9-11

9–30 (continued)

assessment, the auditor should revise the risk assessment and

9–31 a. Several of the recent developments at Highland Bank and Trust may

trigger risks of material misstatement at the financial statement level,

including the following:

The integration of the pending acquisition of the small community

bank into Highland’s operations and financial reporting processes

may trigger the potential for misstatements across a number of

Any challenges associated with the integration of IT systems of

The integrity and competency of personnel from the acquired bank

reporting.

The expansion of online service options for customers could

trigger risks across a number of accounts, given customers use

b. Several of the recent developments at Highland Bank and Trust may

trigger risks of material misstatement at the assertion level, including

the following:

The expansion of online service operations may affect the

9-12

9–31 (continued)

misstatements related to the posting and summarization

transaction–related audit objective may occur.

loan loss reserves.

The expansion into new types of investments subject to fair value

accounting where the bank does not have employees with the

appropriate valuation skills and competencies increases the risks

for investments.

c. Given the significance of these recent events, the risks noted in

answers to part a. and b. would most likely be deemed as significant

risks in the current year’s audit.

a. True. A CPA firm should attempt to use reasonable uniformity from

audit to audit when circumstances are similar. The only reasons

for having a different audit risk in these circumstances are the

b. True. Users who rely heavily upon the financial statements need

more reliable information than those who do not place heavy

reliance on the financial statements. To protect those users, the

are correctly stated.

c. True. The reasoning for c. is essentially the same as for b.

9-13

9–32 (continued)

9–33

audit risk.

by a single person.

management rather than the audit committee.

management positions.

audit risk.

on audit risk.

experience with the client.

8. Increase A change in the method of accounting increases the

method.

9. Increase The unusual transaction increases audit risk.

10. Decrease The resolution of the lawsuit decreases risk related

11. Increase Related party transactions increase audit risk.

effect on audit risk.

