An individual who is not party to the contract between a CPA and the client, but who is

known by both and is intended to receive certain benefits from the contract is known as

A) a third party.

B) a common law inheritor.

C) a tort.

D) a third-party beneficiary.

A proof of cash represents

A) a test of controls and substantive test of transactions.

B) a substantive test of transactions.

C) a substantive test of transactions and test of details of balances.

D) a test of details of balances.

Which of the following is part of planning?

A) Set materiality for the financial statements as a whole.

B) Estimate total misstatement in the segment.

C) Estimate the combined misstatement.

D) Compare the combined estimated with preliminary judgment.

A schedule of investment activity will include all of the following except

A) the purchases and sales.

B) ending balances.

C) the gains and losses.

D) the opinion of management as to the suitability of the investment to the company.

Which of the following will generally be considered a significant risk?

A) a sale to a customer

B) the determination of the amount of bad debt expense

C) the purchase of inventory

D) obtaining a loan from the bank

Which of the following statements is true when the CPA has been engaged to perform

an audit of financial statements?

A) The CPA firm is engaged and paid by the client; therefore, the firm has primary

responsibility to be an advocate for the client.

B) The CPA firm is engaged and paid by the client, but the primary beneficiaries of the

audit are those who rely on the financial statements.

C) Should a situation arise where there is no convincing authoritative standard

available, and there is a choice of actions which could impact a client’s financial

statements, the CPA is free to endorse the choice which is in the investors’ interests.

D) The CPA firm has primary responsibility to the FASB.

In the audit of notes payable, it is common to include tests of principal and interest

payments as a part of the audit of the acquisitions and payment cycle because the

payments are in the cash disbursements journal that is being sampled. It is also normal

to test these transactions as part of the capital acquisitions and repayment cycle because

A) it is not unusual for the auditor to duplicate a process, thereby gathering a larger

quantity of evidence.

B) replicating the evidence will provide the auditor with a higher level of assurance.

C) the tests done in the acquisitions and payments cycle will look only at the cash credit

side so the tests done in the capital acquisitions and repayment cycle will look at the

debit side of the transaction.

D) due to the infrequency of these transactions, in many cases no transactions involving

notes payable are included in the sample tests of acquisitions and payments.

Which of the following would be considered a violation of the AICPA Code of

Conduct?

A) The CPA makes the audit files available to the client’s bank without the permission

of the client.

B) The CPA firm charges a contingent fee for nonattestation services to a client for

whom he does not perform any attestation services.

C) The CPA firm takes a prospective client to lunch to discuss auditing services.

D) A CPA firm uses the name San Diego Tax Specialists.

When the auditor determines that the financial statements are fairly stated, but there is a

nonindependent relationship between the auditor and the client, the auditor should issue

A) an adverse opinion.

B) a disclaimer of opinion.

C) either a qualified opinion or an adverse opinion.

D) either a qualified opinion or an unqualified opinion with modified wording.

When identifying audit objectives and existing controls,

A) audit objectives are identified for classes of transactions, account balances, and

presentation and disclosure.

B) the auditor identifies controls to satisfy each objective.

C) it is helpful for the auditor to use the five control activities as reminders of controls.

D) all of the above

The document that accompanies the customer’s payment is the

A) credit memo.

B) remittance advice.

C) vendor invoice.

D) monthly statement.

Which of the following is not seen as an advantage to using generalized audit software

(GAS)?

A) Auditors can learn the software in a short period of time.

B) It can be applied to a variety of clients after detailed customization.

C) It can be applied to a variety of clients with minimal adjustments to the software.

D) It greatly accelerates audit testing over manual procedures.

The test of details of balance procedure which requires the auditor to perform tests of

lower of cost or market, selling price, and obsolescence is an attempt to satisfy the

objective of

A) existence.

B) completeness.

C) accuracy.

D) realizable value.

One of the primary approaches in dealing with uncertainties in loss contingencies uses

a(n) ________ threshold.

