The sum of the tolerable exception rate and the estimated population exception rate is

the precision of the initial sample estimate.

Operational audits are often categorized as functional, organizational, or special

assignments.

Subsequent events represent events that occasionally occur after the balance sheet date,

but before the issuance of the financial statements and the auditor’s report, that have an

effect on the financial statements.

Considerable guidance is provided by the AICPA Guide for Prospective Financial

Statements which includes criteria against which an attestation engagement can be

compared.

Paying employees for their services ends the payroll and personnel cycle.

Statements on Standards for Accounting and Review Services (SSARS) are issued by

the SEC.

An analytical procedure to determine a possible misstatement of commission expense is

to compare commission expense to salaries payable.

Favorable results from analytical procedures may reduce the extent to which the auditor

needs to test details of balances.

Required sample size increases as the auditor’s tolerable misstatement for an account

balance or class of transactions decreases.

When there is a lack of consistent application of GAAP due to a new accounting

pronouncement, no explanatory paragraph is required.

A nonaudit engagement in which the accountant undertakes to present, in the form of

financial statements, information that is the representation of management, without

undertaking to express any assurance on the statements is called a review engagement.

In an audit of a nonpublic company, the less control risk there is, the smaller the amount

of planned substantive evidence that is required.

Only tests of details of cash balances are useful when auditors are specifically testing

for fraud.

Information obtained by a CPA from a client is legally privileged in federal court.

Auditors must perform tests of controls separately from substantive tests of

transactions.

Auditors perform preliminary analytical procedures to better understand the client’s

business and to assess client business risk.

An effective procedure to test the occurrence/existence objective for sales is to vouch

sales journal entries to copies of sales orders, shipping documents, and sales invoices.

The results of tests of controls and substantive tests of transactions affect the design of

tests of details of balances.

The audit procedure “Examine canceled check for authorized signature, proper

endorsement, and cancellation by the bank” is used to test the occurrence objective for

cash disbursements.

One of the auditor’s primary objectives when auditing manufacturing equipment is

completeness.

When documenting their understanding of a client’s internal controls, auditors are

required to use narratives.

A narrative should describe the disposition of every document and record in the system.

The scope of the auditor’s report on internal control is limited to obtaining reasonable

assurance that significant weaknesses in internal control are identified.

Internal auditing standards are included in the Blue Book.

When a client has standard cost records, an efficient and useful method of determining

valuation is to review and analyze variances.

An acquisitions transaction file is a computer generated file that includes all

information entered into the system regarding acquisition transactions.

The assessment of control risk is the measure of the auditor’s expectation that internal

controls will prevent material misstatements from occurring or detect and correct them

if they have occurred.

If internal controls are tested and are considered effective, the auditor generally will

increase both substantive tests of transactions and tests of details of balances.

It is typically more difficult to evaluate the materiality of potential misstatements

resulting from a scope limitation than for failure to follow GAAP.

It is virtually impossible to reduce sampling risk to zero.

Substantive tests are procedures designed to test for dollar misstatements that directly

affect the correctness of financial statement balances.

An approved purchase requisition form authorizes shipment of goods to customers.

Confirmations are among the most expensive type of evidence to obtain.

Subsequent discoveries of facts requiring the reissuance of financial statements arise

from events occurring after the date of the auditor’s report.

Determining materiality requires professional judgment.

Total estimated misstatements include known misstatements and projected

misstatements plus a sampling error.

The primary purpose of a compliance audit is to determine whether the financial

statements are prepared in compliance with generally accepted accounting principles.

The embedded audit module approach requires the auditor to insert an audit module in

the client’s application system to to identify specific types of transactions.

Auditing standards define ________ as the magnitude of misstatements that

individually, or when aggregated with other misstatements, could reasonably be

expected to influence the economic decisions of users made on the basis of the financial

statements.

A) fraud

B) inherent risk

C) materiality

D) significant

Each page of the financial statements reviewed for a nonpublic entity should include the

reference

A) “These financial statements are unaudited.”

B) “We express no assurance on these financial statements.”

C) “See independent accountant’s review report.”

D) “See the audit opinion for the review procedures performed.”

The acceptable risk of overreliance

A) is normally assessed at a high level when auditing an accelerated filer public

company.

B) and the extent of tests of controls depends on assessed control risk for accelerated

filer public companies.

C) and the control risk will be assessed as low for audits where there is extensive

reliance on internal controls.

D) does not impact the effectiveness of the audit.

