The last paragraph of the accountant’s review report

A) details the responsibilities of management.

B) details the responsibilities of the accountant.

C) expresses limited assurance in the form of negative assurance.

D) lists the analytical procedures performed.

Audit procedures designed to uncover credit sales made after the client’s fiscal year-end

that relate to the current year being audited provide evidence for which of the following

audit objectives?

A) realizable value

B) accuracy

C) cutoff

D) existence

Which of the following tests are typically not necessary when auditing a client’s

schedule of recorded disposals?

A) footing the schedule

B) tracing the totals on the schedule to the recorded disposals in the general ledger

C) tracing cost and accumulated depreciation of the disposals to the property master file

D) All of the above are necessary.

When a compensating control exists, the absence of a key control

A) is no longer a concern because there is no longer a significant deficiency or material

weakness.

B) is still a major concern to the auditor.

C) could cause a material loss, so it must be tested using substantive procedures.

D) is magnified and must be removed from the sampling process and examined in its

entirety.

Which of the following statements is most correct about an auditor’s required

communication with management and those charged with corporate governance?

A) The auditor is required to inform those charged with governance about significant

errors discovered and subsequently corrected by management.

B) Any significant matter reported to those charged with governance must also be

communicated to management.

C) Communication is required before the audit report is issued.

D) The auditor does not have any requirement to communicate with anyone other than

the company’s senior management.

After the auditor determines whether any conditions exist which require a departure

from a standard unmodified opinion audit report, the next step in the decision process is

to

A) write the report.

B) decide the materiality for each condition.

C) decide the appropriate type of report for the condition.

D) discuss the report with management.

You have been assigned to the accounts payable transaction cycle as part of your

auditing responsibilities. You have decided to vouch a sample of entries in the accounts

payable master file to supporting documents. Which assertion is this test of controls

most likely to support?

A) accuracy

B) classification

C) completeness

D) occurrence

The amount of time spent verifying owners’ equity is frequently minimal for closely

held corporations because

A) these companies are so small that it is not necessary to audit the capital section.

B) the few owners all have access to the books so the auditor spends more time on

accounts like liabilities, which affect outsiders.

C) there are few if any transactions during the year for the capital stock accounts,

except for earnings and dividends.

D) there is no public interest in these companies.

To obtain an understanding of an entity’s control environment, an auditor should

concentrate on the substance of management’s policies and procedures rather than their

form because

A) management may establish appropriate policies and procedures but not act on them.

B) the board of directors may not be aware of management’s attitude toward the control

environment.

C) the auditor may believe that the policies and procedures are inappropriate for that

particular entity.

D) the policies and procedures may be so weak that no reliance is contemplated by the

auditor.

The auditor’s responsibility section of the standard unmodified opinion audit report

states that the auditor is

A) responsible for the financial statements and the opinion on them.

B) responsible for the financial statements.

C) responsible for the opinion on the financial statements.

D) jointly responsible for the financial statements with management.

The auditor’s primary concern relative to presentation and disclosure-related objectives

is

A) accuracy.

B) existence.

C) completeness.

D) occurrence.

A financial institution sues the audit firm for failure to discover that a borrower’s

financial statements are materially misstated. This is an example of which of the

following legal liability concepts?

A) liability to clients

B) liability to third parties under common law

C) civil liability under federal securities law

D) criminal liability

Which of the following best describes the corporate minutes of an entity?

A) official record of the meetings of the board of directors and the stockholders

B) unofficial record of the meeting of the board of directors

C) official record of management meeting with investors and creditors of the company

D) unofficial record of the board of directors meetings

Which of the following is a correct statement regarding the shipment of goods?

A) The shipping document must be in paper form.

B) The shipping document is used to update the perpetual inventory records.

C) Only one copy of the shipping document is needed.

D) All of the above are correct statements.

The Sarbanes-Oxley Act requires

A) all public companies to issue reports on internal controls.

B) all public companies to define adequate internal controls.

C) the auditor of public companies to design effective internal controls.

D) the auditor of public companies to withdraw from an engagement if internal controls

are weak.

Which of the following is a factor that relates to incentives or pressures to commit

fraudulent financial reporting?

A) significant accounting estimates involving subjective judgments

B) excessive pressure for management to meet debt repayment requirements

C) management’s practice of making overly aggressive forecasts

D) high turnover of accounting, internal audit, and information technology staff

If a potential loss on a contingent liability is remote, the liability usually is

A) disclosed in footnotes, but not accrued.

B) neither accrued nor disclosed in footnotes.

C) accrued and indicated in the body of the financial statements.

D) disclosed in the auditor’s report but not disclosed on the financial statements.

The principal issue in cases involving alleged negligence is usually

A) if an engagement letter was issued.

B) the level of care required.

C) if fraud was committed by upper-level management.

D) whether the auditor is liable under civil or criminal laws.

