10-1

Chapter 10

Assessing and Responding to Fraud Risks

Concept Checks

P. 311

1. The three conditions of fraud referred to as the “fraud triangle” are (1)

Incentives/Pressures; (2) Opportunities; and (3) Attitudes/Rationalization.

management or employees to commit a dishonest act or they are in an

environment that imposes sufficient pressure that causes them to rationalize

committing a dishonest act.

2. Sources used to gather information about fraud risks include:

Information obtained from communications among audit team

members about their knowledge of the company and its industry,

Responses to auditor inquiries of management about their views of

Specific risk factors for fraudulent financial reporting and

Analytical procedures results obtained during planning that indicate

Knowledge obtained through other procedures such as client

P. 323

1. The three auditor responses to fraud are: (1) change the overall conduct of

the risk of management override of controls.

2. Three main techniques used to manipulate revenue include: (1) recording of

fictitious revenue; (2) premature revenue recognition including techniques such

10-2

Review Questions

fixed assets to increase earnings.

10-2 Misappropriation of assets is fraud that involves theft of an entity’s assets.

Two examples are an accounts payable clerk issuing payments to a fictitious

debt covenants or obtain additional financing.

Opportunities – Ineffective oversight of financial reporting by the

Attitudes/Rationalization – Management is overly aggressive. For

10-4 The following are examples of risk factors for misappropriation of

assets for each of the three fraud conditions:

Incentives/Pressures – The individual is unable to meet personal

financial obligations.

Attitudes/Rationalization – Management has disregarded the

10-5 Auditing standards require the audit team to conduct discussions to

share insights from more experienced audit team members and to “brainstorm”

ideas that address the following:

1. How and where they believe the entity’s financial statements might

create an incentive or pressure for management to commit

fraud.

rationalize fraudulent acts.

10-3

10-5 (continued)

reporting.

3. How assets of the entity could be misappropriated.

4. How the auditor might respond to the susceptibility of material

misstatements due to fraud.

10-6 Auditors must inquire whether management has knowledge of any fraud

or suspected fraud within the company. Auditing standards also require auditors

to inquire of the audit committee about its views of the risks of fraud and whether

10-7 Professional skepticism suggests the auditor should neither assume that

management is dishonest, nor assume unquestioned honesty, and an auditor

should remain professionally skeptical throughout the entire audit process. A

questioning mind will encourage the auditor to gather more persuasive evidence

10-8 The corporate code of conduct establishes the “tone at the top” of the

importance of honesty and integrity and can also provide more specific guidance

10-9 Management and the board of directors are responsible for setting the “tone

at the top” for ethical behavior in the company. It is important for management

10-4

10-11 The auditor can choose among several overall responses to increased

fraud risk. The auditor may begin by first discussing the auditor’s findings about

greater emphasis may be placed on the importance of increased professional

skepticism. The auditor may place greater emphasis on management’s choice of

10-13 Revenue and related accounts receivable and cash accounts are

especially susceptible to manipulation and theft. Research finds that a majority of

financial statement fraud instances involve revenues and accounts receivable. As

a result of the frequency of financial reporting frauds involving revenue

10-14 The handling of cash by individuals operating cash registers is particularly

susceptible to theft. The notice “your meal is free if we fail to give you a receipt”

example, the auditor may attempt to corroborate the information obtained from

management by making assessment inquiries of individuals in accounts

receivable and shipping. Interrogative inquiry is used to determine if the

10-5

10-16 When making inquiries of a deceitful individual, three examples of verbal

sweating or fidgeting.

10-17 When the auditor suspects that fraud may be present, auditing standards

require the auditor to obtain additional evidence to determine whether material

fraud has occurred. Auditing standards also require the auditor to consider

magnitude by senior management is at least a significant deficiency and may be

a material weakness in internal control over financial reporting. This includes

fraud by senior management that results in even immaterial misstatements. If the

discussion occurred and who participated.

Procedures performed to obtain information necessary to identify and

assess the risks of material fraud.

Specific risks of material fraud that were identified at both the overall

Results of the procedures performed to address the risk of management

override of controls.

taken by the auditor.

The nature of communications about fraud made to management, the

audit committee, or others.

