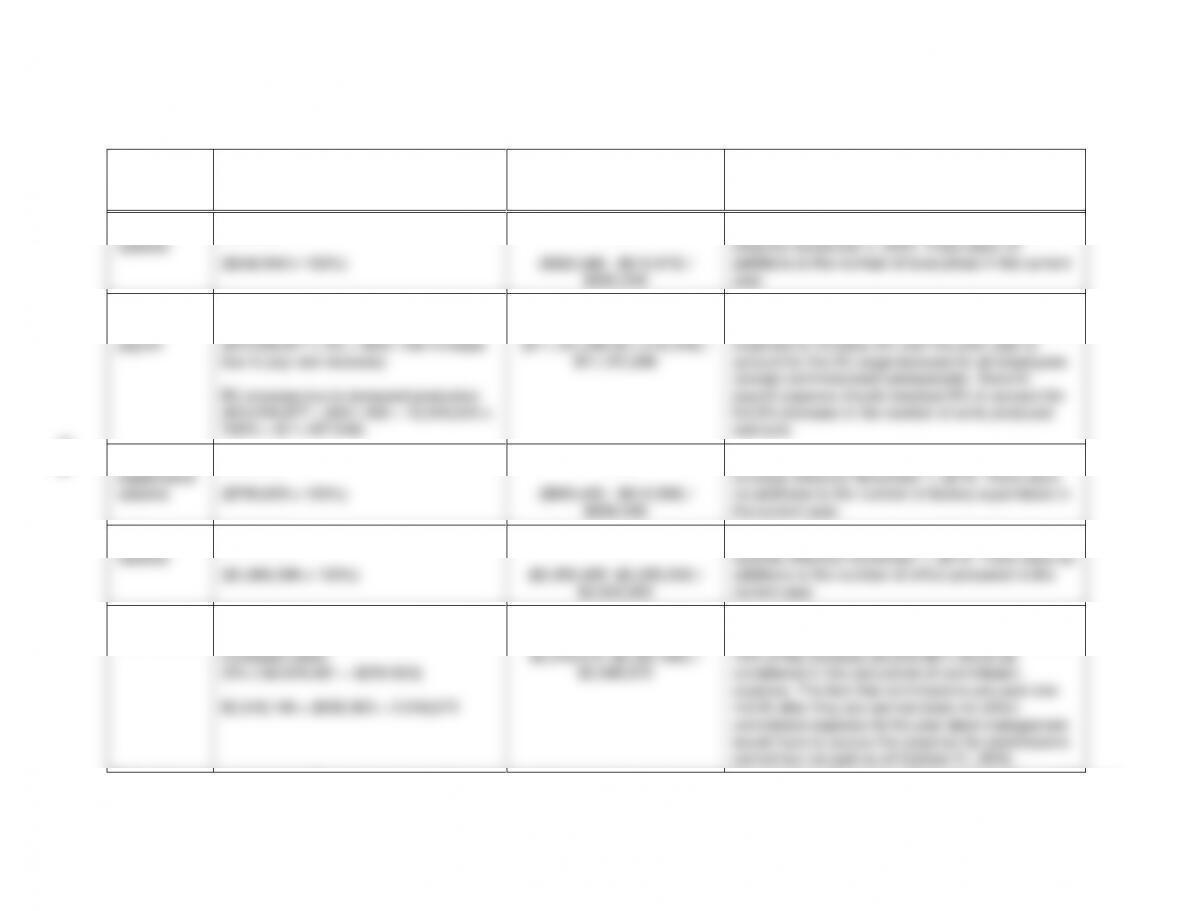

7-35 Here are expected values for each account except sales and the calculated difference between the expected value

and actual recorded balance:

ACCOUNT

EXPECTED VALUE

DIFFERENCE

IN EXPECTED

AND RECORDED

REASONING TO SUPPORT EXPECTED VALUE

Executive

salaries

$563,348

($546,940 x 103%)

–9.34%

($563,348 – $615,970) /

$563,348

All executives received a 3% increase in salaries

effective November 1, 2015. There were no

additions to the number of executives in the current

year.