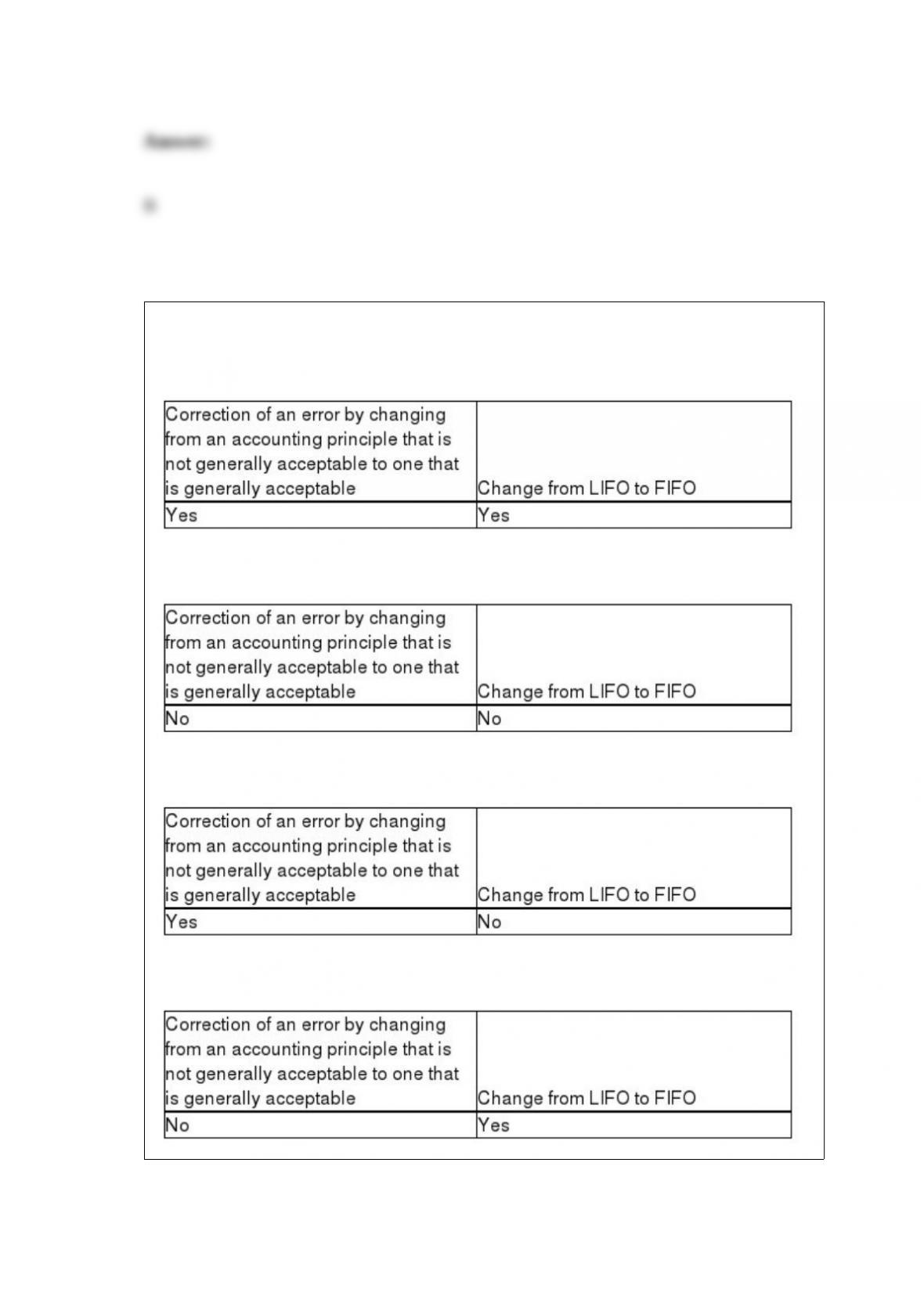

Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

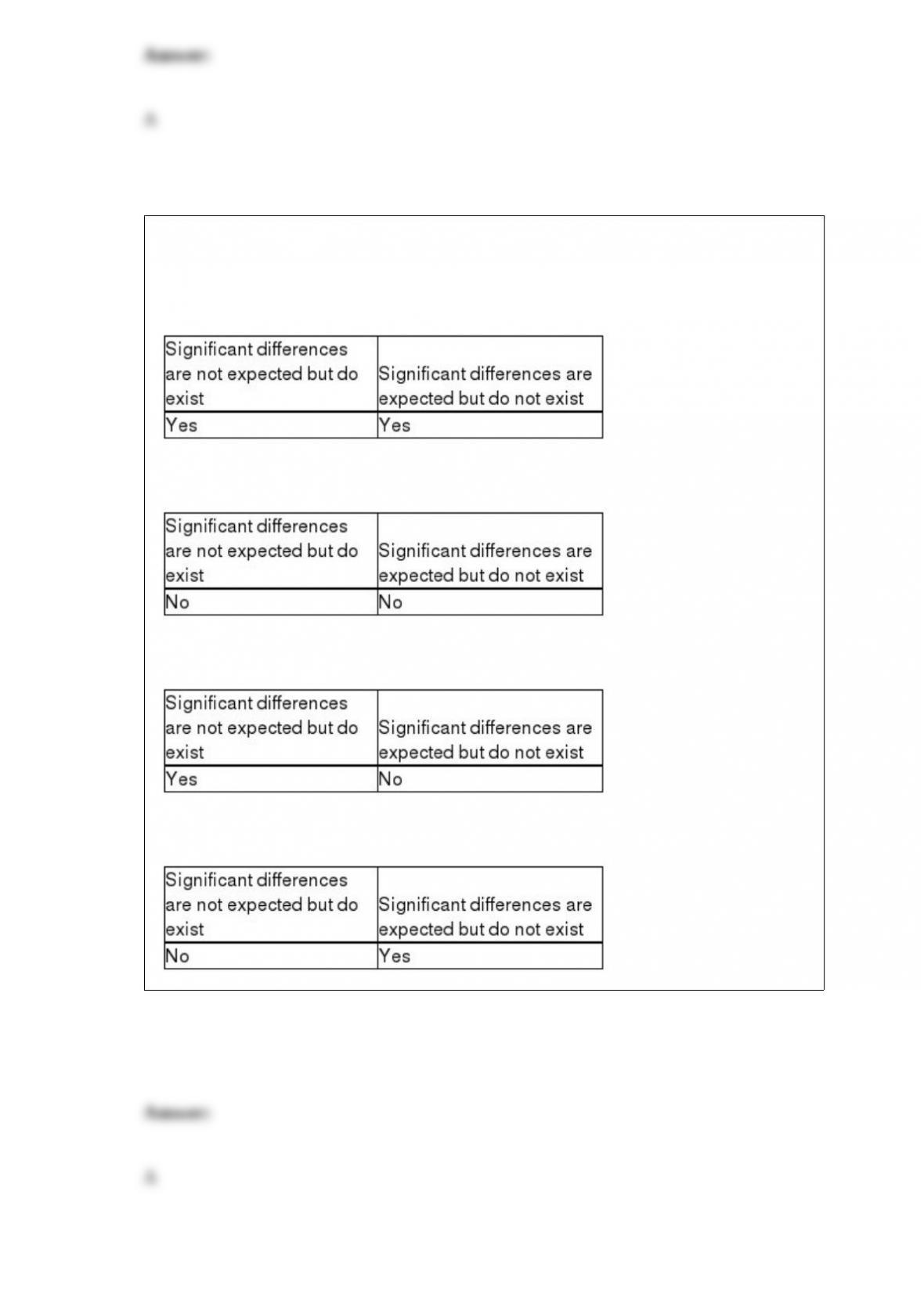

Audit procedures can result in significant, unexpected differences. The auditor should

investigate further if

A)

B)

C)

D)

Which of the following is not considered a commitment?

A) agreements to purchase raw materials

B) pension plans

C) agreements to lease facilities at set prices

D) Each of the above is a commitment.

When the auditor uses tracing as an audit procedure for tests of transactions, she is

primarily concerned with which audit objective?

A) occurrence

B) completeness

C) cutoff

D) classification

Sarbanes-Oxley and the Securities and Exchange Commission restrict auditors from

providing many consulting services to their publicly traded audit clients. Which of the

following is true for auditors of publicly traded companies?

I. They are restricted from providing consulting services to privately held companies.

II. There is no restriction on providing consulting services to non-audit clients.

A) I only

B) II only

C) I and II

D) Neither I nor II

The starting point to effective professional judgment begins with

A) gathering the facts.

B) identifying alternatives.

C) identifying relevant literature.

D) identifying and defining the issue.

The internal control that requires that “checks are prenumbered and accounted for”

satisfies the objective of

A) accuracy.

B) existence.

C) completeness.

D) posting and summarization.

Which of the following needs to be considered when the auditor generalizes from the