10-6

Multiple Choice Questions From CPA Examinations

10-19 a. (1) b. (2) c. (4)

10–22 a. (3) b. (3) c. (4)

Discussion Questions and Problems

10-23

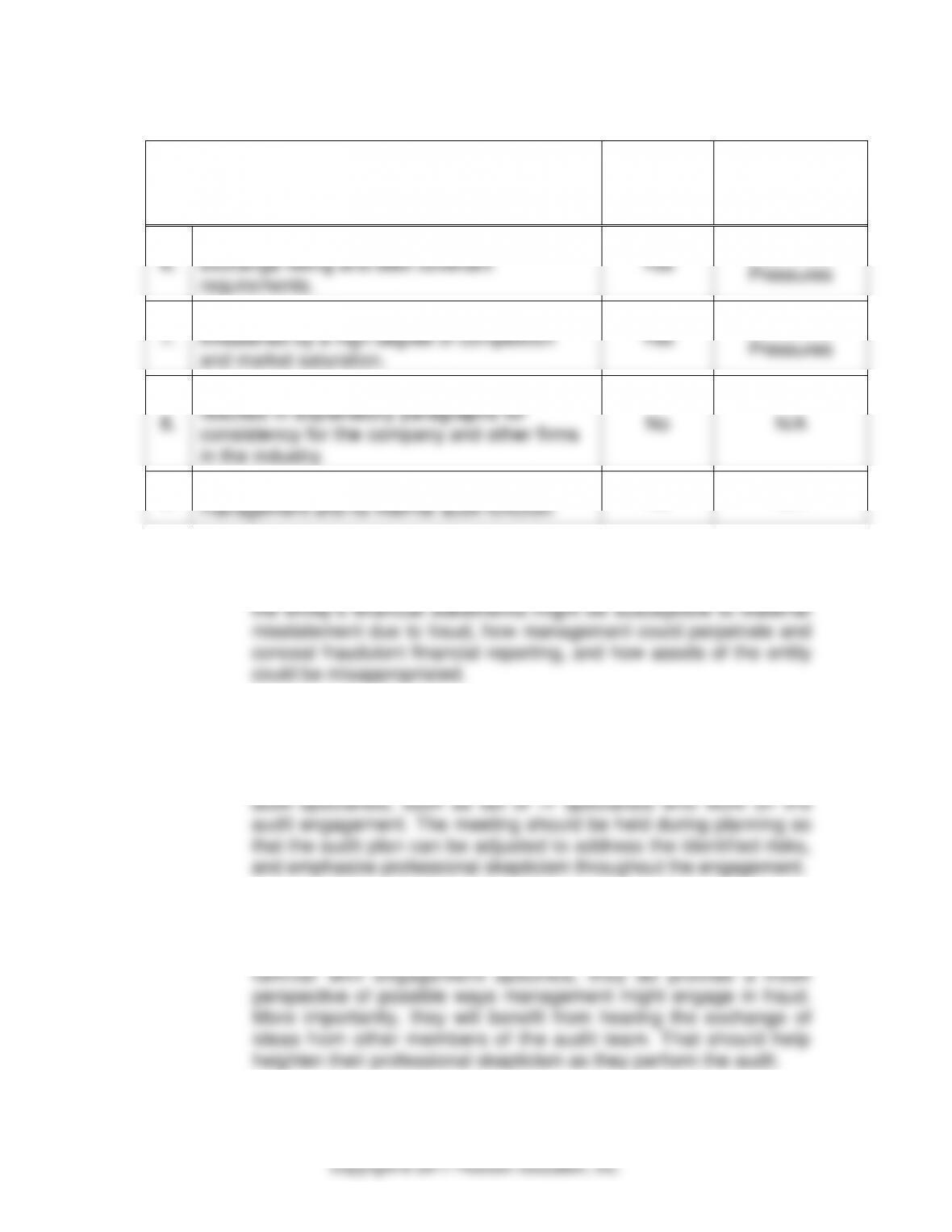

INFORMATION

a.

FRAUD

RISK

b.

FRAUD

CONDITION

1.

Significant operations are located and

conducted across international borders in

jurisdictions where differing business

environments and cultures exist.

Yes

Opportunities

2.

There are recurring attempts by management to

justify marginal or inappropriate accounting on

the basis of materiality.

Yes

Attitudes/

Rationalization

3.

