All known related parties must be identified and included in the auditor’s permanent

files related to the client.

Auditing standards require the auditor’s assessment of going concern issues.

When performing substantive analytical procedures for notes payable, if actual interest

expense is materially larger than the auditor’s expectation, one possible cause would be

interest payments on unrecorded notes payable.

Companies with securities traded on national and over-the-counter exchanges are

required to submit audited financial statements once every three years to the Securities

and Exchange Commission.

Operational auditors must accumulate sufficient appropriate evidence to provide a basis

for a conclusion about the objectives being tested.

Auditors typically set performance materiality for accounts payable relatively low.

Preliminary analytical procedures can help the auditor assess client business risk.

On most audits, the calculation for payroll tax expense is costly and is not necessary

unless analytical procedures indicate a problem that cannot be resolved through other

procedures.

Nonprobabilistic sampling methods are not based on mathematical probabilities, and

therefore the representativeness of the sample may be difficult to determine.

Auditors should attempt to minimize ARIA and maximize ARIR.

Upon discovering information that indicates a material misstatement due to fraud, the

auditor must assume that the misstatement is an isolated incident.

The three most important balance-related audit objectives for notes payable are

existence, realizable value, and accuracy.

Because of the lack of independence between related parties, the Sarbanes-Oxley Act

prohibits all related party transactions.

Parallel simulation is used primarily to test internal controls over the client’s IT

systems, whereas the test data approach is used primarily for substantive testing.

For prospective clients that have previously been audited by another CPA firm, the

predecessor auditor must initiate the communication with the successor auditor.

When examining the relationships of the five cycles and general cash, the cycles have

no beginning or end except at the origin or final disposition of the company.

A rationalization method that can easily result in unethical behavior is the argument that

“everybody does it.”

The audit report is normally addressed to the company’s president or chief executive

officer.

The auditor must communicate significant deficiencies in internal control only after the

entire audit is complete to ensure the auditor has a sufficient understanding of the

circumstances surrounding the deficiency.

Tests of controls are generally more costly to perform than analytical procedures.

When a qualified opinion is issued, an explanatory paragraph is added immediately

after the opinion paragraph to explain the nature of the qualification that affects the

opinion.

When the auditor foots the journals and the subsidiary ledgers, it is considered

reperformance.

In the case of a disclaimer due to lack of independence, the entire scope paragraph is

excluded from the report.

The chart of accounts is helpful in preventing classification errors if it accurately

describes which type of transaction should be in each account.

Processing controls are a category of application controls.

A detailed reconciliation of the information on the payroll tax forms and the payroll

records must be prepared as part of the test of controls over the payroll cycle.

Misstatements involving the completeness objective for sales lead to overstatements of

assets and income.

Under the interpretations to the AICPA Code, independence is considered to be

impaired if fees remain unpaid for professional services provided more than six months

before the date of the current year’s report.

Tests of controls are performed to support a reduced assessment of detection risk.

An increased sample size will always cause the population to be accepted.

Independent registrars commonly disburse cash dividends to shareholders.

A 100 % audit risk is complete certainty.

Credit should be approved before a customer’s order is received.

A qualified report can take the form of a qualification of both the scope and the opinion

or of the opinion alone.

Tests of controls should be performed after substantive tests of transactions.

“Physical control over assets” is not a type of control that is applicable to the payroll

cycle.

The auditor’s risk assessment for fraud should be ongoing throughout the audit.

Checks should be prenumbered to make it easier to account for all checks.

To address heightened risks of fraud, the auditor can do all of the following except

A) use specialists to assist in evaluating the accuracy and reasonableness of

management’s key estimates.

B) decrease the amount of substantive tests.

C) use ACL or IDEA to search for fictitious revenue transactions.

D) use EXCEL to perform analytical procedures at the disaggregated level.

For departures from GAAP or scope restrictions, the auditor must decide if the potential

effect on the financial statements is

A) immaterial.

B) material.

C) highly material.

D) any of the above.

When making a preliminary assessment of control risk, the starting point for most

auditors is

A) IT assessment controls.

