The estimated unpaid obligations for services or benefits that have been received before

the balance sheet date are

A) accounts payable.

B) accounts receivable.

C) unearned liabilities.

D) accrued liabilities.

Which ratio is computed by dividing operating income by net sales?

A) gross profit percent

B) profit margin

C) return on sales

D) return on assets

To succeed in an action against the auditor, the client must be able to show that

A) the auditor was fraudulent.

B) the auditor was grossly negligent.

C) there was a written contract.

D) there is a close causal connection between the auditor’s behavior and the damages

suffered by the client.

When choosing the appropriate acceptable risk of overreliance, the auditor needs to

A) rely on his/her professional judgment.

B) err on the side of conservatism.

C) consult the professional standards.

D) follow SEC guidelines.

The AICPA’s Code of Professional Conduct requires CPAs to maintain the

confidentiality of client information. This rule would be violated if a CPA disclosed

information without a client’s consent as a result of a

A) subpoena or summons.

B) peer review.

C) complaint filed with the trial board of the Institute.

D) request by a client’s largest stockholder.

To determine that sales are accurately recorded, the unit prices on the duplicate sales

invoices are normally compared with

A) the original invoices.

B) an approved master price list.

C) the amounts recorded in the sales journal for that transaction.

D) the amounts posted to the customer’s account in the accounts receivable master file.

In auditing payroll, the auditor wants to determine that the individuals included in her

sample were employees of the company for the period under review. What is the

auditor’s best source of evidence?

A) examination of human resource records

B) examination of the payroll master file

C) examination of the payroll transaction file

D) examination of the payroll tax records

Which of the following is a business function related to sales returns and allowances?

A) processing customer orders

B) writing off uncollectible accounts

C) processing and recording credit memos

D) granting credit

Cutoff misstatements occur

A) either by error or fraud.

B) by error only.

C) by fraud only.

D) randomly without causes related to errors or fraud.

Which of the following best defines fraud in a financial statement auditing context?

A) Fraud is an unintentional misstatement of the financial statements.

B) Fraud is an intentional misstatement of the financial statements.

C) Fraud is either an intentional or unintentional misstatement of the financial

statements, depending on materiality.

D) Fraud is either an intentional or unintentional misstatement of the financial

statements, depending on consistency.

