The auditors ultimate substantive tests depend on the relative effectiveness of internal

controls related to accounts payable.

For sales, the completeness transaction-related audit objective affects the existence

balance-related audit objective.

Auditors seldom expect to find misstatements when testing payroll transactions.

When auditing financial instruments, interest income and dividends can be recomputed

and compared to a public source.

Tolerable exception rate (TER) is inversely related to sample size.

The starting point for the verification of current-year acquisitions of property, plant, and

equipment is normally a client-prepared schedule of all acquisitions recorded in the

general ledger during the year.

The first step in applying materiality is to determine performance materiality.

Changes in an estimate, such as a change in the estimated useful life of an asset for

depreciation purposes, affect consistency but not comparability, and therefore require an

explanatory paragraph in the audit report.

When designing an audit program for tests of details of balances, the auditor should

make assumptions about inherent risk and control risk, and predictions concerning the

outcome of tests of controls, substantive tests of transactions, and analytical procedures.

The auditor must extend the audit procedures in the audit of year-end cash when there

are inadequate internal controls.

The purpose of stratification is to permit auditors to emphasize certain aspects of a

population and deemphasize others.

One very useful method of auditing depreciation is to use an analytical procedure to test

for reasonableness.

Operational audits are primarily geared towards improving a company’s operational

efficiency and effectiveness.

If loans require significant restrictions on the activities of the company, they must be

disclosed in the footnotes.

Accounts with zero or negative year-end balances have no chance of being included in a

standard probability proportional to size (PPS) sample.

Since confirmation replies and copies of client agreements are not considered schedules

in the usual sense, they are not indexed and filed.

A proof of cash disbursements is not effective for discovering checks written for an

improper amount, fraudulent checks, or misstatements in which the dollar amount

appearing in the cash disbursements records is incorrect.

Whenever practical and reasonable, the confirmation of accounts receivable is required

of CPAs.

Auditing standards in the United States allow an auditor to perform an audit of a

nonpublic U.S. entity in accordance with both generally accepted auditing standards in

the U.S. and the ISAs.

The auditor’s preliminary judgment about materiality is the maximum amount by which

the auditor believes the financial statements could be misstated and still not affect the

decisions of reasonable users.

Examining the minutes of the board of directors’ meetings for proper authorization

ordinarily tests the occurrence objective for capital stock transactions.

Many small, local accounting firms perform audits as their primary service to their

clients.

Since there are a large number of accounts involved in the acquisition and payment

cycle, there is the potential for classification misstatements, some of which are likely to

affect income.

Auditors may expand other substantive procedures to address the heightened risks of

fraud.

For significant risks, including fraud risks, the auditor should obtain an understanding

of the internal controls related to the risks.

Each client misstatement in accounts receivable must be analyzed to determine whether

it was consistent with the original assessed level of control risk.

Control activities are a subcomponent of the information and communication

component of internal control.

Integrity is one of the Institute of Internal Auditors’ ethical principles.

The only unmodified opinion audit report that does not include an explanatory

paragraph is when other auditors are involved. In this case only the introductory

paragraph is modified.

The two most common areas of fraud in payroll are the creation of fictitious employees

and the overstatement of individual payroll hours.

Section 404(b) of the Sarbanes Oxley Act requires that the auditor of a public company

attest to management’s report on the efficiency of internal controls over financial

reporting.

To maximize audit efficiency, the auditor should allocate less tolerable misstatement to

accounts that can be verified by using low-cost audit procedures, such as analytical

procedures, than to accounts that are more costly to audit.

The primary purpose of allocating the preliminary judgment about materiality to

financial statement accounts is to help the auditor decide the appropriate evidence to

accumulate.

Acceptable risk of incorrect acceptance (ARIA) and sample size are inversely related;

that is, as ARIA increases, sample size decreases.

Three conditions are required for a contingent liability to exist. Which of the following

is not one of those conditions?

