4-1

Chapter 4

Professional Ethics

Concept Checks

P. 85

1. The following is the six-step approach to resolving an ethical dilemma:

1. Obtain the relevant facts.

2. Identify the ethical issues from the facts.

each person or group is affected.

dilemma.

5. Identify the likely consequence of each alternative.

6. Decide the appropriate action.

Step 1 involves obtaining the relevant facts. In this case, a colleague has

proposed that each staff person submit a mileage reimbursement request,

alternatives and consequences. If the mileage is requested, the staff person

will receive extra compensation and the firm would overpay for travel

expenses and they would then overbill their client for those expenses.

However, if the firm learns of this action, it could issue punishment up to

consequences.

2. There is a special need for ethical behavior by professionals to maintain

public confidence in the profession, and in the services provided by members

of that profession. The ethical requirements for CPAs are similar to the ethical

professionals, such as attorneys, are expected to be an advocate for their

clients.

4-2

P. 89

1. The Principles of Professional Conduct describe characteristics required of a

the basic requirements of ethical and professional conduct. The six principles

are:

1. Responsibilities

2. The Public Interest

3. Integrity

4. Objectivity and Independence

5. Due Care

6. Scope and Nature of Services

2. The conceptual framework for the Rules of Conduct is designed to assist

members in situations where the interpretations of the rules do not address a

P. 96

1. Independence of mind exists when the auditor is actually able to maintain an

unbiased attitude throughout the audit, whereas independence in appearance

1. Ownership of a financial interest in the audited client.

2. Directorship or officer of an audit client.

3. Performance of management advisory or bookkeeping or accounting

2. All members of the audit committee are required to be independent. Several

audit committee activities help maintain auditor independence. The audit

committee is responsible for the appointment, compensation, and oversight of

4-3

P. 103

requirement are:

1. Obligations related to technical standards

2. Subpoena or summons or compliance with laws and regulations

3. Participation in peer review

4. Response to AICPA Ethics Division

independence; or

(c) an examination of prospective financial information.

The prohibition is necessary to help maintain the objectivity of the CPA in

Review Questions

1. Trustworthiness 4. Fairness

2. Respect 5. Caring

3. Responsibility 6. Citizenship

organizations’ codes of conduct.

4-2 An ethical dilemma is a situation that a person faces in which a decision

must be made about the appropriate behavior. There are many possible ethical

dilemmas that one can face, such as finding a wallet containing money or dealing

4-4

4-2 (continued)

1. Obtain the relevant facts.

2. Identify the ethical issues from the facts.

each person or group is affected.

4. Identify the alternatives available to the person who must resolve

legal liability.

4-4 The three categories of members under the Code of Professional Conduct

are 1) members in public practice; 2) members in business; and 3) other

members.

and due care, confidentiality, and professional behavior.

4-6 Independence in auditing means taking an unbiased viewpoint. Users of

financial statements would be unlikely to rely on the statements if they believed

auditors were biased in issuing audit opinions.

A partner in the office of the partner responsible for an audit

engagement cannot own stock in that audit client. A partner can own stock in an

participate in the audit engagement.

4-5

4-7 (continued)

office.

Professional staff violation: An audit manager owns stock in a client whose audit

is performed by the office where the audit manager works. The manager is

nonaudit services:

1. Bookkeeping and other accounting services

2. Financial information systems design and implementation

3. Appraisal or valuation services

4. Actuarial services

5. Internal audit outsourcing

Nonaudit services that are not prohibited by the Sarbanes–Oxley Act and

the SEC rules must be preapproved by the company’s audit committee. In

Companies are required to disclose in their proxy statement or annual

filings with the SEC the total amount of audit and nonaudit fees paid to the audit

4-9 Ways to reduce the appearance of the lack of independence are: the use

of an audit committee to select auditors made up of directors who are not a part

of management; a requirement that all changes of auditors and reasons therefore

be reported to the SEC or other regulatory agency; and approval of the CPA firm

4-6

4-10 A CPA firm has several options when it decides it is not competent to

perform an audit:

