Staff assigned to an audit engagement must be knowledgeable about the client’s

industry.

Current professional standards prohibit accountants from performing engagements to

review forecasts or projections.

It is common to use a combination of positive and negative confirmations by sending

the latter to accounts with large balances and the former to those with small balances.

There are five Trust Service principles, including security and viability.

The majority of financial instruments are valued at the lower of cost or market.

The Credit Alliance approach to the concept of foreseen users states that to be liable to

third parties, an auditor (1) must know and intend that the work product would be used

by the third-party for a specific purpose, and (2) the knowledge and intent must be

evidenced by the auditor’s conduct.

The audit procedure “recompute hours worked from time cards” is normally performed

when testing the completeness objective for payroll.

Under the cycle approach to segmenting an audit, transactions recorded in different

journals should never be combined with the general ledger balances that result from

those transactions.

When performing compilation services, the accountant is not required to obtain an

understanding of the client’s internal control.

Inventory compilation tests are used to verify that the inventory is recorded at the lower

of cost or market.

Both U.S. and international auditing standards require the use of confirmations for

accounts receivable.

The balance-related audit objective realizable value is not applicable when auditing

accounts payable.

Since the audit risk model is a planning model, it assists the auditor in evaluating

results.

The procedures to obtain an understanding of internal control are only applied when the

assessed control risk is high.

The use of monetary unit sampling is most appropriate when the auditor expects to find

many errors and when a monetary result is desired.

Auditors seldom learn about the capital acquisition and repayment cycle when gaining

an understanding of the client’s business and industry.

When verifying the correct balance in accounts payable, vendors’ invoices are more

useful than vendors’ statements.

Management is required by GAAP to reduce information risk, even if the costs

outweigh the benefits.

Many of the audit procedures for finding contingencies are usually performed as an

integral part of various segments of the audit rather than as a separate activity near the

end of the audit.

Information and idea exchange sessions by the audit team are required by current

auditing standards.

If, during the completion phase of the audit, the auditor determines that he or she has

not obtained sufficient evidence to draw a conclusion about the fairness of the client’s

financial statements, there are two choices: accumulate additional evidence or issue

either a qualified or an adverse opinion.

The audit objectives are the well-defined methodology for organizing an audit to ensure

that the evidence gathered is sufficient and appropriate.

Safeguards can always reduce the threat to an acceptable level.

When auditing the capital acquisition and repayment cycle, it is common to verify each

transaction taking place in the cycle for the entire year as a part of verifying the balance

sheet accounts.

Ineffective oversight by the board of directors over financial reporting is an example of

an incentives/pressures risk factor.

CPA firms are never allowed to provide bookkeeping services for clients.

For a private company client, auditors are required to test any internal controls they

believe have not been operating effectively during the period under audit.

Preliminary judgments about materiality are often changed during the course of the

engagement.

A proof of cash receipts is not useful for uncovering the theft of cash receipts or the

recording and deposit of an improper amount of cash.

Most companies, with the exception of small ones, have effective controls over the

payroll cycle.

Client representation letters are required by professional auditing standards, whereas

management letters are optional.

The extent of tests of controls in audits of nonpublic companies depends on the

effectiveness of the controls and the extent to which the auditor believes they can be

relied on to reduce control risk.

Accounts receivable confirmations must be controlled by the client from the time they

are prepared until the time they are returned to the auditor.

Interrogative inquiry is often confrontational.

Inherent risk can be extended to individual balance-related audit objectives.

Substantive analytical procedures performed in all phases of the audit generally use

aggregate data to help understand where misstatements are more likely to occur.

Operational audits may be performed by internal auditors and government auditors, but

not by external auditors.

The Public Company Accounting Oversight Board (PCAOB) provides oversight to

auditors of publicly traded and private companies.

The general cash account is considered a significant account in almost all audits

A) where the ending balance is material.

B) even when the ending balance is immaterial.

C) except those of not-for-profit organizations.

D) where either the beginning or ending balance is material.

Which of the following statements is correct?

A) Bank personnel are responsible for providing reasonable assurance that a response to

a bank confirmation is accurate.

B) Bank personnel are responsible for providing complete assurance that a bank

confirmation is complete.

C) Bank personnel are not responsible for searching their records for bank balances or

loans beyond those included on the bank confirmation.