13. Increase The potential for improper revenue recognition

14. Increase A planned stock offering increases incentives to

9-14

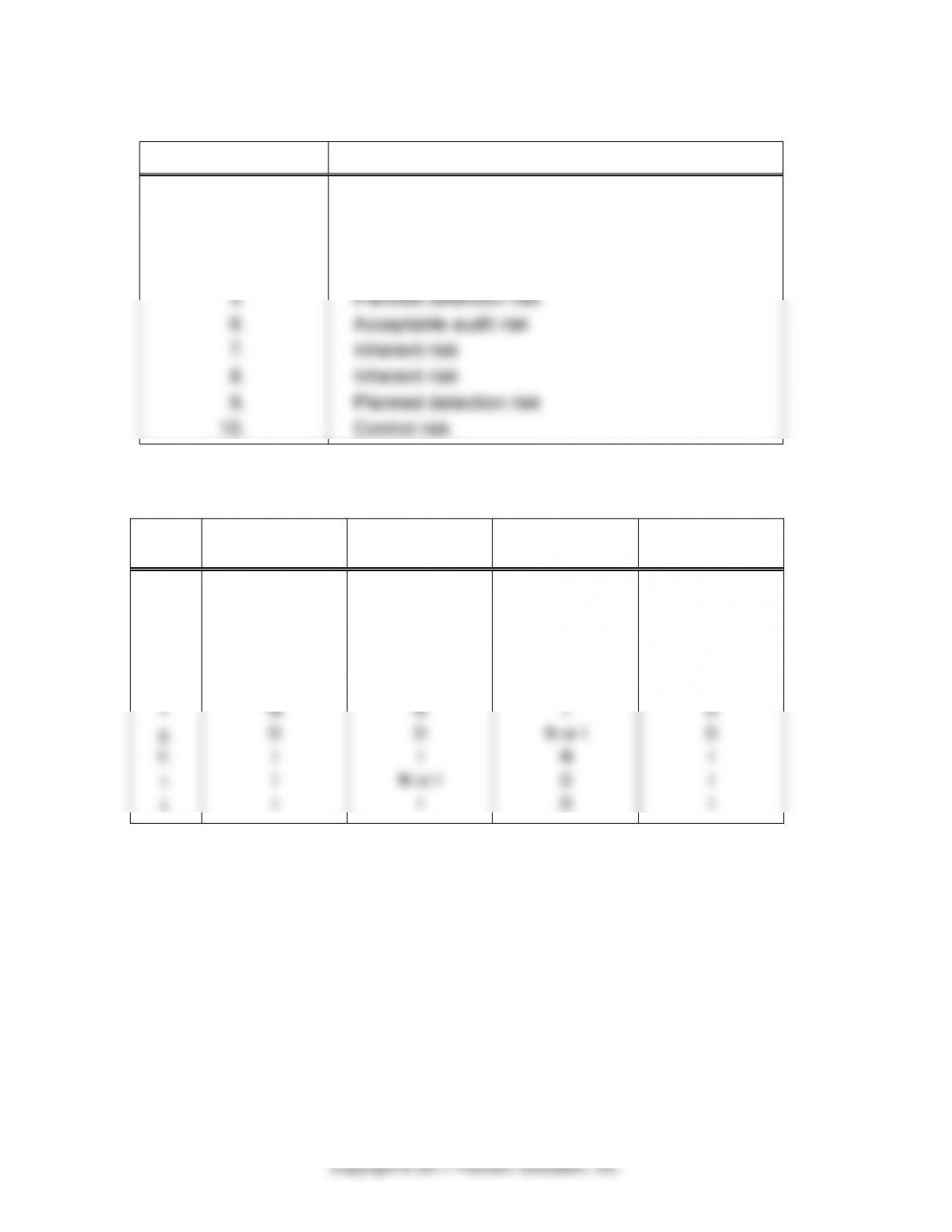

9–34 a. Low, medium, and high for the four risks and planned evidence

have meaning only in comparison to each other. For example,

b. 1 2 3 4 5 6

Acceptable Audit Risk H H L L H M

c.

EFFECT ON PDR

EFFECT ON EVIDENCE

(1) Decrease

(2) Increase

(3) NA

(4) Increase

(5) No effect

Increase

Decrease

Increase

Decrease

No effect

opinion.

Inherent risk A measure of the auditor’s assessment of the

susceptibility of an assertion to material misstatement before

Control risk A measure of the auditor’s assessment of the risk

that a material misstatement could occur in an assertion and not

9-15

9–35 (continued)

Planned detection risk A measure of the risk that audit evidence

exceeding performance materiality, should such misstatements

b.

Risk of Material

Misstatement

Balance–Related

Audit Objectives

Acceptable

Audit Risk

Inherent

Risk

Control

Risk

Planned

Detection

Risk

Existence

Medium

Medium

Medium

Medium

Completeness

Medium

Low

Medium

Medium

Accuracy

Low

High

Medium

Low

Classification

Medium

Low

Low

High

Cutoff

Medium

Medium

Low

Medium

Detail tie–in

Low

Medium

Low

Low /

Medium

Realizable value

Low

High

Medium

Low

Rights and

obligations

Medium

Medium

Low

Medium

d. Hopper may increase his assessment of control risk in the

existence, completeness, and cutoff audit objectives, which

9–36

RISK FACTOR

RELATED AUDIT RISK MODEL COMPONENT

1.

Acceptable audit risk

2.

Control risk

3.

Acceptable audit risk

4.

Inherent risk

5.

Planned detection risk

6.

Acceptable audit risk

7.

Inherent risk

8.

Inherent risk

9.

Planned detection risk

10.

Control risk

9–37

CONTROL

RISK

INHERENT

RISK

ACCEPTABLE

AUDIT RISK

PLANNED

EVIDENCE

a.

b.

c.

d.

e.

f.

g.

h.

i.

j.

