Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

21-1

Chapter 21

Audit of the Inventory and Warehousing Cycle

Concept Checks

P. 694

1. Inventory is often the most difficult and time consuming part of many

audit engagements because:

to fully understand.

fairly complicated.

5. The valuation of inventory is difficult due to such factors as the

large number of different items involved, the need to allocate the

manufacturing costs to inventory, and obsolescence.

electronic files, ledgers, worksheets, and reports, which accumulate

material, labor, and overhead costs by job or process as the costs are

incurred.

inventories for financial statement purposes.

P. 701

1. A proper cutoff of purchases and sales is heavily dependent on the

To make sure the cutoff for sales is accurate, the following information

1. The last shipping document number should be recorded in the

21-2

Concept Check, P. 701 (continued)

2. A review should be made of shipping to test for the possibility of

cutoff problems.

3. When prenumbered shipping documents are not used, a careful

first step in testing the cutoff.

4. A list of the most recent shipments should be included in the

working papers for subsequent follow-up to sales records.

For the purchase cutoff, the following information should be noted:

1. The last receiving report number should be noted in the working

2. The auditor documents used, unused, and voided tag numbers at the end of

the physical inventory observation to partially satisfy the existence and

occurrence balance-related audit objectives during follow-up testing. To test

existence, the auditor will examine an inventory listing by tag number to

verify that inventory included in the final listing consists of only those items

3. The direct labor hours for an individual inventory item would be verified by

examining engineering specifications or similar information to determine

The manufacturing overhead rate is calculated by dividing the total

annual number of labor hours into total manufacturing overhead. These

21-3

Review Questions

for the materials required to produce a customer order, or orders may be

initiated upon periodic evaluation of the situation in light of the prior experience

of inventory activity. After receiving the materials ordered, as part of the

acquisition and payment cycle, the materials are inspected with a copy of the

cycle.

1. Compare the inventory cost entered into the inventory system to

the supporting invoice to determine that it was properly recorded

21-2 The most important tests of the perpetual records the auditor must make

before assessed control risk can be reduced, which may permit a reduction in

other audit tests, are:

1. Tests of the purchases of raw materials and pricing thereof.

goods have been manufactured.

3. Tests of the reduction in the finished goods inventory through the

sale of goods to customers.

Assuming the perpetual records are determined to be effective, physical

inventory tests may be reduced, as well as tests of inventory cutoff. In addition,

21-4

21-3

SUBSTANTIVE ANALYTICAL

PROCEDURE

TYPE OF

POTENTIAL MISSTATEMENT

1. Compare gross margin percentage

with previous years.

Overstatement or understatement of

inventory amounts (prices and/or

quantities).

2. Compare inventory turnover with

previous years.

Obsolete inventory.

3. Compare unit costs with previous

years.

Overstatement or understatement of

unit costs.

4. Compare extended inventory value

with previous years.

Errors in compilation, unit costs, or

extensions.

5. Compare current year manufacturing

costs with previous years.

Misstatement of unit costs of inventory,

especially direct labor and

manufacturing overhead.

business.

2. Review the perpetual records for slow-moving items.

inventory, inventory in unusual locations, and unusual amounts of

dust on the inventory.

7. Examine obsolescence reports, scrap sales, and other records in

at a reduced cost.

8. Calculate inventory ratios, by type of inventory if possible, and

compare them to previous years or industry standards.

21-5 The continuation of shipping operations during the physical inventory

will require the auditor to perform additional procedures to ensure that a

Since no second count is taken, the auditor must increase the number

21-5

21-6 The auditor could have uncovered the misstatement if there were

adequate controls over the use of inventory tags. More specifically, the auditor

should have assured himself or herself that the client had accounted for all

used and unused tag numbers by examining all tags, if necessary. In addition,

the auditor should have selected certain tags (especially larger items) and had

21-7 The auditor must not give the controller a copy of his or her test counts.

The auditor’s test counts are the only means of controlling the original counts

21-8 The most important audit procedures to test for the ownership of inventory

during the observation of the physical counts and as a part of subsequent

valuation tests are:

1. Discuss ownership issues, such as inventory held on consignment,

with the client.

2. Obtain an understanding of the client’s operations.

3. Be alert for inventory set aside or specially marked.

21-9 Assuming the auditor properly documents receiving report numbers as

a part of the physical inventory observation procedures, the auditor should

verify the proper cutoff of purchases as a part of subsequent tests by examining

each invoice to see if a receiving report is attached. If the receiving report

21-6

21-10 Compilation tests are the tests of the summarization of physical counts,

the extension of price times quantity, footing the inventory summary, and tracing

the totals to the general ledger.