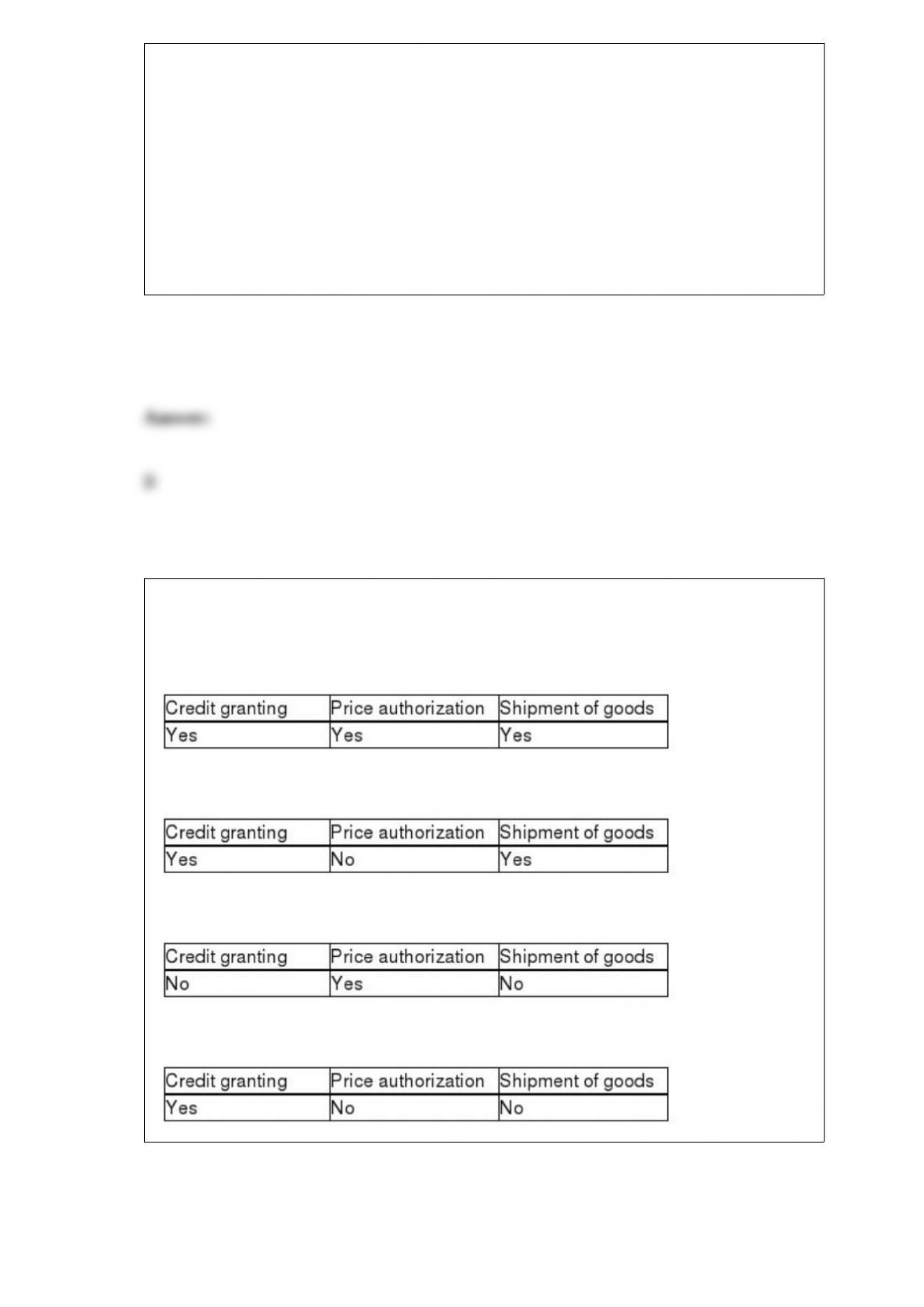

Which of the following is the appropriate point at which the auditor deems

authorization to be critical?

A)

B)

C)

D)

Draft a report that would be appropriate when an independent accountant has performed

a compilation of financial statements with disclosures in accordance with accounting

principles generally accepted in the United States of America.

External auditors would consider internal auditors effective if they

A) are independent of the operating units being evaluated.

B) are competent and well trained.

C) apply a systematic and disciplined approach, including quality control.

D) all of the above.

Several months after an unqualified audit report was issued, the auditor discovers the

financial statements were materially misstated. The client’s CEO agrees that there are

misstatements, but refuses to correct them. She claims that “confidentiality” prevents

the CPA from informing anyone. Which of the following statements is correct?

A) The CEO is correct and the auditor must maintain confidentiality.

B) The CEO is incorrect, but since the audit report has been issued, it is too late to

correct the report.

C) The CEO is correct, but to be ethically correct, the auditor should violate the

confidentiality rule and disclose the error.

D) The CEO is incorrect, and the auditor has an obligation to issue a revised audit

report, even if the CEO will not correct the financial statements.

In an IT system, automated equipment controls or hardware controls are designed to

A) correct errors in the computer programs.

B) monitor and detect errors in source documents.

C) detect and control errors arising from the use of equipment.

D) arrange data in a logical sequential manner for processing purposes.

