies of

receiving reports

must be present

before invoices

are approved for

payment. Have

an independent

person test

extensions to

determine that

the clerical tests

are effective.

18–19

Copyright © 2017 Pearson Education, Inc.

18–24

MISSTATEMENT

a.

TRANSACTION–

RELATED AUDIT

OBJECTIVE NOT MET

b.

PREVENTIVE

CONTROL

c.

SUBSTANTIVE

PROCEDURE

1

Cash disbursement

transactions are

recorded on the

correct dates

(timing).

Transactions are

recorded

automatically using

a computer process

with the same

information as the

check preparation.

Trace last checks

written to cash

disbursements

journal.

Examine date checks

cancelled at bank to

determine if checks

were held by the

client.

2

Acquisition

transactions are

recorded on the

correct dates

(timing).

Receiving reports to

be delivered to

accounting at the

end of the day on

which the raw

materials are

received.

Accounting

department

accounts for

numerical sequence

of receiving reports

after obtaining the

last number used

from receiving

personnel.

At the date on which

the cutoff test is to

be performed, the

auditor obtains the

number of the last

receiving report(s)

that should have

been recorded and

accounts for the

numerical sequence

of all previous

receiving report(s)

that should have

been recorded.

3

Recorded acquisitions

are for goods and

services received,

consistent with the

best interests of the

client (occurrence).

Require that an

authorized purchase

order and/or

approval of each

invoice by the

ordering department

head be required

before payments

are made for goods

received.

Examine underlying

documents for

reasonableness and

authenticity.