B) assessment of entity level controls.

C) transaction-related controls.

D) fraud controls.

In testing acquisitions, the auditor must understand the relevant accounting standards to

insure the client adheres to accepted accounting practices for property, plant, and

equipment. Describe three of the auditor’s concerns in this area.

Which of the following is a factor that relates to attitudes or rationalization to

misappropriate assets?

A) significant accounting estimates involving subjective judgments

B) excessive pressure for management to meet debt repayment requirements

C) a sense of superiority by executives

D) high turnover of accounting, internal audit and information technology staff

A system walkthrough is primarily used to help the auditor

A) test the ending account balances.

B) test the details of transactions.

C) determine whether internal controls have been properly implemented.

D) determine whether the audit engagement should be accepted.

An auditor traces the sales prices to the authorized price list in effect at the date of the

transaction. Which of the following procedures has the auditor performed?

A) inquiry

B) observation

C) reperformance

D) examination

The trait that distinguishes auditors from accountants is the

A) auditor’s ability to interpret accounting principles generally accepted in the United

States.

B) auditor’s education beyond the bachelor’s degree.

C) auditor’s ability to interpret FASB Statements.

D) auditor’s expertise in the accumulation and interpretation of audit evidence.

If acceptable audit risk is increased, acceptable risk of incorrect acceptance should be

A) increased.

B) reduced.

C) unaffected.

D) modified.