D) Bank personnel are not responsible for providing information related to interest on

the bank confirmation.

When the auditor uses supporting evidence for amounts posted to account balances with

documentary evidence, that process is called

A) inquiry.

B) confirmation.

C) vouching.

D) physical examination.

Because the failure to record disposals of property, plant, and equipment can

significantly affect the financial statements, the search for unrecorded disposals is

essential. Which of the following is not a procedure used to verify disposals?

A) Make inquiries of management and production personnel about the possibility of the

disposal of assets.

B) Review whether newly acquired assets replace existing assets.

C) Test the valuation of fixed assets recorded in prior periods.

D) Review plant modifications and changes in product line, property taxes, or insurance

coverage.

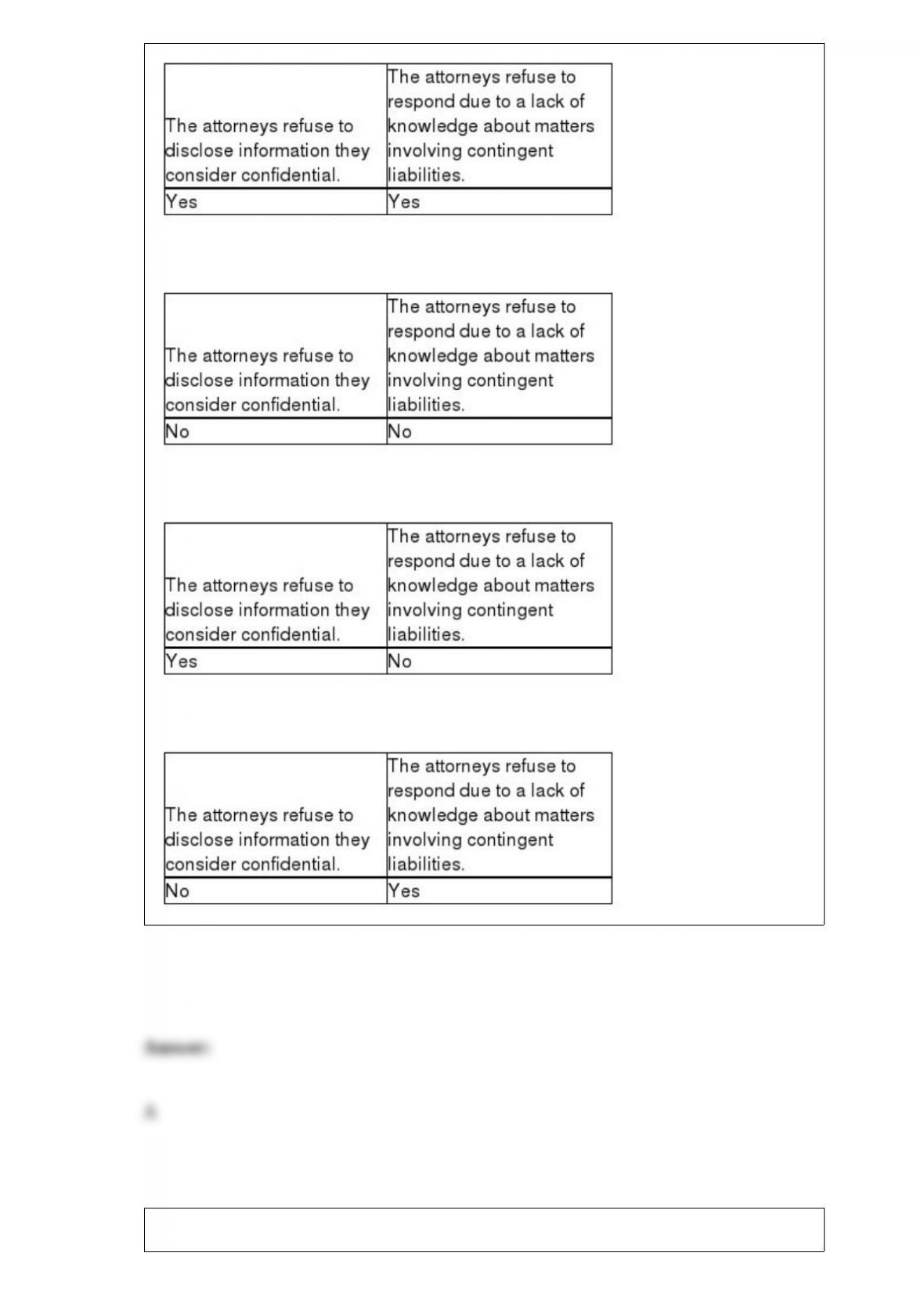

What is one of the main reasons an attorney may refuse to provide auditors with

complete information about contingent liabilities?

