The bank reconciliation

A) must be done on a daily basis if the client uses electronic banking.

B) should be performed by someone independent of the handling or recording of cash

receipts.

C) should be performed by someone who handles cash disbursements.

D) ensures that no cash has been embezzled.

Which of the following best describes effective internal control over payroll?

A) The preparation of the payroll must be under the control of the personnel

department.

B) The confidentiality of employee payroll data should be carefully protected to prevent

fraud.

C) The duties of hiring, payroll computation, and payment to employees should be

segregated.

D) The payment of cash to employees should be replaced with payment by checks.

A CPA firm can issue a compilation report

A) only if the partners are independent.

B) only if all the partners and the staff in the office performing the engagement are

independent.

C) if the partners have no material or direct immaterial interest in client.

D) even if it is not independent.

Which of the following is not an element of the examination of prospective financial

statements?

A) evaluating the preparation of the prospective financial statements

B) understanding internal controls

C) evaluating the support underlying the assumptions

D) issuing an examination report

Which of the following scenarios does not result in a qualified opinion?

A) A scope limitation prevents the auditor from completing an important audit

procedure.

B) Circumstances exist that prevent the auditor from conducting a complete audit.

C) The auditor lacks independence with respect to the audited entity.

D) An accounting principle at variance with GAAP is used.

Match seven of the terms (a-o) with the descriptions/definitions provided below (1-7):

a. compliance audit

b. economy and efficiency audit

c. effectiveness

d. efficiency

e. functional audit

f. Government Auditing Standards

g. government audit

h. Institute of Internal Auditors

i. operational auditing

j. organizational audit

k. program audit

l. Single Audit Act

m. special assignment

n. IIA Practice Standards

o. Statements on Internal Auditing Standards

________ 1. the official title of the Yellow Book

________ 2. a management request for an operational audit for a specific purpose, such

as investigating the possibility of fraud in a division or making recommendations for

reducing the cost of a manufactured product

________ 3. a government audit to determine whether an entity is acquiring, protecting,

and using its resources economically and efficiently and whether the entity has

complied with laws and regulations concerning such matters

________ 4. the degree to which the organization’s objectives are accomplished

________ 5. the review of an organization for efficiency and effectiveness

________ 6. federal legislation that provides for a single coordinated audit to satisfy the

audit requirements of all federal funding agencies

________ 7. statements issued by the Internal Auditing Standards Board of the Institute

of Internal Auditors (IIA) to provide authoritative interpretation of the Institute of

Internal Auditors’ Practice Standards

A management representation letter is

A) prepared on the CPA’s letterhead.

B) addressed to the client.

C) signed by high-level corporate officials.

D) dated as of the balance sheet date.

Which of the following is not a primary consideration when assessing inherent risk?

A) nature of client’s business

B) existence of related parties

C) effectiveness of internal controls

D) susceptibility to misappropriation of assets

Which of the following is not a general control?

A) Computer performed validation tests of input accuracy.

B) Equipment failure causes error messages on monitor.

C) There is a separation of duties between programmer and operators.

D) There are adequate program run instructions for operating the computer.

The most important output control is

A) distribution control, which assures that only authorized personnel receive the reports

generated by the system.

B) review of data for reasonableness by someone who knows what the output should

look like.

C) control totals, which are used to verify that the computer’s results are correct.

D) logic tests, which verify that no mistakes were made in processing.

For which of the following accounts is cutoff least important?

A) sales

B) sales returns and allowances

C) cash collections

D) inventory

Methods used to determine if there are legal encumbrances related to fixed assets

include all but which of the following?

A) Read the terms of loan and credit agreements.

B) Send loan confirmation requests to banks and other lending institutions.

C) Have discussions with the client or send letters to legal counsel.

D) All of the above may be used to identify legal encumbrances.

To ensure proper segregation of duties, who should maintain the perpetual inventory

master files?