Factory

hourly

payroll

$11,167,246

Increase due to 3% pay rate increase:

($10,038,877 x 3% = $301,166 increase

due to pay rate increase)

8% increase due to increased production

($10,038,877 + $301,166 = 10,340,043 x

108% = $11,167,246)

–2.77%

($11,167,246-$11,476,319) /

$11,167,246

The increase in factory hourly payroll is attributed to

two primary factors. First, payroll expense would be

expected to increase 3% over the prior year to

account for the 3% wage increase for all employees

(except commissioned salespeople). Second,

payroll expense should increase 8% to account for

the 8% increase in the number of units produced

and sold.

Factory

supervisors’

salaries

$809,400

($785,825 x 103%)

–.15%

($809,400 – $810,588) /

$809,400

All factory supervisors’ salaries received a 3%

increase effective November 1, 2015. There were

no additions to the number of factory supervisors in

the current year.

Office

salaries

$2,050,005

($1,990,296 x 103%)

–.26%

($2,050,005 -$2,055,302) /

$2,050,005

All office personnel received a 3% increase in

salaries effective November 1, 2015. There were no

additions to the number of office personnel in the

current year.

Sales

commissions

$2,249,072

Increase in commissions due to

increased sales:

(5% x $4,618,461 = $230,923)

$2,018,149 + $230,923 = 2,249,072

–5.3%

$2,249,072 -$2,367,962) /

$2,249,072

Sales increased by $6,157,948. Commissions are

only earned on about 75% of the sales. Thus, only

75% of the increase ($4,618,461) would be

considered in the calculation of commission

expense. The fact that commissions are paid one

month after they are earned does not affect

commission expense for the year since management

would have to accrue the expense for commissions

earned but not paid as of October 31, 2016.

(Note: Sales have increased 12% over prior year. Four percent of that is due to an increase in the average selling price. The remaining 8% is attributed to