A)

B)

C)

D)

Which of the following is correct with respect to the design and use of business

documents?

A) The documents should be in paper format.

B) Documents should be designed for a single purpose to avoid confusion in their use.

C) Documents should be designed to be understandable only by those who use them.

D) Documents should be prenumbered consecutively to facilitate control over missing

documents.

Distribution of which of the following types of reports is limited?

A) audit

B) review

C) agreed-upon procedures

D) examination

When testing the controls for the completeness transaction-related audit objectives,

A) failure to record the acquisition of goods or services will generally understate net

income.

B) failure to record the acquisition of goods or services has no impact on the balance

sheet.

C) it is generally easy for the auditor to determine whether unrecorded transactions

exist.

D) the audit time for accounts payable can be reduced if the client has effective internal

controls and the auditor properly tests those controls.

Since the rules cannot address all circumstances, the Code includes a conceptual

framework approach for members to use to evaluate threats to compliance. Using this

framework,

A) the first step is to discuss the threat with the client’s management team.

B) all threats must be completely eliminated.

C) safeguards can be used to eliminate any threat.

D) more than one safeguard may be necessary.

Who is generally responsible for opening receipts when a company uses a lockbox to

speed the handling of cash receipts?

A) company personnel

B) temporary employees in the town where the lockbox is located

C) bank employees

D) company controller

Which of the following is not a difference between operational auditing and financial

auditing?

A) Both must be performed by a CPA.

B) Operational audit reports are usually of a restricted distribution while financial audit

reports are widely distributed.

C) Operational audits often cover nonfinancial issues while financial audits do not.

D) None of the above is a difference.

Which of the following is not a key control for sales and cash receipts?

A) active board of directors

B) adequate separation of duties

C) internal verification procedures

D) adequate documents and records

One of the first steps that should be performed for a review of a nonpublic entity’s

financial statements is to

A) read the financial statements.

B) obtain knowledge of the accounting principles and practices of the client’s industry.

C) inquire whether management has omitted substantially all of the disclosures required

by applicable accounting standards.

D) apply analytical procedures to provide limited assurance that no material

modifications should be made to the financial statements.

Which of the following types of engagement reports would provide positive assurance?

A) an examination

B) a review

C) an agreed-upon procedures engagement

D) a compilation

Which one of the following substantive analytical procedures would be most useful in

alerting the auditor to the possibility of obsolete inventory?

A) Compare gross margin percentage with that of previous years.

B) Compare unit costs of inventory with previous years.

C) Compare inventory turnover ratio with previous years.

D) Compare current year manufacturing costs with previous years.

When using the audit risk model,

A) auditors find it relatively easy to measure the components of the model.

B) many auditors use broad and subjective measurement terms.

C) auditors find it easy to measure the amount of evidence implied by a given planned

detection risk.

D) auditors are only concerned with understating accounts.

Inventory is often a significant part of a company’s current assets. Because of its

importance,

A) auditors are required by auditing standards to observe the client taking a physical

inventory count.

B) price tests must be performed to verify whether the physical counts were correctly

summarized.

C) companies are required to use perpetual inventory systems.

D) auditors are required by auditing standards to take the physical inventory for the

client.

Which balance sheet accounts are included in the payroll and personnel cycle?

A) cash in bank, accrued payroll, trade accounts receivable

B) accrued payroll, notes payable, and deferred tax

C) accrued payroll, cash in bank, and accrued payroll taxes

D) salaries and commissions, cash in bank, accrued payroll taxes

An auditor performs a test to determine whether all merchandise for which the client

was billed was received. The population for this test consists of all

A) merchandise received.

B) vendors’ invoices.

C) canceled checks.

D) receiving reports.

Which of the following is a correct statement regarding review, compilation, and

preparation services?

A) A written engagement letter is not needed for a review, compilation or preparation

service.