A) production personnel

B) inventory storeroom personnel

C) inventory receiving personnel

D) accounting department personnel

In monetary unit sampling, the relationship between tolerable misstatement size and

required sample size is

A) direct.

B) inverse.

C) varied.

D) indeterminable.

An auditor needs to determine whether all customers of an electric utility company are

being billed. The auditor should test from the

A) sales register to the accounts receivable ledger.

B) sales register to the meter department records.

C) accounts receivable ledger to the sales register.

D) meter department records to the sales register.

Which deficiency exists if a necessary control is missing or not properly implemented?

A) control

B) significant

C) design

D) operating

For sales, the occurrence transaction-related audit objective affects which of the

following balance-related audit objectives?

A) existence

B) completeness

C) rights

D) detail tie-in

With which of management’s assertions with respect to implementing internal controls

is the auditor primarily concerned?

A) efficiency of operations

B) reliability of financial reporting

C) effectiveness of operations

D) compliance with applicable laws and regulations

An auditor who audits a business cycle that has low inherent risk should

A) increase the amount of audit evidence gathered.

B) assign more experienced staff to that area.

C) expand planning procedures.

D) do none of the above.

Which of the following statements relating to the competence of evidential matter is

always true?

A) Evidence from outside an enterprise is always reliable.

B) Accounting data developed under satisfactory conditions of internal control is not

reliable.

C) Oral representations made by management are not reliable evidence.

D) Evidence must be both reliable and relevant to be considered appropriate.

When determining the methodology for designing tests of details of balances for

accounts payable,

A) the focus by many companies on improving their supply-chain management

activities has led to numerous changes in the design of systems used to initiate and

record acquisition and payment activities.

B) it is relatively inexpensive to audit accounts payable.

C) performance materiality for accounts payable is set relatively low.

D) inherent risk is often set at low.