A) There is a potential future payment to an outside party or the impairment of an asset

that resulted from an existing condition.

B) The outcome must be resolved by a third-party.

C) There is uncertainty about the amount of the future payment or impairment.

D) The outcome will be resolved by some future event or events.

When planning the sample,

A) auditors using attributes sampling assign a low, medium, or high acceptable risk of

overreliance.

B) tables are used by the auditor in statistical sampling to determine initial sample size.

C) most auditors use attributes sampling for medium to small populations.

D) the tolerable exception rate does not need to be specified for statistical sampling.

When the auditor is obtaining an understanding of the independent computer service

center’s internal controls, the auditor should

A) use the same criteria used to evaluate the client’s internal controls.

B) use different criteria because the service center resides outside the company.

C) use the same criteria used to evaluate the client’s internal controls but omit tests of

transactions.

D) use different criteria for the service center by including substantive tests of balances.

Any service that requires a CPA firm to issue a report about the reliability of an

assertion that is made by another party is a(n)

A) accounting and bookkeeping service.

B) attestation service.

C) assurance service.

D) tax service.

Controls which are built in by the manufacturer to detect equipment failure are called

A) input controls.

B) data integrity controls.

C) hardware controls.

D) manufacturer’s controls.

To test for cutoff errors which overstate liabilities, the auditor should trace the receiving

reports issued ________ to vendors’ invoices.

A) after year-end

B) before year-end

C) the last day of the fiscal year

D) both before and after year-end

When a client uses a service center for processing transactions,

A) the auditor can assume that the controls are adequate because it is an independent

enterprise.

B) auditing standards require the auditor to test the service center’s controls if the

service center application involves processing significant financial data.

C) and the user auditor decides to rely on the service auditor’s report, the user audit

must make reference to the report of the service auditor in the opinion on the user

organization’s financial statements.

D) none of the above

Which of the following requires recognition in the auditor’s opinion as to consistency?

A) The correction of an error in the prior year’s financial statements resulting from a

mathematical mistake in capitalizing interest.

B) A change in the estimate of provisions for warranty costs.

C) The change from the cost method to the equity method of accounting for investments

in common stock.

D) A change in depreciation method which has no effect on current year’s financial

statements but is certain to affect future years.

Whenever an auditor issues an audit report for a public company, the auditor can choose

to issue a report in which of the following forms?

I. A combined report on financial statements and internal control over financial

reporting

II. Separate reports on financial statements and internal control over financial reporting

A) I only

B) II only

C) either I or II

D) neither I nor II

Match seven of the terms (a-k) with the definitions provided below (1-7):

a. accounts receivable balance-related audit objectives

b. aged trial balance

c. alternative procedures

d. blank confirmation form

e. cutoff misstatements

f. evidence planning worksheet

g. negative confirmation

h. positive confirmation

i. realizable value of accounts receivable

j. timing difference in an account receivable confirmation

k. invoice confirmation

________ 1. the follow-up of a positive confirmation not returned by the debtor with

the use of documentation evidence to determine whether the recorded receivable exists

________ 2. a letter, addressed to the debtor, requesting that the recipient indicate

directly on the letter whether the stated account balance is correct or incorrect and, if

incorrect, by what amount

________ 3. misstatements that take place as a result of current period transactions

being recorded in a subsequent period, or subsequent period transactions being recorded

in the current period

________ 4. a letter, addressed to the debtor, requesting the recipient to fill in the

amount of the accounts receivable balance.

________ 5. a letter, addressed to the debtor, requesting a response only if the recipient

disagrees with the amount of the stated account balance

________ 6. a reported difference in a confirmation from a debtor that is determined to

be a timing difference between the client’s and debtor’s records and therefore not a

misstatement

________ 7. a listing of the balances in the accounts receivable master file at the

balance sheet date broken down according to the amount of time that has passed

between the date of sale and the balance sheet date

When comparing the auditor’s responsibility for detecting employee fraud and for

detecting errors, the profession has placed the responsibility

A) more on discovering errors than employee fraud.