1. Withdraw from the engagement.

2. Obtain the expertise through continuing education and self-studies.

3. Hire someone who has the expertise.

4. Work on a consulting basis with another CPA firm.

4-11 A fee based upon the amount of time it takes to complete is not a violation

of the contingent fees rule, which states that professional services for clients

receiving assertion opinions shall not be offered or rendered under an

agreement whereby no fee will be charged unless a specific finding or result is

4-12 Audits should be maintained at a high level of quality even if solicitation,

advertising, and competitive bidding are allowed for several reasons:

1. Professionals do high quality work because it is a characteristic of

2. A reputation of doing high quality work usually pays off in more clients

3. Potential legal liability is also a deterrent to substandard work.

4. The Code of Professional Conduct requires a high quality of

performance.

4-13 Acts that would be considered discreditable to the profession include

conviction of a crime punishable by imprisonment for more than one year, the

willful failure to file any income tax return that the CPA is required to file by law,

or the filing (or aiding in filing) of a false or fraudulent tax return on behalf of the

without permission of the AICPA.

4-14 Prohibiting paying commissions to obtain clients who receive attestation

services is intended to discourage overly aggressive obtaining of clients by

giving “finders’ fees” to banks and others in a position to give business rather

than on the basis of competitive and other qualifications. Prohibiting receiving

commissions for referrals to other CPAs or other providers of services where

attestation services are provided is intended to discourage referrals to others on

the basis of a “sales commission” rather than the competition of those offering

services. Commissions when attestation services are not provided are permitted

to encourage competition for these types of services.

4-7

4-15 A CPA may practice in one of the following forms:

2. A general partnership

3. A general corporation (if permitted by state law)

4-16 Violations of the AICPA Code of Professional Conduct may result in a

remedial or corrective disciplinary action, such as requiring additional continuing

Multiple Choice Questions From CPA Examinations

Multiple Choice Questions From Becker CPA Review

Discussion Questions And Problems

to be enforced.

b. Ethics is important to the conduct of business because it is difficult

to transact with others without confidence that they will conduct

business in an ethical manner.

c. There are several reasons people act unethically, including greed,

not be detected.