7-19

7-36 a. PCAOB Auditing Standard 3 indicates that audit documentation

must not be deleted or discarded after the documentation

b. Audit documentation should be sufficient to enable an experienced

auditor, having no previous connection with the audit, to understand

(a) the nature, timing, and extent of the audit procedures performed

c. AU-C 500.A50-52 indicates that the auditor should obtain evidence

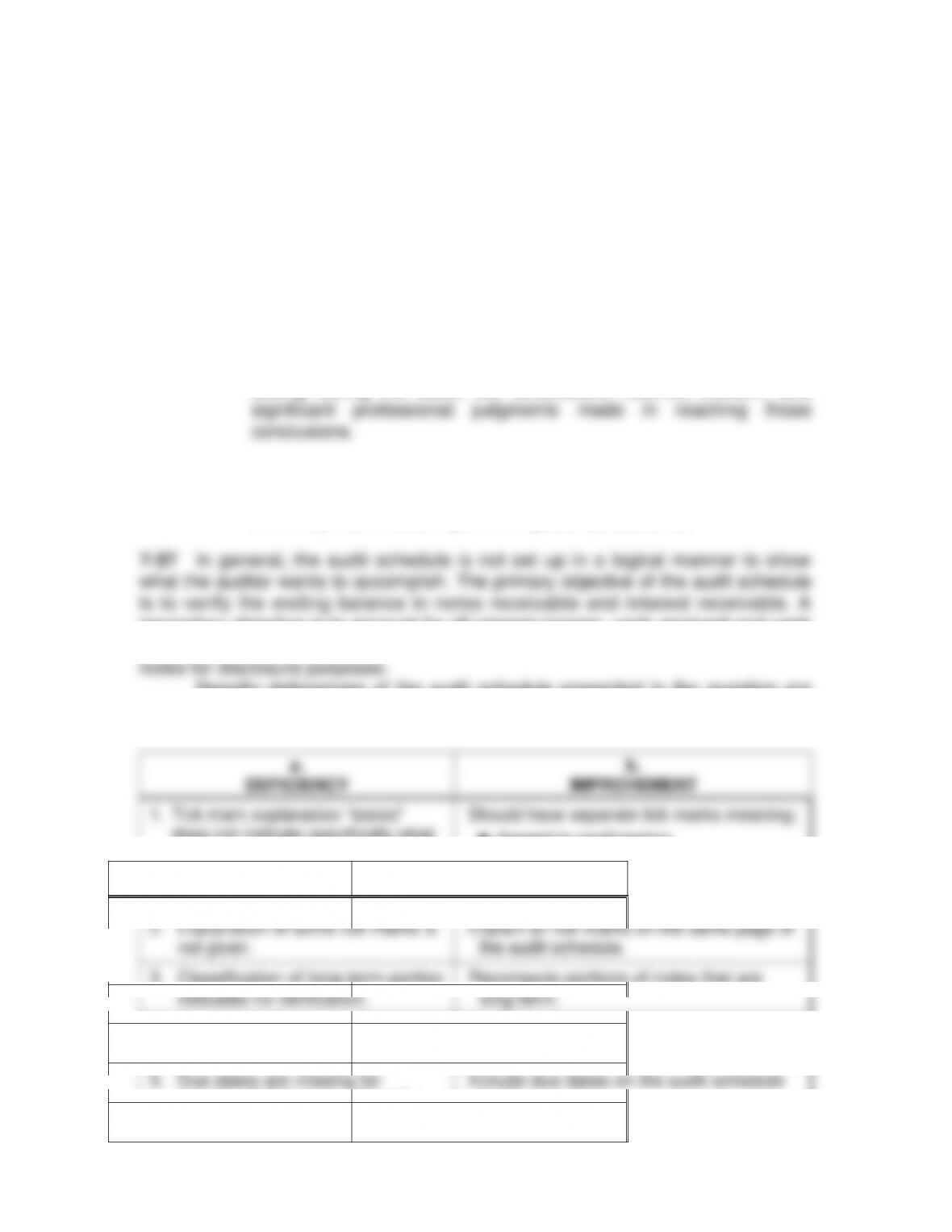

7-37 In general, the audit schedule is not set up in a logical manner to show

what the auditor wants to accomplish. The primary objective of the audit schedule

a.

DEFICIENCY

b.

IMPROVEMENT

1. Tick mark explanation “tested”

does not indicate specifically what

was done.

Should have separate tick marks meaning:

Agreed to confirmation

Footed

Traced to cash receipts journal

Recomputed, etc.

2. Explanation of some tick marks is

not given.

Explain all tick marks on the same page of

the audit schedule.

3. Classification of long-term portion

indicates no verification.

Recompute portions of notes that are

long-term.

4. Paid-to-date row is confusing.

Column should say “date paid to” and this

should be confirmed.

5. Due dates are missing for

J.J. Co., P. Smith, and Tent Co.

Include due dates on the audit schedule

for these notes.

