The auditors determine which disclosures must be presented in the financial statements.

The phrase “Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free from material

error” is included in the auditor’s opinion section of an audit report.

Professional guidelines for performing internal audits for companies are not as

well-defined as for external audits.

A suspension of judgment is the recognition that people’s motivations and perceptions

can lead them to provide biased or misleading information.

When the estimated population exception rate exceeds the sample exception rate, the

auditor can conclude that the sample results do not support the preliminary assessed

control risk.

Management must recognize that almost any employee is capable of committing a

dishonest act under the right circumstances.

It is generally more difficult for the auditor to detect payment of fraudulent hours than

payment of fictitious employees.

Most people define unethical behavior as conduct that differs from what they believe is

appropriate given the circumstances.

CPAs must be independent to issue a compilation report.

Users of the financial statements rely on the auditor’s report because of the absolute

assurance the report provides.

When the auditor receives inconsistent responses from management and others within

the organization, the auditor should obtain additional audit evidence to resolve the

inconsistency.

Turnover in accounting personnel can create a rationalization for misstatement.

Changes in accounting estimates requires the auditor to issue a modified audit report

with a consistency paragraph inserted after the opinion paragraph.

All litigation by a client related to tax or other nonaudit services will impair

independence.

Of the three types of attestation engagements, examination engagements provide a

higher level of assurance than agreed-upon procedures engagements but less than

review engagements.

The most widely used profitability ratio is the gross profit percent.

A financial statement review conducted in compliance with Statements on Standards for

Accounting and Review Services (SSARS) includes obtaining an understanding of

internal control.

The audit procedure “Perform tests of lower-of-cost-or-market, selling price, and

obsolescence” provides assurance mainly for the realizable value objective for

inventory pricing and compilation.

Acceptable risk of incorrect acceptance is directly affected by acceptable audit risk.

Credit should be approved before goods are shipped to a customer.

A misstatement of an expense account usually also results in an equal misstatement of

accounts receivable.

The introductory paragraph of the auditor’s report states that the auditor is responsible

for the preparation, presentation and opinion on financial statements.

Key controls are not sufficient to achieve the transaction-related audit objectives.

Both accountants and auditors must possess expertise in the accumulation and

interpretation of audit evidence.

Auditors typically perform the acquisitions and cash disbursements tests at different

times.

Risk assessment procedures are performed to assess the risk of material misstatement in

the financial statements.

An auditor will issue a disclaimer when he concludes that the financial statements are

not fairly presented.

The auditor is generally concerned about the realizable value and the rights to cash.

Independence is a fundamental ethical principle for internal auditors.

In job cost systems, costs are accumulated by individual jobs.

When using nonstatistical sampling, the sample must be a probabilistic one.

Ordinarily, if you are auditing a continuing client, it is unnecessary to test the accuracy

objective or the classification objective for fixed assets acquired in prior years.

The auditor should keep in mind that the amount in insurance expense is a residual

amount.

Other accrued expenses are normally considered to be associated with the acquisition

and payment cycle.

One of the most challenging parts of auditing is properly applying the factors that affect

tests of details of balances.

When using MUS, the projected misstatement is the percentage misstatement times the

sampling interval.

When auditing the payroll and personnel cycle, tests of controls are routinely

performed.

Under the Confidential Client Information rule, permission is not required from the

client to use the audit documentation relating to that client during an AICPA authorized

peer review program with another CPA firm.

Procedures to obtain an understanding of internal control generally provide sufficient

appropriate evidence that a control is operating effectively.

Most closely held corporations have numerous transactions during the year for capital

stock accounts.

Which of the following is not a function within the inventory and warehousing cycle?

A) process the goods

B) store raw materials

C) ship finished goods

D) process invoices for shipped goods

Boxes or other containers holding inventory should also be opened during test counts to

determine the ________ of the inventory.

A) classification

B) detail tie-in

C) existence

D) realizable value

Which of the following is not a characteristic of the reliability of evidence?

A) effectiveness of client internal controls

B) education of auditor

C) independence of information provider

D) timeliness

Analytical procedures are so important that they are required during the

A) planning and test of control phases.

B) planning and completion phases.

C) test of control and completion phases.

D) planning, test of control, and completion phases.

Factors that impact inherent risk of financial instruments donot include

A) management’s objectives related to investment activity.

B) the complexity of the securities.

C) the cost of the securities.

D) the company’s prior experience with certain investments.

