Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

14-21

14-30

POSSIBLE ERROR OR FRAUD

CONTROL

1. Customer checks are properly

credited to customer accounts and

are properly deposited, but errors

are made in recording receipts in

the cash receipts journal.

g. An employee, other than the

bookkeeper, periodically prepares

a bank reconciliation.

2. Customer checks are

misappropriated before being

forwarded to the cashier for deposit.

f. Monthly statements are mailed to

customers with outstanding balances.

3. Customer checks are received for

less than the customers’ full

account balances, but the

customers’ full account balances

are credited.

e. Total amounts posted to the

accounts receivable subsidiary

records from remittance advices

are compared to the validated

deposit slip.

4. Customer checks are credited to

incorrect customer accounts.

f. Monthly statements are mailed to

customers with outstanding balances.

5. Different customer accounts are

each credited for the same cash

receipt.

e. Total amounts posted to the

accounts receivable subsidiary

records from remittance advices are

compared to the validated bank

deposit slip.

14-22

14-31

DEFICIENCY

RECOMMENDED IMPROVEMENT

1. Financial secretary exercises too

much control over collections.

To extent possible, financial secretary’s

responsibilities should be confined to

record keeping.

2. Finance committee is not exercising

its assigned responsibility for

collection.

Finance committee should assume a

more active supervisory role.

3. The finance committee is responsible

for the auditing function and

administration of the cash function.

Moreover, the finance committee has

not performed the auditing functions.

An audit committee should be

appointed to perform periodic auditing

procedures or engage outside

auditors.

4. The head usher has sole access to

cash during the period of the count.

One person should not be left alone

with the cash until the amount has

been recorded or control established

in some other way.

The number of counters should be

increased to at least two, and cash

should remain under joint surveillance

until counted and recorded so that any

discrepancies will be brought to

attention.

5. The collection is vulnerable to robbery

while it is being counted and from the

church safe prior to its deposit in the

bank.

The collection should be deposited in

the bank’s night depository

immediately after the count. Physical

safeguards, such as locking and

bolting the door during the period of

the count, should be instituted.

Vulnerability to robbery will also be

reduced by increasing the number of

counters.

6. The head usher’s count lacks

usefulness from a control standpoint

because he surrenders custody of

both the cash and the record of the

count.

The financial secretary should receive a

copy of the collection report for

posting to the financial records. The

head usher should maintain a copy of

the report for use by the audit

committee.

7. Contributions are not deposited intact.

There is no assurance that amounts

withheld by the financial secretary for

expenditures will be properly

accounted for.

Contributions should be deposited

intact. If it is considered necessary for

the financial secretary to make cash

expenditures, he should be provided

with a petty cash fund. The fund

should be replenished by a check

based upon a properly approved

reimbursement request and

satisfactory support.

14-23

14-31 (continued)

DEFICIENCY

RECOMMENDED IMPROVEMENT

8. Members are asked to enter “cash” on

the payee line, thus making the

checks completely negotiable and

vulnerable to misappropriation.

Members should be asked to make

checks payable to the church. At the

time of the count, ushers should stamp

the church’s restrictive endorsement

(For Deposit Only) on the back of the

check.

9. No mention is made of bonding.

Key employees and members involved

in receiving and disbursing cash should

be bonded.

10. Written instructions for handling cash

collections apparently have not been

prepared.

Especially because much of the work

involved in cash collections is

performed by unpaid, untrained church

members, often on a short-term basis,

detailed written instructions should be

prepared.

11. The envelope system has not been

encouraged. Control features that it

could provide have been ignored.

The envelope system should be

encouraged. Ushers should indicate on

the outside of each envelope the

amount contributed. Envelope

contributions should be reported

separately and supported by the empty

collection envelopes. Prenumbered

envelopes will permit ready identification

of the donor by authorized persons

without general loss of confidentiality.

12. Records of contributions received that

are supplied to members as a tax

record of contributions made.

The church should only provide members

documentation of actual contributions

received versus contributions pledged

for tax purposes.

14-32

INTERNAL CONTROL

a.

STRENGTH OR

DEFICIENCY

b.

TRANSACTION RELATED

AUDIT OBJECTIVE

c.

