Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

14-30

14-34 (continued)

d.

TRANSACTION-

RELATED

AUDIT OBJECTIVE

SUBSTANTIVE TEST OF TRANSACTIONS

AUDIT PROCEDURES

1. Recorded sales

occurred.

Select a sample of sales from sales journal and

examine customer’s purchase order, sales order

form, and bill of lading to determine that the goods

were ordered and shipped.

2. Existing sales

transactions are

recorded.

Perform analytical tests, including comparisons of

operating statistics to prior years’ and month to

month at year-end.

3. Recorded sales

transactions are stated

at the correct amounts.

Compare sales prices to price lists. Examine

customer correspondence indicating pricing

disputes. Test clerical accuracy of a sample of sales

invoices.

4. Sales transactions are

properly included in

the accounts

receivable master file

and are correctly

summarized.

Foot the sales journal and trace the balance to the

general ledger.

5. Recorded sales are

properly classified.

Examine sales documents to determine that sales

transactions are properly classified.

6. Sales are recorded on

the correct dates.

Compare dates on bills of lading to the sales journal

to determine that sales are recorded on a timely

basis. Compare sales month to month and

investigate any significant fluctuations, especially

near year-end.

e. An audit program for conducting the audit of sales is as follows:

1. Obtain the sales journal for the year and perform the following

procedures:

general ledger balance.

(b) From the journal, select a sample of invoices and

perform the following:

14-31

14-34 (continued)

Compare quantity, sales price, customer name,

and date of shipment to sales journal. Obtain

explanation of any differences.

(2) Examine sales order form for indication of

credit approved.

2. Select a sample of bill of lading numbers. Locate the

sales journal to determine the promptness of recording.

3. Examine customer correspondence during the year for

disputes on pricing of invoices.

4. Prepare a schedule of sales, cost of sales, and gross margin

percentage, showing comparison between recent years and

fluctuations.

Integrated Case Application

14-35 a.,

b.,

c.,

and d.