Several examples of audit procedures to verify compilation are:

1. Trace the tag numbers used to the final inventory summary to make

2. Trace the test counts recorded in the working papers to the final

3. Trace inventory items on the final inventory list to the tags as a

21-11

DATE

PURCHASE

QUANTITY

PRICE

TO BE INCLUDED IN

12-31-16 INVENTORY

EXTENSION

11-26-16

12-06-16

2,400

1,900

$2.07

$2.28

700 @ $2.07

1,900 @ $2.28

$1,449.00

4,332.00

$5,781.00

Assuming FIFO inventory valuation, the 12-31-16 inventory should be

valued at $5,781, and is thus currently overstated by $121.

If the 1-26-17 purchase was for 2,300 binders at $2.12 each, the 12-31-

21-12 With a job cost system, labor charged to a specific job is accumulated

on a job cost sheet. The direct labor dollars included on the job cost sheet can

Multiple Choice Questions From CPA Examinations

21-13 a. (2) b. (4) c. (2)

21-14 a. (3) b. (4) c. (3)

21-15 a. (4) b. (3) c. (1)

Discussion Questions and Problems

21-16

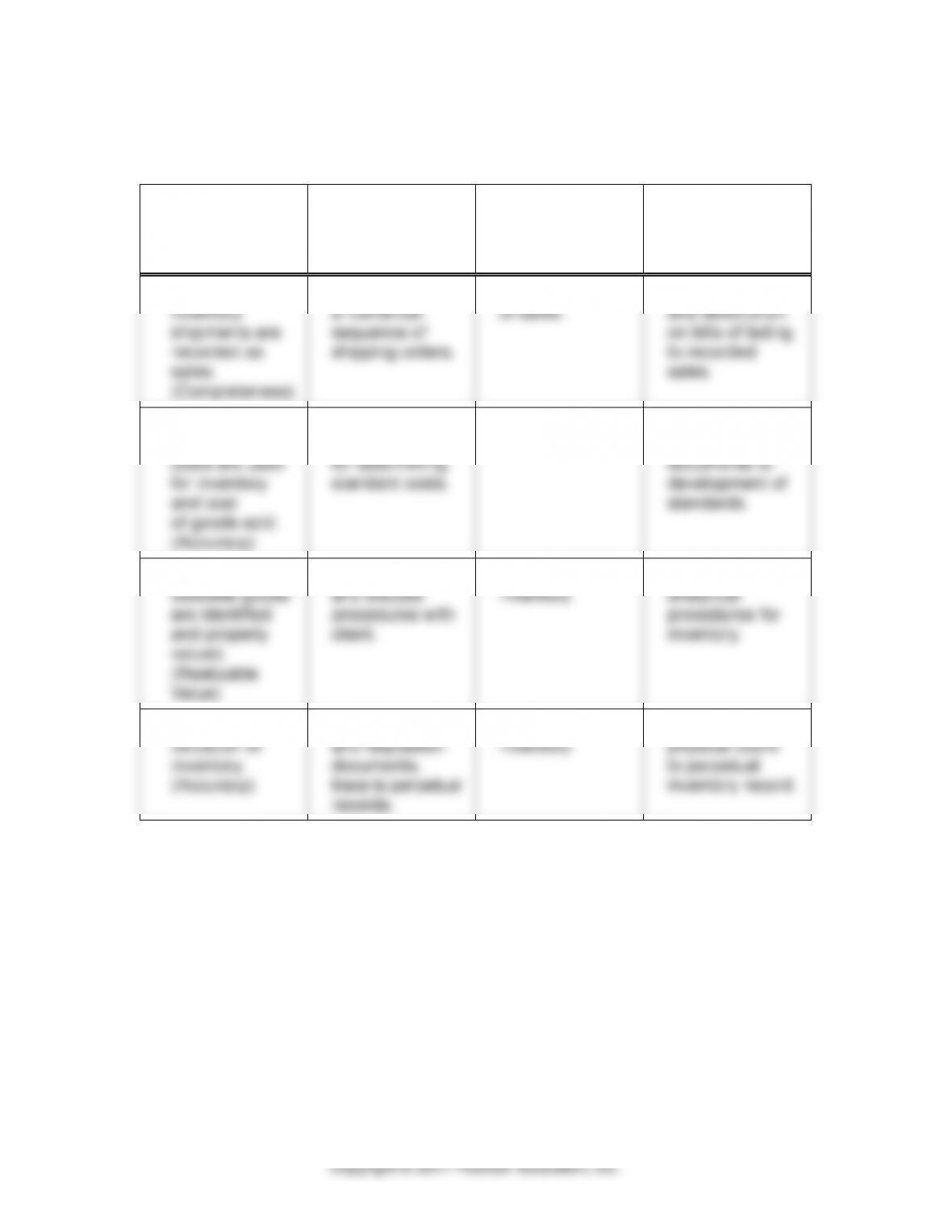

a.