NATURE OF DEFICIENCY

1. Credit is granted by a

credit department.

Strength

Occurrence of sales.

2. Once shipment occurs

and is recorded in the

sales journal, all

shipping documents are

marked “recorded” by

the accounting staff.

Strength

Completeness of sales.

3. Sales returns are

presented to a sales

department clerk who

prepares a written,

prenumbered receiving

report.

Deficiency

Prenumbered receiving reports should be

prepared by receiving department clerks

immediately upon receipt of returned goods.

A duplicate copy of the receiving report

should be sent to the credit department for

approval and preparation of a credit

memorandum that is then forwarded to

accounting to record the sales return.

4. Cash receipts received

in the mail are received

by a secretary with no

recordkeeping

responsibility.

Strength

Completeness of cash

receipts.

5. Cash receipts received

in the mail are

forwarded unopened

with remittance advices

to accounting.

Deficiency

This represents inadequate segregation of

duties because it gives custody of the cash to

those in accounting who are responsible for

recordkeeping activities. Personnel in

accounting could misappropriate cash

receipts and alter accounting records to hide

the fraud.

14-24

Copyright © 2017 Pearson Education, Inc.

14-32 (continued)

INTERNAL CONTROL

a.

STRENGTH OR

DEFICIENCY

b.

TRANSACTION RELATED

AUDIT OBJECTIVE

c.

NATURE OF DEFICIENCY

6. The cash receipts

journal is prepared by

the treasurer’s

department

Deficiency

The cash receipts journal represents the

primary accounting record for all cash

received. It should be prepared by personnel

within the accounting function, not the

treasury function. The treasury function has

primarily responsibilities surrounding the

any recordkeeping responsibilities.

7. Cash is deposited

weekly.

Deficiency

Cash should be deposited at least daily to

prevent loss or theft of cash.

8. Statements are sent

monthly to customers.

Strength

Occurrence of sales

Accuracy of sales

Posting and

summarization of sales

Completeness of cash

receipts

Accuracy of cash receipts

Posting and summarization of

cash receipts

9. Write-offs of accounts

receivable are

approved by the

controller.

Deficiency

This is an inappropriate segregation of

duties. The controller has recordkeeping

responsibilities. The write-off of accounts

involves authorization responsibilities. The

write-offs should be approved by the credit

department, not the controller.

10. The bank reconciliation

is prepared by

individuals independent

of cash receipts

recordkeeping.

Strength

Occurrence of cash

receipts

Completeness of cash

receipts

Accuracy of cash receipts

14-25

Copyright © 2017 Pearson Education, Inc.

14-26

14-33

CONTROL

TRANSACTION-

RELATED AUDIT

OBJECTIVE

POTENTIAL FINANCIAL STATEMENT

MISSTATEMENT IF CONTROL IS ABSENT

1.

Occurrence

Sales may be recorded for invalid or non-

existent products.

Accuracy

Sales may be processed based on inaccurate

price information.

2.

Occurrence

Sales may be recorded for non-existent

products.

Accuracy

Sales may be processed for existing products

using quantities ordered, even when ordered

quantities are not on hand.

3.

Occurrence

Sales may be processed for customers who are

unable to pay.

4.

Occurrence

Shipments may be made to persons making an

unauthorized credit card purchase (e.g., with a

stolen credit card).

5.

Accuracy

Sales may be processed inaccurately (e.g.,

wrong product, wrong price, wrong quantity).

6.

Occurrence

Sales may be recorded even though shipment

has not occurred.

Timing

Sales may be recorded in the wrong time

period.