B) more on discovering employee fraud than errors.

C) equally on discovering errors and employee fraud.

D) on the senior auditor for detecting errors and on the manager for detecting employee

fraud.

When designing tests of details of balances, an important point to remember is

A) auditors emphasize income statement accounts.

B) the audit procedures selected depends heavily on whether planned evidence for a

given objective is low, medium, or high.

C) if accounts receivable are overstated, then sales will be understated.

D) sales cutoff is the most important test of details of accounts receivable.

Which of the following would offer the best protection for a company that wishes to

prevent a reoccurrence of a previously detected “lapping” problem with trade accounts

receivable?

A) Separate duties so that the bookkeeper in charge of the general ledger has no access

to incoming mail.

B) Separate duties so that no employee has access to both checks from customers and

currency from daily cash receipts.

C) Have a mandatory vacation policy for employees who both handle cash and enter

cash receipts into the system.

D) Request that customer’s payment checks be made payable to the company and

addressed to the treasurer.

Privity of contract exists between

A) auditor and the federal government.

B) auditor and third parties.

C) auditor and client.

D) auditor and client attorney.

What distinguishes internal control evaluation and testing for financial and operational

auditing?

A) purpose of the work

B) scope of the work

C) both A and B

D) neither A nor B

You are auditing Raji and Company. You discover an item of inventory with an audited

value of $5,000 with a recorded amount of $3,000. If this is the only error you discover,

the projected misstatement for the sample would be

A) $5,000.

B) $2,000.

C) $3,000.

D) $4,000.

Auditing standards make ________ distinction(s) between the auditor’s responsibilities

for searching for errors and fraud.

A) little

B) a significant

C) no

D) various

Examples of unmodified opinions which contain modified wording (without adding an

explanatory paragraph) include

A) the use of other auditors.

B) the lack of consistent application of generally accepted accounting principles.

C) substantial doubt about the audited company (or the entity) continuing as a going

concern.

D) lack of consistent application of GAAP.

When determining tolerable exception rate (TER),

A) the auditor considers the degree of reliance to be placed on the control and the

significance of the control to the audit.

B) if only one internal control is used to support a low control risk assessment for an

objective, TER will be higher for the attribute than if multiple controls are used to

support a low control risk assessment for the same objective.

C) control deviations increase both the risk of material misstatements in the accounting

record, and will always result in misstatements.

D) a smaller sample size is needed for a low TER than for a high TER.

The computer-generated file which records acquisitions, disbursements and allowances

for each vendor is the

A) accounts payable master file.

B) cash disbursements file.

C) acquisitions transaction file.

D) purchase approval file.

Transaction-related audit objectives would most likely be performed in which phase of

the audit process?

A) plan and design audit approach

B) perform tests of controls and substantive tests of transactions

C) perform substantive analytical procedures and tests of details of balances

D) complete the audit and issue the audit report

All of the following are steps that should be performed in a review engagement except

for

A) understand the company’s ownership structure.

B) read the company’s financial statements.

C) perform analytical procedures.

D) assess fraud risk.