e. Some believe that ethics are innate and cannot be taught. Others

believe ethics should not be taught but instilled by parents and

4-8

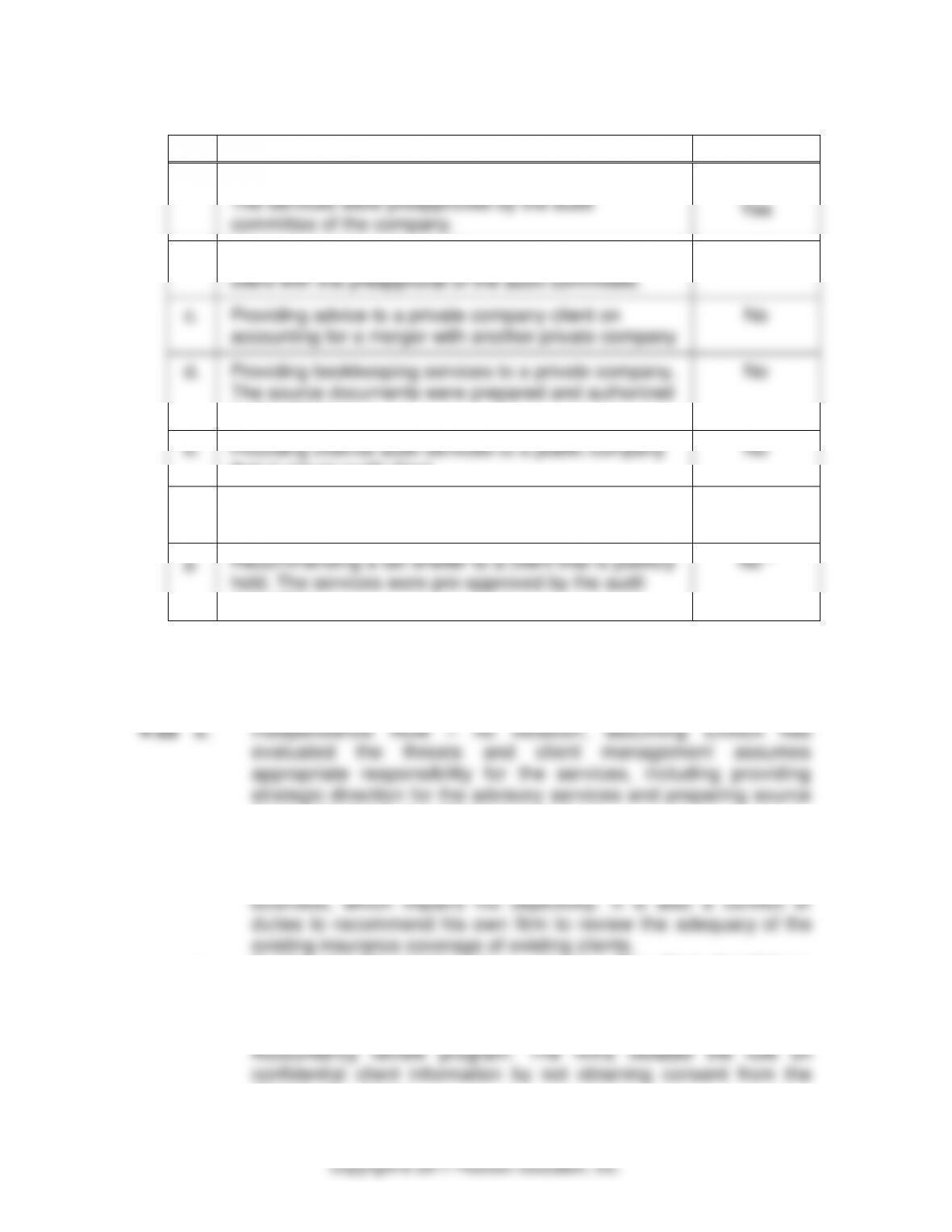

4-21

Service

Violation?

a.

Providing bookkeeping services to a public company.

The services were preapproved by the audit

committee of the company.

Yes

b.

Providing internal audit services to a public company

client with the preapproval of the audit committee.

Yes

c.

Providing advice to a private company client on

accounting for a merger with another private company

No

d.

Providing bookkeeping services to a private company.

The source documents were prepared and authorized

by the client.

No

e.

Providing internal audit services to a public company

that is not an audit client.

No

f.

Implementing a financial information system designed

by management for a private company.

No

g.

Recommending a tax shelter to a client that is publicly

held. The services were pre-approved by the audit

committee.

No *

* Recommending tax shelters is not prohibited as long as the service does not

meet the characteristics of an abusive tax avoidance strategy and does not have

the potential to impair independence.

documents for the bookkeeping services.

b. Independence and Integrity and Objectivity – violation. Appearance

of independence has been impaired by Steve Custer’s agency’s

financial dealing with his audit clients and participation in a

c. Confidential Client Information – violation. The client should have

been notified that the review was to take place, and an attempt

made to obtain the client’s permission for such review since the

review was not a part of an AICPA, state CPA society, or Board of

client for the review.

4-9

4-22 (continued)

expertise to review the work of the consultant hired by Wilkenson.

Wilkenson should have suggested that the company hire the

consultant directly.

f. Integrity and Objectivity – violation. This rule states that in tax

International Accounting Standards Board (IASB) is the established

body for issuing international financial accounting standards.

h. Acts Discreditable – no violation. The rule is vague and the

interpretation would be made by the state Board of Accountancy. In

of another network firm would not impair independence as long as

Miller and Yancy have not involvement with the audit engagement.

b. Violation of Independence Rule – Only pre-existing mortgages

provided by a new audit client that is a bank are permissible. No

new mortgage loans are permitted, however.

modified audit procedures to reduce the risk that Stokely has

knowledge of the audit plan, independence would not be impaired.

4-10

4-23 (continued)

date for the 2016 financial statement audit would likely be in 2017,

more than one year would have transpired.

f. No violation of Independence Rule – Because Jessica promptly

notified her office’s managing partner of the offer and because she

g. Violation of Independence Rule – Providing financial information

systems design and implementation services to a publicly traded

CPA does not perform any other services for that client that might

include audit, review, compilation, examinations of prospective

financial information, or certain tax return services.

whether independence is impaired.