21–25 (continued)

CLIENT

a.

ISSUES

TO CONSIDER

b.

LOCATIONS TO VISIT

c.

POTENTIAL RISKS

OF MATERIAL

MISSTATEMENT

d.

AUDITOR

RESPONSES

TO RISKS

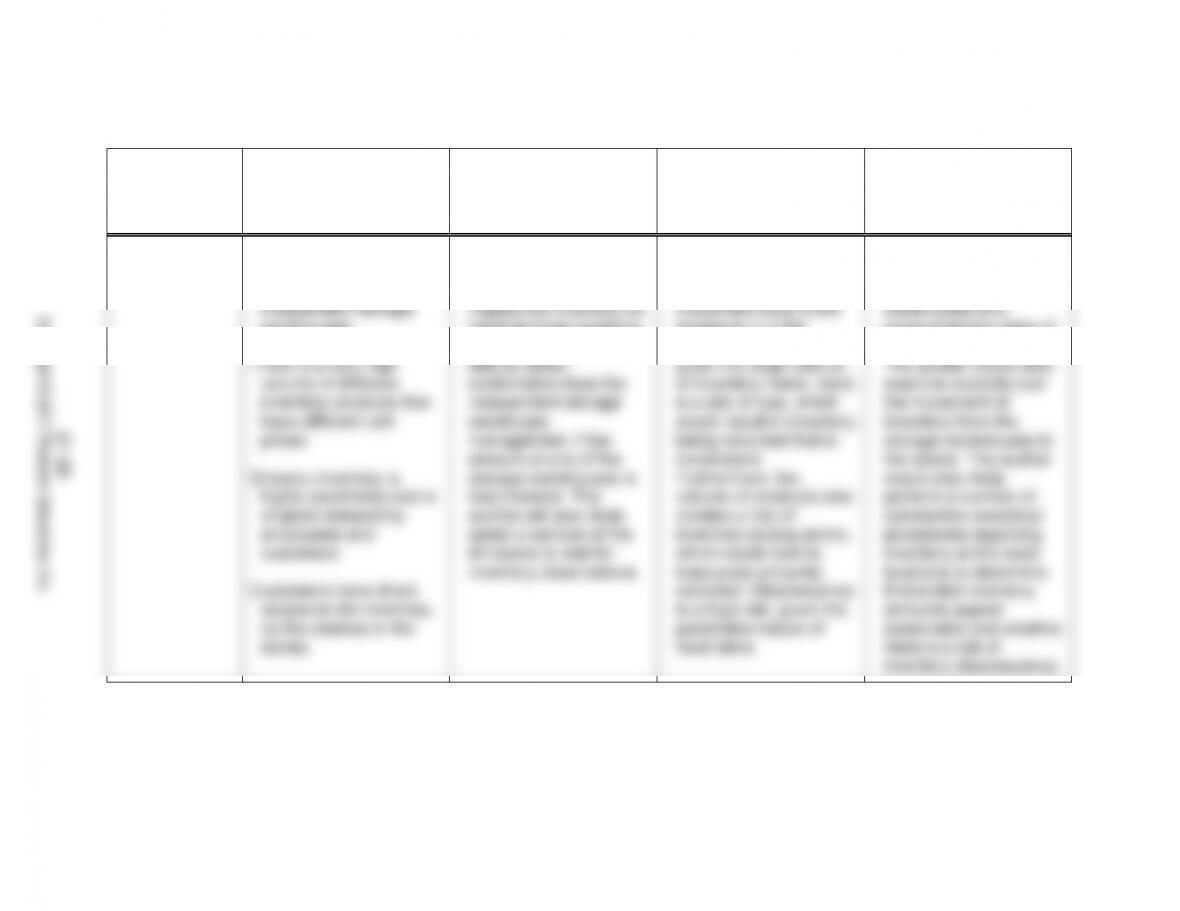

4. Food Giant

Three–fourths of the

inventory balance is

located at the five

independent storage

warehouses.

There is a very high

volume of different

inventory products that

have different unit

prices.

Grocery inventory is

highly perishable and is

of great demand by

employees and

customers.