PINNACLE MANUFACTURING―Part V

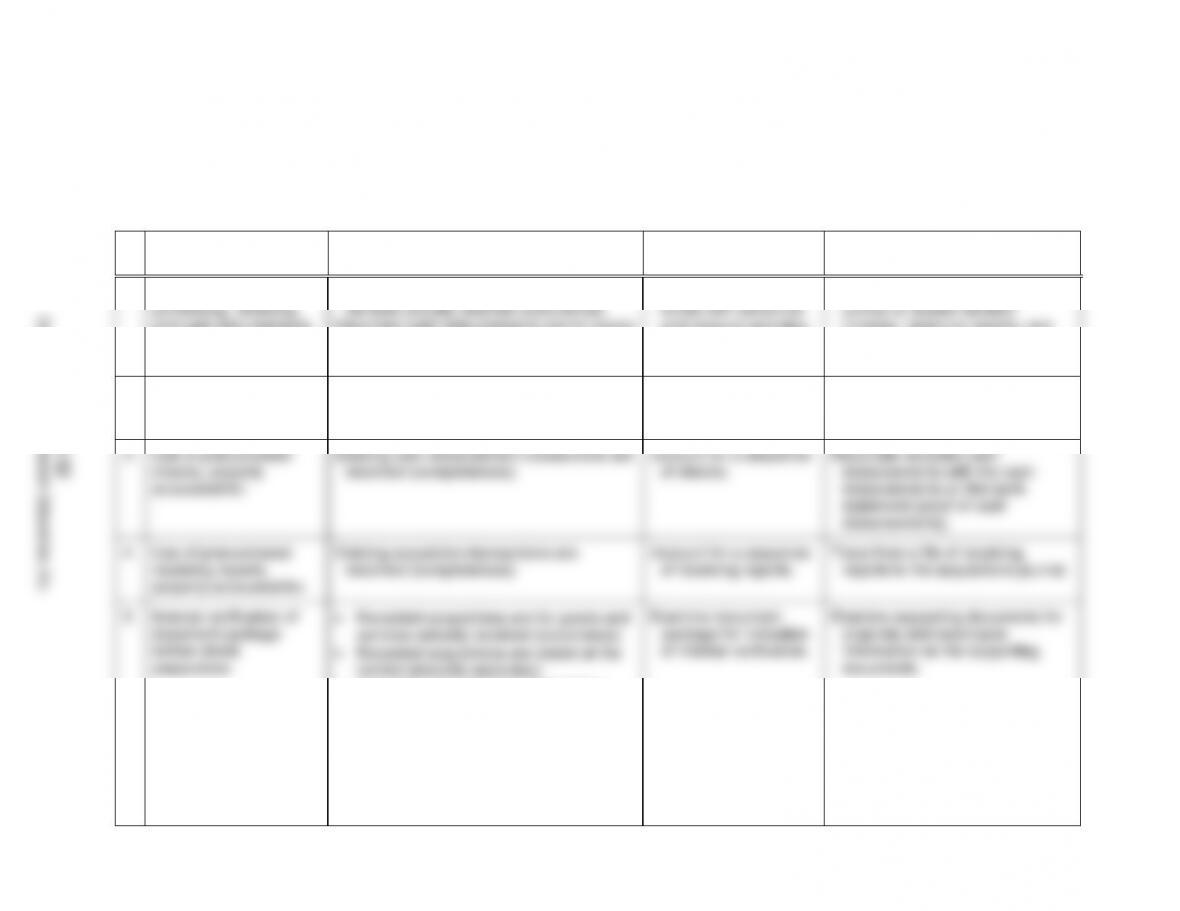

#

a.

Key Internal Control

b.

Transaction Related Audit Objectives

c.

Test of Control

d.

Substantive Test of Transaction

1.

Segregation of the

purchasing, receiving,

and cash disbursements

functions.

Recorded acquisitions are for goods and

services actually received (occurrence).

Recorded cash disbursements are for goods

and services actually received

(occurrence).

Discuss segregation of

duties with personnel

and observe activities.

Trace entries in the acquisitions

journal to related vendors’

invoices, receiving reports, and

purchase orders.

2.

Use of prenumbered

voucher packages,

properly accounted for.

Existing acquisition transactions are

recorded (completeness).

Account for a sequence

of voucher packages.

Trace from a file of vendors’

invoices to the acquisitions

journal.

3.

Use of prenumbered

checks, properly

accounted for.

Existing cash disbursement transactions are

recorded (completeness).

Account for a sequence

of checks.

Reconcile recorded cash

disbursements with the cash

disbursements on the bank

statement (proof of cash

disbursements).

4.

Use of prenumbered

receiving reports,

properly accounted for.

Existing acquisition transactions are

recorded (completeness).

Account for a sequence

of receiving reports.

Trace from a file of receiving

reports to the acquisitions journal.

5.

Internal verification of

document package

before check

preparation.

Recorded acquisitions are for goods and

services actually received (occurrence).

Recorded acquisitions are stated at the

correct amounts (accuracy).

Acquisition transactions are properly

included in the master files, and are

properly summarized (posting and

summarization).

Acquisitions are properly classified

(classification).

Acquisitions are recorded on the correct

dates (timing).

Examine document

package for indication

of internal verification.

Examine supporting documents for

propriety and recompute

information on the supporting

documents.

14-32

Copyright © 2017 Pearson Education, Inc.

14-35 (continued)

a.,

b.,

c.,

and d.