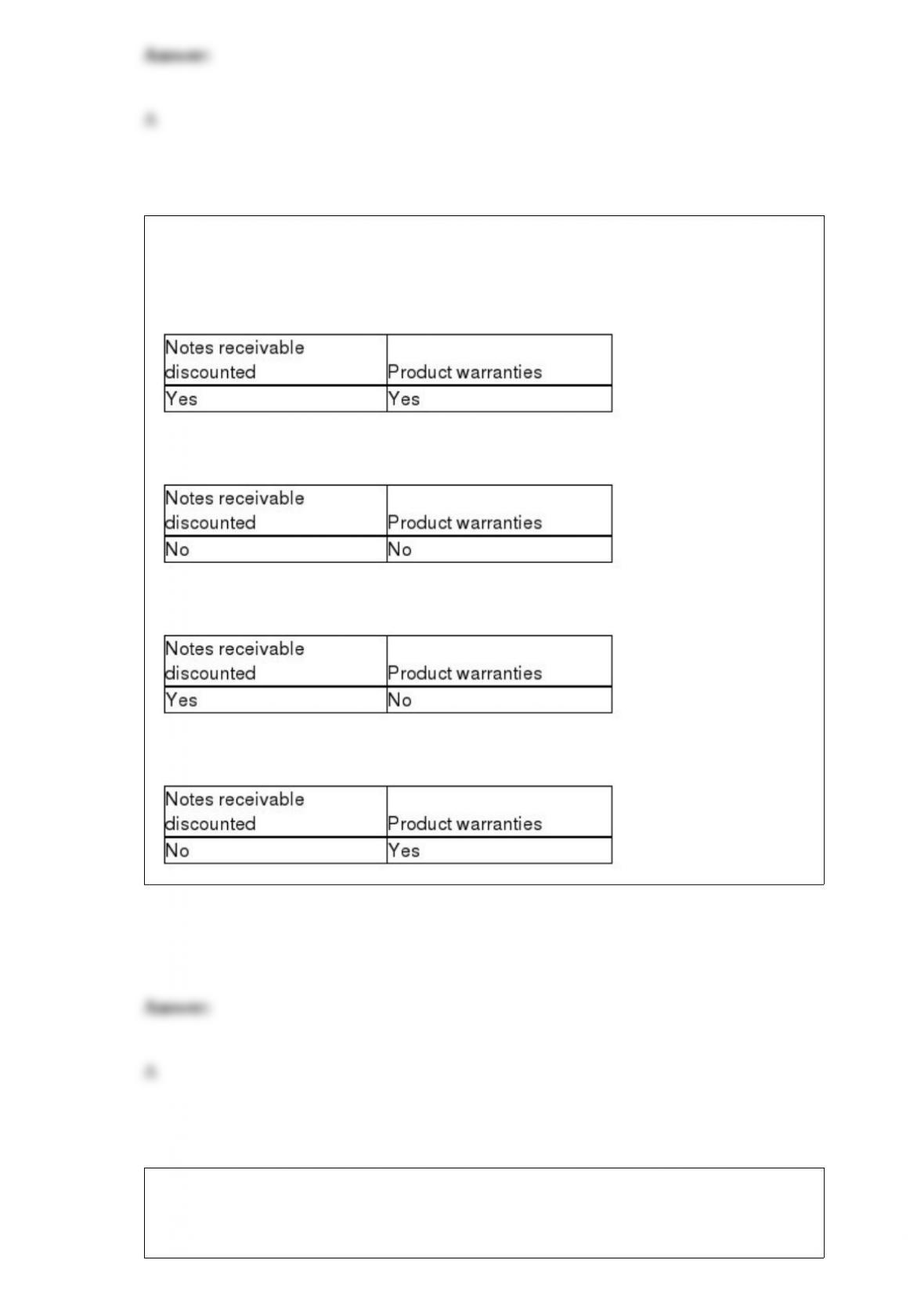

Which of the following is a contingent liability with which an auditor is particularly

concerned?

A)

B)

C)

D)

Which of the following is a risk assessment principle?

A) accountability

B) use relevant, quality information to support the functioning of internal controls