14-27

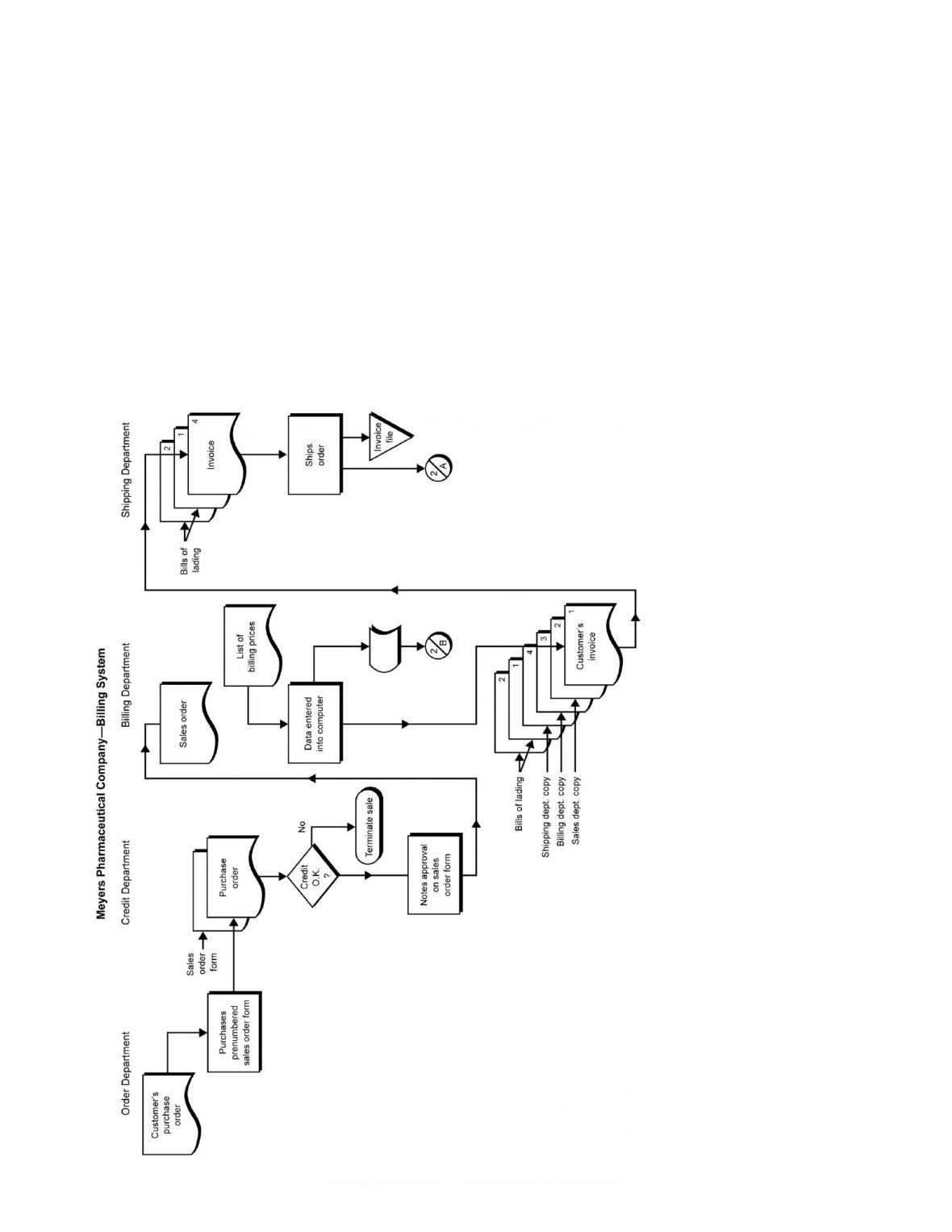

■ Case

14-34 a.

14-28

14-34 (continued)

