When a successor auditor requests information from a company’s previous auditor, and

there are legal problems or disputes between the client and the predecessor auditor, the

predecessor auditor’s response to the new auditor may be limited to stating that no

information will be provided.

The estimation of bad debts expense relates to the write-off of uncollectible accounts.

Auditors use tick marks, which are symbols adjacent to the detail on the body of the

schedule.

The acquisition and payment cycle consists of one class of transactions.

One disadvantage of functional auditing is the failure to evaluate interrelated functions.

Management has a legal and professional responsibility to be sure that the financial

statements are prepared in accordance with reporting requirements of applicable

accounting frameworks.

Acceptable audit risk and the amount of substantive evidence required are inversely

related.

Statements on Auditing Standards provide detailed, objective guidance on how auditors

are to establish a preliminary materiality level, thus eliminating the need for subjective

auditor judgment in this task.

Depreciation expense results from the allocation of accounting data rather than discrete

transactions.

Cutoff is more important in testing transactions as a client may want to record a gain or

a loss on the sale at the end of the year.

An auditor must be competent and have an independent mental attitude.

An example of a supporting schedule is a reconciliation of amounts, which consists of

the details that make up a year-end balance.

The preliminary judgment on materiality is compared to the total estimated

misstatement amount to determine if an account balance is materially misstated.

If a prospective client has been audited in the past, the successor auditor will typically

rely solely on the representations about the client by the predecessor auditor.

Fraudulent financial reporting is an intentional misstatement or omission of amounts or

disclosures with the intent to deceive users.

Audit evidence to support an opinion about the fairness of a client’s financial statements

consists entirely of written information.

In a CPA firm operating as a limited liability partnership (LLP), the liability for one

partner’s actions does not extend to another partner’s personal assets.

Blank confirmations are considered less reliable than standard positive confirmations.

Under the Securities Act of 1933, a third party plaintiff does not have the burden of

proof that he or she relied on the financial statements or that the auditor was negligent

or fraudulent in doing the audit. Rather, the plaintiff need only prove that the audited

financial statements contained a material misrepresentation or omission.

The overall purpose of the Securities and Exchange Commission is to assist in

providing investors with reliable information upon which to make investment decisions.

When part of the client’s inventory is in a public warehouse or in the possession of other

outside custodians, the auditor does not need to observe a physical count of the

inventory if a written confirmation is obtained directly from the inventory custodians.

When the client’s perpetual inventory master files are inadequate, the auditor will

probably choose to test the physical inventory prior to the balance sheet date.

Internal control over payroll is normally highly structured and well controlled.

If acceptable audit risk is low, and inherent risk and control risk are both low, then

planned detection risk should be high.

Cost is never an adequate justification for omitting a necessary procedure or not

gathering an adequate sample size.

In a CPA firm operating as a limited liability partnership (LLP), the liability for one

partner’s actions extends to the firm’s assets.

The general cash account will not be audited if the ending balance is immaterial.

Auditors are required to communicate either orally or in writing with the audit

committee about internal control weaknesses.

The Sarbanes-Oxley Act provides for criminal penalties.

Objective evidence is more reliable, and hence more persuasive, than subjective

evidence.

In order to mitigate availability, the auditor should consult with others and make the

opposing case.

When the sample exception rate (SER) exceeds the tolerable exception rate (TER), the

auditor should decide whether to increase sample size or to revise assessed control risk

on the basis of cost versus benefit.

MUS has the statistical simplicity of attributes sampling, yet provides a statistical result

expressed as a percentage.

The audit risk model that must be used for planning audit procedures and evaluating

audit results is:

= AAR

Which of the following is a risk factor related to opportunities and financial statement

fraud?

A) ineffective communication of company values

B) promotions inconsistent with expectations

C) significant related-party transactions

D) adverse relationships between management and employees

Which of the following statements is not correct?

A) Materiality is a relative rather than an absolute concept.

B) The most important base used as the criterion for deciding materiality is total assets.