Cash receipts from sales on account have been misappropriated. Which of the following

acts would conceal this fraud and be least likely to be detected by an auditor?

A) understating the sales journal by not recording cash sales

B) overstating the accounts receivable control account by intentionally misstating prices

charged for goods sold

C) overstating the accounts receivable subsidiary ledger by not recording payments

made by customers

D) understating the cash receipts journal by purposely recording incorrect amounts

Which of the following is not one of the AICPA categories of assertions?

A) assertions about classes of transactions and events for the period under audit

B) assertions about financial statements and correspondence to GAAP

C) assertions about account balances at period end

D) assertions about presentation and disclosure

Which of the following would least concern an auditor regarding the lack of a specific

authorization to conduct the sales transaction?

A) granting of credit

B) shipment of goods

C) determination of discounts

D) selling of goods for cash

Interpretations of the AICPA Code of Professional Conduct are dominated by the

concept of

A) independence.

B) compliance with standards.

C) accounting.

D) acts discreditable to the profession.

How must significant deficiencies and material weaknesses be communicated to those

charged with governance?

A) Either oral or written communication is acceptable.

B) Oral communication is required.

C) Written communication is required.

D) Written communication is required for material weaknesses, but oral communication

is allowed for significant deficiencies.

Which of the following is an accurate statement relating to separation of duties?

A) Management should deny cash access to anyone responsible for entering sales and

cash receipts transaction information into the computer.

B) All disagreements on the monthly statements should be directed to a designated

person who has no responsibility for handling cash or recording sales or accounts

receivable.

C) The credit granting function should be separate from the sales function.

D) All of the above are accurate statements.

Which is usually included in the engagement letter?

A)

B)

C)

D)

The posting and summarization audit objective is the auditor’s counterpart to

management’s assertion of

A) occurrence.

B) completeness.

C) accuracy.

D) classification.

As directed by the Sarbanes-Oxley Act,

A) an attorney must report material violations of federal securities law to the public

company’s chief legal counsel or chief executive officer.

B) attorneys cannot breach confidentiality rules even if a client is committing a crime or

a fraud.

C) if the audit committee fails to remedy any material violations of the federal

securities law, the attorney must report the violation to the SEC.

D) All of the above are required by Sarbanes-Oxley.

Which of the following occurrences would be least likely to warrant further audit

attention for the auditor?

A) deviations from client’s established control procedures

B) deviations from client’s budgeted values

C) monetary misstatements in populations of transaction data

D) monetary misstatements in populations of account balance details

The tests of details of balances procedure which requires the auditor to examine notes

paid after year-end to determine whether they were liabilities at the balance sheet date is

an attempt to satisfy the audit objective of

A) existence.

B) completeness.

C) accuracy.

D) classification.

You are gathering evidence for the audit objective that existing inventory items are

included in the inventory listing schedule. The audit procedure that would provide you

with the best evidence to confirm this objective is

A) trace from inventory tags to the inventory listing schedule and make sure the

inventory on the tags is included.

B) trace the inventory totals to the general ledger.

C) perform tests of lower-of-cost-or-market.

D) account for unused tags shown in the auditor’s documentation to make sure no tags

have been added.

Auditors typically rely on internal controls of their private company clients

A) only as needed to complete the audit and satisfy Sarbanes-Oxley requirements.

B) only if the controls are determined to be effective.

C) only if the client asks an auditor to test controls.

D) only if the controls are sufficient to increase control risk to an acceptable level.

An agreed-upon procedures engagement is one in which

A) the CPA and management agree that procedures will be applied to all accounts and

circumstances.

B) the CPA and management agree that procedures will not be applied to all accounts

and circumstances.

C) the CPA, the responsible party making the assertions, and the specific persons who

are the intended users of the CPA’s report agree to all the procedures the CPA will

perform.

D) the CPA, the responsible party making the assertions, and the specific persons who

are the intended users of the CPA’s report agree that the CPA will apply his judgment to

determine the procedures to be performed.

You are auditing Nelson and Company and determined that the sample results support a

conclusion that the account is materially misstated, when in fact it was not misstated.

This illustrates the risk of

A) incorrect acceptance.

B) incorrect rejection.

C) control risk too low.

D) control risk too high.

