Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

19-17

19-27 (continued)

4. The paving and fencing are land improvements and should

be depreciated over their useful lives.

Land improvements (may be $50,000

combined with buildings account

— buildings and improvements)

Land $50,000

Depreciation expense $2,500

5. The cost and allowance for depreciation should have been

removed from the accounts and a gain or loss on sale

recorded.

Cost of asset $480,000

Allowance for depreciation:

To 12/31/15 –

480,000/10 x 3-1/2 168,000

For 20163 –

The correcting entry is:

Allowance for depreciation—

Machinery and Equipment $203,000

6. Donated property should be capitalized at its fair market

value.

Land $100,000

Donated Property

To record land and building for new plant donated by Crux

City.

19-18

19-27 (continued)

Depreciation expense $8,000

19-28 a.

To: In-Charge Auditor

From: Audit Manager

Subject: Concerns about the schedule prepared by the client and the

staff assistant in the audit of Vernal Manufacturing Company

The analytical procedures schedule for the audit of Vernal Manufacturing

Company is completely inadequate and needs to be redone. There are

several deficiencies:

1. The headings, references, and indexing on the audit schedule are

information than the single-step statement provided.

3. The schedule should include the additional columns showing the

in each account.

5. There is no identification of accounts that we are concerned may be

materially misstated. For example, the $1,381 change in

other expense may be significant.

investigation and the nature of such investigation.

7. There is no indication that the client’s explanations have been

19-19

19-28 (continued)