The company’s controller works very hard,

including evenings and weekends, and has not

taken a vacation in two years.

Yes

Opportunities

4.

The company’s board of directors includes

a majority of directors who are independent

of management.

No

N/A

5.

Assets and revenues are based on significant

estimates that involve subjective judgments

and uncertainties that are hard to corroborate.

Yes

Opportunities

10-7

10-23 (continued)

INFORMATION

a.

FRAUD

RISK

b.

FRAUD

CONDITION

6.

The company is marginally able to meet

exchange listing and debt covenant

requirements.

Yes

Incentives/

Pressures

7.

The company’s financial performance is

threatened by a high degree of competition

and market saturation.

Yes

Incentives/

Pressures

8.

New accounting pronouncements have

resulted in explanatory paragraphs for

consistency for the company and other firms

in the industry.

No

N/A

9.

The company has experienced low turnover in

management and its internal audit function.

No

N/A

10-24 a. The purpose of the audit team’s brainstorming session is for the

audit team to exchange ideas about how and where they believe

b. The brainstorming meeting should ordinarily involve the key members

of the audit team, ranging from audit staff members to partners on

the engagement. This meeting would include audit team members

located in other offices who work on the engagement as well as

c. The two staff members on the engagement are just as responsible

for engaging in the exchange of ideas as other members of the

engagement team. While the two new staff accountants may not be

10-8

10-24 (continued)

d. The auditor has a responsibility to plan and perform the audit to

obtain reasonable assurance about whether the financial statements

participated.

10-25 a.

WEAKNESSES IN PROCESSES

RECOMMENDATION

1. There is no basis for

establishing the number of

paying patrons.

Prenumbered admission tickets should be issued

upon payment of the admission fee.

2. There is no segregation of

duties between persons

responsible for collecting

admission fees and persons

responsible for authorizing

admission.

One clerk (hereafter referred to as the cash

receipts clerk) should collect admission fees

and issue prenumbered tickets. The other clerk

(hereafter referred to as the admission clerk)

should authorize admission upon receipt of the

ticket or proof of membership.

3. An independent count of

paying patrons is not made.

The admission clerk should retain a portion of

the prenumbered admission ticket (admission

ticket stub).

4. There is no proof of accuracy

of amounts collected by the

clerks.

Admission ticket stubs should be reconciled with

cash collected by the treasurer each day.

5. Cash receipts records are not

promptly prepared.

The cash receipts should be recorded by the

cash receipts clerk daily on a permanent record

that will serve as the first record of

accountability.

6. Cash receipts are not promptly

deposited. Cash should not be

left undeposited for a week.

Cash should be deposited at least once each

day.

10-9

10-25 (continued)

WEAKNESSES IN PROCESSES

RECOMMENDATION

7. There is no proof of the

accuracy of amounts

deposited.

Authenticated deposit slips should be compared

with daily cash receipts records. Discrepancies

should be promptly investigated and resolved.

In addition, the treasurer should establish a

policy that includes a review of cash receipts.

8. There is no record of the

internal accountability for

cash.

The treasurer should issue a signed receipt for

all proceeds received from the cash receipts

clerk. These receipts should be maintained and

should be periodically checked against cash

receipts and deposit records.

receipts.

c. The weaknesses have less of an effect on the likelihood of fraudulent

financial reporting than they do for misappropriation of assets. The

10–26 a. This fraud is an example of both asset misappropriation and

purchases from her husband or others. Behavioral red flags in the

office may have included being too controlling and not delegating

10–10

10-26 (continued)

c. It would be unusual for a manufacturing company to have several

cashier’s checks rather than using their primary bank account pre–

numbered checks. The auditors can use audit software to search

for recurring payments to vendors who are not on the company’s

approved vendor list, or can also search for cash disbursements

of the company.

d. Koss Corporation could have had more monitoring controls in

place to oversee the activities of the principal accounting officer.

The company also could have had a policy requiring employees

e. The auditors could have changed their audit approach from year–

to-year so that it was not as predictable. The auditors could have

fraud or failed to exercise due professional care. For example,

assume a fraud is covered up by incorrectly footing a bank

reconciliation, but the auditor failed to independently verify the

accuracy of the bank reconciliation. In that case, the auditor would