A substantive tests of transactions for acquisitions that would be used to provide

evidence regarding the occurrence assertion would be to

A) compare the classification with the chart of accounts by referring to vendors’

invoices.

B) recompute the clerical accuracy on the vendors’ invoice.

C) review the acquisitions journal for large or unusual amounts.

D) trace from a file of receiving reports to the acquisition journal.

Which of the following statements is most correct with respect to the evaluation of

nonprobabilistic sample results?

A) It is acceptable to make nonprobabilistic evaluations only when probabilistic sample

selection is used.

B) It is acceptable to make nonprobabilistic evaluations only if the auditor cannot

quantify sampling risk.

C) It is never acceptable to evaluate a nonprobabilistic sample using statistical methods.

D) All of the above are correct.

Ethics are

A) needed in the professions, but is not needed for society in general.

B) a set of moral principles or values.

C) not formed by life experiences.

D) always incorporated in laws.

An audit to determine whether an entity is following specific procedures or rules set

down by some higher authority is classified as a(n)

A) audit of financial statements.

B) compliance audit.

C) operational audit.

D) production audit.

Which of the following is likely to be detected as part of the audit of the bank

reconciliation?

A) failure to bill a customer

B) duplicate payment of a vendor invoice

C) cash received by the client after year-end, but included in cash receipts in the current

year

D) an embezzlement of cash by intercepting cash receipts from customers before they