N

N

I

I or N

N

N

D

I

I

I

N

N

N

I

I

N

D

I

N or I

I

I

D

N

N

N

I

N or I

N

D

D

D

I

I

I

I

D

D

I

I

I

9-17

Cases

9–38

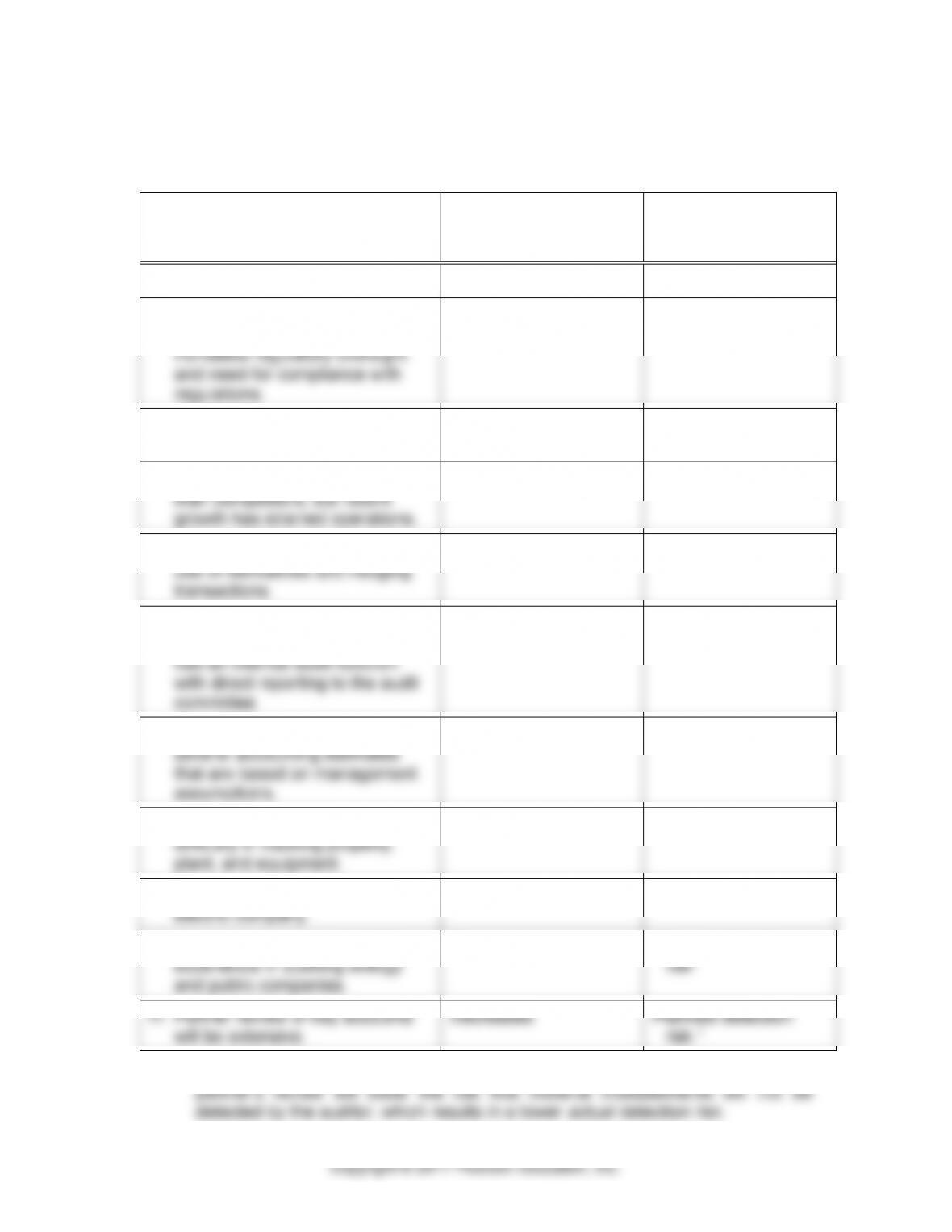

FACTOR

EFFECT ON THE

RISK OF MATERIAL

MISSTATEMENT

AUDIT RISK

MODEL

COMPONENT

1. Henderson is a new client.

Increases

Inherent risk

2. Henderson operates in a

regulated industry, which

increases regulatory oversight

and need for compliance with

regulations.

Increases

Acceptable audit risk

3. The company’s stock is publicly

traded.

Increases

Acceptable audit risk

4. The company is more profitable

than competitors, but recent

growth has strained operations.

Increases

Acceptable audit risk

5. The company has expanded its

use of derivatives and hedging

transactions.

Increases

Inherent risk

6. Henderson has added

competent accounting staff and

has an internal audit function

with direct reporting to the audit

committee.

Decreases

Control risk

7. The financial statements contain

several accounting estimates

that are based on management

assumptions.

Increases

Inherent risk

8. The company has experienced

difficulty in tracking property,

plant, and equipment.

Increases

Control risk

9. Henderson acquired a regional

electric company.

Increases

Inherent risk

10. The audit engagement staff have

experience in auditing energy

and public companies.

Decreases

Planned detection

risk1

11. Partner review of key accounts

will be extensive.

Decreases

Planned detection

risk.1

1 The competency of the audit engagement staff and the thoroughness of the

9-18

9–39 Note: Excel solutions (P939a.xls and P939b.xls) are contained on the

text website.

a. See Worksheet 9–39A on pages 9–22 and 9–23. It is important to

recognize that there is no one solution to this requirement. The

determination of materiality and allocation to the accounts is

always arbitrary. In this illustration, the auditor makes estimated

creates a sensitivity that will need to be watched carefully as the

audit progresses. The allocation to the accounts is particularly

arbitrary. It is noteworthy that the sum of allocated amounts

b. The level of acceptable audit risk is based on an evaluation of

three factors:

1. The degree to which external users rely on the statements.

after the audit report is issued.

3. The auditor’s evaluation of management’s integrity.

Stanton Enterprise is a public company and therefore has a

high degree of reliance by external users on its financial

statements. The Company’s operating results and financial

Overall, then, an acceptable audit risk level of medium

would seem appropriate.

c. See Worksheet 9–39B on pages 9–24 and 9–25 that shows both

9-19

9–39 (continued)

Furthermore, the Company’s current, quick, cash, and times

interest earned ratios are up, and its debt to equity ratio is

down, indicating that the Company is extremely sound from a

liquidity standpoint.

the allowance may be significantly understated for 2016 and

must be looked at very carefully during the current audit. This

review would include considering whether a liberalization of

credit policies was used to help increase sales.

recorded, but may not, depending on dates of acquisition and

depreciation method used. Depreciation must be tested

considering these facts as determined.

Goodwill Goodwill also increased significantly, by $855,000.

Accounts Payable Accounts payable went down from 2015

to 2016. This doesn’t seem reasonable at all given an increase