b. For every explanation provided by the client, an alternative possibility

is a misstatement in the financial statements. The auditor must be

ACCOUNT

POSSIBLE MISSTATEMENT

Sales

Cutoff error for sales

Sales returns and allowances

Returns due to technological deficiencies in

products that may indicate obsolete inventory

Miscellaneous income

Including proceeds of the sale of equipment as

income rather than decreasing the

equipment account

Cost of goods sold

Small increase in cost of goods sold compared

to net sales may indicate an overstatement

of ending inventory or understatement of any

of the accounts making up cost of goods sold

c. To perform a meaningful determination of the most important

variances, an alternative design of the audit schedule follows. It is

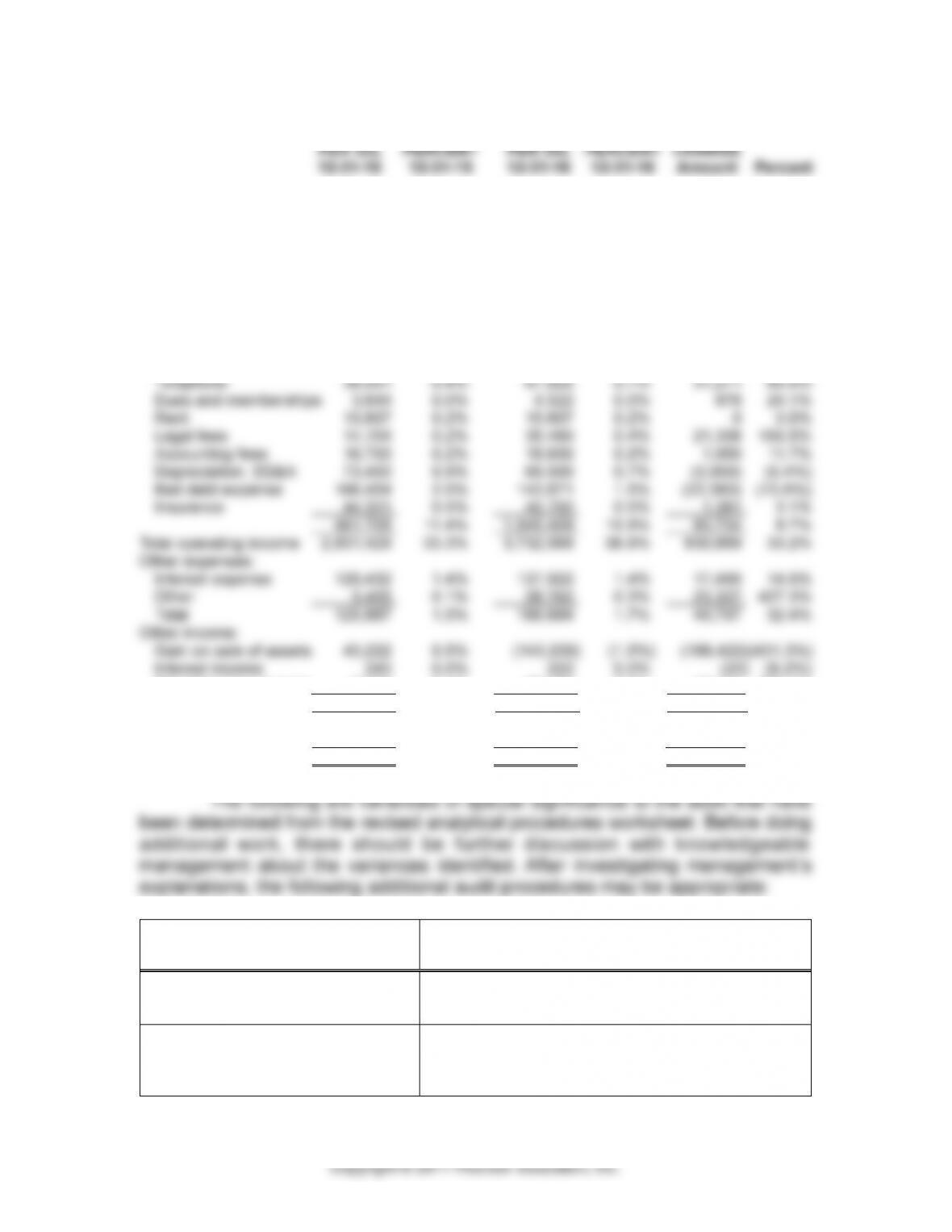

Sales $8,467,312 100.8% $9,845,231 102.5% $1,377,919 16.3%

Sales returns and

allowances (64,895) (0.8%) (243,561) (2.5%) (178,666) 275.3%

Net Sales 8,402,417 100.0% 9,601,670 100.0% 1,199,253 14.3%

Cost of goods sold:

Beginning inventory 1,487,666 17.7% 1,389,034 14.5% (98,632) (6.6%)

Purchases 2,564,451 30.5% 3,430,865 35.7% 866,414 33.8%

Freight-in 45,332 0.5% 65,782 0.7% 20,450 45.1%

19-20

19-28 (continued)

Selling, general and administrative:

Executive salaries 167,459 2.0% 174,562 1.8% 7,103 4.2%

Executive benefits 32,321 0.4% 34,488 0.4% 2,167 6.7%

Office salaries 95,675 1.1% 98,540 1.0% 2,865 3.0%

Office benefits 19,888 0.2% 21,778 0.2% 1,890 9.5%

Travel and entertainment 56,845 0.7% 75,583 0.8% 18,738 33.0%

Advertising 130,878 1.6% 156,680 1.6% 25,802 19.7%

Other sales expense 34,880 0.4% 42,334 0.4% 7,454 21.4%

Stationery and supplies 38,221 0.5% 21,554 0.2% (16,667) (43.6%)

Postage 14,657 0.2% 18,756 0.2% 4,099 28.0%

Miscellaneous income 6,365 0.1% 25,478 0.3% 19,113 300.3%

Total 49,830 0.6% (117,499) (1.2%) (167,329)(335.8%)

Income before taxes 2,725,372 32.4% 3,447,915 35.9% 722,543 26.5%

Income taxes 926,626 11.0% 1,020,600 10.6% 93,974 10.1%

Net income $1,798,746 21.4% $2,427,315 25.3% $ 628,569 34.9%

ACCOUNT

POTENTIAL ADDITIONAL

AUDIT PROCEDURES

1. Sales

Perform extensive cutoff tests and other tests

for possible overstatements.

2. Sales returns and

allowances

Examine supporting documents for the largest

sales returns and allowances and consider

the effect on inventory valuation.

19-21

19-28 (continued)

ACCOUNT

POTENTIAL ADDITIONAL

AUDIT PROCEDURES

3. Cost of goods sold. Cost

of goods sold increased

only $185,000, but sales

increased 1.2 million.

Do careful tests of physical counts, costing,

cutoff, inventory, and tests for obsolescence.

4. Travel and entertainment

Examine supporting documentation for large

travel and entertainment expenses.

5. Telephone

Compare telephone expense by month to

determine the possibility of a misclassification.

6. Legal expense

Analyze legal expense to determine the

possibility of lawsuits or other legal actions

that might affect the financial statements.

7. Depreciation expense

Compare depreciation by month to determine

the possibility of the failure to record one

month’s depreciation.

8. Bad debt expense

Performed detailed analytical procedures and

other tests of accounts receivable to evaluate

the adequacy of the allowance for

uncollectible accounts.

9. Other expense

Analyze other expense to determine the

nature of other expense and the possibility of

misclassification or incorrect accounting.

10. Gain on the sale of assets

Analyze the account to determine the nature of

the transactions and any misclassification or

incorrect accounting.

19-29

a. Property, plant, and equipment is in Topic 360 under Assets.

b. Topic 360-10-50-1 indicates:

notes thereto:

a. Depreciation expense for the period

19-22

19-29 (continued)

depreciable assets.

c. The ASC indicates that impairment is the condition that exists when

d. Topic 310-50-2 indicates:

impairment loss is recognized:

a. A description of the impaired long-lived asset (asset group) and

the facts and circumstances leading to the impairment

b. If not separately presented on the face of the statement, the

another valuation technique)

d. If applicable, the segment in which the impaired long-lived asset

(asset group) is reported under Topic 280.