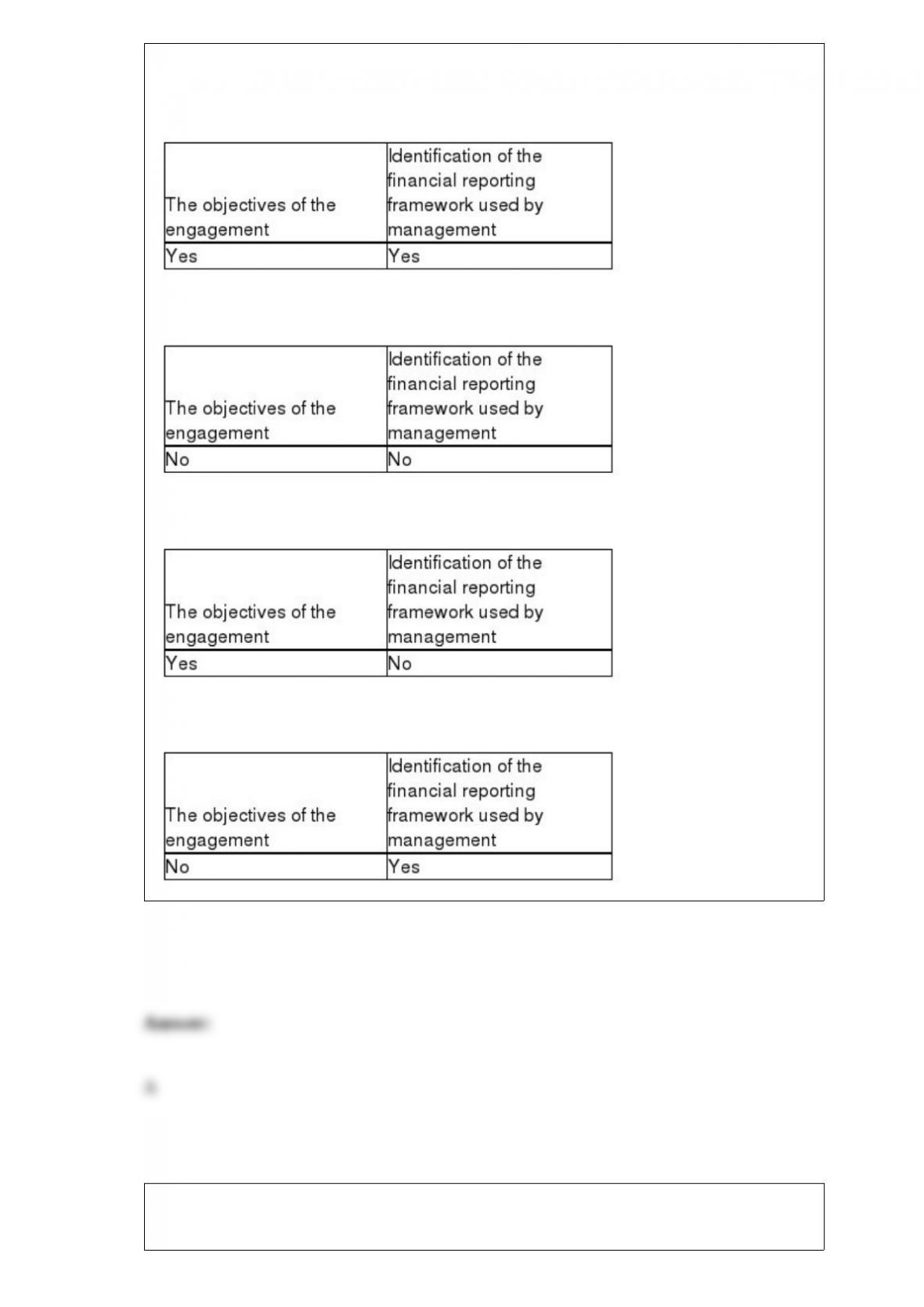

Which is usually included in an engagement letter?

A)

B)

C)

D)

Once the auditor determines that the company’s policy for accruing wages is consistent

with prior years, the appropriate audit procedure to test for accuracy and cutoff is

A) recalculating the client’s accrual.

B) performing extensive tests of controls.

C) performing extensive tests of details.

D) none of the above.

Sampling risk results from the auditor’s failure to recognize exceptions in transaction

data.

One of the bases other than GAAP or IFRS is the Financial reporting framework for

small- and medium-sized businesses. This basis

A) has not yet been approved by the AICPA.

B) is the same as the income tax basis.

C) draws upon a blend of traditional accounting principles and accrual income tax

methods of accounting.

D) must be used by a business with sales under $1 million.