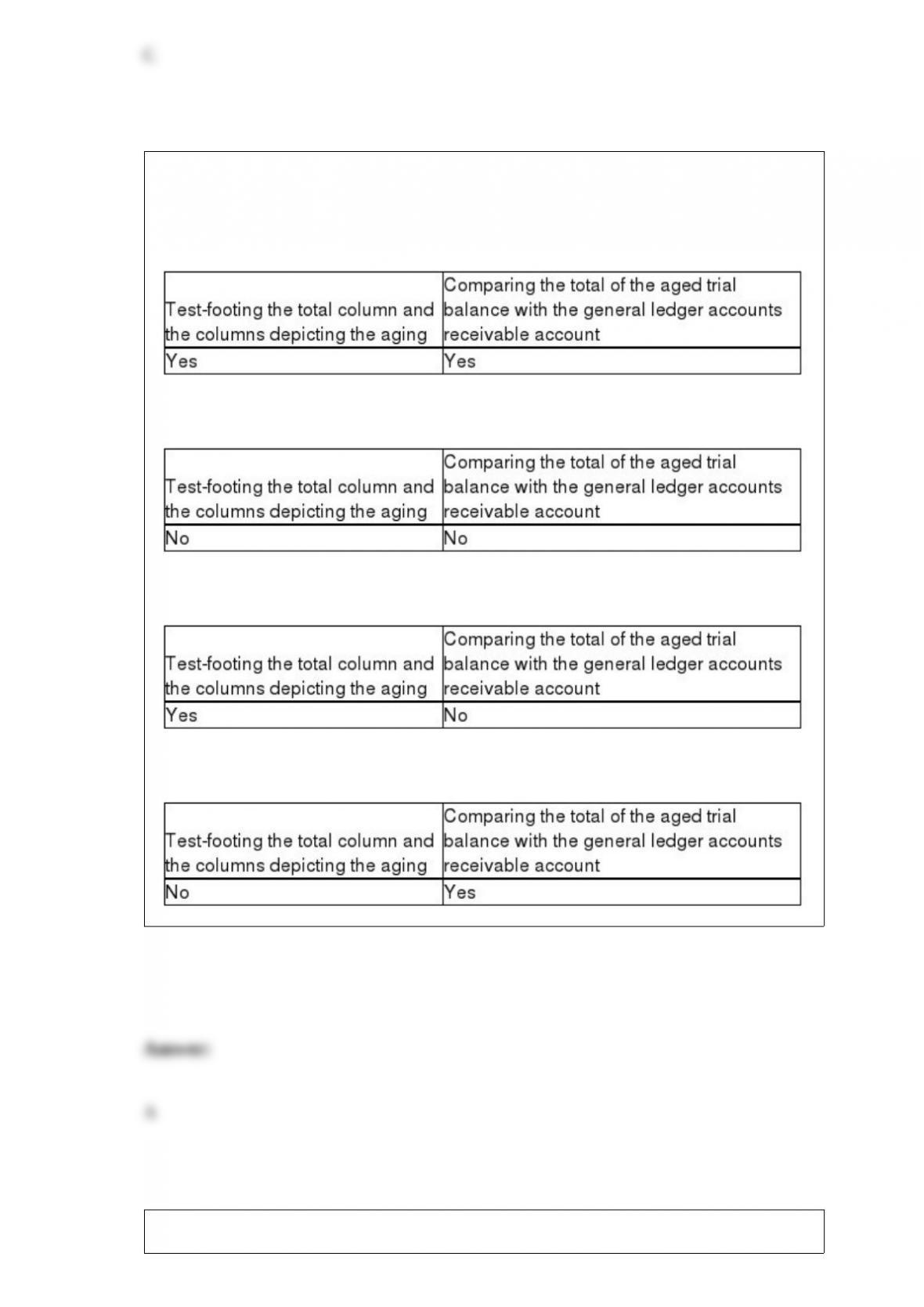

Testing the information on the aged trial balance for detail tie-in is a necessary audit

procedure, which would normally include

A)

B)

C)

D)

Which of the following is a true statement regarding the enforcement mechanism for

CPA conduct?

A) The PCAOB has the authority to investigate and discipline registered public

accounting firms.

B) All disciplinary action by the AICPA must go through the Joint Trial Board.

C) Disciplinary actions taken by the AICPA are not disclosed to the public.

D) Only a few states have adopted the AICPA rules of conduct.

Companies are required to disclose in their proxy statement or annual filings with the

SEC the total amount of audit and non-audit fees paid to the audit firm for the two most

recent years. Which of the following is not one of the categories of fees that must be

disclosed?

A) tax fees

B) consulting fees

C) audit-related fees

D) all other fees

The reason for testing the client’s bank reconciliation is to verify whether the client’s

recorded bank balance is the same amount as the actual cash in bank, except for

deposits in transit, checks outstanding, and other reconciling items. The information

needed to complete the tests of the reconciliation is provided by the

A) client’s records and ledgers for the year under audit.

