18–28 (continued)

a.

BERGERON

INTERNAL CONTROLS

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

c.

TEST OF CONTROLS

11. Controller reconciles

on a monthly basis the

accounts payable listing

to the accounts payable

general ledger account.

Controller initials

reconciliation upon

completion.

Posting and

summarization

Examine a sample of monthly

reconciliations to determine

they are initialed and

prepared properly.

12. Independent inventory

counts are obtained

quarterly and reconciled

to the perpetual inventory

records.

Occurrence,

Completeness,

Accuracy

Observe client inventory

count teams during one of

the quarterly inventory

counts to determine

whether they are following

the client’s inventory

counting procedures.

18–29 a. It is an appropriate procedure to have the client perform the

reconciliations of vendors’ statements as long as the auditor maintains

amount of time.

For Statement 2, the auditor should request that the vendor

provide additional details of the account balance. Otherwise, the

auditor will not be able to use the vendor’s statement and will have

to include the $5,735.69 as a potential misstatement.

June 30, including consideration of inventory.

The Statement 4 reconciliation is incorrect. The payment by

Milner on July 3 should not have been deducted from the accounts

18-29

18–29 (continued)

inventory at June 30. This may be accomplished by requesting

that the vendor send proof of shipment for the goods invoiced.

c. The auditor must consider whether the coverage achieved by the

suppliers, the auditor may wish to reconcile these statements.

■ Case – Ward Publishing Company

Application of audit sampling is not appropriate for Procedures 1

through 8 due to the nature of the procedures. In this case, audit sampling

is also not appropriate for Procedure 10 because the sampling unit is a

line item in the cash disbursements journal. The sampling data sheet

DESCRIPTION

OF ATTRIBUTE

PLANNED AUDIT

EPER

TER

ARO*

INITIAL

SAMPLE

SIZE**

9.a.

Entry in CD journal agrees with

details on cancelled check.

0%

6%

10%

38

9.b.(1)

All supporting documents attached

to vendor’s invoice.

1%

5%

10%

77

9.b.(2)

Documents agree with

disbursements.

0%

6%

10%

38

18-30

18-30 (continued)

DESCRIPTION

OF ATTRIBUTE

PLANNED AUDIT

EPER

TER

ARO*

INITIAL

SAMPLE

SIZE**

9.b.(3)

Entry in CD journal agrees with

details on vendor’s invoice.

0%

6%

10%

38

9.b.(4)

Discount was taken as appropriate.

0%

6%

10%

38

9.b.(5)

Vendor’s invoice initialed.

1%

5%

10%

77

9.b.(6)

Account coding reasonable.