A) monetary

B) materiality

C) probability

D) analytical

The statement that “We are not aware of any material modifications that should be

made to the accompanying financial statements” expresses which of the following?

A) disclaimer of an opinion

B) negative assurance

C) negative confirmation

D) shared opinion

There is a direct relationship between the ________ transaction-related audit objective

and the ________ balance-related audit objective.

A) occurrence; existence

B) timing; cutoff

C) posting and summarization; detail tie-in

D) all of the above

When the computed upper exception rate (CUER) is greater than the tolerable

exception rate (TER), it is necessary for the auditor to take specific action. Which of the

following courses of action would be most difficult to justify?

A) Reduce the tolerable exception rate so as to accept the sample results.

B) Expand the sample size and perform more tests.

C) Revise the assessed control risk upward.

D) Write a letter to management which outlines the control deficiencies.

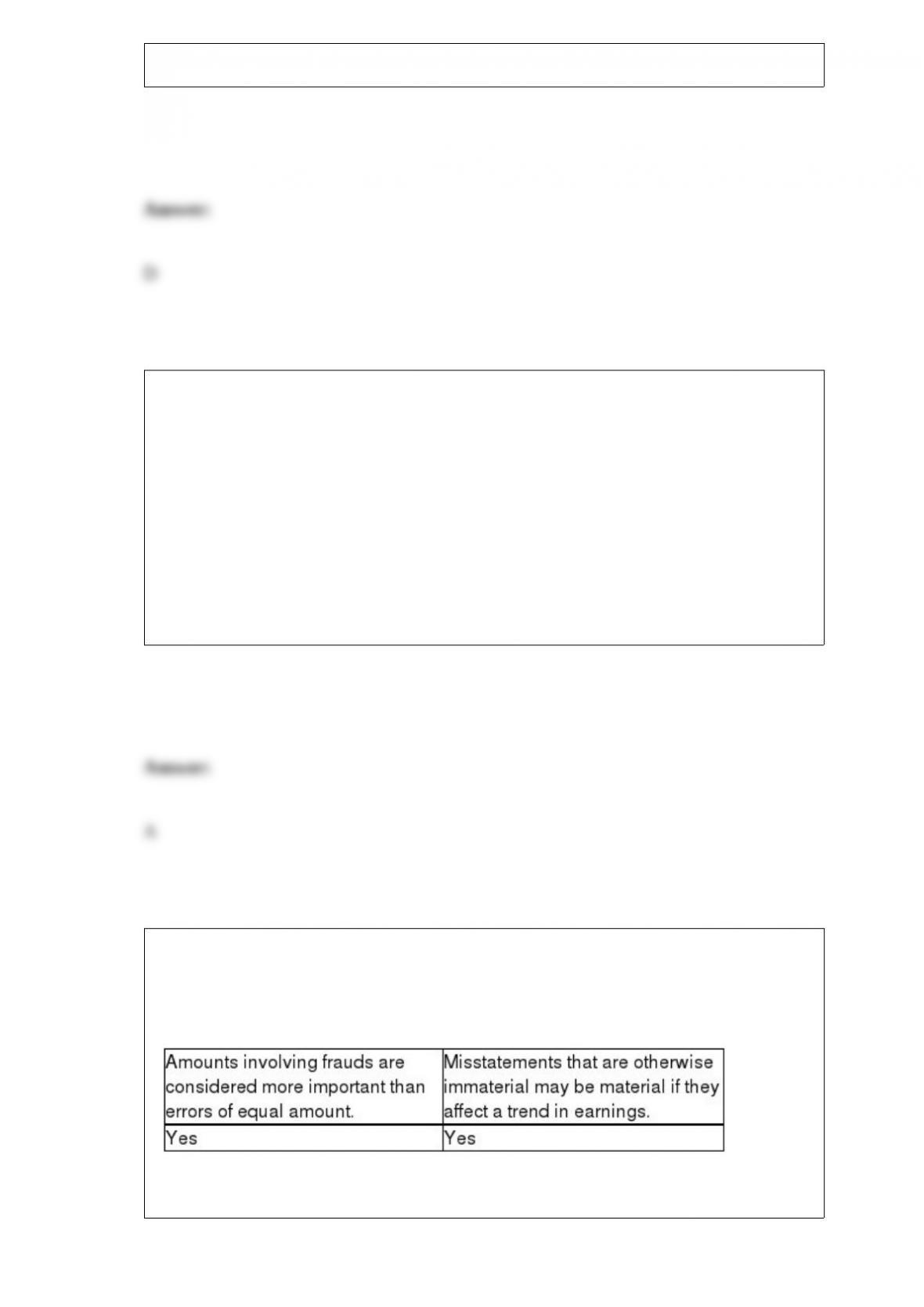

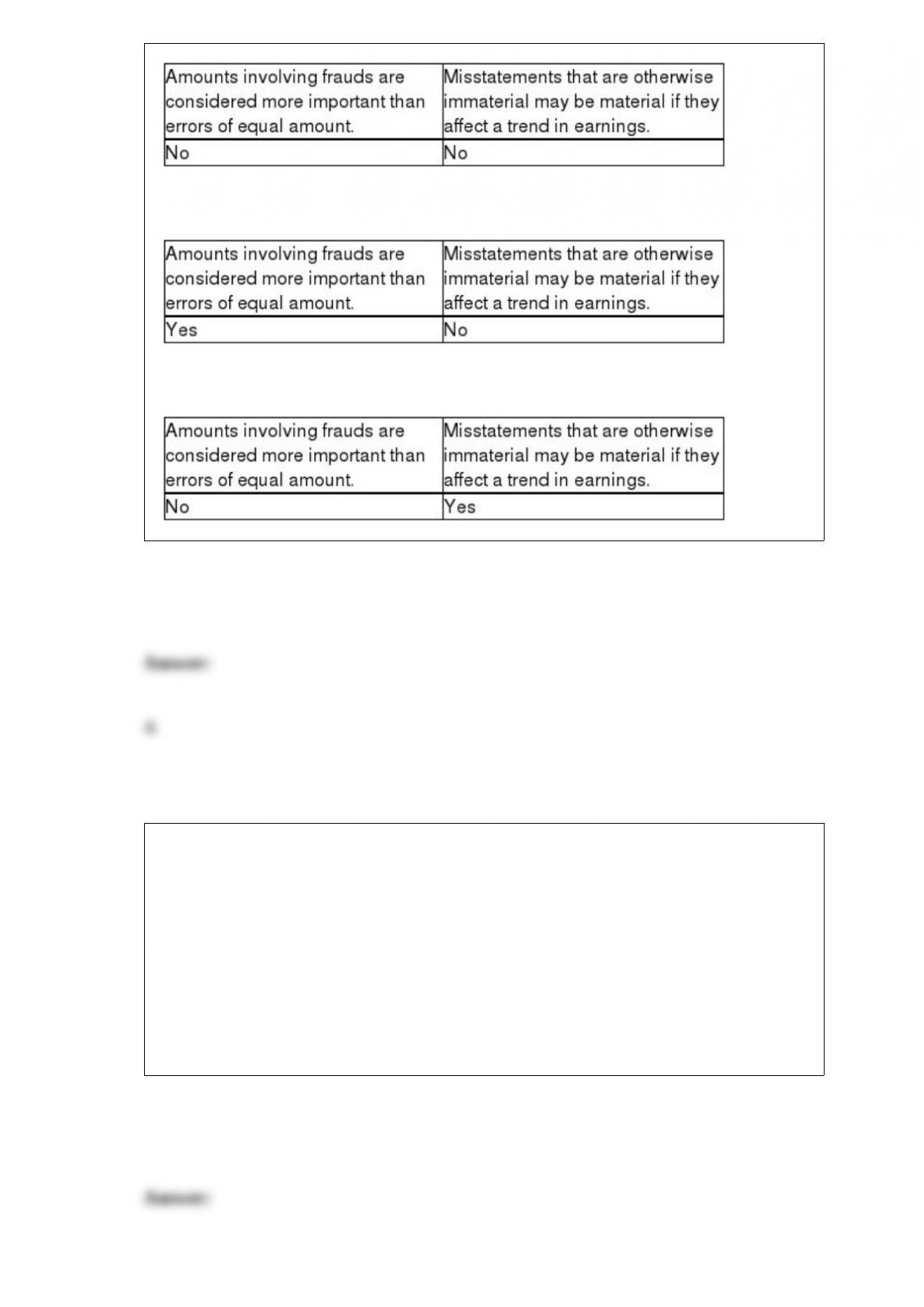

Certain types of misstatements are likely to be more important than other types to users,

even if the dollar amounts are the same. Which of the following demonstrates this?

A)

B)

C)

D)

When a company’s financial statements contain a departure from GAAP with which the

auditor concurs, the departure should be explained in

A) the scope paragraph.

B) an introductory paragraph.

C) the opinion paragraph.

D) a separate paragraph.

Which of the following most likely would be detected by a review of a client’s sales

cutoff?

A) excessive sales discounts

B) unrecorded sales for the year

C) unauthorized goods returned for credit

D) lapping of year-end accounts receivable

The most effective audit evidence gathered for accounts receivable is the

A) detail tie-in of the records.

B) analysis of the allowance for doubtful accounts.

C) confirmation of accounts receivable.

D) examination of sales invoices.

The overall objective in the audit of accounts payable is to determine whether accounts

payable

A) are fairly stated and properly disclosed.

B) are overstated.

C) are understated.

D) are accurately stated.

An internal control deficiency occurs when computer personnel

A) participate in computer software acquisition decisions.

B) design flowcharts and narratives for computerized systems.

C) originate changes in customer master files.

D) provide physical security over program files.

Auditing standards ________ that the basis used to determine the preliminary judgment

about materiality be documented in the audit files.