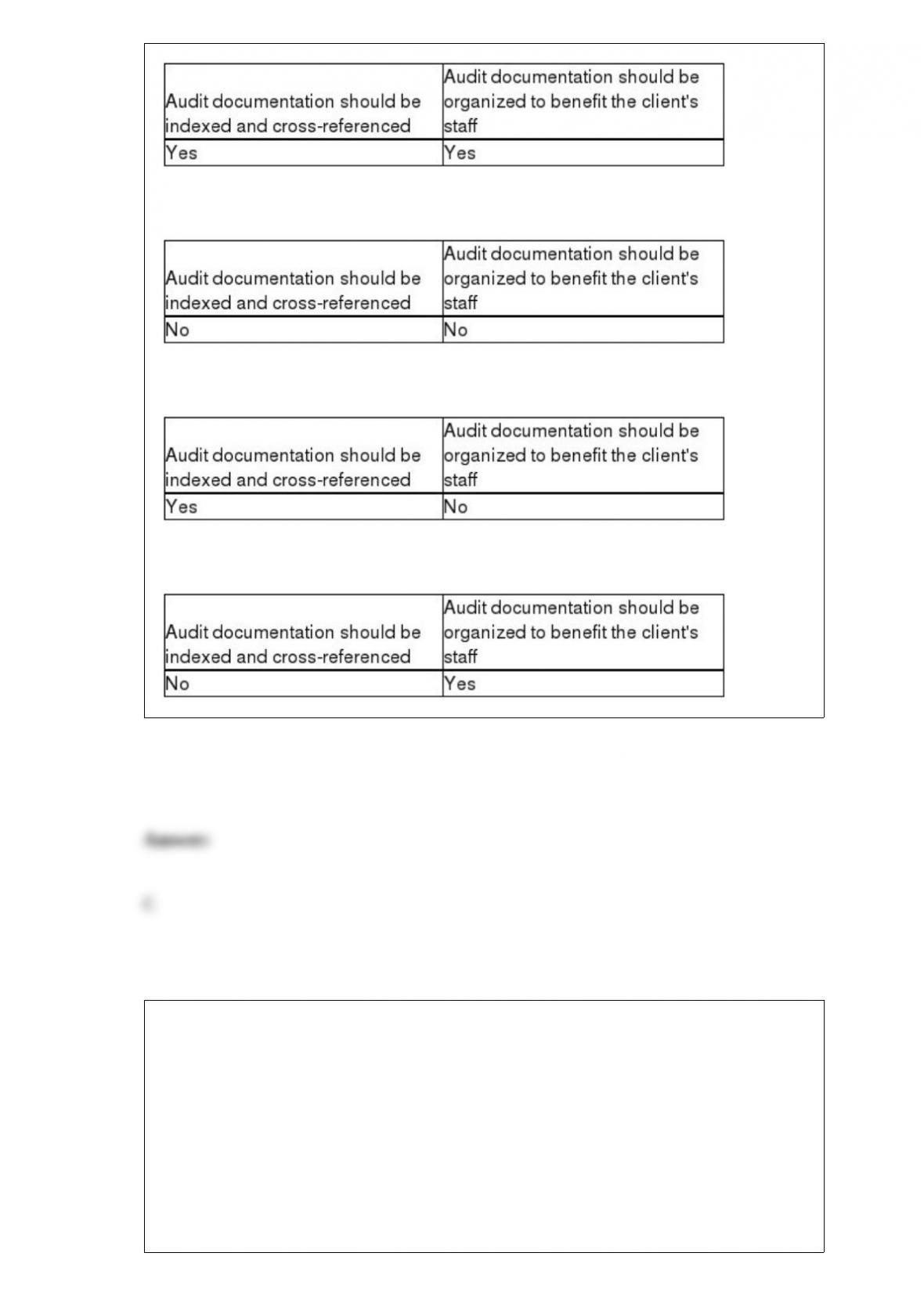

Audit documentation should possess certain characteristics. Which of the following is

true regarding those characteristics?

A)

B)

C)

D)

You are performing an audit of Hawk Company. In evaluating the accounts payable

balance you are concerned with the completeness assertion. Which of the following

audit procedures best satisfies your concern?

A) Send confirmations to only vendors with large balances.

B) Send confirmations to vendors with large, active, zero balance accounts and a

representative sample of all others.

C) Send confirmations to vendors chosen from sample stratified by the dollar balance.

D) Send confirmations to all vendors.

At the completion of the audit, management is asked to make a written statement that it

is not aware of any undisclosed contingent liabilities. This statement would appear in

the

A) management letter.