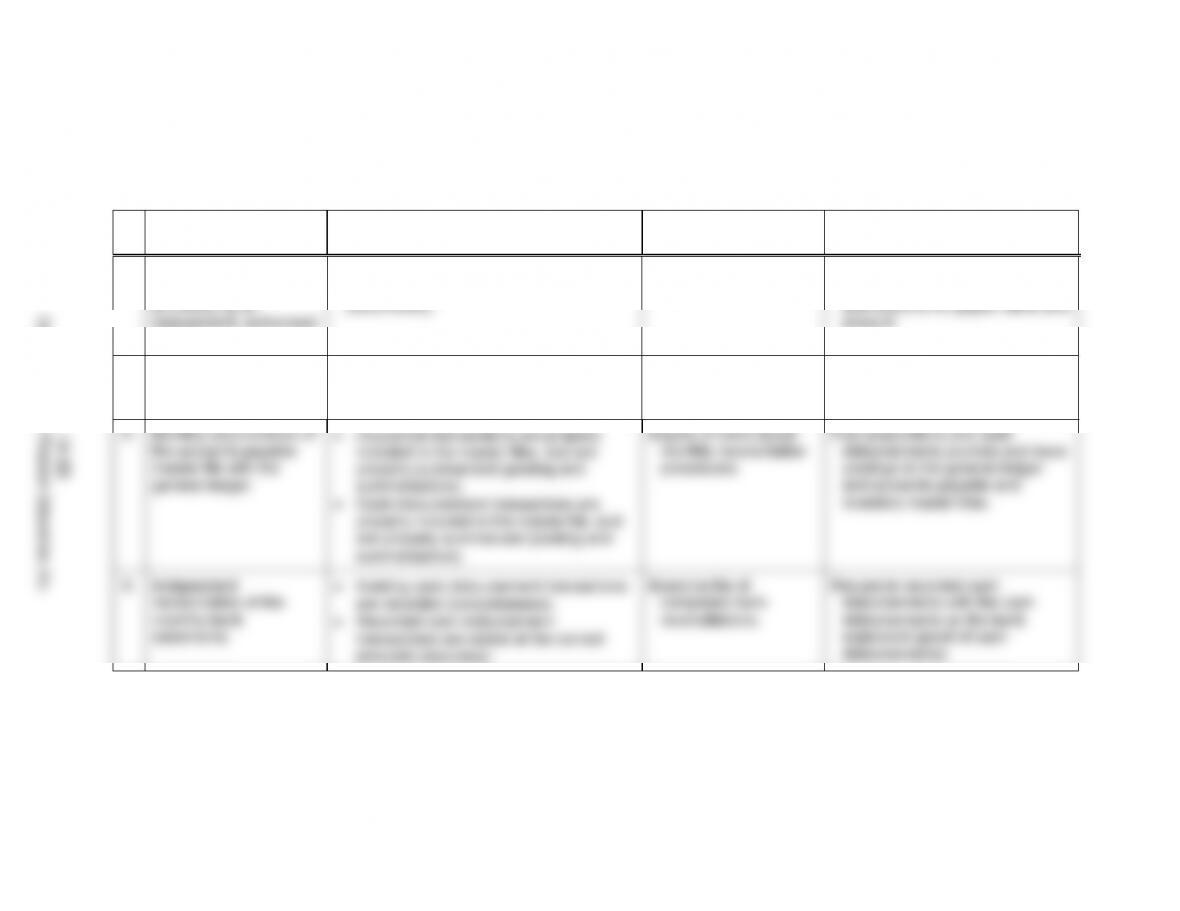

#

a.

Key Internal Control

b.

Transaction Related Audit Objectives

c.

Test of Control

d.

Substantive Test of Transaction

6.

Review of supporting

documents and signing

of checks by an

independent, authorized

person.

Recorded cash disbursements are for goods

and services actually received

(occurrence).

Examine checks for

signature.

Trace the cancelled check to the

related acquisitions journal entry

and examine for payee name and

amount.

7.

Cancellation of

documents prior to

signing of the check.

Recorded acquisitions are for goods and

services actually received (occurrence).

Examine indication of

cancellation.

Examine the acquisitions journal

for duplicate entries to a vendor.

8.

Monthly reconciliation of

the accounts payable

master file with the

general ledger.

Acquisition transactions are properly

included in the master files, and are

properly summarized (posting and

summarization).

Cash disbursement transactions are

properly included in the master file, and

are properly summarized (posting and

summarization).

Inquire of client about

monthly reconciliation

procedures.

Foot acquisitions and cash

disbursements journals and trace

postings to the general ledger

and accounts payable and

inventory master files.

9.

Independent

reconciliation of the

monthly bank

statements.

Existing cash disbursement transactions

are recorded (completeness).

Recorded cash disbursement

transactions are stated at the correct

amounts (accuracy).

Examine file of

completed bank

reconciliations.

Reconcile recorded cash

disbursements with the cash

disbursements on the bank

statement (proof of cash

disbursements).

14-33

Copyright © 2017 Pearson Education, Inc.

14-35 (continued)

e.

Acquisitions Substantive Tests of Transactions

Note: More than one audit procedure is listed for certain objectives even though the requirement is for only one procedure.

