Auditing standards require that the auditor evaluate whether there is a substantial doubt

about a client’s ability to continue as a going concern for at least

A) one quarter beyond the balance sheet date.

B) one quarter beyond the date of the auditor’s report.

C) one year beyond the balance sheet date.

D) one year beyond the date of the auditor’s report.

The two characteristics of the appropriateness of evidence are

A) relevance and timeliness.

B) relevance and accuracy.

C) relevance and reliability.

D) reliability and accuracy.

What typically initiates the acquisitions and payment cycle?

A) issuance of a purchase requisition or request for purchase of goods or services

B) issuance of payment to vendor

C) approval of a new vendor

D) purchase requisition

The Securities and Exchange Commission requires quarterly financial information as a

part of the

A) 10-K report.

B) 10-Q report.

C) 8-K report.

D) auditor’s report.

Which of the following tests commonly occur together?

A) substantive tests of transactions and tests of controls

B) substantive tests of transactions and obtaining an understanding of internal controls

C) analytical procedures and tests of controls

D) tests of controls and tests of details of balances

Auditing standards specifically require auditors to identify ________ as a fraud risk in

most audits.

A) overstated assets

B) understated liabilities

C) revenue recognition

D) overstated expenses

The auditor has a responsibility to review transactions and activities occurring after the

balance sheet date to determine whether anything occurred that might affect the

statements being audited. The procedures required to verify these transactions are

commonly referred to as the review for

A) contingent liabilities.

B) subsequent year’s transactions.

C) late unusual occurrences.

D) subsequent events.

Which of the following procedures would most likely be performed in response to the

auditor’s assessment of the risk of monetary misstatements in the financial statements?

A) ratio analysis

B) tests of controls

C) tests of details of balances

D) risk assessment procedures

When evaluating the results of attributes sampling,

A) the acceptable risk of overreliance (ARO) is set at high or low.

B) tables are used to compute the computed upper exception rate (CUER).

C) if the sample size is not equal to those provided for in the attributes sampling

evaluation tables, the tables cannot be used.

D) the true exception rate is computed from various tables.

The audit objective of determining that cash in bank, as stated on the reconciliation,

foots correctly and agrees with the general ledger can be tested by which of the

following procedures?

A) performing tests for kiting

B) receiving and testing a cutoff bank statement

C) proving the bank reconciliation as to additions and subtractions, including all

reconciling items

D) examining the minutes of the board of directors for restrictions on the use of cash

Which of the following is an accurate statement regarding the auditor’s responsibility

for understanding internal control?

A) Transaction-related audit objectives typically have no impact on the rights and

obligations objectives.

B) Transaction-related audit objectives typically have a significant impact on the

balance-related audit objective of realizable value.

C) Auditors generally emphasize internal control over account balances rather than

classes of transactions.

D) Auditors and management are both equally concerned about controls that affect the

efficiency and effectiveness of company operations.

A CPA firm should decline an offer to perform consulting services engagement if

A) the proposed engagement is not accounting related.

B) recommendations made by the CPA firm are to be subject to review by the client.

C) acceptance would require the CPA firm to make management decisions for an audit

client.

D) any of the above is true.

Which of the following is a form of earnings management in which revenues and

expenses are shifted between periods to reduce fluctuations in earnings?

A) fraudulent financial reporting

B) expense smoothing

C) income smoothing

D) Each of the above is correct.

An interim review of the financial information for public companies is performed

following standards of the

A) American Institute of Certified Public Accountants (AICPA).

B) Public Company Accounting Oversight Board (PCAOB).

C) Securities and Exchange Commission (SEC).

D) Statements on Standards for Accounting and Review Services (SSARS).

An auditor uses ________ inquiry to corroborate or contradict prior information.

A) assessment

B) declarative

C) interrogative

D) informational

________ is the tendency to make assessments by starting from an initial value and

then adjusting insufficiently away from that initial value.

A) Anchoring

B) Availability

C) Overconfidence

D) Confirmation

The most important consideration in evaluating the fairness of the amounts accrued for

vacation pay, sick pay, and other benefits is the

A) consistent accrual of these liabilities relative to those of preceding periods.

B) actual expense incurred for the prior period.

C) amount expended to date in the current period.

D) profitability of the client which will enable these liabilities to be met.

Under the AICPA independence rules, independence can be considered impaired when

A) billed fees remain unpaid for professional services for more than ninety days.

B) a client in bankruptcy has unpaid fees for more than one year.

C) there is litigation by the client related to the auditor’s tax or other nonaudit services

for an immaterial amount.