B) The Statements on Standards for Accounting and Review Services (SSARS) clarity

project used international standards as the base standard when revising the SSARS.

C) CPAs must be independent of the client in a review service engagement and for an

audit engagement.

D) The amount of evidence accumulated in a review is minimal.

The ________ has the responsibility for approving the number of hours worked for

each employee.

A) employee’s supervisor

B) human resources department

C) chief financial officer

D) budgeting supervisor

The exception rate that the auditor will permit in the population and still be willing to

use the preliminary control risk assessment is called the

A) acceptable exception rate.

B) estimated population exception rate.

C) sample exception rate.

D) tolerable exception rate.

An accountant who reviews the financial statements of a nonpublic entity should issue a

report stating that a review

A) is substantially equivalent in scope to an audit.

B) is substantially more in scope than a compilation.

C) is substantially less in scope than an audit.

D) provides only minimal assurance that the financial statements are fairly presented.

Which of the following is an incorrect statement regarding the allocation of the

preliminary judgment about materiality to balance sheet accounts?

A) Auditors expect certain accounts to have more misstatements than others.

B) The allocation has virtually no effect on audit costs because the auditor must collect

sufficient appropriate audit evidence.

C) Auditors expect to identify overstatements as well as understatements in the

accounts.

D) Relative audit costs affect the allocation.

When an employee who is authorized to make customer entries in the accounts

receivable subsidiary ledger purposefully enters cash received into the wrong

customer’s account that employee may be suspected of

A) kiting.

B) lapping.

C) floating.

D) shorting.

Which of the following should be audited on the interbank transfer schedule?

A) Receipts on the interbank transfer schedule should be correctly included in or

excluded from year-end bank reconciliations as deposits in transit.

B) Disbursements on the interbank transfer schedule must always be shown as

outstanding checks.

C) The interbank transfers cannot be recorded in both the receiving and disbursing

banks.

D) All transfers that occurred for the month before and the month after the year-end

must be included on the interbank transfer schedule.

If an auditor believes the chance of financial failure is high and there is a corresponding

increase in business risk for the auditor, acceptable audit risk would likely

A) be reduced.

B) be increased.

C) remain the same.

D) be calculated using a computerized statistical package.

There must be a periodic physical count by the client of the inventory items on hand

A) only if the client uses the LIFO method.

B) only if the client uses a lower-of-cost-or-market method.

C) regardless of the client’s inventory valuation method.

D) only if the client uses either the LIFO or FIFO method.

Which of the following types of evidence is not available when using substantive tests

of transactions?

A) inspection

B) confirmation

C) inquiries of the client

D) reperformance

The allowance for sampling risk when no misstatements are found in the sample is

A) tolerable risk of misstatement.

B) basic precision.

C) confidence factor.

D) population variance.

Describe three audit procedures an auditor would use to test for the realizable value

balance-related audit objective

Discuss the actions an auditor should take when an illegal act is identified or suspected.

Discuss two causes of nonsampling risk. Also discuss ways the auditor can control

nonsampling risk.

Describe the standard unmodified opinion audit report to be issued for an audit of a

private company. Begin by specifying the eight parts of the report, and then discuss the

contents of each part.

EPM, Inc., is a private manufacturing company with a calendar year-end. Their

financial statements include a balance sheet, a statement of income, statement of cash

flows, and statement of stockholders’ equity. For the most recent audit, Harrington and

Perry, LLP, audited the 2015 and 2016 financial statements. The auditors completed all

significant fieldwork on March 5, 2017 and issued the audit report on March 16, 2017.

Required:

Consider all the facts given and write the standard unmodified opinion audit report,

including all eight sections of the report.

Discuss the primary purpose of an audit engagement letter. Is an engagement letter

required?

The completeness transaction-related audit objective must be considered when

determining key controls for sales. List three of the key controls that must be

considered when cash received is recorded in the cash receipts journal.

State the three phases of the audit where analytical procedures can be performed and

describe the specific procedures performed in each phase.

Discuss the relationship between quality control and generally accepted auditing

standards.

There are four steps to generalize from the sample to the population using difference

estimation sampling. Identify each of these four steps.

Discuss the advantages and benefits of using generalized audit software.

List three of the major factors affecting sample size for confirming accounts receivable.