B) letter of inquiry.

C) letters testamentary.

D) management letter of representation.

The permanent files included as part of audit documentation do not normally include

A) a copy of the current and prior years’ audit programs.

B) copies of articles of incorporation, bylaws and contracts.

C) information related to the understanding of internal control.

D) results of analytical procedures from prior years.

Which of the following statements is not true?

A) Inherent risk is inversely related to the amount of audit evidence whereas detection

risk is directly related to the amount of audit evidence required.

B) Inherent risk is directly related to evidence whereas detection risk is inversely

related to the amount of audit evidence required.

C) Inherent risk is the susceptibility of the financial statements to material error,

assuming no internal controls.

D) Inherent risk and control risk are assessed by the auditor and function independently

of the financial statement audit.

Shown below (1 through 5) are the five types of tests which auditors use to determine

whether financial statements are fairly stated. Which three are substantive tests?

1. risk assessment procedures

2. tests of controls

3. substantive tests of transactions

4. substantive analytical procedures

5. tests of details of balances

A) 1, 2, and 3

B) 3, 4, and 5

C) 2, 3, and 5

D) 2, 3, and 4

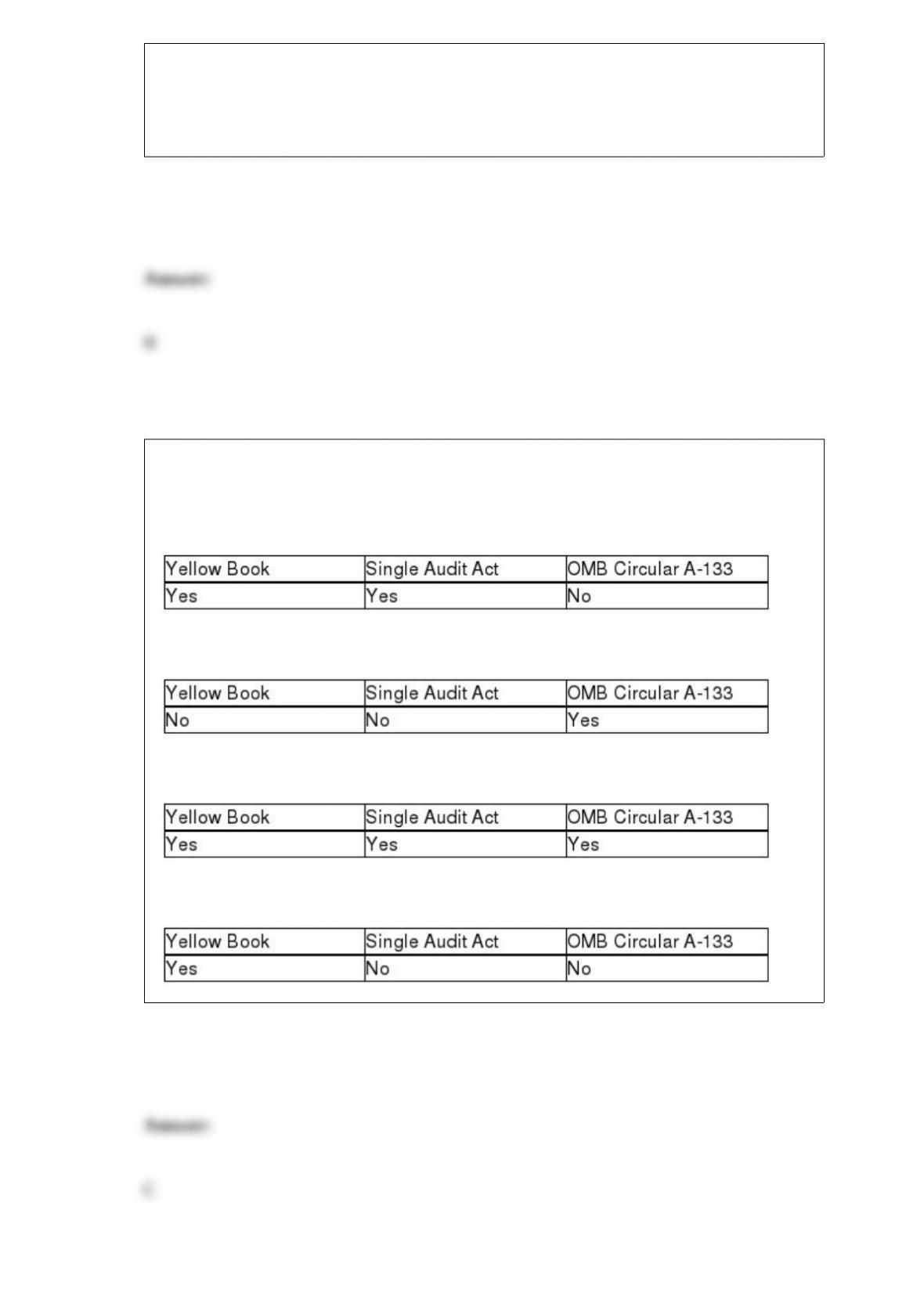

When a state or local government agency receives federal funds, it is subject to the

audit requirements of

A)

B)

C)

D)