C) consider the potential for fraud

D) develop general controls over technology

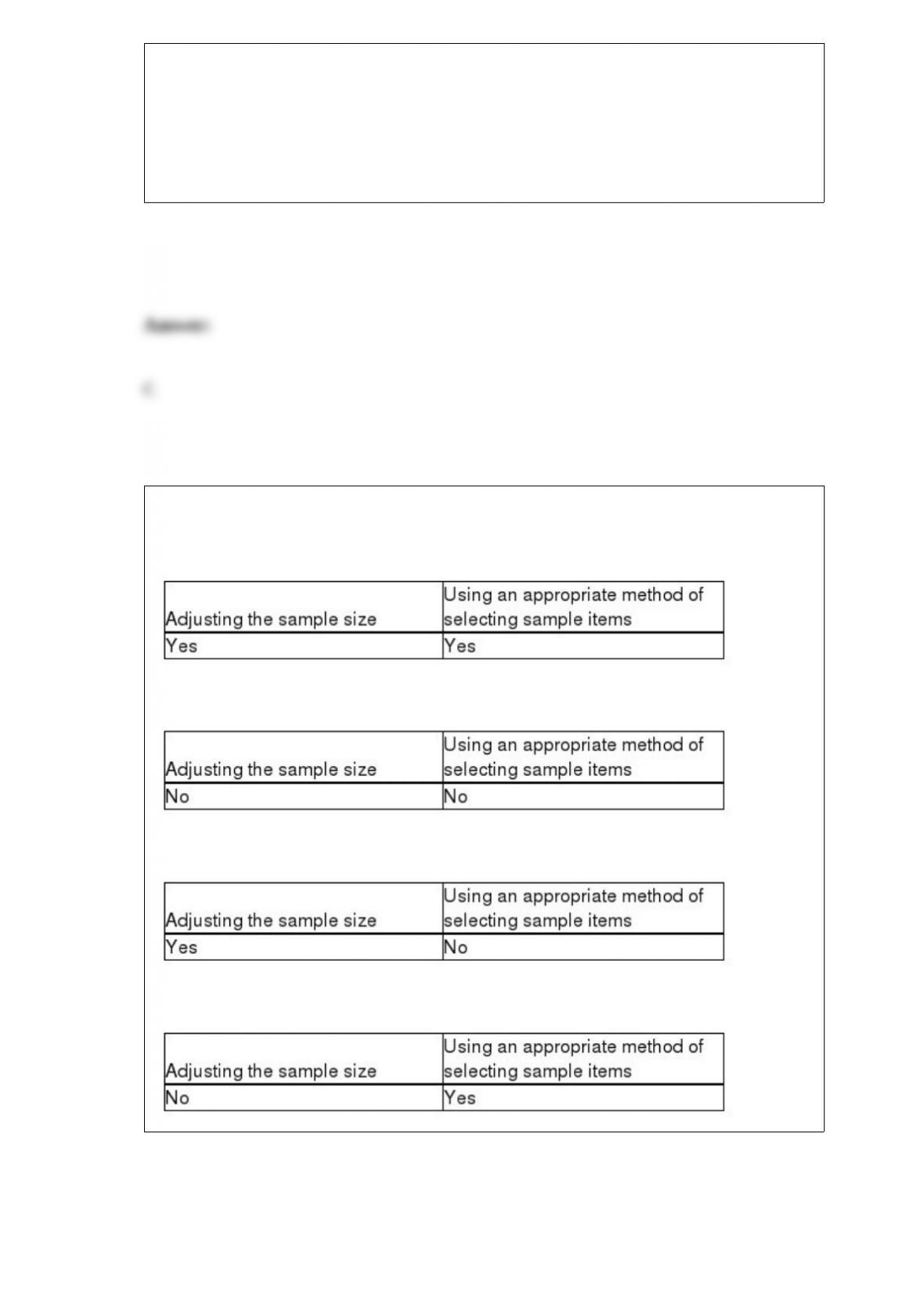

Sampling risk may be controlled by

A)

B)

C)

D)

Which of the following is an accurate statement regarding audit evidence?

A) Responses to the auditor’s questions by client employees is considered highly

persuasive evidence.

B) Audit evidence should provide an absolute level of assurance.

C) The auditor uses evidence to determine whether the statements are fairly presented.

D) All evidence must be highly persuasive.

One way to evaluate sampling risk when nonstatistical sampling is used is to

A) subtract the sample exception rate from the tolerable exception rate.

B) add the sample exception rate and the tolerable exception rate.

C) subtract the sample exception rate from the acceptable risk of overreliance.

D) add the sample exception rate and the acceptable risk of overreliance.

Risk of material misstatement at the assertion level

A) is only relevant to account balances.

B) determines the nature, timing, and extent of further audit procedures.

C) refers to risks that are pervasive to the financial statements as a whole.

D) consists of business risk and inherent risk.

Which of the following would have the least amount of importance regarding controls

over the processing of payroll?

A) The person authorized to sign paychecks should not be otherwise involved in the

preparation of the payroll.

B) A check-signing machine should not be used to replace a manual signature.

C) Distribution of pay checks should be performed by someone who is not involved in

the other payroll functions.

D) Unclaimed paychecks should be immediately returned for redeposit.

Which of the following statements is not correct?

A) It is possible to vary the sample size from one unit to 100% of the items in the

population.

B) Cost is an adequate justification for not gathering an adequate sample size.

C) The decision of how many items to test must be made by the auditor for each audit

procedure.

D) The sample size for any given procedure is likely to vary from audit to audit.

The two primary classes of transactions in the sales and collection cycle are

A) sales and sales discounts.

B) sales and cash receipts.

C) sales and sales returns.

D) sales and accounts receivable.