13–26

a.

TRANSACTION–RELATED

AUDIT OBJECTIVE

b.

TEST OF

CONTROL PROCEDURE

c.

SUBSTANTIVE

TEST

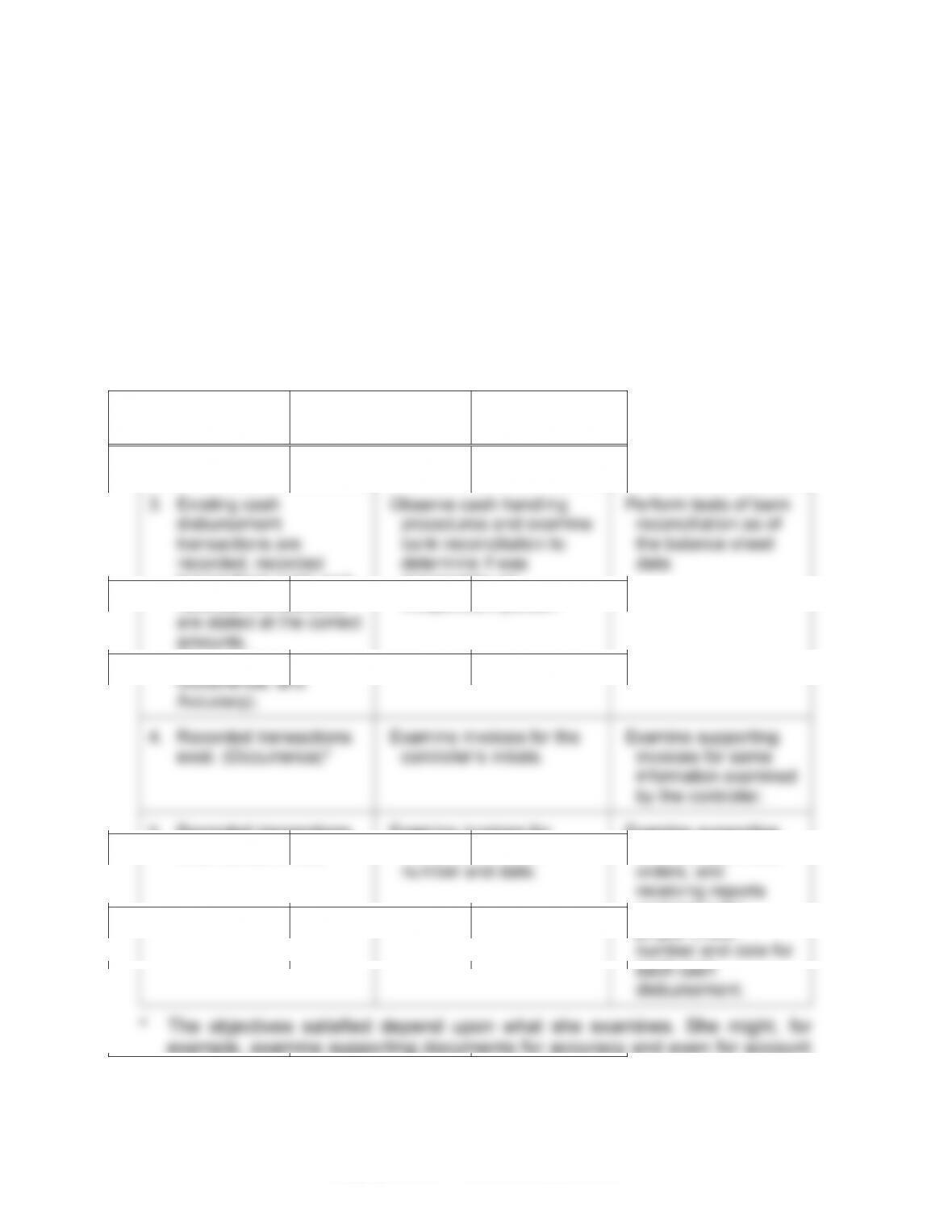

1. Recorded transactions

exist, recorded

transactions are stated

at the correct amounts,

and transactions are

properly classified.

(Occurrence, Accuracy,

and Classification)

Examine invoice

packages for initials

indicating that review

has been performed.

Examine supporting

invoices and

recheck items

checked by the

clerk.

2. Existing acquisition

transactions are

recorded.

(Completeness)

Account for numerical

sequence of receiving

reports and trace to

acquisitions journal entry.

Reconcile vendor

statements to

accounts payable

listing.

3. Existing cash

disbursement

transactions are

recorded, recorded

transactions exist, and

recorded transactions

are stated at the correct

amounts.

(Completeness,

Occurrence, and

Accuracy).

Observe cash handling

procedures and examine

bank reconciliation to

determine if was

prepared by an

independent person.