Match six of the terms (a-j) with the definitions provided below (1-6):

a. Application controls

b. Error listing

c. General controls

d. Hardware controls

e. Input controls

f. Output controls

g Parallel simulation

h. Parallel testing

i Pilot testing

j. Processing controls

________ 1. The new and old systems operate simultaneously in all locations.

________ 2. Controls that relate to all aspects of the IT system.

________ 3. Controls such as review of data for reasonableness, designed to assure that

data generated by the computer is valid, accurate, complete, and distributed only to

authorized people.

________ 4. Controls that apply to processing of transactions.

________ 5. A new system is implemented in one part of the organization while other

locations continue to rely on the old system.

________ 6. Controls such as proper authorization of documents, check digits, and

adequate documentation, designed to assure that the information to be entered into the

computer is authorized, complete, and accurate.

You are the in-charge auditor for a company who has been an audit client for several

years. Which of the following is not a category of tests commonly associated with the

audit of manufacturing equipment?

A) verification of depreciation expense

B) analytical procedures

C) verification of current-period disposals

D) verification of the beginning balance in the equipment account

The PCAOB considers International Standards on Auditing (ISA) when developing its

standards.

A CPA firm

A) can sell securities to a client for whom they perform an attestation service.

B) can receive a commission for a client that they are engaged to perform an attestation

service for.

C) cannot receive a referral fee for recommending the services of another CPA.

D) can receive a commission from a nonattestation client as long as the situation is

disclosed.

A principal advantage of statistical methods of attributes sampling over nonstatistical

methods is that they provide a quantifiable basis for establishing the

A) risk of assessing control risk too low.

B) tolerable exception rate.

C) expected population exception rate.

D) sample size.

Which of the following is an accurate statement concerning the auditor’s responsibility

to consider laws and regulations?

A) Auditors can follow an easy, step-by-step procedure to determine how laws and

regulations impact the financial statements.

B) The auditor’s responsibility will depend on whether the laws or regulations are

expected to have a direct impact on the financial statements.

C) It is the responsibility of the auditor to determine if an act constitutes

noncompliance.

D) The auditor must inform an outside party if management has knowingly not

complied with a law or regulation.

Which of the following is a correct statement regarding analytical procedures?

A) If an auditor identifies a possible misstatement in sales using analytical procedures,

accounts payable will be the likely offsetting misstatement.

B) Auditors should also compare the results of their analytical procedures to budgets

and industry trends.

C) If sales are overstated, the income statement will be incorrect, but the balance sheet

will be correct.

D) If an analytical procedure uncovers an unusual fluctuation, the auditor must assume

fraud is involved.

Which of the following is(are) true concerning the Ethical Principles of the Code of

Professional Conduct?

I. They identify ideal conduct.

II. They are general ideals and are not enforceable.

A) I only

B) II only

C) I and II

D) Neither I nor II

The form that must be filed with the Securities and Exchange Commission whenever a

company plans to issue new securities to the public is the

A) Form S-1.

B) Form 8-K.

C) Form 10-K.

D) Form 10-Q.

Which of the following ratios is not a measure of a company’s short-term debt paying

ability?

A) accounts receivable turnover

B) cash ratio

C) current ratio

D) quick ratio

List and describe the six organizational structures available to CPA firms.

Describe each of the following types of confirmations:

– positive confirmation

– blank confirmation

– invoice confirmation

– negative confirmation

Describe the audit procedures typically used to test for out-of-period liabilities (also

referred to as the search for unrecorded accounts payable).

Discuss the differences and similarities between the roles of accountants and auditors.

What additional expertise must an auditor possess beyond that of an accountant?

Consider the steps in sampling for tests of details and for tests of controls. Explain the

differences in applying sampling to these two types of tests.

Describe each of the major types of cash accounts maintained by business entities.

How do auditors commonly verify sales commission expense?

State the four most important audit objectives for capital stock and describe how the

auditor typically verifies each of the four objectives.

List the four underlying principles of risk assessment per the COSO framework

Auditors should be alert for potential judgment tendencies, traps, and biases that may

impact their decision making process. Identify and define four of these judgment

tendencies. Then, for each judgment tendency, suggest a way to avoid or mitigate the

tendency.

The text suggested a five-step approach to identify deficiencies, significant deficiencies,

and material weaknesses. Describe this approach.

Discuss the four areas of responsibility under the IT function that should be segregated

in large companies.

Discuss the key internal controls for prepaid insurance that affect the auditor’s extent of

testing of the prepaid insurance account.

