Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

16-28

16-36 (continued)

about unintentional errors in billing, recording sales, and cash

receipts. Relatedly, the auditor would most likely deem the risks

errors in accounts receivable and bad debts.

16-36 (continued)

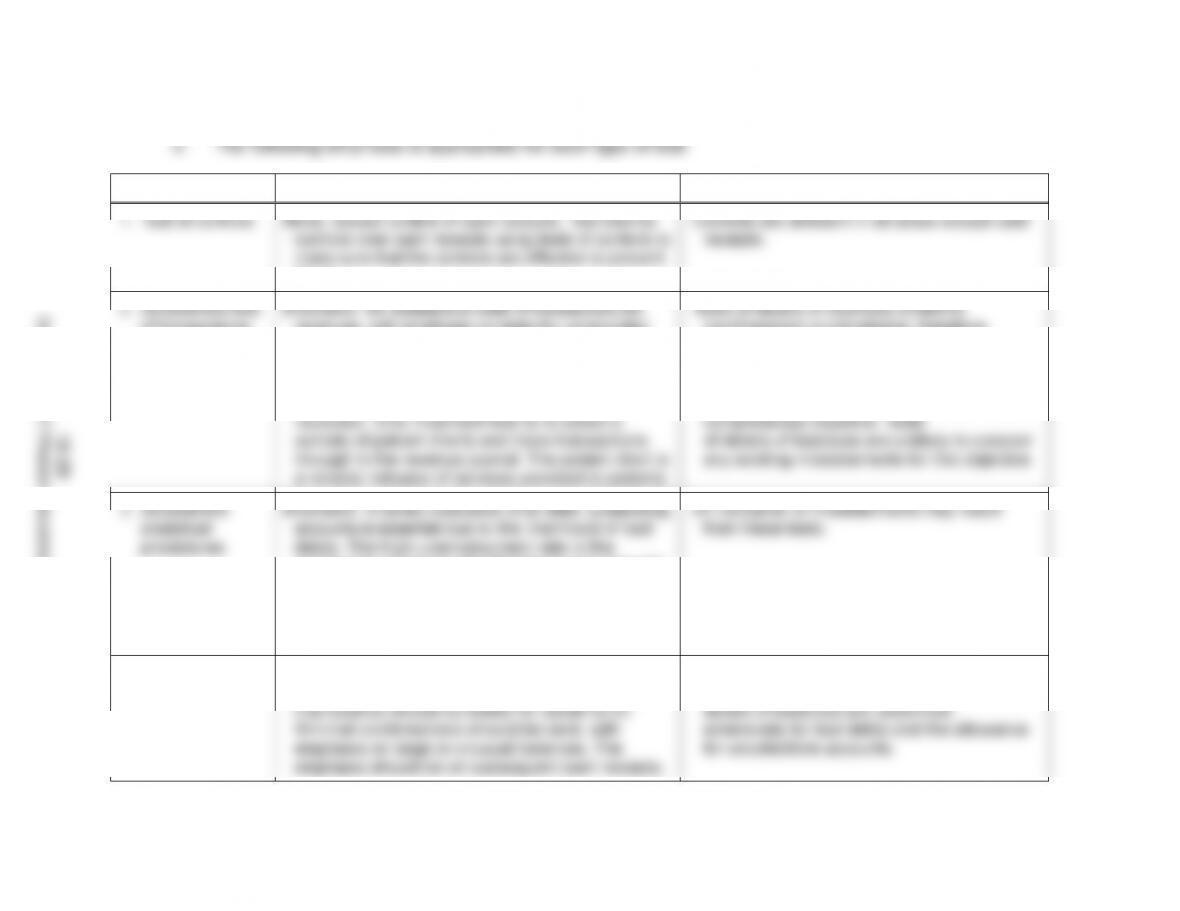

TYPE OF TEST

EMPHASIS

REASON

1. Test of controls

None, except control of cash receipts. Test internal

controls over cash receipts using tests of controls to

make sure that the controls are effective to prevent

fraud.

Controls are deficient in all areas except cash

receipts.

2. Substantive test

of transactions

Extensive. Do substantive tests of transactions for

revenues, with emphasis on tests for unrecorded

revenues, billing misstatements, and recording

misstatements. The sample for sales should be

traced to subsequent cash receipts to test

whether each receipt has been correctly

recorded. One important test is to select a

sample of patient charts and trace transactions

through to the revenue journal. The patient chart is

a reliable indicator of services provided to patients

Tests of details of balances evidence

(confirmation) is not reliable, therefore

substantive tests of transactions are the

most important evidence. Substantive tests

of transactions are even more important

because of potential for misstatement for the

completeness objective. Tests

of details of balances are unlikely to uncover

any existing misstatements for this objective.

3. Substantive

analytical

procedures

Extensive. A careful evaluation of all older, outstanding

accounts is essential due to the likelihood of bad

debts. The high unemployment rate in the

community increases the likelihood of a material

misstatement of the allowance for uncollectible

accounts. A number of substantive analytical

procedures would be performed to analyze trends

related to collectibility.

An indication of misstatements may result

from these tests.

4. Tests of details

of balances

Reasonably extensive, except confirmations which

should be minimal. The accounts receivable aged

trial balance should be tested for detail tie-in.

Minimal confirmations should be sent, with

emphasis on large or unusual balances. The

emphasis should be on subsequent cash receipts.