PURPOSE OF

INTERNAL

CONTROL

b.

TEST OF

CONTROL

c.

POTENTIAL

FINANCIAL

MISSTATEMENT

d.

SUBSTANTIVE

AUDIT

PROCEDURE

1. To ensure

inventory

shipments are

recorded as

sales.

(Completeness)

Account for

a numerical

sequence of

shipping orders.

Understatement

of sales.

Trace quantity

and description

on bills of lading

to recorded

sales.

2. To assure

reasonable

costs are used

for inventory

and cost

of goods sold.

(Accuracy)

Review

procedures

for determining

standard costs.

Misstatement of

inventory.

Trace costs

from supporting

documents to

development of

standards.

3. To make sure

obsolete goods

are identified

and properly

valued.

(Realizable

Value)

Read policy

and discuss

procedures with

client.

Misstatement of

inventory.

Substantive

analytical

procedures for

inventory.

4. For a proper

valuation of

inventory.

(Accuracy)

Examine receiving

and requisition

documents,

trace to perpetual

records.

Misstatement of

inventory.

Compare

physical count

to perpetual

inventory record.

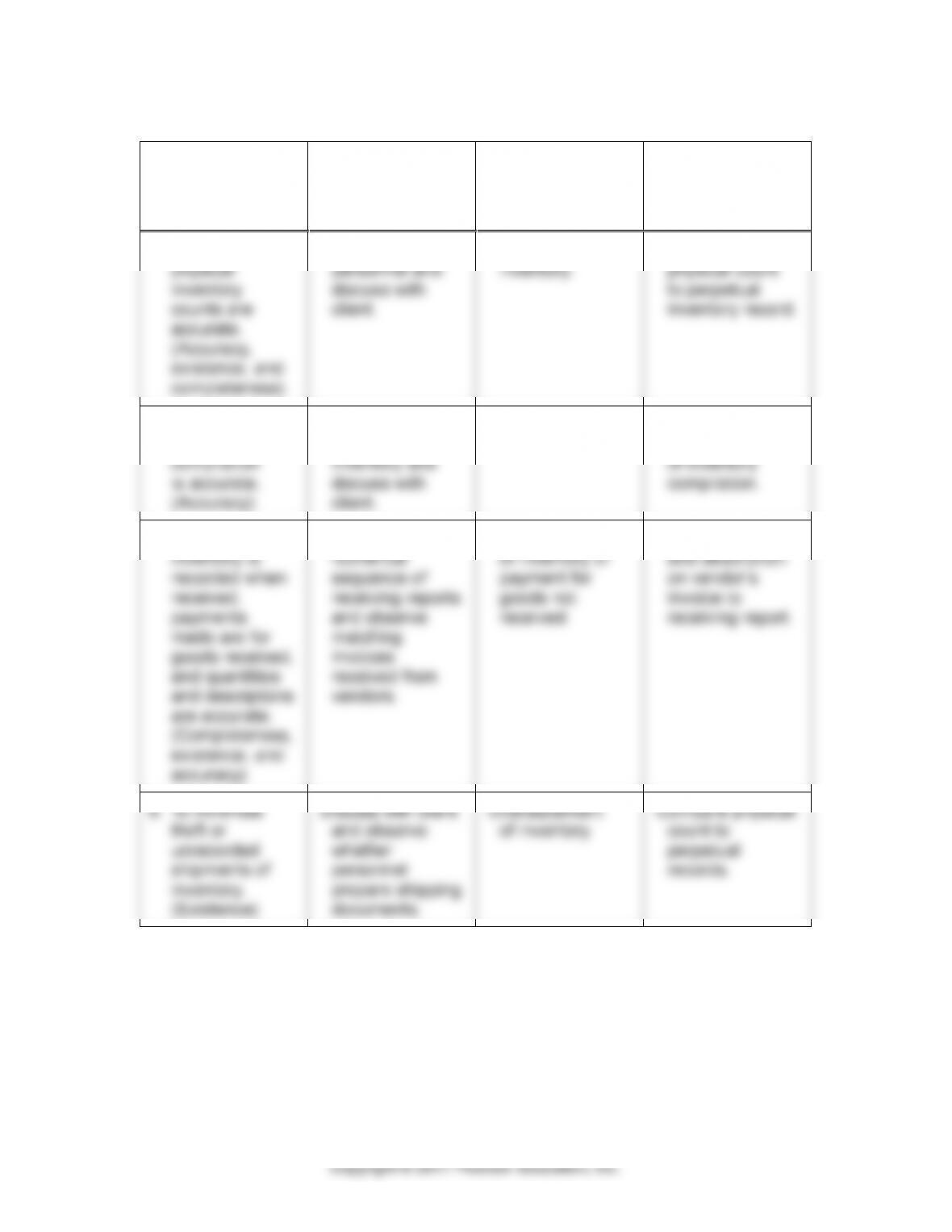

21-16 (continued)

a.

PURPOSE OF

INTERNAL

CONTROL

b.

TEST OF

CONTROL

c.

POTENTIAL

FINANCIAL

MISSTATEMENT

d.

SUBSTANTIVE

AUDIT

PROCEDURE

5. To make sure

physical

inventory

counts are

accurate.

(Accuracy,

existence, and

completeness)

Observe counting

personnel and

discuss with

client.

Misstatement of

inventory.

Compare

physical count

to perpetual

inventory record.

6. To make sure

inventory

compilation

is accurate.

(Accuracy)

Observe who

compiles the

inventory and

discuss with

client.

Misstatement of

inventory.

Reperform

clerical tests

of inventory

compilation.

7. To ensure

inventory is

recorded when

received,

payments

made are for

goods received,

and quantities

and descriptions

are accurate.

(Completeness,

existence, and

accuracy)

Account for a

numerical

sequence of

receiving reports

and observe

matching

invoices

received from

vendors.

Understatement

of inventory or

payment for

goods not

received.

Trace quantity

and description

on vendor’s

invoice to

receiving report.

8. To minimize

theft or

unrecorded

shipments of

inventory.

(Existence)

Discuss with client

and observe

whether

personnel

prepare shipping

documents.

Overstatement

of inventory.

Compare physical

count to

perpetual

records.