D) there is a lawsuit by the client claiming deficiencies in the previous year’s audit.

Which of the following would not increase the risks of material misstatement at the

overall financial statement level?

A) effective oversight by the board of directors

B) deficiencies in management’s integrity

C) inadequate accounting systems

D) all of the above

In the accounts receivable master file, the length of time the account has been due can

be useful to the client and the auditor in preparing the

A) trial balance.

B) working trial balance.

C) accounts receivable trial balance.

D) aged accounts receivable trial balance.

If the scope restriction imposed by the client is so material that the overall fairness of

the financial statements is in question, the auditor should issue a(n)

A) standard unmodified opinion.

B) disclaimer of opinion.

C) adverse opinion.

D) unmodified opinion with revised wording in the scope paragraph.

When auditing accrued property taxes,

A) the source for the debits to the liability account is the acquisitions journal.

B) realizable value is an important balance-related audit objective.

C) the ending balance in the account should be confirmed with the applicable taxing

authority.

D) the most important consideration for the auditor is that the same portion of each tax

payment for the accrual that was used in the preceding year is used in the current year.

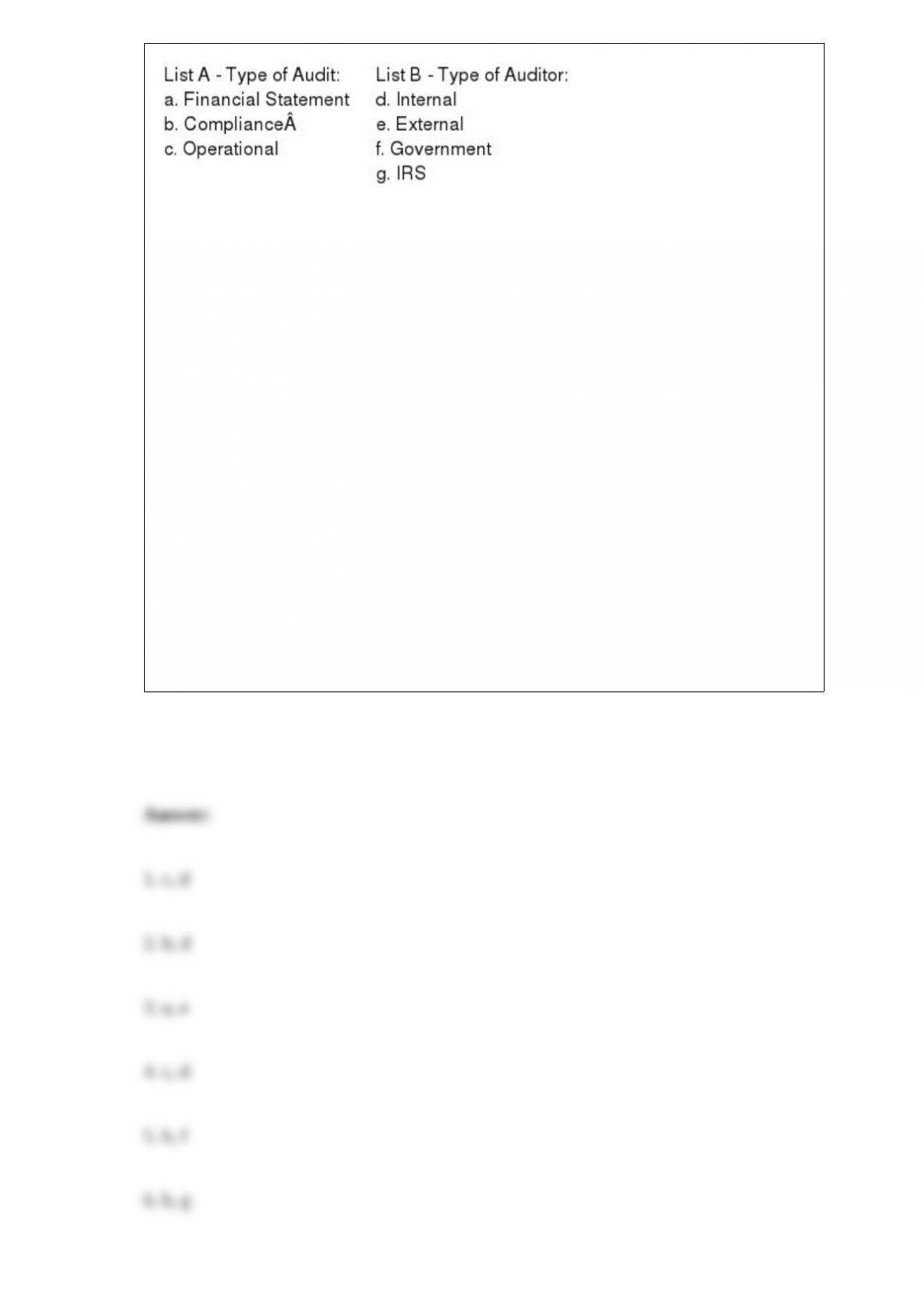

Match the engagement described to the (A) type of audit and (B) auditor that would

most likely perform the engagement. Each engagement will have an answer from List-A

and List-B. An answer can be used once, more than once, or not at all.