are recorded

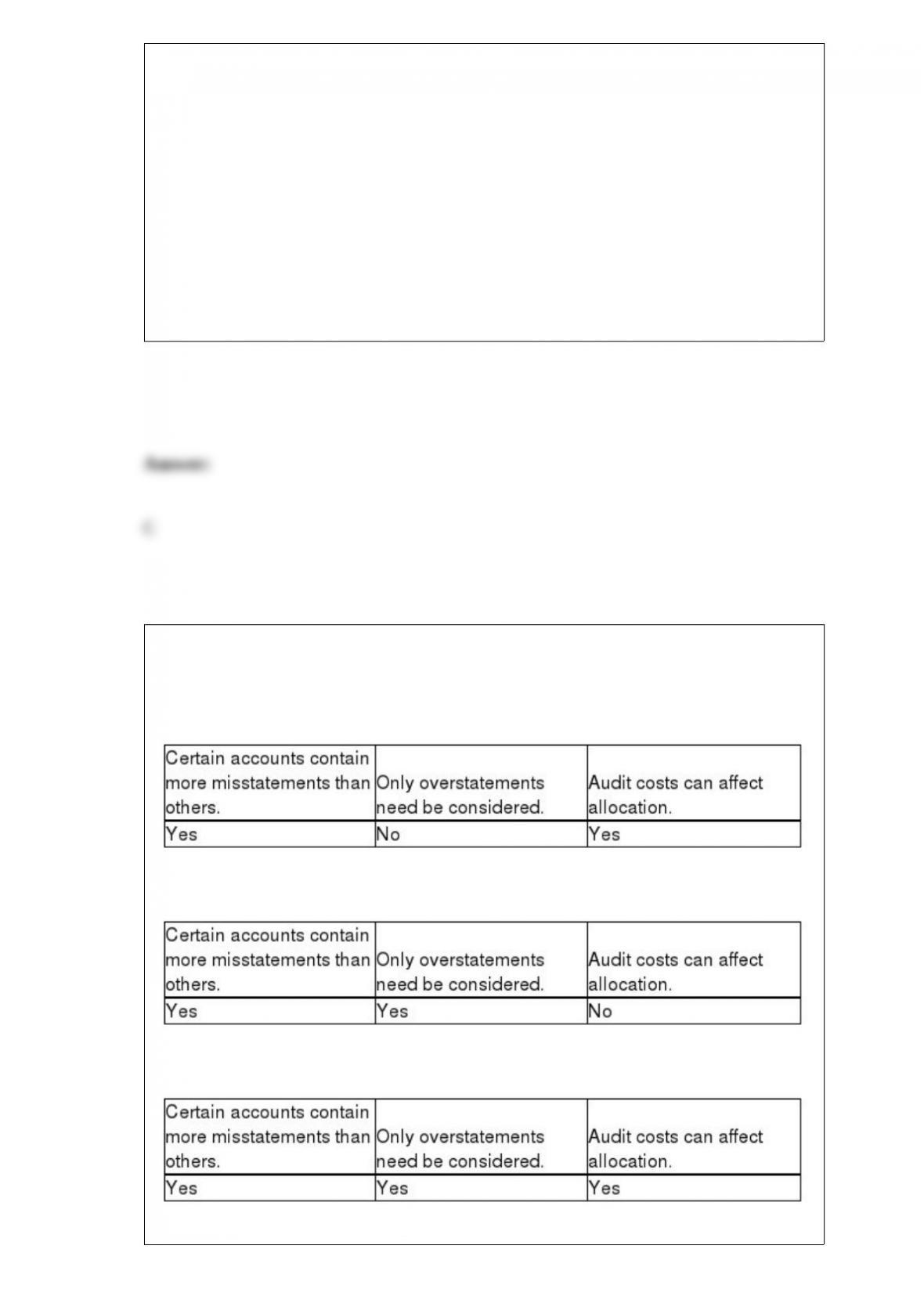

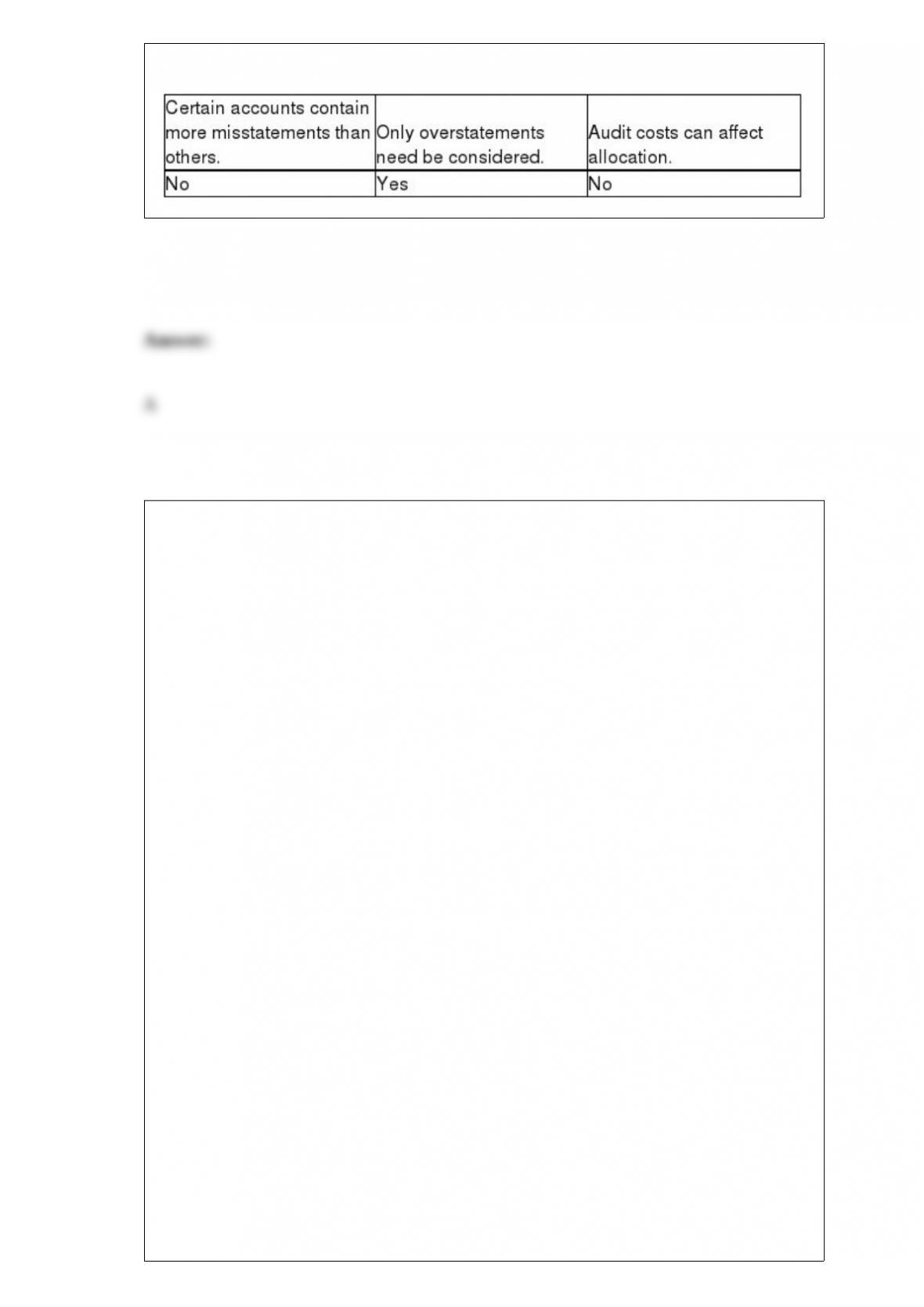

Which of the following are major difficulties auditors face when allocating materiality

to balance sheet accounts?