21-17

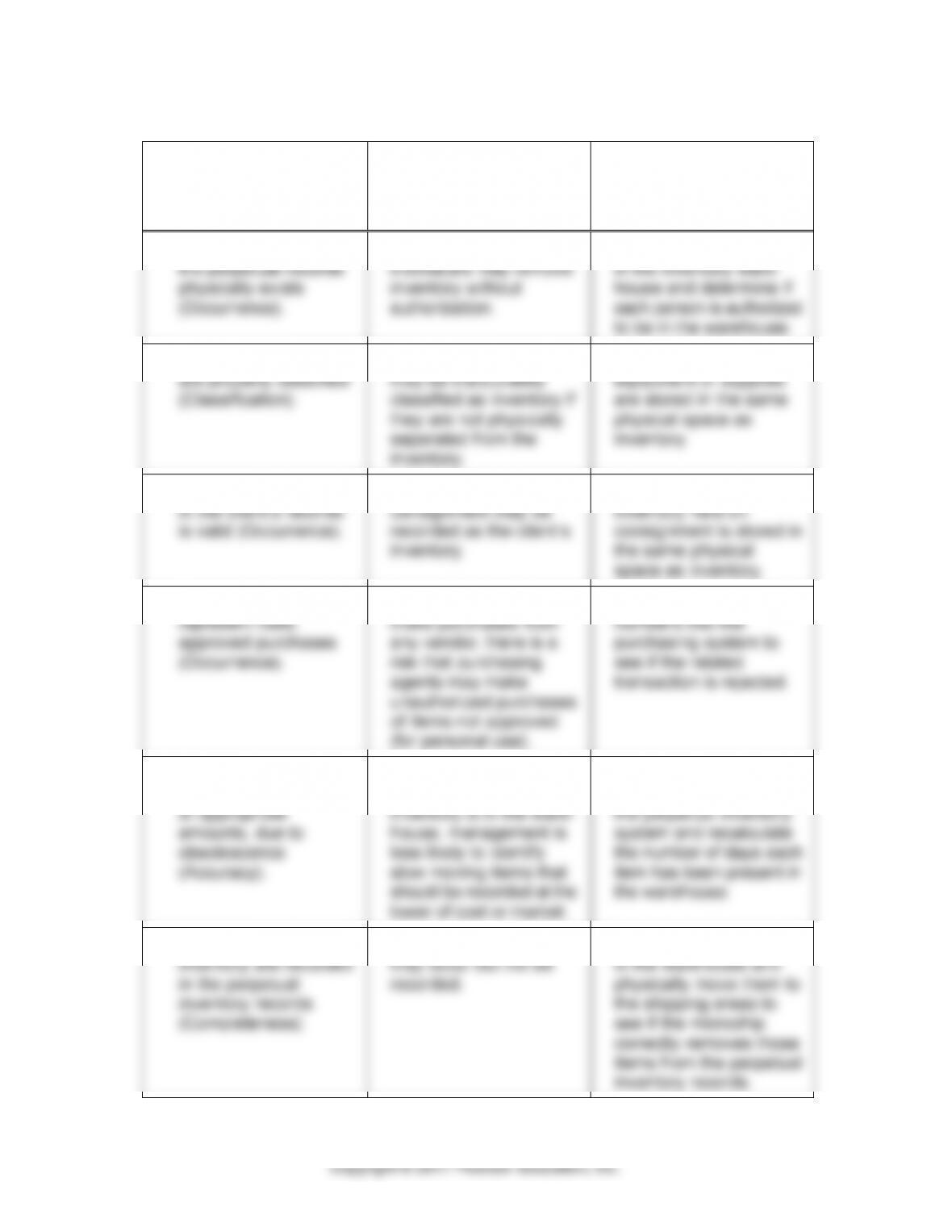

a.

TRANSACTION-

RELATED AUDIT

OBJECTIVE

b.

RELATED RISK

c.

TEST OF CONTROL

1. Inventory recorded in

the perpetual records

physically exists

(Occurrence).

Non-inventory warehouse

individuals may remove

inventory without

authorization.

Observe client personnel

in the inventory ware-

house and determine if

each person is authorized

to be in the warehouse.

2. Inventory transactions

are properly classified

(Classification).

Equipment or supplies

may be inaccurately

classified as inventory if

they are not physically

separated from the

inventory.

Observe whether

equipment or supplies

are stored in the same

physical space as

inventory.

3. Recording of inventory

in the client’s records

is valid (Occurrence).

Inventory held on

consignment may be

recorded as the client’s

inventory.

Observe whether

inventory held on

consignment is stored in

the same physical

space as inventory.

4. Recorded transactions

represent valid,

approved purchases

(Occurrence).

If purchasing agents can

make purchases from

any vendor, there is a

risk that purchasing

agents may make

unauthorized purchases

of items not approved

(for personal use).

Enter non-valid vendor

numbers into the

purchasing system to

see if the related

transaction is rejected.

5. Recorded inventory

may not be recorded

at appropriate

amounts, due to

obsolescence

(Accuracy).

Without information about

the amount of time

inventory is in the ware-

house, management is

less likely to identify

slow moving items that

should be recorded at the

lower of cost or market.

Select a sample of

inventory items from

the perpetual inventory

system and recalculate

the number of days each

item has been present in

the warehouse.

6. Actual shipments of

inventory are recorded

in the perpetual

inventory records

(Completeness).

Shipments of inventory

may occur but not be

recorded.

Select a sample of items

in the warehouse and

physically move them to

the shipping areas to

see if the microchip

correctly removes those

items from the perpetual

inventory records.