Customers have direct

The auditor will most

likely visit the five

distribution centers to

inspect the inventory on

hand at those locations.

The auditor might be

able to obtain

confirmation from the

independent storage

warehouse

management, if the

amount at one of the

storage warehouses is

less material. The

auditor will also likely

select a sample of the

42 stores to visit for

inventory observations.

There is a risk of theft

given grocery inventory

is of high demand and

customers have direct

access to it in the

stores. Additionally,

given the large volume

of inventory items, there

is a risk of loss, which

would result in inventory

being recorded that is

nonexistent.

Furthermore, the

volume of products also

creates a risk of

inventory pricing errors,

which would lead to

inaccurate amounts

recorded. Obsolescence

The auditor would

examine inventory on

hand at the storage

warehouses and

conduct pricing tests of

the inventory records.

The auditor would also

examine controls over

the movement of

inventory from the

storage warehouses to

the stores. The auditor

would also likely

perform a number of

substantive analytical

procedures regarding

inventory at the store

locations to determine

if recorded inventory

21–20

Copyright © 2017 Pearson Education, Inc.

21–21

21–26 (see text Web site for Excel solution.– Filename P2126.xls)

a.

2016 2015 2014 2013

Gross margin % 26.3% 22.6% 22.4% 22.4%

Inventory turnover 6.6 7.6 7.6 7.9

b. Logical causes of the changes in the gross margin as a percent of

sales include:

in cost of sales.

2. The method of accounting for inventory was changed,

causing a higher ending inventory (more expenses absorbed

into inventory) and lower cost of sales.

items were sold than in previous years.

5. An improper journal entry was recorded, which adjusted the

gross margin upward.

Logical causes of the changes in the inventory turnover include:

1. The increased selling prices, which caused the gross margin

decreased the inventory turnover.

of increased sales in the future.

expected inventory)

$11.6 million – 9.0 million =

$2,600,000 potential misstatement

Both calculations indicate a potential misstatement exceeding

$2,000,000.

21–22

21–26 (continued)

21–27 a. 1. Exclude

2. Include

3. Include

4. Exclude

5. Exclude

b. 1. Goods held “on consignment” do not belong to the consignee,

and should not be included in inventory.

it should be included in inventory.

3. Title to goods shipped F.O.B. shipping point normally passes

to the buyer on delivery to the transportation agency, and in

this instance the goods belong to your client at December

31, 2016. There is an error in recording the acquisition.

materials and labor are appropriated to the job. When the

job is completed and ready for shipment as in this case, it

may be considered as a completed sale.

21–28 a. 1. Extension errors are as follows:

DESCRIPTION

EXTENSION

AS

RECORDED

ACTUAL

EXTENSION

OVER

(UNDER)

STATEMENT

Wood

Metal cutting tool

Cutting fluid

Sandpaper

$ 11.04

1,740.00

240.00

579.00

$ 110.40

1,470.00

1,040.00

5.70

$ ( 99.36)

270.00

(800.00)

573.30

$ ( 56.06)

21–23

21–28 (continued)

2. The differences in the previous year’s and this year’s cost

indicate a problem. The auditor should attempt to obtain

support for the current year’s cost if the effect of the

reasonableness indicates the following:

a) Precision cutting torches are expensive. Maybe $800

or a price list.

b) Aluminum scrap values may fluctuate significantly.

The two prices may be reasonable. Look at sales

invoices for the two years.

c) Lubricating oil cost appears unreasonable for this

the need for disclosure of the misstatements.

3. Investigate the reasons for the omission of these tags from

final inventory compilation. If it is determined that the omission

4. Page total footing errors are as follows:

PAGE NO.

CLIENT

TOTAL

CORRECT

TOTAL

OVER– (UNDER–)

STATEMENT

14

82

$2,375.36

6,721.18

$2,375.30

6,421.18

$ 0.06

300.00

$300.06

must consider sampling error.

The net effect of the misstatements for which we were able

to compute the actual misstatement was an overstatement of

inventory by $244.00, which is a small amount (see items 1 and 4).

21–24

21–28 (continued)

reasonableness and obvious misstatements.