A)

B)

C)

D)

The following situations involve a possible violation of the AICPA’s Code of

Professional Conduct. For each situation, 1/ determine the applicable rule from the

Code, 2/ decide whether or not the Code has been violated, and 3/ briefly explain how

the situation violates (or does not violate) the Code.

a. In 2014, Freeman and Johnson, both CPAs, decided to form a CPA practice. In 2016,

Freeman and Johnson approached Bill Delaney, a physician and medical expert, and

asked him to assist them with their growing medical consulting practice. Delaney

agreed, but only after he was given an ownership interest in the firm. Delaney does not

intend to quit his private medical practice.

Rule: ________ Violation? Yes No

Explanation:

b. Brian DePalie has a successful dentistry practice in Charleston. Brian has

recommended one of his patients to Katie Walton, CPA. To show gratitude for the

referral, Katie has agreed to pay Brian a token gift of $50. Katie discloses the payment

arrangement to her new clients.

Rule: ________ Violation? Yes No

Explanation:

c. The accounting firm of Bayer & Peng, CPAs, is negotiating a fee with a new audit

client. They agree the client will pay $50,000 if Bayer & Peng issues a clean,

unmodified opinion, $40,000 if a qualified opinion is issued, and only $20,000 if an

adverse opinion is issued.

Rule: ________ Violation? Yes No

Explanation:

d. Don Smith, CPA, is a member of the engagement team that performs the audit of

Shaw Corporation. Don’s five-year-old daughter, Precious, received ten shares of Shaw

Corporation’s common stock for her fifth birthday. The stock was a gift from Precious’s

grandmother.

Rule: ________ Violation? Yes No

Explanation:

e. Jennifer Harris, CPA, is a partner in the CPA firm that audits Alltech, Inc., a closely

held corporation. Jennifer’s sister-in-law is the chief financial officer at Alltech, Inc.

Rule: ________ Violation? Yes No

Explanation:

The starting point for the verification of the balance in the general bank account is to

obtain

A) a bank reconciliation from the client.

B) the client’s cash account from the general ledger.

C) a cutoff bank statement directly from the bank.

D) the client’s year-end bank statement.

An auditor is likely to use four types of procedures to support the operating

effectiveness of internal controls. Which of the following would generally not be used?

A) make inquiries of appropriate client personnel

B) examine documents, records, and reports

C) reperform client procedures

D) inspect design documents

Which of the following is most correct regarding the requirements under Section 404 of

the Sarbanes-Oxley Act?

A) The audits of internal control and the financial statements provide reasonable

assurance as to misstatements.

B) The audit of internal control provides absolute assurance of misstatement.

C) The audit of financial statements provides absolute assurance of misstatement.

D) The audits of internal control and the financial statements provide absolute

assurance as to misstatements.

Practitioners who perform preparation, compilation, or review engagements are referred

to in the Statements on Standards for Accounting and Review Services (SSARS)

standards as

A) bookkeepers.

B) accountants.

C) auditors.

D) CPAs.

Which of the following accounts is not associated with the acquisition and payment

cycle?

A) common stock

B) property, plant and equipment

C) accrued property taxes

D) income tax expense

The auditor’s objectives for the sales and cash collections activities when the client is

primarily an e-commerce business as compared to a “brick and mortar” business are

A) unchanged.

B) expanded.

C) mitigated.

D) decreased.

Rodgers CPA believes that the rate of client billing errors is 4% and has established a

tolerable deviation rate of 6%. In auditing client invoices Rodgers should use

A) stratified sampling.

B) classical sampling.

C) proportional sampling.

D) attributes sampling.

As part of their internal control procedures, management needs to have procedures in

place to properly classify financial instruments as trading, available-for-sale, or

held-to-maturity, based on

A) cost.

B) intent.

C) maturity.

D) probable future gain or loss.

If the auditor has obtained a reasonable level of assurance about the fair presentation of

the financial statements through understanding internal control, assessing control risk,

testing controls, and analytical procedures, then the auditor

A) can issue an unqualified opinion.

B) can significantly reduce other substantive tests.

C) can write the engagement letter.

D) needs to perform additional tests of controls so that the assurance level can be

increased.

An examination of part of an organization’s procedures and methods for the purpose of

evaluating efficiency and effectiveness is what type of audit?