List six accounts in the capital acquisition and repayment cycle commonly found on

balance sheets of corporations. What characteristics do these accounts have in common

that distinguish them from other accounts?

Discuss the required communications between predecessor and successor auditors.

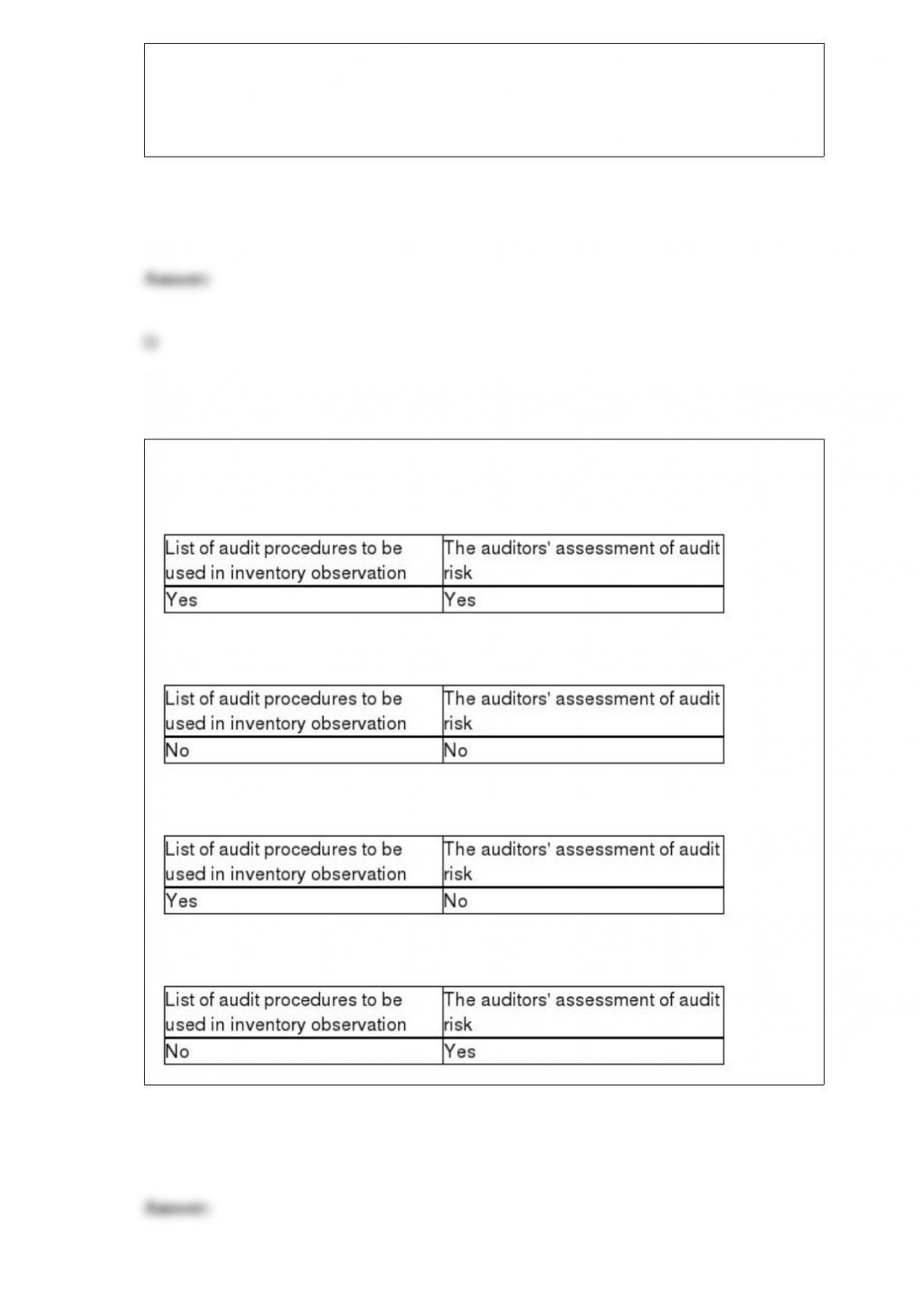

In auditing the long-term investments account, Arens, CPA, is unable to obtain audited

financial statements for an investee located in a foreign country. Levine concludes

sufficient appropriate audit evidence regarding this investment cannot be obtained.