For the items for which the amount of the misstatement

could not be determined, the auditor should follow up as described

in 2 and 3 above. From the results of the follow–up, the effect of

c. Prior to compiling the inventory next year, Martin Manufacturing

should implement the following internal controls:

1. Review formulas in schedule for inventory compilation.

Accuracy of spreadsheet should be independently reviewed.

Material in Car #AR38162 — received

in warehouse on January 2, 2017 $ 8,120

Materials stranded en route

this case.

21–25

21–29 (continued)

b. Auditor’s worksheet adjusting entries:

1. Purchases $ 2,183

Accounts Payable $ 2,183

To record goods in warehouse but

not invoiced–received on RR 1060.

To reverse out of sales material

included in both sales (SI 966)

and in physical inventory

(after adjustment).

5. No adjustment required.

6. Claims receivable 1,600

Purchases 1,250

Freight In 350

To reverse out of sales invoices

#969, 970, 97l. The sales book

was held open too long. This

merchandise was in warehouse

at time of physical count and so

included therein.

21–26

■ Case

21–30 (see text Web site for Excel solution.– Filename P2130.xls)

Descriptions of the potential inventory misstatements for the seven items in

question are provided below:

A. A price of $8 is proper for pricing L37 spars at 12–31–16 since

the next shipment of spars was not received until 1–06–17.

However, the next invoice shows a lower cost, which indicates

B. The total is 10,000 inches/12 = 833.33 feet times $1.20 per

833 feet (10,000/12) = $1,155.79 or an overstatement of

inventory by $10,844.21.

C. FIFO value would be:

Voucher 12–61 1,000 yards at $10.00 per yard = $10,000

date is after year–end.

D. FIFO value would be:

the cost.

E. Pricing is correct if the item is for inventory. It is possible

that this item should be capitalized.

F. Proper FIFO cost is 40 pair x 2 = 80 springs x $69.00

each = $5,520. Inventory is understated by $5,244.

21–30 (continued)

b.

SEA GULL AIRFRAMES, INC.

SUMMARY OF INVENTORY MISSTATEMENTS

Quantity

Price

Item No. and

Description

Per

Inventory

Correct

Difference

Per

Inventory

Correct

Difference

Recorded

Amount

Correct

Amount

Amount of

Misstatement

A. L37 Spars

B. B68 Metal Formers

C. R01 Metal Ribs

D. St26 Struts

E. Industrial hand

drills

F. L803 Steel Leaf

Springs

G. V16 Fasteners

3,000

10,000

1,500

1,000

45

40

5.50

3,000

833

1,500

1,000

45

80

5.50

0

9,167

0

0

0

– 40

0

8.00

1.20

10.00

8.00

20.00

69.00

10.00

8.00

1.3875

10/9.50

8/8.20

20.00

69.00

10.00

0.00

– 0.1875

.50

– .20

0.00

0.00

0.00

24,000.00

12,000.00

15,000.00

8,000.00

900.00

276.00

55.00

24,000.00

1,155.79

14,750.00

8,040.00

900.00

5,520.00

55.00

0.00

– 10,844.21

– 250.00

40.00

0.00

5,244.00

0.00

Total misstatement

– 5,810.21

Items over $5,000

Items under

$5,000

– 11,054.21

5,244.00

– 5,810.21

CONCLUSION: (see next page for calculations)

REMARKS:

There is a material potential misstatement due to the

number and size of misstatements found relative to

the sample chosen. In order to determine a more

accurate estimate of the actual misstatement,

additional tests are necessary.

A. NRV [assumed] exceeds cost.

B. Quantity based on inches, not feet; freight not included.

C. 500 yards overpriced.

D. 200 feet underpriced. NRV [assumed] O.K.

E. [Assumed] not capitalizable.

F. Includes extension error in inventory.

G. Consider separately for obsolescence.

21–27

Copyright © 2017 Pearson Education, Inc.

21–28

21–30 (continued)

PROJECTED MISSTATEMENTS

Dollars tested

Sample items Over 5,000 Under $5,000

No exceptions 360,000 2,600

A 24,000

B 12,000

results are equally unacceptable.