A) operational audit

B) compliance audit

C) financial statement audit

D) production audit

Under the Ultramares doctrine, ordinary negligence is insufficient for liability to third

parties unless the third party is

A) a primary beneficiary.

B) an injured party.

C) a foreseen user.

D) a bank.

Which of the following is correct regarding supplementary information?

A) The auditor must express an opinion on the supplementary information.

B) When reporting on supplementary information, the auditor uses a different

materiality threshold from that used in forming an opinion on the basic financial

statements.

C) If the auditor’s report on the audited financial statements contains an adverse

opinion, the auditor can still issue an unqualified opinion on the supplementary

information.

D) The auditor can issue a separate report on the supplementary information; it does not

need to be part of the report on the financial statements.

To minimize the opportunity for fraud, unclaimed salary checks should be

A) redeposited.

B) kept in the payroll department.

C) left with the employee’s supervisor.

D) held for the employee in the personnel department.

The most significant audit issue that came as a result of the court decision in the Escott

et al. v. BarChris Construction Corporation case in 1968 was

A) the court’s reaffirmation that the burden of proof was on the plaintiff to prove the

auditor was negligent.

B) the affirmation of an increase in the auditor’s responsibility when performing a

review of events subsequent to the balance sheet date (S-1 review) for registration

statements.

C) the increased auditor responsibility when associated with unaudited financial

statements.

D) the court’s refusal to allow the percentage-of-completion method of accounting for

revenues.

The auditor will issue an unqualified opinion on internal control over financial

reporting when

A) there are no identified material weaknesses as of the end of the fiscal year.

B) there have been no restrictions on the scope of the auditor’s work.

C) both a and b

D) either a or b

Which of the following statements are true for the standard unmodified opinion audit

report of a nonpublic entity?

I. The introductory paragraph states that management is responsible for the preparation

and content of the financial statements.

II. The scope paragraph states that the auditor evaluates the appropriateness of

accounting policies used and the reasonableness of significant accounting estimates

made by management.

A) I only

B) II only

C) I and II

D) Neither I nor II

A correct relationship among the auditor, the client, and the external users is

A) management of a public company hires the independent auditor.

B) the audit committee of a private company hires the independent auditor.

C) the client provides capital to the external users.

D) the external users can rely upon the auditor’s report to reduce information risk.

The appropriate audit report date for a standard unmodified opinion audit report for a

nonpublic entity should be

A) the date the financial statements are given to the Board of Directors.

B) the date of the financial statements.

C) the date the auditor completed the auditing procedures in the field.

D) 60 days after the date of the financial statements as required by the SEC.

Handling the receipt of ordered goods is a part of the ________ cycle.

A) purchasing

B) acquisition and payment

C) inventory

D) inventory and warehousing

If the auditor concludes that there are contingent liabilities, he or she must evaluate the

significance of the potential liability and the nature of the disclosure needed in the

financial statements. Which of the following statements is not true?

A) The potential liability is sufficiently well known in some instances to be included in

the financial statements as an actual liability.

B) Disclosure may be unnecessary if the contingency is highly remote or immaterial.

C) A CPA firm often obtains a separate evaluation of the potential liability from its own

legal counsel rather than relying on management or management’s attorneys.

D) The client’s attorneys must remain independent when evaluating the likelihood of

losing the lawsuit.

Which phase(s) of the audit uses inquiries of clients as a type of evidence?

A) plan and design

B) tests of controls and substantive tests of transactions

C) completion of the audit and issuance of the audit report

D) all of the above

Risk assessment procedures are performed by auditors during an audit in order to

A) determine the risk of material misstatement in the financial statements.

B) determine the amount of testing of internal control.

C) determine the extent of testing of details of balances.

D) determine the extent of testing of transactions.

External auditors typically consider internal auditors effective if they meet three

criteria. What are these criteria?

Which of the following is a substantive test of transactions?

A) Review personnel policies.

B) Account for a sequence of payroll checks.

C) Reconcile the disbursements in the payroll journal with the disbursements on the

payroll bank statement.

D) Examine printouts of transactions rejected by the computer as having invalid

employee IDs.

Distinguish between “joint and several liability” and ‘separate and proportionate

liability.”

Your CPA firm has completed the fieldwork for the 2016 audit of Sharp Corporation, a

private company with an October year-end. You were preparing to draft a standard,

unqualified audit report when you discovered that the audit manager on the Sharp

engagement owns 10 shares of Sharp’s common stock. Prepare the appropriate report.