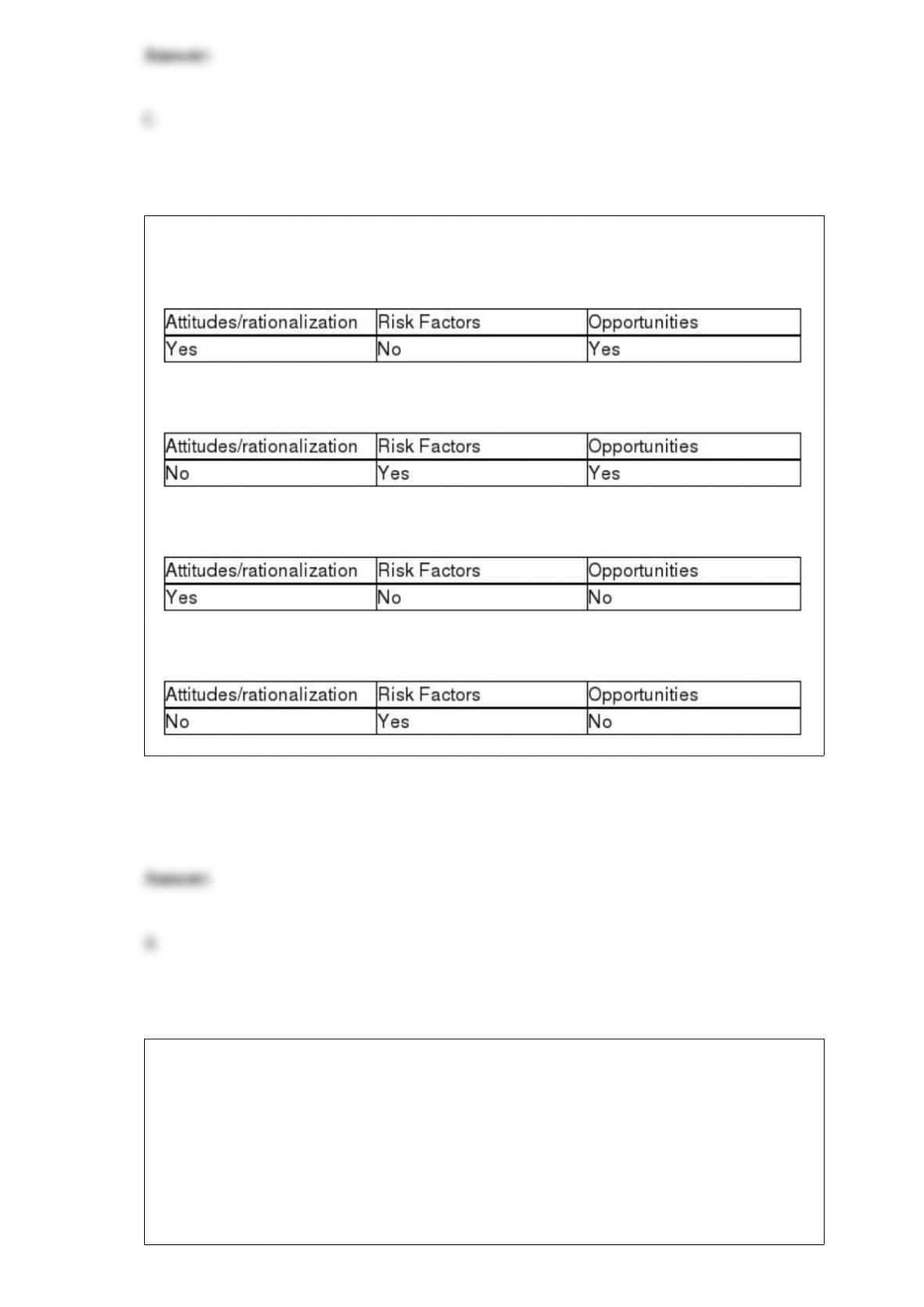

Which of the following are elements of the fraud triangle?

A)

B)

C)

D)

Which of the following groups could be involved in an operational audit?

A) CPA firms

B) internal auditors

C) government auditors

D) All of the above could be involved.

Which of the following is an illustration of liability under the federal securities acts?

A) A client sues the auditor for not discovering a theft of assets by an employee.

B) A bank sues the auditor for not discovering that the borrower’s financial statements

are misstated.

C) A combined group of stockholders sues the auditor for not discovering materially

misstated financial statements.

D) The auditor sues a client for not cooperating during the engagement.