Engagement:

1. Evaluate a company’s payroll processing for economy.

2. Evaluate/determine if bank covenants are being met.

3. Evaluate financial statements that are to be submitted to a bank.

4. Evaluate the promptness of materials inspection in a manufacturer’s receiving

department.

5. Determine if Medicare reimbursements are in accordance with the Healthcare

Financing Administration (HCFA).

6. Determine if the tax return of a multinational corporation is in accordance with the

tax code.

7. Determine if a public school is properly applying their reimbursement for the

payment-in-kind program.

8. Determine the effectiveness of a Department of Defense project.

A ________ is a document that indicates a request for merchandise by a customer.

A) sales invoice

B) vendor invoice

C) customer order

D) sales order

The auditor normally does not need to test the accuracy or classification of fixed assets

recorded in prior periods if they are the continuing auditor because

A) they are rarely material to the audit.

B) they rarely contain misstatements.

C) they are verified in previous audits.

D) they don’t affect the balance sheet.

Which of the following is an accurate statement regarding a company’s ability to meet

its long-term debt obligations?

A) If the debt-to-equity ratio is too high, it may indicate that the company has used up

its borrowing capacity.

B) If the debt-to-equity ratio is too high, it may mean that available leverage is not

being used to the owners’ benefit.

C) The times interest earned ratio indicates if a company can make its principal and

interest payments.

D) The key ratios that are used to measure a long-term solvency are debt to equity,

return on assets, and times interest earned.

In testing for the transaction-related audit objective of occurrence, an auditor is

verifying that the recorded payroll payments are for work actually performed by

existing employees. List three key internal controls that a company should have in place

in this area.

When dealing with financial instruments, the most difficult balance-related audit

objective to test is

A) existence.

B) accuracy.

C) rights.

D) realizable value.

Calculating the gross margin for the current audit year as a percent of sales and

comparing it with previous years is what type of evidence?

A) physical examination

B) analytical procedures

C) observation

D) inquiry

The fieldwork for the December 31, 2016 audit of Schmidt Corporation ended on

March 17, 2017. The financial statements and auditor’s report were issued on March 29,

2017. In each of the material situations (1 through 5) below, indicate the appropriate

action (a, b, c). The possible actions are as follows

a. Adjust the December 31, 2016 financial statements.

b. Disclose the information in a footnote in the December 31, 2016 financial statements.

c. No action is required.

The situations are as follows:

________ 1. On March 1, 2017, one of Schmidt Corporation’s major customers

declared bankruptcy. The customer’s financial condition in 2016 was deteriorating and

they owed Schmidt Corporation a large sum of money as of the balance sheet date.

________ 2. On February 17, 2017, Schmidt Corporation sold some machinery for its

book value.

________ 3. On February 20, 2017 a flood destroyed the entire uninsured inventory in

one of Schmidt’s warehouses.

________ 4. On January 5, 2017, there was a significant decline in the market value of

the securities held for resale from their value as of the balance sheet date.

________ 5. On March 10, 2017, the company settled a lawsuit at an amount

significantly higher than the amount recorded as a liability on the books as of the

balance sheet date.

You are auditing the long-term notes payable account for a client. Which of the

following audit procedures would you most likely employ?

A) Compare interest expense recorded by the client with the notes payable account for

reasonableness.

B) Confirm bonds payable with individual bond holders.

C) Perform analytical procedures on the bond discount or premium account.

D) Examine bond documents for the presence of hybrid securities.

In order to promote audit efficiency the auditor considers cost in selecting audit tests to

perform. Which of the following audit tests would be the most costly?

A) substantive analytical procedures

B) risk assessment procedures

C) tests of controls

D) tests of details of balances

Research indicates that the most effective way to prevent and deter fraud is to

A) implement programs and controls that are based on core values embraced by the

company.

B) hire highly ethical employees.

C) communicate expectations to all employees on an annual basis.

D) terminate employees who are suspected of committing fraud.