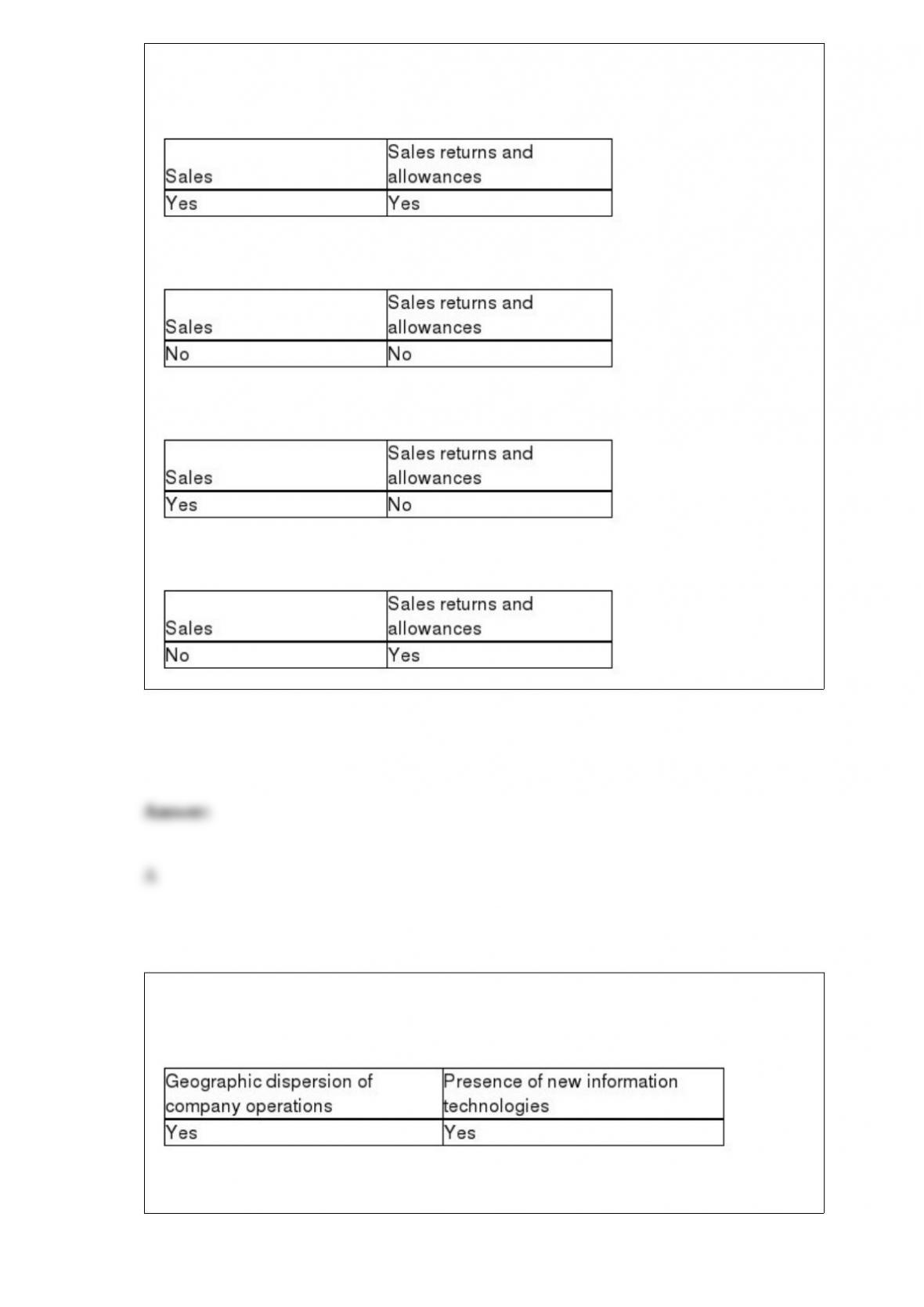

Cutoff misstatements can occur for

A)

B)

C)

D)

Which of the following factors may increase risks to an organization?

A)

B)

C)

D)

Evidence for a review engagement consists primarily of

A)

B)

C)

D)

Which type of misstatement is always a fraud?

A) sales included in the journals for which no shipment was made

B) sales to related parties, such as officers and subsidiaries

C) shipments made to nonexistent customers and recorded as sales

D) sales recorded more than once.

The auditor is concerned about authorization at three key points. What are the key

points?

Discuss the need for maintaining professional skepticism during an audit.

Auditors frequently audit statements prepared on bases other than GAAP. Discuss four

commonly used bases other than GAAP.

Describe the differences between statistical and nonstatistical sampling in terms of (1)

the sample selection methods used, and (2) quantification of sampling risk.

There are 14 steps to attributes sampling, divided into three sections: plan the sample,

select the sample and perform the audit procedures, and evaluate the results. Discuss the

three steps that comprise the “evaluate the results” section.

What are two important internal control procedures that companies should implement to

prevent misstatements in owners’ equity when a company maintains its own records of

stock transactions and outstanding stock?

List and describe the three factors that influence the organizational structure of all CPA

firms. What are the most common forms of CPA firm organization?

There are three main reasons why an auditor should properly plan audit engagements.

Discuss each of these reasons.

Describe three computer auditing techniques available to the auditor.

Why is the appropriateness of audit evidence obtained by the auditor important in

forming an audit opinion? Describe the qualities information should have to be

considered appropriate by the auditor.

Principles related to the auditor’s responsibilities in the audit stress three important

personal qualities that the auditor should possess. List and discuss these three qualities.

When designing tests of controls and substantive tests an auditor is gathering evidence

to satisfy the transaction-related audit objectives. What are the four steps the auditor

would normally follow to reduce assessed control risk?

Separation of duties is essential in preventing errors and intentional misstatements on

the financial statements. List below the four general guidelines.

The audit of the inventory and warehousing cycle will be affected by the results from

other business processes. Identify the “other” business cycles and how they impact the

audit of inventory.

Distinguish between constructive fraud and fraud.

Discuss the key internal controls related to the disposal of property, plant, and

equipment.

Discuss the circumstances in which it is desirable to send confirmation requests to the

client’s vendors.

Discuss the four aspects of the audit of cost accounting with which the auditor is most

concerned.

List and describe the six elements of quality control. Who establishes the standards for

quality control?

Discuss the key internal controls that should be present in the receiving goods and

servicesfunction in the acquisitions and payment cycle.