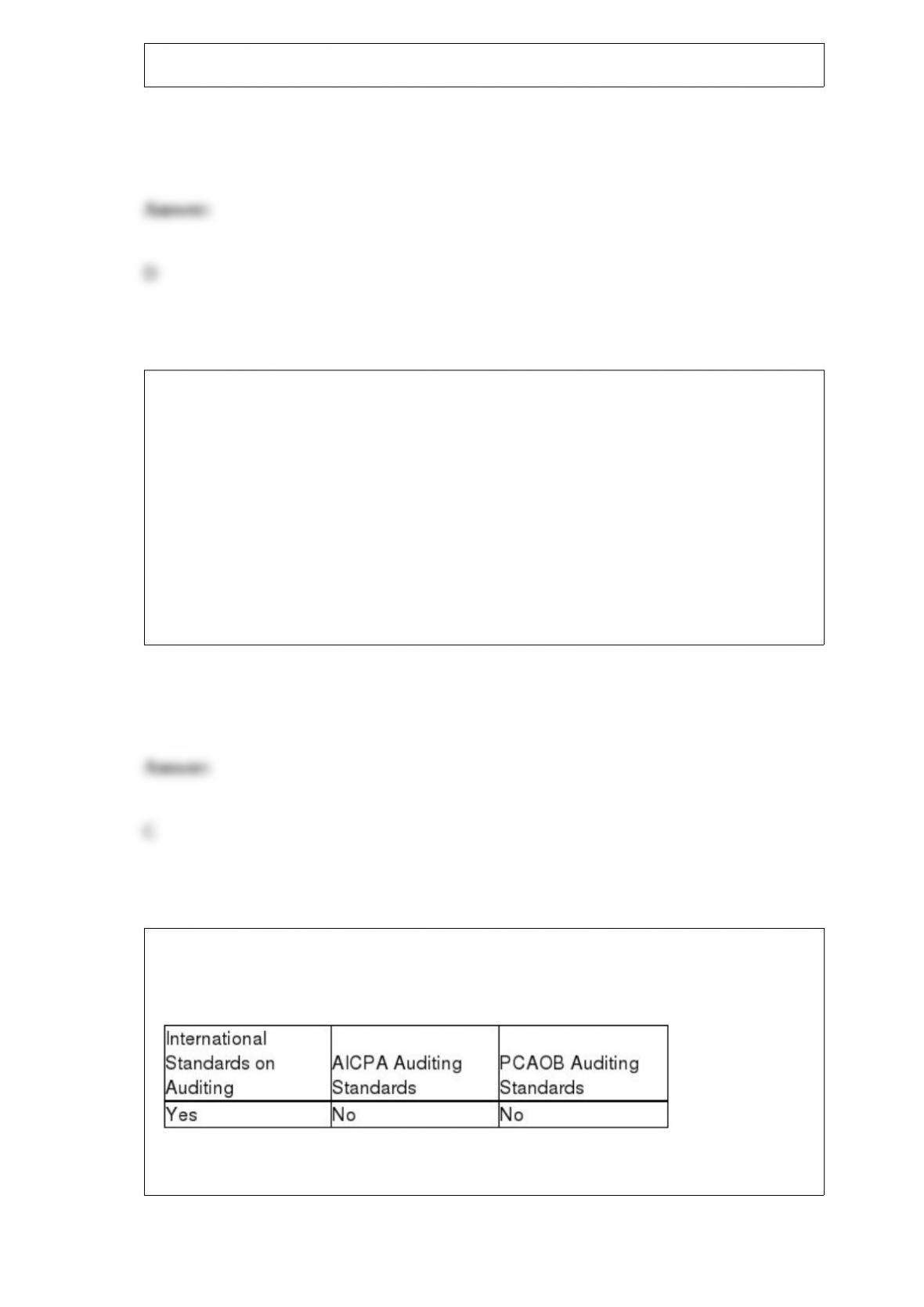

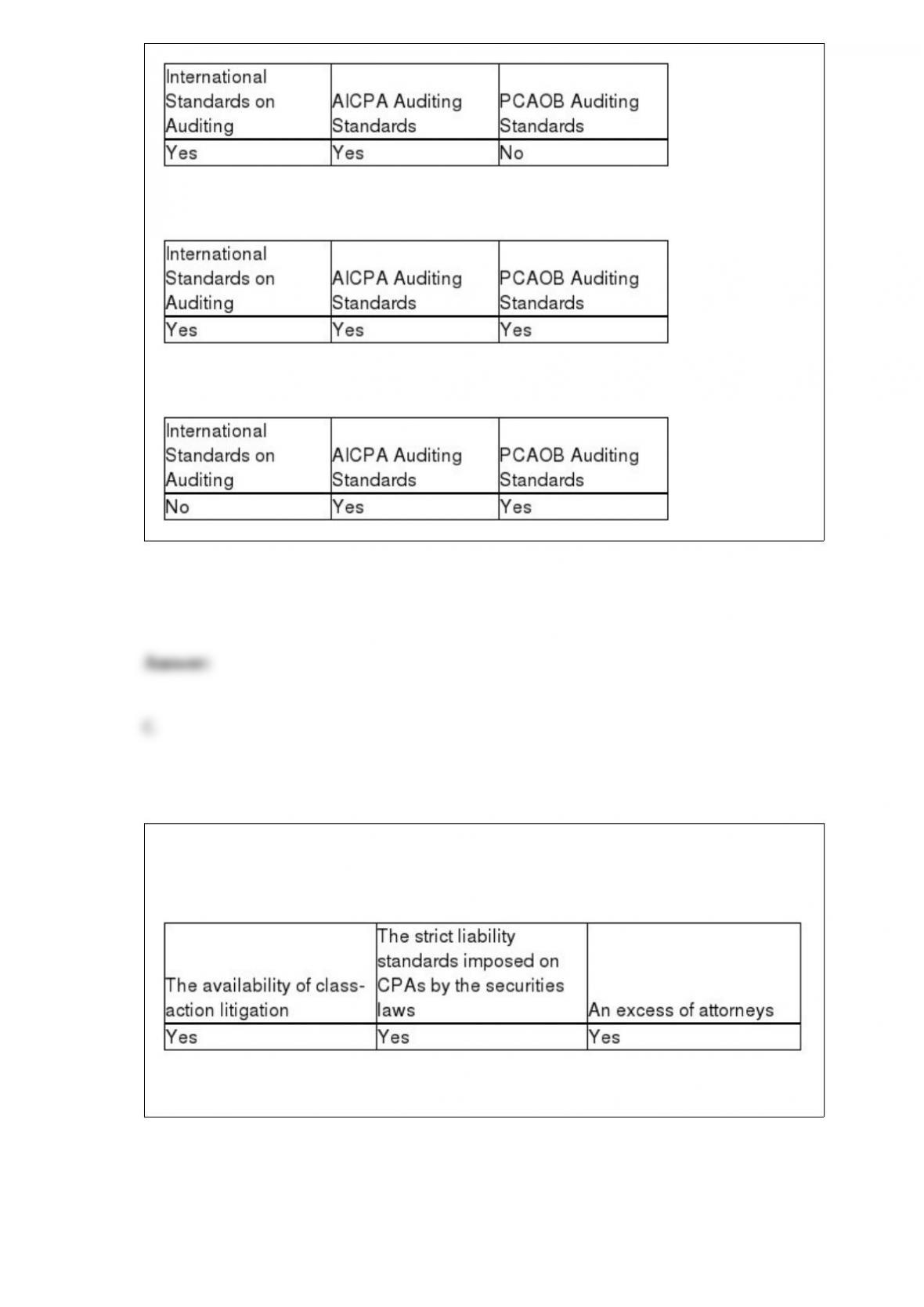

Which of the following are audit standards used in professional practice by audit firms?

A)

B)

C)

D)