sample to the population?

A)

B)

C)

D)

Any company with stock listed on a securities exchange is required to engage a(n)

A) equity analyst.

B) stock transfer agent.

C) independent registrar.

D) equity placement specialist.

A common way for a CPA firm to demonstrate a lack of duty to perform is by use of

a(n)

A) expert witness’ testimony.

B) engagement letter.

C) management representation letter.

D) confirmation letter.

Which of the following can affect the independence of operational auditors?

A)

B)

C)

D)

Supporting schedules

A) must be prepared by the auditor.

B) make up the largest portion of audit documentation.

C) must consist of either reconciliation of amounts or substantive analytical procedures.

D) all of the above

Auditor confirmation of accounts payable balances at the balance sheet date may not

need to be performed by the auditor because

A) this is a duplication of cutoff tests.

B) there is likely to be other reliable external evidence available to support the balances.

C) accounts payable balances at the balance sheet date may not be paid before the audit

is completed.

D) correspondence with the audit client’s attorney will reveal all legal action by vendors

for nonpayment.

A(n) ________ is the detailed instruction that explains the audit evidence to be obtained

during the audit.

A) audit objective

B) audit procedure

C) audit assertion

D) audit program

PPS samples can be obtained in an efficient manner using all but which of the

following?

A) hand selection by the auditor

B) computer software

C) random number tables

D) systematic sampling techniques