TRANSACTION-RELATED

AUDIT OBJECTIVES

SUBSTANTIVE AUDIT PROCEDURES

Occurrence

Examine underlying documents for propriety.

large or unusual amounts.

Completeness

Trace a sample of receiving reports to the acquisitions journal.

Trace from a file of vendors’ invoices to the acquisitions journal.

Trace from additions in perpetual inventory records to recorded acquisitions.

Accuracy

Compare amounts for entries in acquisitions journal to related vendors’ invoices,

purchase orders and receiving reports.

Recompute information on vendor invoices.

Compare prices on vendor invoices with approved price limits established by

management.

Posting and Summarization

Trace individual entries in accounts payable master file to acquisitions journal.

Classification

Examine vendors’ invoices for proper classification.

Compare classification with chart of accounts by reference to vendors’ invoices.

Timing

Compare dates of receiving reports and vendors’ invoices with dates in the

acquisitions journal.

14-34

Copyright © 2017 Pearson Education, Inc.

14-35 (continued)

f.

Cash Disbursements Substantive Tests of Transactions

Note: More than one audit procedure is listed for certain objectives even though the requirement is for only one procedure.

TRANSACTION-RELATED

AUDIT OBJECTIVES

SUBSTANTIVE AUDIT PROCEDURES

Occurrence

Trace cancelled check numbers in the cash disbursements journal to related cancelled

Examine cancelled check for authorized signature, proper endorsement, and

cancellation by the bank.

Review the cash disbursements journal, general ledger, and accounts payable master

file for large or unusual amounts.

Trace cancelled check to the related acquisitions journal entry and examine for payee

name and amount.

Completeness

Trace entries in acquisitions journal to subsequent payment in cash disbursements

journal.

Accuracy

Compare cancelled checks with the related acquisitions journal and cash disbursements

journal entries.

Recompute cash discounts.

Posting and Summarization

Trace individual entries in accounts payable master file to cash disbursements journal.

Classification

Compare classification with chart of accounts by reference to vendors’ invoices and

acquisitions journal.

Timing

Compare dates on cancelled checks with cash disbursements journal.

Compare dates on cancelled checks with the bank cancellation date.

14-35

Copyright © 2017 Pearson Education, Inc.

14-36

14-35 (continued)

through f.

General

1. Discuss the following items with client personnel and observe

activities:

a. Segregation of duties

with the general ledger.

2. Test journal summarization and posting for a test month:

master files.

b. Foot cash disbursements journal and trace postings

3. Examine file of completed bank reconciliations.

4. Account for a sequence of cancelled checks.

5. Reconcile recorded cash disbursements with cash

Acquisitions

8. Trace entries in the acquisitions journal to related vendors’

invoices, receiving reports, and purchase orders.

and summarization.

b. Examine supporting documents for propriety.

14-37

14-35 (continued)

9. Account for a sequence of receiving reports and voucher

packages.

10. Trace a sample of receiving reports and vendors’ invoices

to the acquisitions journal.

Cash Disbursements

11. Select a sample of cancelled checks and:

a. Trace cancelled check to the related cash

14-36 ACL Problem Solution

the worksheet on the screen).

b. There are nine shipments with ship dates in 2013. (Use Quick Sort

command for the ship_date column).

c. There are no duplicate shipping numbers. There are 24 gaps

involving 46 missing shipping documents. A number of the gaps

misstatements. (Use Gaps and Duplicates command under

Analyze for the Shipping Number column).

d. The greatest number of shipments was 11 to customer 0239212,

which is a small percentage of the 4,082 shipments. The most

shipments by customer number).

14-38

14-36 ACL Problem Solution (continued)

descending order).

f. There are 1,042 shipments with 100 or more items. The output

using 10 equal intervals is shown below. (Use Filter to exclude all

shipments with less than 100 items and then use Stratify

<<< STRATIFY over 100-> 183 >>>

>>> Minimum encountered was 100

>>> Maximum encountered was 183

items_shipped Count <-- % % --> Items

Shipped

100 -> 108 141 13.53% 10.48% 14,685

109 -> 116 138 13.24% 11.08% 15,530

117 -> 124 144 13.82% 12.39% 17,376

125 -> 133 102 9.79% 9.39% 13,165

1042 100.00% 100.00% 140,187