0%

6%

10%

38

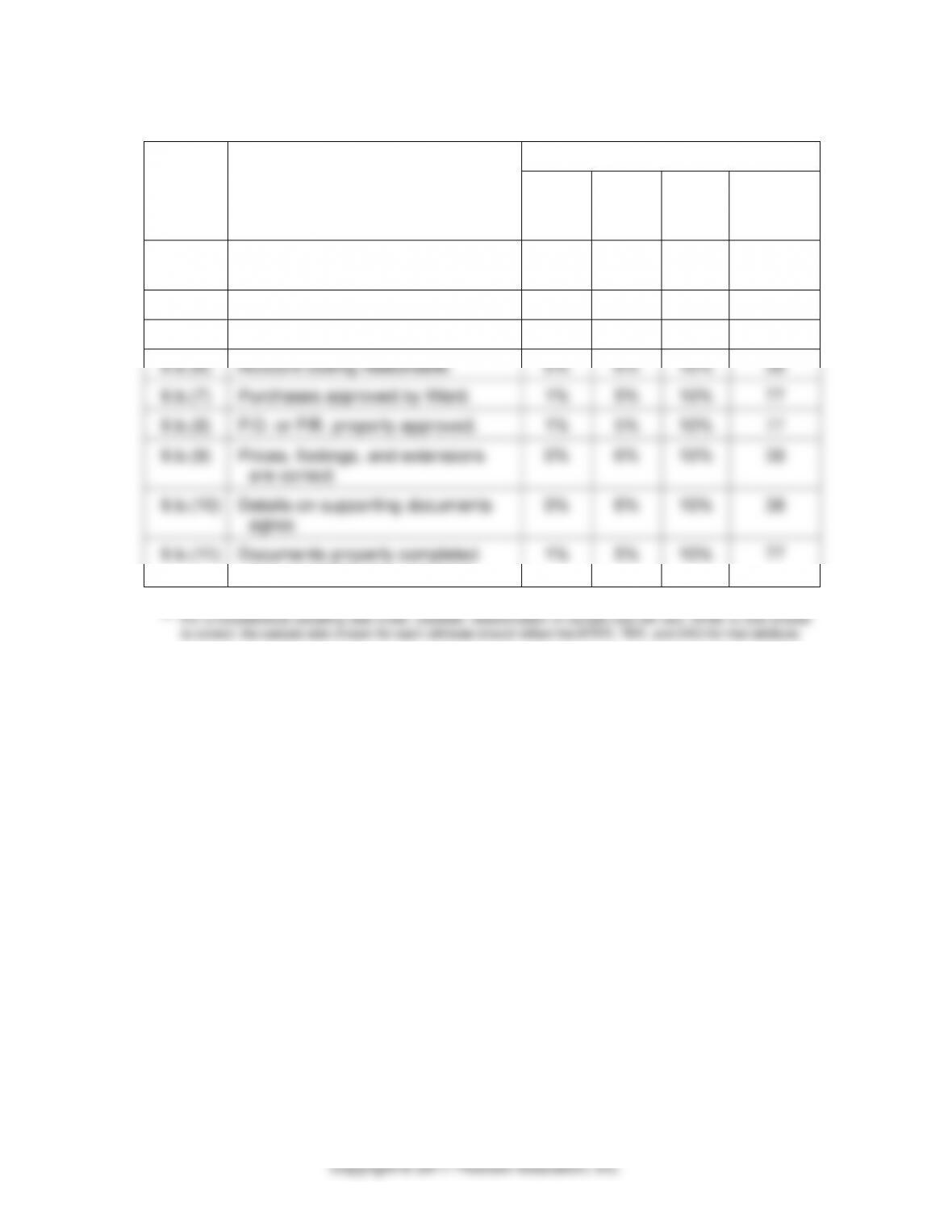

9.b.(7)

Purchases approved by Ward.

1%

5%

10%

77

9.b.(8)

P.O. or P.R. properly approved.

1%

5%

10%

77

9.b.(9)

Prices, footings, and extensions

are correct.

0%

6%

10%

38

9.b.(10)

Details on supporting documents

agree.

0%

6%

10%

38

9.b.(11)

Documents properly completed

and cancelled upon payment.

1%

5%

10%

77

* For a nonstatistical sampling data sheet, ARO columns should indicate “medium” for all attributes.

18–30 (continued)

Part II

a. Attributes sampling approach: The results portion of the sampling

data sheet are as follows:

ATTRIBUTE

NO.

SAMPLE

SIZE

EXCEPTIONS

SAMPLE

EXCEPTION

RATE

CUER

9.a.

9.b. (1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

50

50

50

50

50

50

50

50

50

50

50

50

0

1*

0

0

0

6*

3**

0

0

0

0

0

0

2%

0

0

0

12%

6%

0

0

0

0

0

4.6%

7.6%

4.6%

4.6%

4.6%

20.2%

12.9%

4.6%

4.6%

4.6%

4.6%

4.6%

* Control deviations

** Monetary misstatements

Nonstatistical approach: Because CUER under nonstatistical

sampling is estimated using auditor judgment, students’ answers

to this question will vary. They will most likely be similar to the

CUERs calculated using attributes sampling.

Because the SER is zero for attributes 9.a., 9.b.(2) through (4),

and 9.b.(7) through (11), it is unlikely that students will estimate

CUER greater than the TER of 5% (tests of controls) or 6%

18-32

18–30 Part II (continued)

b. Exception 1 is not an exception, and has no effect on tests of

details of accounts payable.

Exception 2 is a control deviation. Even though it is not a

monetary misstatement, controls require the presence of all

supporting documents before a purchase and the related

disbursement are processed. If an invalid purchase is recorded,

the liability and the related debited account may be overstated. If

Exception 3 is a control deviation where one–half of those

items also contain monetary misstatements. Misclassification is a

serious misstatement. However, it relates to the debit entry, not

c. An audit program for accounts payable is shown on the following

page. The balance–related audit objectives tested by each procedure

are indicated. Because the appropriate acceptable audit risk

18-33

18–30 Part II (continued)

BALANCE–RELATED

AUDIT OBJECTIVES

Detail tie–in

Existence

Completeness

Accuracy

Classification

Cutoff

Obligations

1. Obtain list of accounts payable. Foot the list

and agree to general ledger.

X

2. Trace all items on the list over $10,000 to

vendor’s invoice and supporting documents.

X

X

3. Obtain vendor’s statements for 20 vendors

with greatest volume of purchases, plus

10 others, by confirmation. Reconcile

statements to accounts payable list.

X

X

X

X

4. Examine all subsequent period disbursements

and payments in process of amounts over

$5,000 to determine if they were recorded in

the proper period.

X

X

5. Review the list of accounts payable for proper

classification of accounts due to related

parties, debit balances, or items with unusual

terms.

X

considered necessary for obligations.