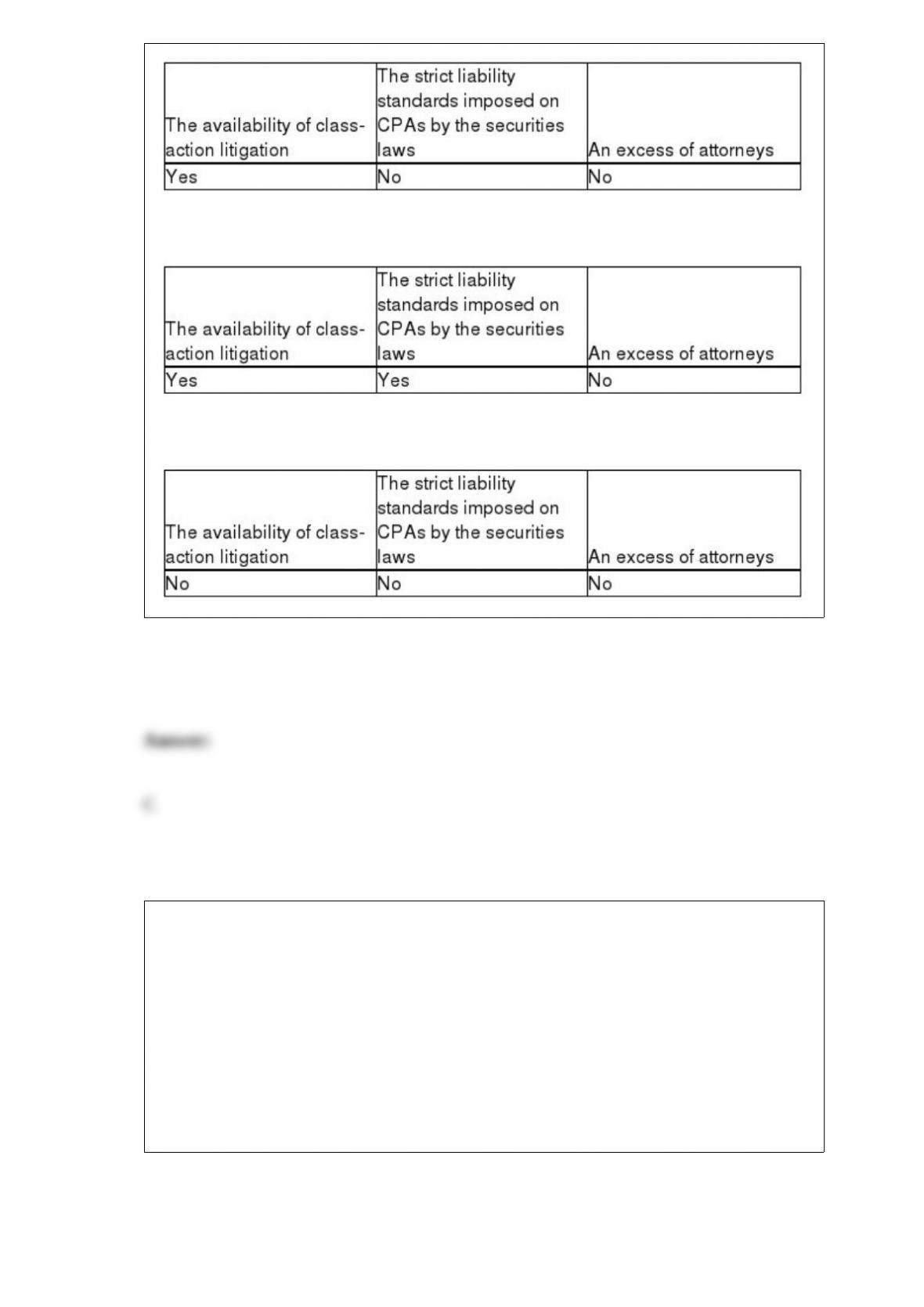

The increased litigation under the federal securities laws has resulted from

A)

B)

C)

D)

A six-step approach is often used to resolve an ethical dilemma. The first step in this

process is to

A) identify the alternative actions available.

B) identify the ethical issues from the facts.

C) determine who will be affected by the outcome of the dilemma.

D) obtain the relevant facts.

If the phrase “except for” is present in the opinion paragraph of the audit report, the

auditor has issued a(n)

A) adverse opinion.

B) disclaimer of opinion.

C) unqualified opinion.

D) qualified opinion.

When assessing control risk,

A) many auditors use actuarial tables to assist in the control risk assessment process.

B) each control can be used to satisfy only one audit objective.

C) many auditors use a control risk matrix to assist in the control risk assessment

process.

D) all controls, including key controls, should be considered.

Fictitious revenues

A) increase accounts receivable turnover.

B) understate the gross margin percentage.

C) lower accounts receivable turnover.

D) have no impact on the gross margin percentage.

Which of the following is a correct statement?

A) When internal controls are effective, control risk can be reduced, and therefore the

auditor will decrease the ARIA.

B) There is a direct relationship between ARIA and the required sample size.

C) A lower control risk requires a lower ARO in testing the controls.

D) ARO measures the auditor’s desired assurance for an account balance.

A company’s long-term solvency

A) can be measured by the gross profit percentage.

B) depends on the success of its operations and on its ability to raise capital for

expansion.

C) can be measured by the days to collect receivables ratio.

D) depends on its ability to generate cash for the payment of dividends.

Which of the following is an accurate statement regarding perpetual inventory master

files?

A) When perpetual inventory master files are accurate, auditors can test the physical

inventory after the balance sheet date.

B) It is a difficult procedure for the auditor to test the accuracy of the perpetual

inventory master files.

C) Auditors test the perpetual records for reductions in finished goods for sale as part of

the sales and collection cycle.

D) All of the above are accurate statements.

Which of the following statements is true?