Perform tests of bank

reconciliation as of

the balance sheet

date.

4. Recorded transactions

exist. (Occurrence)*

Examine invoices for the

controller’s initials.

Examine supporting

invoices for same

information examined

by the controller.

5. Recorded transactions

exist. (Occurrence)

Examine invoices for

indication of check

number and date.

Examine supporting

invoices, purchase

orders, and

receiving reports

containing the

proper check

number and date for

each cash

disbursement.

* The objectives satisfied depend upon what she examines. She might, for

13–27

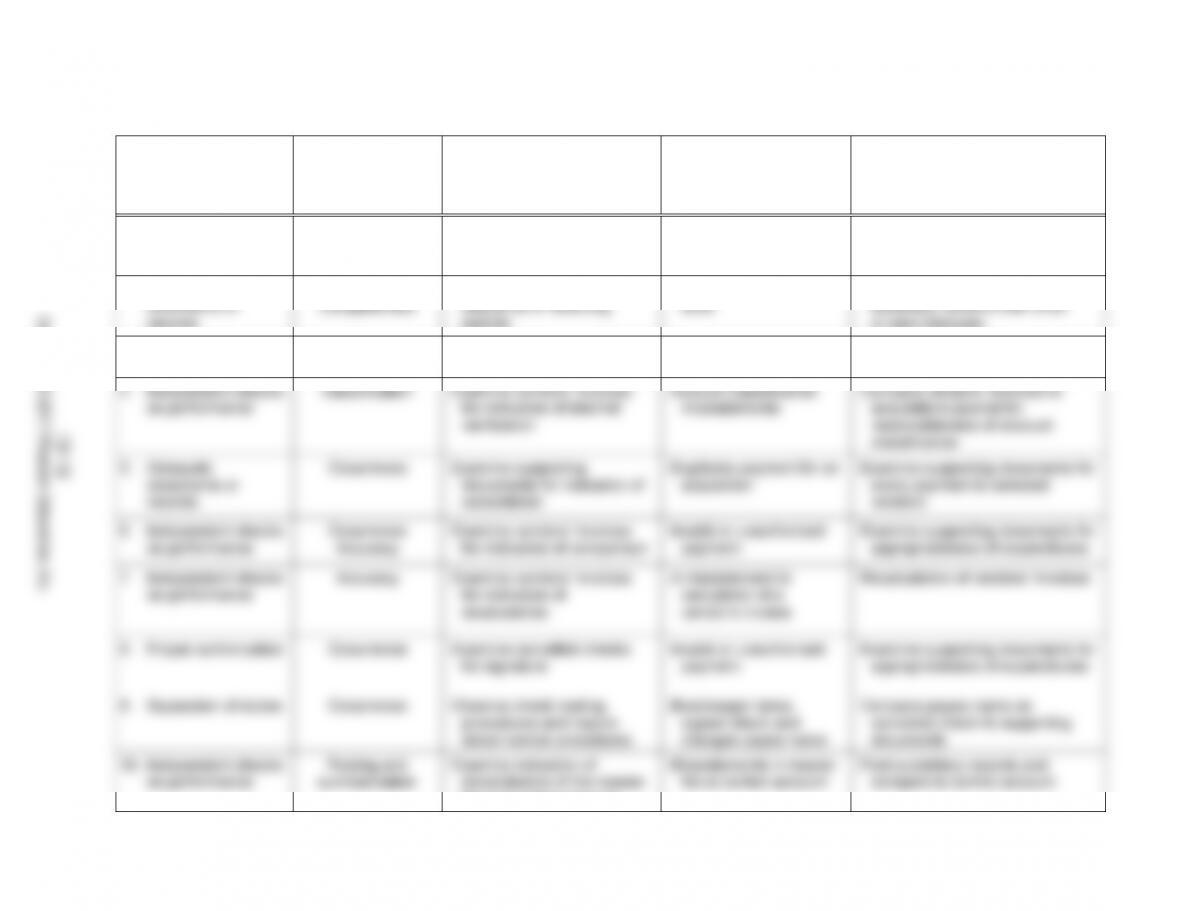

(a)

CONTROL

ACTIVITY

(b)

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

(c)

TEST OF

CONTROL

(d)

POSSIBLE

MISSTATEMENT

(e)