B) cutoff bank statement.

C) client’s records and ledgers for the subsequent year.

D) canceled checks for the year under audit.

Which of the following is an accurate statement regarding sampling?

A) A 95 percent confidence level provides a 5 percent sampling risk.

B) The auditor can perform the audit tests only after the sample items are selected.

C) The purpose of planning the sample is to make sure that the audit tests are performed

in a manner that provides the desired sampling risk and minimizes the likelihood of

nonsampling errors.

D) All of the above are accurate statements.

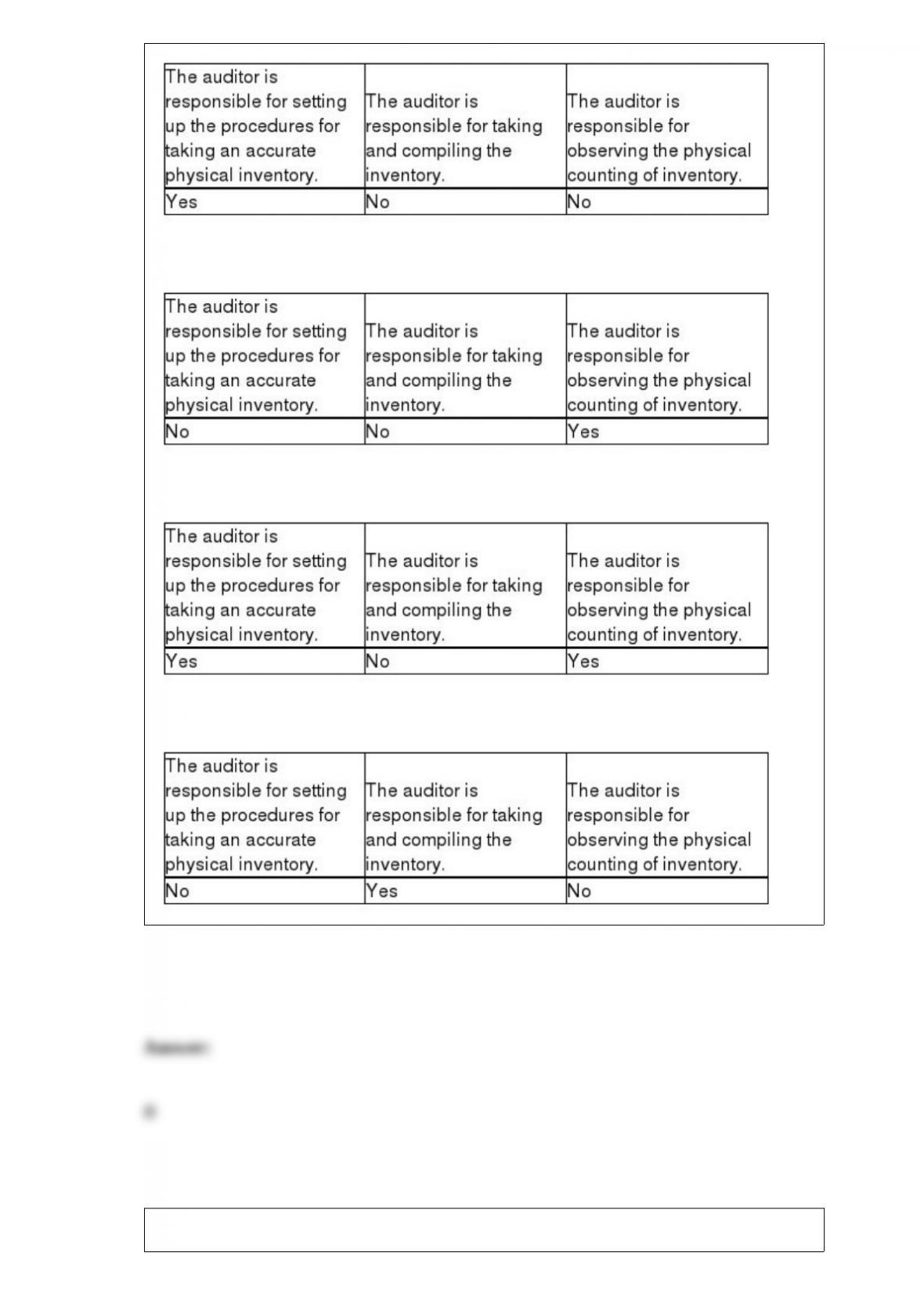

Which of the following statements is correct regarding the auditor’s responsibility with

respect to the year-end inventory procedures of an audit client?