Confirmations are not emphasized because of

the lack of reliability in the situation. Tests of

details of balances are used most

extensively for bad debts and the allowance

for uncollectible accounts.

16-29

Copyright © 2017 Pearson Education, Inc.

16-30

Integrated Case Application

16-37

PINNACLE MANUFACTURING - PART VII

a. Relationships, ratios, and trends:

1. Comparison of current listing of accounts payable with that

2. Ratios:

Accounts payable / purchases

Gross profit ratio

Overhead / materials cost

unit cost basis

Overhead / direct labor

3. Trends:

Purchases by month

Gross profit by month

Other recurring expenses by month

Ending balance tests

2. Select a sample of 51 vendors and request that they send a

vary.)

3. Trace from the accounts payable list to vendors’ invoices

and statements for any non-responses.

Cutoff tests

physical observation of inventory.

5. Examine subsequent cash disbursements greater than

$50,000 and examine related documentation to

determine if such disbursements were properly recorded

16-31

16-37 (continued)

6. Trace a sample of receiving reports issued just before and

invoice.

7. Examine vendor invoices for merchandise received shortly

origin basis.

Disclosure and classification tests

8. Review the list and master file for related parties, notes or

other interest-bearing liabilities, long-term payables, and

debit balances.

9. Review financial statements to make sure that material

related parties, long-term, and interest-bearing liabilities are

segregated.

c. Audit procedures would be conducted more extensively and

sample sizes would increase in a situation where assessed control

risk and inherent risk were high and analytical procedures

d,

e,

and f. See pages 16-32 and 16-33.

g. Students’ conclusion about whether accounts payable is materially

misstated will depend on their estimate of the allowance for

sampling risk in part e. The projected error in accounts payable

affecting the income statement is an overstatement of $124,915

compared to performance materiality of $250,000. The total

projected error in accounts payable is an understatement of

$171,607. Students should also recognize that some of the

16-37 (continued)

Requirements d., e., and f.

Vendor

Key Accounts

(>$250,000)

Balance

Per

Books

Amount

Confirmed

by Vendor

Difference:

Books

Over

(Under)

Amount

Confirmed

Timing

Difference:

No

Misstatement

Misstatement

in Accounts

Payable

o/s (u/s)

Misstatement in

Related Accounts

Brief

Explanation

Other Balance

Sheet

Misstatement

o/s (u/s)

Income

Stmt mis-

statement

o/s (u/s)

Total

793,050

825,550

(32,500)

--

(32,500)

(32,500)

--

Accounts in Stratum

$50,001 - $250,000

Mobil

93,210

131,022

(37,812)

(37,812)

Timing difference – shipment in

transit

Norris

88,315

205,611

(117,296)

(117,296)

117,296

Unrecorded A/P (Purchases and

A/P)

Remington

123,411

123,411

--

53,529

(53,529)

Pinnacle recorded FOB shipment

before received (Purchases and

A/P)

Advent

51,750

59,250

(7,500)

(7,500)

(7,500)

B/S fixed asset error

Total

356,686

431,137

(162,608)

(37,812)

(71,267)

(7,500)

63,767

Accts in Stratum

less than or equal to

$50000

Fuller

32,470

39,570

(7,100)

(7,100)

Timing difference – payment in

transit

Total

32,470

39,570

(7,100)

(7,100)

--

--

--

16-30

16-32

Copyright © 2017 Pearson Education, Inc.

16-37 (continued)

Estimate of m/s

in the income statement

Misstatements in sample-Stratum

$50,000-$250,000

63,767

Dollars sampled-Stratum

$50,001-$250,000

2,660,879

Dollars in Pop-Stratum

$50,001-$250,000

5,212,467

Income statement m/s -

Point estimate

124,915

(63,767/2,660,879*5,212,467)

Total Estimate

224,915

Estimate of m/s

in accounts payable

Misstatements in key

items

(32,500)

Misstatements in stratum

$50,001-$250,000:

Misstatements in sample

(71,267)

Dollars sampled

2,660,879

Dollars in Pop-Stratum

$50,001-$250,000

5,212,467

Point estimate

(139,607)

(-71,267/2,660,879*5,212,467)

Accounts payable

m/s-Point estimate

(171,607)

Estimate of sampling

error

(150,000)

Highly judgmental

Total Estimate

(321,607)

16-33

Copyright © 2017 Pearson Education, Inc.

16-34

16-38 ACL Problem

b. When using the Summarize command under Analyze to determine

the amount of accounts receivable outstanding from each

customer, the total amount due is $893,619.03, which equals the

amount determined in part a. There are 90 customers with

outstanding from Customer Number 0252620. Customer Number

0249158 has the largest balance due of $28,821.31. (Use the

Summarize Command under Analyze and then use Quick Sort to

arrange the Invoice Amount column in descending order.)

c. The largest balance due is $28,821.31 from Customer Number

column in descending order.)

d. There are 26 invoices that are more than 90 days outstanding,

comprising 27.62% of the total outstanding invoices. The auditor

would use this information to assess the collectibility of accounts

receivable as part of the examination of the realizable value

Age command under Analyze).

Days

Count

Percent of Count

Percent of Field

Invoice Amount

0 - 29

32

35.16%

42.22%

377,291.82

30 - 59

18

19.78%

13.06%

116,703.48

60 - 90

15

16.48%

17.1%

152,771.32

>90

26

28.57%

27.62%

246,852.41

Totals

91

100%

100%

893,619.03