A)

B)

C)

D)

If most or all users’ decisions that are based on the financial statements are likely to be

significantly affected, the materiality level is

A) unrestricted.

B) material.

C) pervasive.

D) risky.

________ accumulate costs by individual jobs as material is issued into production and

labor costs are incurred.

A) Just-in-time production systems

B) Job cost systems

C) Process cost systems

D) Manufacturing systems

The PCAOB places responsibility for the reliability of internal controls over the

financial reporting process on

A) the company’s board of directors.

B) the audit committee of the board of directors.

C) management.

D) the CFO and the independent auditors.

Which of the following statements is true of a public company’s financial statements?

A) Sarbanes-Oxley requires only the CEO to certify the financial statements.

B) Sarbanes-Oxley requires only the CFO to certify the financial statements.

C) Sarbanes-Oxley requires both the CEO and CFO to certify the financial statements.

D) Sarbanes-Oxley requires neither the CEO nor the CFO to certify the financial

statements.

Auditors may identify conditions during fieldwork that change or support a judgment

about the initial assessment of fraud risks. Which of the following is not a condition

which should alert an auditor that the initial assessment should be changed?

A) The subsidiary ledger agrees with the general ledger.

B) discrepancies in the accounting records

C) unusual relationships between the auditor and management

D) missing or conflicting evidence

Many auditors perform extensive analytical procedures because

A) they are required by GAAS.

B) they pinpoint errors in accounts.

C) they indicate areas of potential risk and misstatement.

D) they are required for tests of controls.

If analytical procedures are performed with no indications of likely misstatements,

ARIA will ________ and the sample size will ________.

A) remain the same; increase

B) decrease; decrease

C) increase; decrease

D) decrease; increase

Describe the methods used by the AICPA and State Boards of Accountancy to enforce

the rules of conduct.

Property, plant, and equipment is normally audited in a different manner than current

asset accounts. State three reasons why this is so, and discuss the differences in how

property, plant, and equipment is audited compared to current assets.

Briefly explain each management assertion related to account balances at period end.

List the three purposes of a program audit.

The transaction-related audit objectives and the client’s methods of controlling

misstatements are essentially the same for credit memos as for sales with the exception

of two differences. What are the two differences from the auditor’s perspective?

Besides the search for contingent liabilities and the review for subsequent events, the

auditor has four important final evidence accumulation responsibilities, all of which are

required by current professional auditing standards. Discuss each of these four

responsibilities.

Discuss three reasons why auditors are responsible for “reasonable” but not “absolute”

assurance.

Audit standards require the auditor to consider the combined amount of misstatement

early in the audit. This is known as preliminary materiality judgment. List and discuss

the three main factors that affect an auditor’s preliminary judgment about materiality.

Briefly discuss the brainstorming session required by current auditing standards. Be

sure to include a list of ideas that should be addressed in the session.

Discuss the overall objectives of the audit of notes payable.

Explain why monetary unit sampling, or probability proportional to size sampling, is

not useful for detecting understatements.

Instead of receiving a cutoff bank statement or if online access to client bank account

information is not available to the auditor, auditors can wait until the subsequent period

bank statement is available to verify reconciling items. Discuss the purpose of

reviewing the subsequent period bank statement and list the verifications the auditor

performs on this bank statement.

In designing substantive audit procedures for tests of transactions for sales, the auditor

needs to test for evidence of misstatements due to errors or fraud. Describe two

potential errors (unintentional) and one intentional (fraud).

List four specific matters that should be included in a client representation letter.

Discuss the key control procedures relating to the client’s physical count of inventory.

List the four principal purposes of the required communication with the audit

committee regarding certain additional information obtained during the audit.

Describe the five sources of information gathered to assess fraud risks.

Distinguish between contingent liabilities and commitments.

The reliability of evidence refers to the degree to which evidence is considered

believable or trustworthy. There are six factors that affect the reliability of audit

evidence. One factor is the independence of the provider; i.e., evidence obtained from a

source outside the client company is more reliable than that obtained within. Identify

and discuss any two of the remaining five factors.