14-29

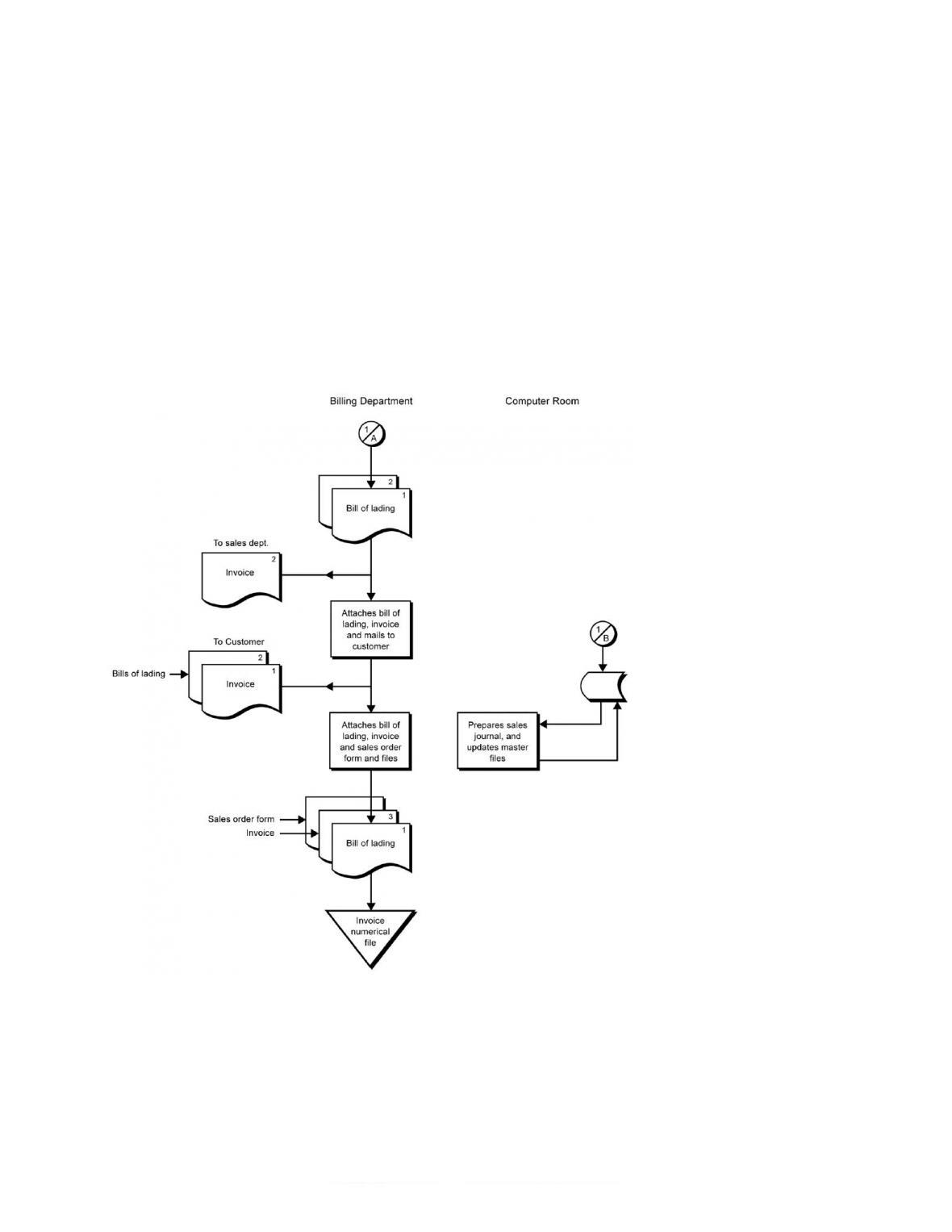

14-34 (continued)

b.

and

c.

TRANSACTION-

RELATED AUDIT

OBJECTIVE

INTERNAL CONTROLS

TEST OF CONTROL

1. Recorded sales

occurred.

Bill of lading and sales order

form are attached to invoice.

Sales are initiated by sales

order form from customer.

Credit department

investigates customer credit

and approves sales before

shipment of merchandise is

authorized.

Examine invoice

package for presence

of bill of lading and

sales order form.

Examine sales order

form for indication

of credit approval.

Review client’s credit

approval system for

effectiveness.

2. Existing sales

transactions are

recorded.

Bill of lading and invoices are

prenumbered (numerical

sequence is not accounted

for) and must be prepared

before merchandise is

shipped.

Account for numerical

sequences of bills

of lading and sales

invoices and

determine that all

have been recorded.

3. Recorded sales are

at the correct

amounts.

Control totals are prepared

and checked by computer.

(No verification of the sales

price is performed.)

Examine computer edit

reports for indication

of errors and

disposition thereof.

4. Sales transactions

are properly included

in the accounts

receivable master file

and are correctly

summarized.

Sales transactions are

simultaneously recorded in

sales, accounts receivable,

cost of sales, and relieved

from the perpetual inventory.

Trace sales

transactions to sales

journal.

5. Recorded sales are

properly classified.

None.

Not applicable.

6. Sales are recorded

on the correct dates.

None.

Not applicable.