C) Qualitative factors as well as quantitative factors affect materiality.

D) Given equal dollar amounts, frauds are usually considered more important than

errors.

Which of the following assertions is described as “this assertion addresses whether all

transactions that should be included in the financial statements are in fact included”?

A) occurrence

B) completeness

C) rights and obligations

D) existence

Authorizations can be either general or specific. Which of the following is not an

example of a general authorization?

A) automatic reorder points for raw materials inventory

B) a sales manager’s authorization for a sales return

C) credit limits for various classes of customers

D) a sales price list for merchandise

The audit procedure which requires the auditor to record the last check number used on

the last day of the year and subsequently trace to the outstanding checks and the cash

disbursements records is performed to satisfy the audit objective of

A) detail tie-in.

B) existence.

C) completeness.

D) cutoff.

The exception rate the auditor will permit in the population and still be willing to

conclude that the control is operating effectively is the

A) tolerable exception rate.

B) estimated population exception rate.

C) acceptable risk of overreliance.

D) sample exception rate.

A questioning mindset

A) means the auditor must prove every statement that management makes to them.

B) means the auditor should approach the audit with a “do not trust anyone” mental

outlook.

C) assures that the auditor will only accept honest clients.

D) means the auditor should approach the audit with a “trust but verify” mental outlook.

Match seven of the terms for documents and records (a-k) used in the payroll and

personnel cycle with the descriptions provided below (1-7):

a. human resource records

b. deduction authorization form

c. rate authorization form

d. time record

e. job time ticket

f. summary payroll report

g. payroll check

h. W-2 form

i. payroll tax returns

j. payroll journal

k. payroll master file

________ 1. a file used for recording payroll transactions for each employee and

maintaining total employee wages paid for the year to date

________ 2. a document indicating the time the hourly employee started and stopped

working

________ 3. a form indicating which jobs an employee worked on during a given time

period

________ 4. forms submitted to local, state, and federal units of government for the

payment of withheld taxes and the employer’s tax

________ 5. a form authorizing payroll deductions, including the number of

exemptions for withholding of income taxes, retirement savings plans, and union dues

________ 6. a form used to authorize the amount of pay

________ 7. records including date of employment, personnel investigations, rates of

pay, etc.

The first step in verifying the valuation of purchased inventory is in determining the

valuation method used by the client. The next step is

A) determining that all inventory that is purchased is expensed through cost of goods

sold.

B) determining which costs should be included in the valuation of an item of inventory.

C) determining that all inventory on hand reconciles to the perpetual inventory records.

D) determining that cut-off procedures have been adhered to prior to counting

inventory.

Analytical procedures are substantive tests and, if the results of the analytical

procedures are favorable, the auditor would normally

A) reduce the extent of tests of details of balances.

B) reduce the extent of tests of controls.

C) reduce the tests of transactions.

D) reduce all of the other tests.

________ tests are for omitted transactions, while ________ tests are for nonexistent

transactions.

A) Tracing; vouching

B) Vouching; tracing

C) Verifying; tracking

D) Tracking; verifying

Peprah Company pays its accounts payable 45 days after receipt of the goods or

services. In this case, which audit procedure should be used to detect any unrecorded

liabilities?

A) Examine cash disbursements for several weeks after the balance sheet date.

B) Reconcile purchase orders to requisition orders.

C) Reconcile purchase orders to receiving reports.

D) Reconcile purchase orders to vendor invoices.