A)

B)

C)

D)

When testing for fraudulent hours or fraudulent expense reports

A) it is easy for the auditor to discover fraudulent hours because of the abundance of

available evidence.

B) it is difficult to prevent fraud in these two areas with adequate internal controls.

C) management falsification of expense reports can be an indicator of disregard for

internal controls and the potential for fraud in other areas.

D) examining payroll records for approval is an important substantive tests of

transactions to uncover fraudulent hours.

When auditing financial instruments, a confirmation is sent to the broker-dealer

A) only if the client has poor internal controls.

B) to confirm interest and dividends.

C) to provide assurance on realizable value.

D) to confirm year-end holdings.

Which of the following is an accurate statement?

A) Auditing standards detail the requirements that a CPA firm must follow when it is

requested to provide an opinion on the application of accounting principles for a client

of another CPA firm.

B) SEC rules prohibit ownership in audit clients by those persons who can influence the

audit.

C) PCAOB rules require a CPA firm, before its selection as the company’s auditor to

document all relationships between the firm and the company.

D) All of the above are accurate statements.

When there is a justified departure from GAAP which is considered material, the

auditor should issue a(n)

A) standard unmodified opinion.

B) disclaimer of opinion.

C) unmodified opinion with an explanatory paragraph.

D) adverse opinion.

What type of report is issued when one or more material internal control weaknesses

exist?

A) unqualified opinion

B) disclaimer of opinion

C) adverse opinion

D) qualified opinion

Which of the following best describes an audit that emphasizes how efficiently and

effectively functions interact?

A) operational

B) compliance

C) financial

D) organizational

The audit procedure that requires an auditor to “foot the acquisition schedule” relates to

which balance-related audit objective?

A) classification

B) detail tie-in

C) existence

D) cut-off

Which of the following is the correct definition of “control deficiency”?

A) A control deficiency exists if the design or operation of controls does not permit

company personnel to prevent or detect misstatements on a timely basis.

B) A control deficiency exists if one or more deficiencies exist that adversely affect a

company’s ability to prepare external financial statements reliably.

C) A control deficiency exists if the design or operation of controls results in a more

than remote likelihood that controls will not prevent or detect misstatements.

D) A control deficiency exists if the design or operation of controls results in a more

than probable likelihood that controls will prevent or detect misstatements.

Below are listed possible misstatements that could occur in the sales and collections

cycle. Provide the analytical procedure that would be most useful in detecting the

possible misstatement.

a. overstatement of sales and accounts receivable

b. uncollectible accounts receivable that have not been provided for

c. overstatement of sales returns and allowances

The auditor traces items from the source documents to the journals in order to

accumulate audit evidence that will satisfy the

A) existence objective.

B) completeness objective.

C) ownership objective.

D) valuation objective.

Which of the following circumstances impairs an auditor’s independence?

I. Litigation by a client against an audit firm claiming a deficiency in the previous audit

II. Litigation by a client against an audit firm related to tax services

III. Litigation by an audit firm against a client claiming management fraud or deceit

A) I and II

B) I and III

C) II and III

D) I, II, and III

Which of the following would most likely not be classified as a related-party

transaction?

A) an advance of one week’s salary to an employee

B) sales of merchandise between affiliated companies

C) loans or credit sales to the principal owner of the client company

D) exchanges of equipment between two companies owned by the same person

When selecting staff for the audit engagement

A) only staff members who are CPAs should be assigned to the audit.

B) only managers and above need to have appropriate competence and capabilities to

perform the audit.

C) continuity of staff members from year to year should not be a factor.

D) staff assigned to the audit must be knowledgeable about the client’s industry.