SUBSTANTIVE

AUDIT PROCEDURE

1. Proper authorization

Occurrence

Examine approved purchase

orders for a sample of

acquisitions

Unauthorized

acquisitions of goods

Examine supporting documents for

appropriateness of expenditures

2. Adequate

documents or

records

Occurrence

Completeness

Account for a numerical

sequence of receiving

reports

Unrecorded acquisitions

exist

Confirm accounts payable,

especially vendors with small

or zero balances

3. Independent checks

on performance

Timing

Examine vendors’ invoices

for indication of comparison

Cutoff misstatements

Perform search for unrecorded

liabilities

4. Independent checks

on performance

Classification

Examine vendors’ invoices

for indication of internal

verification

Account classification

misstatements

Compare vendors’ invoices to

acquisitions journal for

reasonableness of account

classification

5. Adequate

documents or

records

Occurrence

Examine supporting

documents for indication of

cancellation

Duplicate payment for an

acquisition

Examine supporting documents for

every payment to selected

vendors

6. Independent checks

on performance

Occurrence

Accuracy

Examine vendors’ invoices

for indication of comparison

Invalid or unauthorized

payment

Examine supporting documents for

appropriateness of expenditures

7. Independent checks

on performance

Accuracy

Examine vendors’ invoices

for indication of

recalculation

A misstatement in

calculation of a

vendor’s invoice

Recalculation of vendors’ invoices

8. Proper authorization

Occurrence

Examine cancelled checks

for signature

Invalid or unauthorized

payment

Examine supporting documents for

appropriateness of expenditures

9. Separation of duties

Occurrence

Observe check mailing

procedures and inquire

about normal procedures

Bookkeeper takes

signed check and

changes payee name

Compare payee name on

cancelled check to supporting

documents

10. Independent checks

on performance

Posting and

summarization

Examine indication of

reconciliation of the master

file and control account

Misstatements in master

file or control account

Foot subsidiary records and

compare to control account

13–12

Copyright © 2017 Pearson Education, Inc.

13–13

Copyright © 2017 Pearson Education, Inc.

13–28 a. Although a client may have very effective internal controls, the

auditor cannot place complete reliance on them in evaluating

whether the financial statements are fairly stated. This reflects the

inherent limitations of internal control, and the need under auditing

standards to perform certain tests of balances such as confirmation

of receivables and observation of inventory.

b. The auditor may decide not to place the maximum reliance on

internal control if it is not cost–beneficial. The auditor may decide

that it is more cost–effective to reduce reliance on controls and

perform more substantive tests.

c. 1. B, C

2. C

3. A

3. Assess control risk.

controls.

4. Perform tests of controls.

2. Perform substantive tests of details of balances.

Any other sequence is not cost effective or is incorrect. For example:

E

F

A B D

G H D

C D

13–14

13–29 (continued)

needed.

c. The sequence is E, B, G, C. The auditor concluded the internal

controls may be effective, but it was not cost effective to reduce

assessed control risk. The auditor should not have performed tests

d. The sequence is F, A, G, C. The logic is not reasonable. When the

auditor concluded the controls were not effective he or she should

have gone immediately to D and performed expanded substantive

tests of details of balances.

performed expanded tests.

13–30

AUDIT

PROCEDURES

TO OBTAIN AN

UNDERSTANDING

OF INTERNAL

CONTROL

TESTS OF

CONTROLS

SUBSTANTIVE

TESTS OF

TRANSACTIONS

ANALYTICAL

PROCEDURES

TESTS OF

DETAILS

OF

BALANCES

1

E

E

S

E

S

2

M

N

S

M

E

3

E

E

M

E

S, E*

E = Extensive amount of testing.

M = Medium amount of testing.

S = Small amount of testing.

N = No testing.

13–15

13–30 (continued)

locations have a larger portion of the ending inventory balance

than other locations, the auditor can likely completely eliminate tests

probably through accounts payable confirmation and other end of

year procedures. No tests of controls are recommended because

of the impracticality of reduced assessed control risk. Some

substantive tests of transactions and substantive analytical

of the balances.

c. The most serious concern in this audit is the evaluation of the

allowance for uncollectible accounts. Given the adverse economic

conditions and significant increase of loans receivable, the auditor

receivable there will be a greatly reduced assessed control risk

and relatively minor confirmation of accounts receivable. In

evaluating the allowance for uncollectible accounts, the auditor

should test the controls over granting loans and following up on

the tests of net realizable value.

13–16

13–31 a. 1. Audit 2

2. Audit 1

3. Audit 3

accounts payable balance include:

1. Materiality of the account balance

2. Size of the populations

3. Makeup of populations

4. Initial vs. repeat engagement

the third audit, the partner apparently has a high expectation of

misstatements, and therefore believes it is necessary to do extensive

of balances.

c. The audit partners could have spent time discussing the audit

13–32 a. Phase I – Procedures 7, 9, 1

Phase II – Procedure 4

Phase III – Procedures 2, 3, 5

Phase IV – Procedures 6, 8

July Audit Report

31 Date

7, 9, 1, 4 2 3 5 6 8