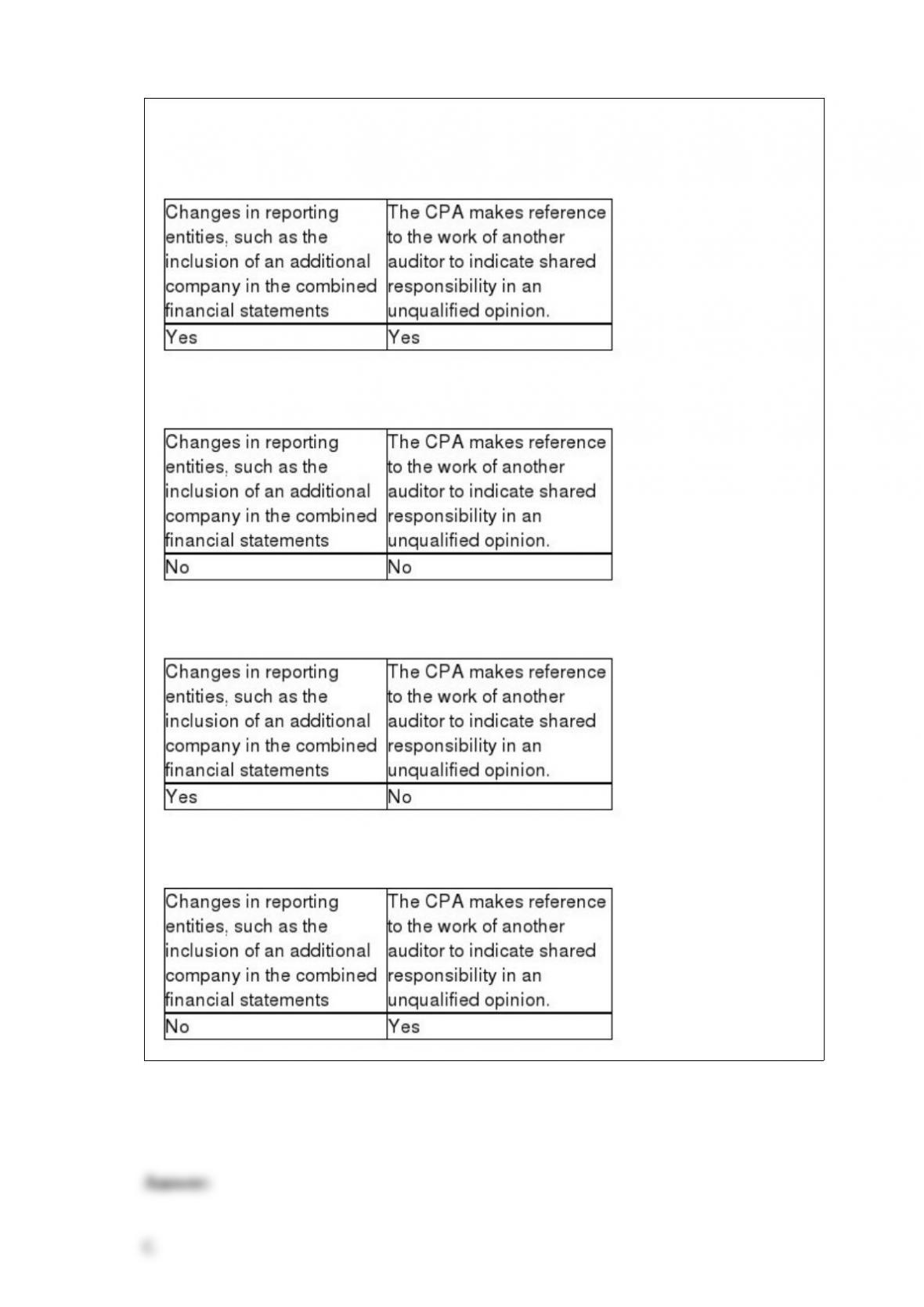

Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

Tort actions against CPAs are more common than breach of contract actions because

A) there are more torts than contracts.

B) the burden of proof is on the auditor rather than on the person suing.

C) the person suing need prove only negligence.

D) the amounts recoverable are normally larger.

Inventory is a complex area to audit for all except which of the following reasons?

A) Inventory is often in different locations.

B) There are several acceptable valuation methods and some entities use different

methods for different types of inventory.

C) Inventory is often the largest account on the balance sheet.

D) Inventory valuation includes few estimates.

Cutoff procedures for inventory purchased should be designed by companies to assure

that

A) inventory owned by the company has been received.

B) inventory included in the year-end inventory count has been paid.