7-21

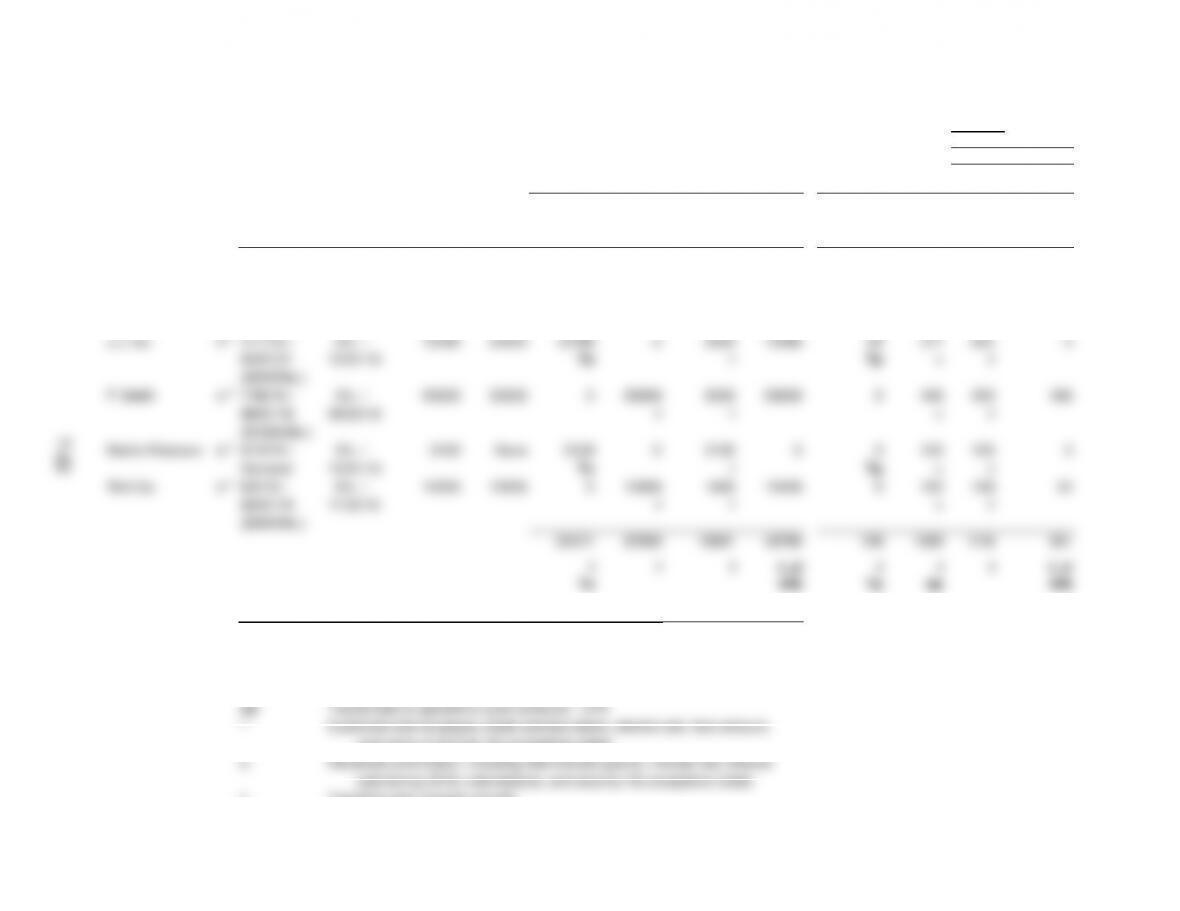

7-37 (continued)

The purpose of using an Excel spreadsheet in this problem is to give

the student some experience in preparing a simple audit schedule

computerized is a matter to be decided. The advantage is that the

completed audit work can then be stored and reviewed electronically.

manually as it is performed.

The following solution was prepared with Excel (Filename

P737.xls). The formulas used are self–evident, so no listing is

deserve comment:

1. An advantage of using a spreadsheet program for these

automatically.

2. When auditor tick marks are done by computer, a problem

arises as to how to place them on the worksheet. One could

7-37 (continued)

VANDERVOORT COMPANY

Schedule

N-1

Date

A/C #110 – NOTES RECEIVABLE

Prepared by

JD

01/21/17

12/31/16

Approved by

PP

02/15/17

Account #110 – Notes Receivable

Interest

Date

Interest

Made/

Rate/Date

Face

Value of

Balance

Balance

Receivable

Receivable

Maker

Due

Paid to

Amount

Security

12/31/15

Additions

Payments

12/31/16

12/31/15

Earned

Recd

12/31/16

Apex Co.

c *

6/15/15 /

5% /

5000

None

4000

0

1000

3000

104

175

0

279

06/15/17

None pd.

Tp

r

Tp

<

Ajax, Inc.

c *

11/21/15 /

5% /

3591

None

3591

0

3591

0

0

102

102

0

Demand

12/31/16

Tp

r

Tp

<

r

J.J. Co.

c *

11/1/15 /

5% /

13180

24000

12780

0

2400

10380

24

577

601

0

04/01/21

12/31/16

Tp

r

Tp

<

r

($200/Mo.)

P. Smith

c *

7/26/16 /

5% /

25000

50000

0

25000

5000

20000

0

468

200

268

08/01/18

09/30/16

r

r

<

r

($1000/Mo.)