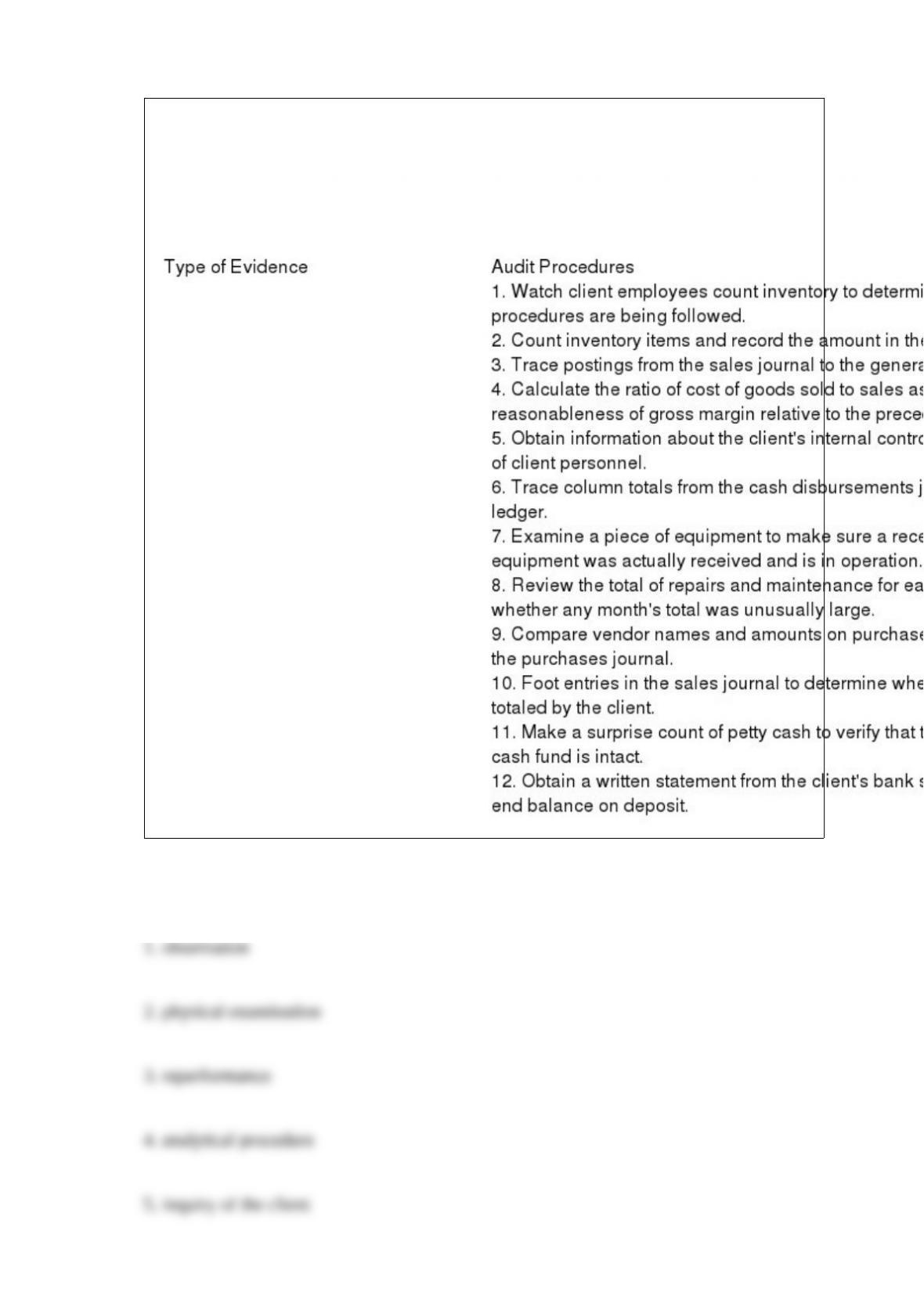

Below are 12 audit procedures. Classify each procedure according to the following

types of audit evidence: (1) physical examination, (2) confirmation, (3) documentation,

(4) observation, (5) inquiry of the client, (6) reperformance, and (7) analytical

procedure.

How might auditors include negative balances when using monetary unit sampling to

evaluate a population?

Discuss the similarities and differences between financial statement audits, operational

audits, and compliance audits. Give an example of each type.