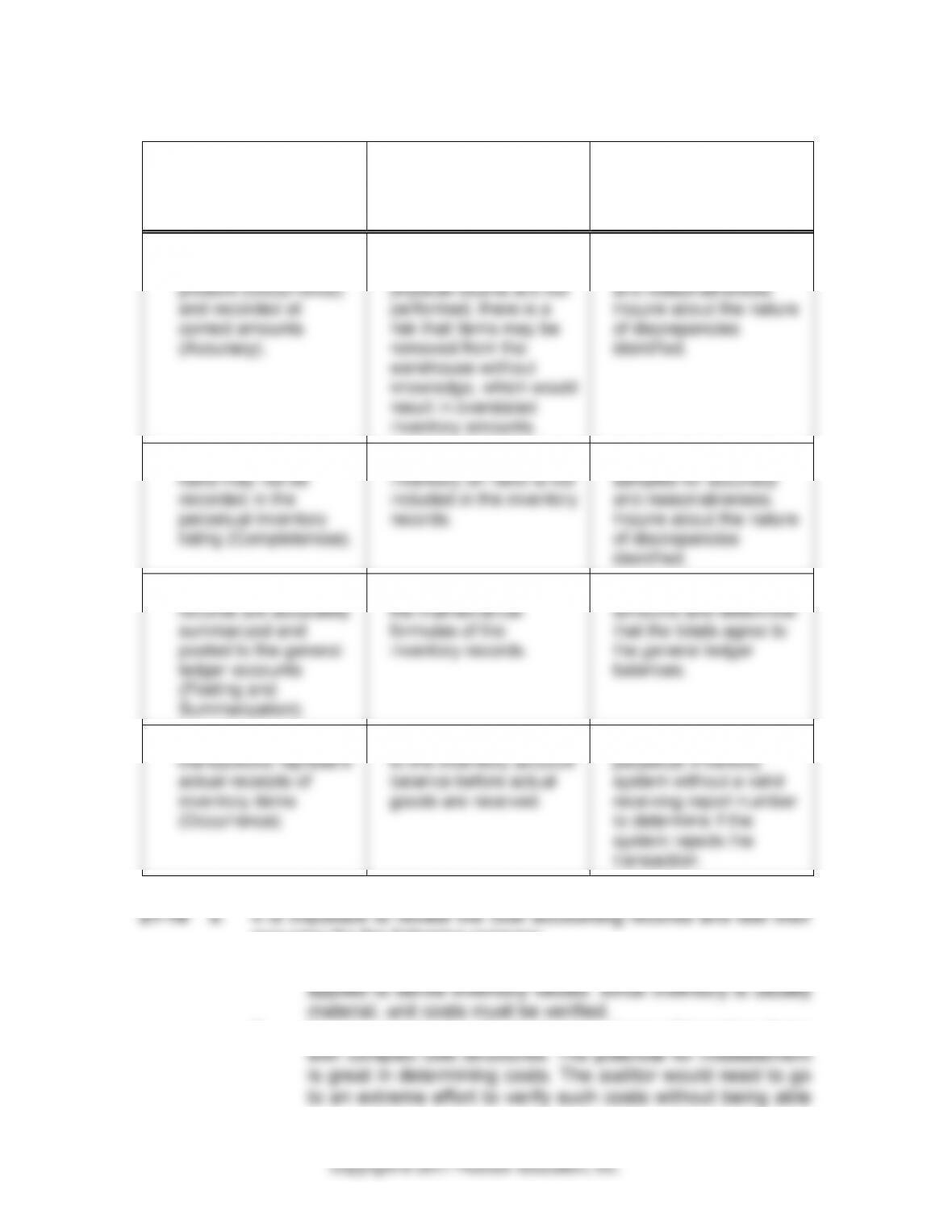

21-17 (continued)

a.

TRANSACTION-

RELATED AUDIT

OBJECTIVE

b.

RELATED RISK

c.

TEST OF CONTROL

7. Recorded inventory

items are physically

present (Occurrence)

and recorded at

correct amounts

(Accuracy).

If periodic reconciliations

of inventory records to

physical counts are not

performed, there is a

risk that items may be

removed from the

warehouse without

knowledge, which would

result in overstated

inventory amounts.

Inspect the client’s test

samples for accuracy

and reasonableness.

Inquire about the nature

of discrepancies

identified.

8. Actual inventory on

hand may not be

recorded in the

perpetual inventory

listing (Completeness).

There is a risk that

inventory on hand is not

included in the inventory

records.

Inspect the client’s test

samples for accuracy

and reasonableness.

Inquire about the nature

of discrepancies

identified.

9. The perpetual inventory

records are accurately

summarized and

posted to the general

ledger accounts

(Posting and

Summarization).

There could be errors in

the mathematical

formulas of the

inventory records.

Recalculate the inventory

amounts and determine

that the totals agree to

the general ledger

balances.

10. Recording inventory

transactions represent

actual receipts of

inventory items

(Occurrence).

Inventory could be added

to the inventory account

balance before actual

goods are received.

Enter an addition to the

perpetual inventory

system without a valid

receiving report number

to determine if the

system rejects the

transaction.

accuracy for the following reasons:

1. The cost accounting records determine unit costs that are

2. In many companies, there are many types of inventory items