A) permit

B) do not allow

C) require

D) strongly encourage

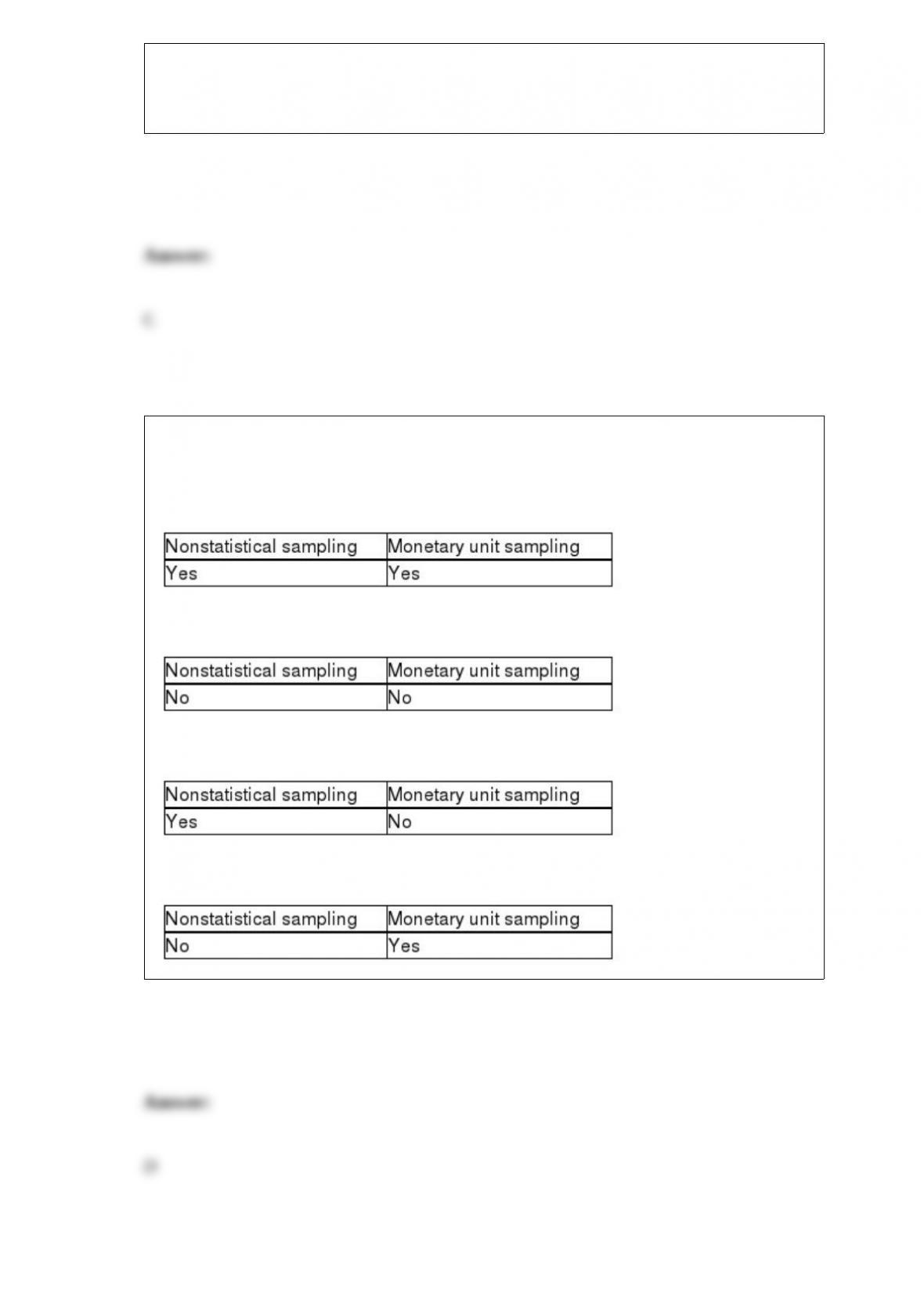

The auditor must consider the possibility that the true population misstatement is

greater than the amount of misstatement that is tolerable when the auditor is performing

A)

B)

C)

D)

A common inventory observation procedure is to select a random sample of tag

numbers and identify the tag with that number attached to the actual inventory item.

The audit objective being achieved by this procedure is

A) inventory as recorded on tags actually exists (existence).

B) existing inventory is counted and tagged (completeness).

C) inventory is counted accurately (accuracy).

D) inventory is classified correctly (classification).

Which of the following can be used as a criteria for evaluating information being

audited?

A) International Financial Reporting Standards (IFRS)

B) Generally Accepted Accounting Principles (GAAP)

C) Internal Revenue Code (IRC)

D) all of the above

In valuing inventory, the auditor must consider all but which of the following factors?

A) The valuation method must be in accordance with GAAP.

B) The valuation method must be applied on a consistent basis.

C) The inventory must be valued at the lower of cost or market.

D) LIFO must be used for work-in-process inventory.

Which of the following is an illustration of liability to clients under common law?

A) A client sues the auditor for not discovering a theft of assets by an employee.

B) A bank sues the auditor for not discovering that the borrower’s financial statements

are misstated.

C) A combined group of stockholders sues the auditor for not discovering materially

misstated financial statements.

D) The federal government prosecutes the auditor for knowingly issuing an incorrect

audit report.

A partial-period bank statement and the related copies of or digital access to cancelled

checks, duplicate deposit slips, and other documents included in bank statements,

mailed by the bank directly to the CPA firm’s office, is called

A) a four-column proof of cash.

B) a year-end bank statement.

C) a cutoff bank statement.

D) a short-period bank statement.

Qualitative factors can affect an auditor’s assessment of materiality. Which of the

following statements is true?

I. Misstatements that are otherwise immaterial may be material if they affect earnings

trends.

II. Misstatements that are otherwise minor may be material if there are possible

consequences arising from contractual obligations.

A) I only

B) II only

C) I and II

D) neither I nor II