Martin-Peterson

c *

5/12/15 /

5% /

2100

None

2100

0

2100

0

0

105

105

0

Demand

12/31/16

Tp

r

Tp

<

r

Tent Co.

c *

9/3/16 /

6% /

12000

10000

0

12000

1600

10400

0

162

108

54

02/01/19

11/30/16

r

r

<

r

($400/Mo.)

22471

37000

15691

43780

128

1589

1116

601

f

f

f

f, cf

f

f

f

f, cf

Tp

wtb

Tp

op

wtb

Legend of Auditor’s Tick Marks

f

Footed

cf

Crossfooted

Tp

Traced to prior year audit files

wtb

Traced total to working trial balance

op

Traced total to operations audit schedule – OP6

*

Examined note for payee, made and due dates, interest rate, face amount,

and value of security. No exceptions noted.

c

Received confirmation, including date interest paid to, interest rate, interest

paid during 2016, note balance, and security. No exceptions noted.

r

Traced to cash receipts records

<

Recomputed for the year

7-22

7-23

Cases

McClure Advertising Credits – An insufficient number of confirmations

(four) were sent. The use of alternative procedures is probably acceptable.

However, one credit was confirmed by telephone, rather than by written

confirmation. Although the differences found were immaterial, the auditors

documentation, which is insufficient to support the credits. The placing of

the validity of the credits.

Ridolfi Credits – The auditor obtained an oral confirmation that these

credits were not valid. The client indicated that the auditor’s information was

incorrect, but would not allow the auditor to obtain written confirmation for

Accounts Payable Accrual – The auditors sent 50 accounts payable

confirmations. Whether this is a sufficient number of confirmations is a

matter of auditor judgment. However, the adequacy of the confirmations

as evidence is significantly undermined by the knowledge that the client

the auditors to agree to a lower amount only if additional testing supported

a lower accrued liability.

7-24

7-39 ACL Problem

screen.)

b. The largest and smallest gross pay amounts are $20.13 and

$14,889.77, respectively. (Use Quick Sort.)

c. Total gross pay was $10,097,295.52 (Use the Total command.)

d. The report below shows gross pay by pay period. (Use the

will contain the same departmental totals.

pay_period

gross_pay

COUNT

4646

389248.69

218

4647

387944.03

220

4648

386699.59

214

4649

389000.55

220

4650

387059.43

218

4651

388215.60

222

4652

388056.95

220

4653

390325.51

225

4654

388645.48

227

4655

388845.66

225

4656

390622.15

228

4657

387892.38

226

4658

389763.65

227

4659

388177.38

226

4660

388229.88

226

4661

388814.15

227

4662

388177.38

226

4663

388289.88

226

4664

388274.88

226

4665

388267.38

226

4666

388184.88

226

4667

387719.88

226

4668

387368.40

221

4669

387306.31

221

4670

389296.25

217

4671

386869.20

217

7-25

7-39 (continued)

Filter: Gross Pay – Deductions < > Net Pay.)

pay_period

employee_number

gross_pay

deductions

net_pay

4646

0000125053

2294.50

573.38

1720.12

4647

0000126112

1103.47

165.49

937.78

4649

0000127262

753.06

112.95

640.05

4649

0000127346

1383.06

345.75

1037.25

4651

0000126713

1139.33

284.82

854.45

4652

0000125653

932.33

139.84

792.43

4653

0000125170

1496.33

374.07

1122.2

4653

0000125703

1509.10

377.25

1131.75

4654

0000127185

903.10

135.45

767.55

4655

0000125399

1130.33

282.57

847.7

4656

0000126030

1060.00

158.85

900.15

4656

0000126038

1572.27

393

1179

4670

0000126962

1151.50

288.38

865.12

4670

0000126976

984.83

147.72

837.05

records.

g. Type of evidence:

Part.

Description

Evidence

a.

Determine number of payroll transactions

Inspection,

Recalculation

b.

Determine largest and smallest payroll

transaction

Inspection,

Recalculation

c.

Determine total gross pay

Recalculation

d.

Determine gross pay by pay period

Recalculation

e.

Recalculate gross pay

Recalculation

f.

Determine if there are any gaps

Inspection