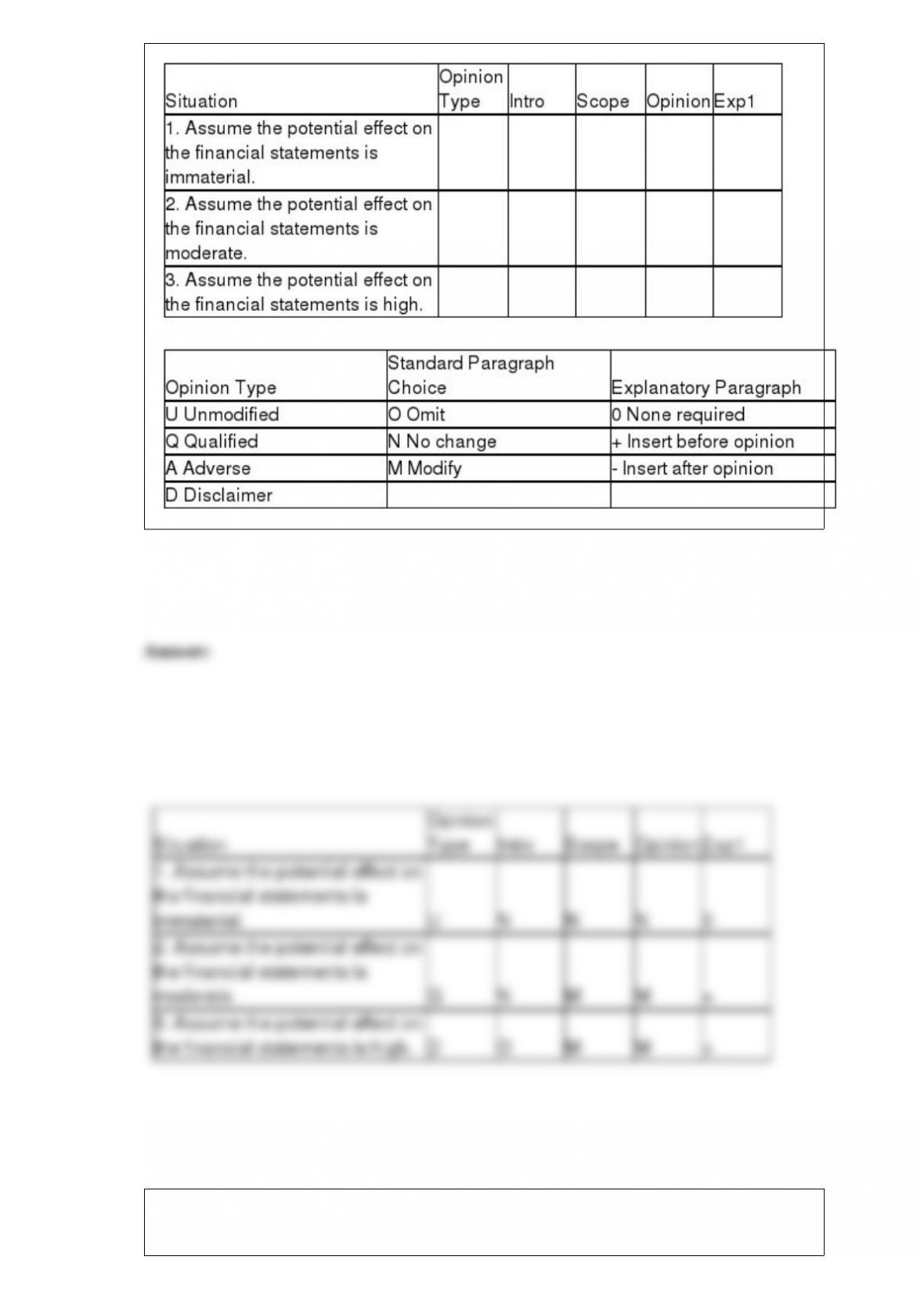

For each of the following situations below, identify the appropriate opinion type and

report modification by selecting a choice from the appropriate tables below.

Operational auditing is the review of an organization for efficiency and effectiveness.

Discuss what is meant by the terms “effectiveness” and “efficiency.”

The “tone at the top” provides a foundation upon which a more detailed code of conduct

can be developed to provide specific guidance for the organization and its employees.

Components of a code of conduct may include sections on 1) general employee

conduct, 2) relationships with clients and suppliers and 3) conflicts of interest. Give a

narrative description of what might be included in each of the above components of a

code of conduct.