C) inventory received before year-end was recorded before year-end.

D) inventory was correctly valued at year-end.

Which of the following is accurate regarding the comparison of client data?

A) Since budgets are only projections, auditors can ignore the differences between

budgeted and actual results.

B) One approach to overcome the limitations of industry averages is to compare the

client to one or more benchmark firms in the industry.

C) It is impractical to relate one account balance to another balance sheet or income

statement account.

D) it is extremely difficult to get industry data for comparative purposes.

An auditor must obtain written client representations that might be signed by all but

which of the following?

A) treasurer

B) chief financial officer

C) vice president of operations

D) chief executive officer

Constructive fraud

A) is also known as recklessness.

B) requires an intent to deceive.

C) involves collusion with the client.

D) is also known as breach of contract.

Which of the following statements is correct regarding the costs involved in obtaining

evidence?

A)

B)

C)

D)

Of the following statements about internal controls, which one is least likely to be

correct?

A) No one person should be responsible for the custodial responsibility and the

recording responsibility for an asset.

B) Transactions must be properly authorized before such transactions are processed.

C) Because of the cost-benefit relationship, a client may apply controls on a test basis.

D) Control procedures reasonably ensure that collusion among employees cannot occur.

Why does the auditor divide the financial statements into smaller segments?

A) Using the cycle approach makes the audit more manageable.

B) Most accounts have few relationships with others and so it is more efficient to break

the financial statements into smaller pieces.

C) The cycle approach is used because auditing standards require it.

D) All of the above are correct.

Which of the following is a correct statement regarding probabilistic versus

nonprobabilistic sample selection?

A) Auditors may make nonstatistical evaluations when using probabilistic sample

selection.

B) The AICPA recommends probabilistic sample selection.

C) Nonstatistical sampling can’t provide results that are as effective as a statistical

sample.

D) There is only one type of nonprobabilistic sample selection method.

Narratives, flowcharts, and internal control questionnaires are three common methods

of

A) testing the internal controls.

B) documenting the auditor’s understanding of internal controls.

C) designing the audit manual and procedures.

D) documenting the auditor’s understanding of a client’s organizational structure.

When considering internal controls,

A) auditors can ignore controls affecting internal management information.

B) auditors are concerned with the client’s internal controls over the safeguarding of

assets if they affect the financial statements.

C) management is responsible for understanding and testing internal control over

financial reporting.

D) companies must use the COSO framework to establish internal controls.

An auditor is vouching a sample of hourly employees from the payroll master file to

approved time clock or time sheet data in order to provide evidence that

A) employees work the number of hours for which they are paid.

B) payments are made at the contractual rate.

C) product cost information is accurate.

D) segregation of duties is present between the payroll function and the payment

function for cash disbursements.

Tolerable misstatement is used to

A)

B)

C)

D)

Match five of the terms (a-h) with the definitions provided below (1-5):

a. audit documentation

b. audit procedures

c. audit objectives

d. analytical procedures

e. budgets

f. reliability of evidence

g. sufficiency of evidence

h. persuasiveness of evidence

________ 1. use of comparisons and relationships to assess the reasonableness of

account balances

________ 2. detailed instructions for the collection of a type of audit evidence

________ 3. the degree to which evidence can be considered believable or trustworthy

________ 4. contains all the information that the auditor considers necessary to conduct

an adequate audit and to provide support for the audit report

________ 5. this is determined by the amount of evidence obtained

If the auditor decides to assess control risk at the moderate level in a private company

audit, when in previous years the auditor set control risk at the maximum level, then

tests of controls for the current year would be

A) increased in number.

B) reduced in number.

C) not performed.

D) unchanged from prior planned settings.

Audit evidence obtained directly by the auditor will not be reliable if

A) the auditor lacks the competence to evaluate the evidence.

B) it is provided by the client’s attorney.

C) the client denies its veracity.

D) it is impossible for the auditor to obtain additional corroboratory evidence.

A direct financial interest violates independence in which of the following

circumstances?

A) when close relatives such as nondependent children, brothers, and sisters have a

significant financial interest in the client

B) when close relatives such as nondependent children, brothers, and sisters have any

financial interest in the client

C) when the CPA owns shares in a mutual fund that has an ownership interest in the

client

D) when close relatives such as a brother, sister, or in-laws are employed by the client

in their engineering department

In describing the cycle approach to segmenting an audit, which of the following

statements is not true?

A) All general ledger accounts and journals are included at least once.

B) Some journals and general ledger accounts are included in more than one cycle.

C) The “capital acquisition and repayment” cycle is closely related to the “acquisition of

goods and services and payment” cycle.

D) The “inventory and warehousing” cycle may be audited at any time during the

engagement since it is unrelated to the other cycles.

________ is the self-confidence to resist persuasion and to challenge assumptions or

conclusions.

A) Self-esteem

B) Interpersonal understanding

C) Suspension of judgment

D) Autonomy

If an auditor wishes to test the completeness transaction-related audit objective in the

payroll and personnel cycle, which of the following would be a reasonable test of

control?

A) Account for a sequence of payroll checks.

B) Examine the procedures manual and observe the recording of transactions.

C) Examine the payroll records for indication of pay rate approval.

D) Reconcile the payroll bank account.

As the amount of misstatements expected in the population approaches tolerable

misstatement, the planned sample size will

A) decrease.

B) increase.

C) vary based on characteristics of the population.

D) be unaffected.

Customer billing is a critical process which auditors must understand. What are the

most important aspects of billing and what are the related objectives?

Define the following terms commonly used in audit procedures:

1. examine

2. scan

3. compute

4. foot

5. compare

6. count

7. vouch

You are determining the appropriate sample size to test accounts receivable. What three

factors are the most important to consider?

When an auditor uses negative confirmations, several factors must be considered. What

are those factors?

What are the three required conditions for a contingent liability to exist?

Listed below are several accounts listed from a company’s trial balance. Next to each

account put the letter corresponding to the transaction cycle used to audit the account.

S = Sales and collection cycle

I = Inventory and warehousing cycle

A = Acquisition and payment cycle

C = Capital acquisition and repayment cycle

P = Payroll and personnel cycle

1. ________ Sales returns and allowances

2. ________ Capital stock

3. ________ Buildings

4. ________ Notes payable

5. ________ Salaries and commissions

6. ________ Cost of goods sold

7. ________ Trade accounts receivable

8. ________ Rent

Attorneys in recent years have become reluctant to provide certain information to

auditors because of their own exposure to legal liability for providing incorrect or

confidential information. State the two main reasons that attorneys refuse to provide the

auditors with complete information.

Discuss each of the four business functions that comprise the acquisition and payment

cycle.

There are several factors that affect engagement risk and, therefore, acceptable audit

risk. Discuss three of these factors.

Discuss how materiality affects audit reporting decisions.

Describe each of the four types of sample selection methods commonly associated with

statistical audit sampling.

List at least three misstatements that are designed to be detected by a bank

reconciliation.

Briefly explain each management assertion related to classes of transactions and events

for the period under audit.

There are four conditions that must be met before an auditor can issue a standard

unmodified opinion audit report for the audit of a private company. Please discuss each

of these five conditions.

An important concept in contract law for accountants to understand is the “third-party

beneficiary doctrine.” Explain and give an example.

You are the audit manager for a new audit client. Your staff auditors are unsure of what

constitutes a control deficiency. Discuss the terms control deficiency, design deficiency,

and operating deficiency.

In addition to an opinion on whether the financial statements are in accordance with

GAAP, identify four other reports required by the OMB Circular A-133/2 CFR 200

subpart F.

List the three phases in audit sampling for both statistical and nonstatistical sampling.

In planning the audit, an auditor takes three basic steps in determining the audit

procedures to be performed for any business cycle or class of transactions in order to

gather audit evidence concerning possible misstatement due to error or fraud. List those

three basic steps below.