Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

21-11

21-18 (continued)

records than the costs themselves).

3. The cost accounting records also deal with transferring

inventories through the production cycle and then from

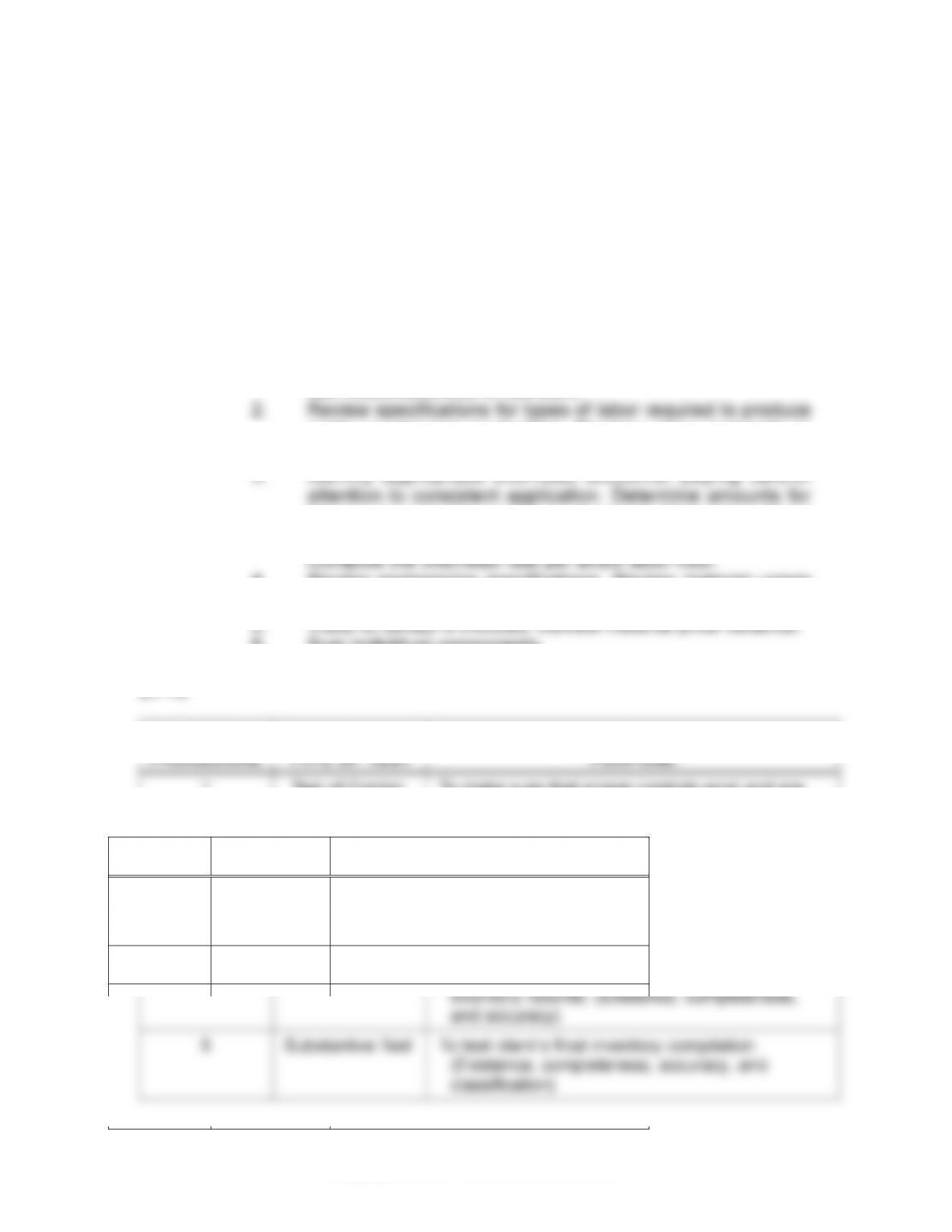

b. 1. Examine engineering specifications for expected (standard)

labor hours. Examine time records for hours worked on the

test reasonableness of standard.

2. Review specifications for types of labor required to produce

parts, or observe production. Review union contracts or

3. Identify appropriate overhead accounts, paying careful

attention to consistent application. Determine amounts for

these accounts for a measured period. Determine direct

4. Review engineering specifications. Review material usage

variance.

21-19

AUDIT

PROCEDURE

a.

TYPE OF TEST

b.

PURPOSE

1

Test of Control

To make sure that proper controls exist and are

being followed in the taking of the physical

inventory. (Existence, completeness, accuracy,

and classification)

2

Substantive Test

To identify slow-moving inventory that may need

to be written down. (Realizable value)

3

Substantive Test

To ensure that all inventory represented by an

inventory tag actually exists. (Existence)

4

Substantive Test

To test the accuracy of the client’s perpetual

inventory records. (Existence, completeness,

and accuracy)

5

Substantive Test

To test client’s final inventory compilation.

(Existence, completeness, accuracy, and

classification)

21-12

21-19 (continued)

AUDIT

PROCEDURE

a.

TYPE OF TEST

b.

PURPOSE

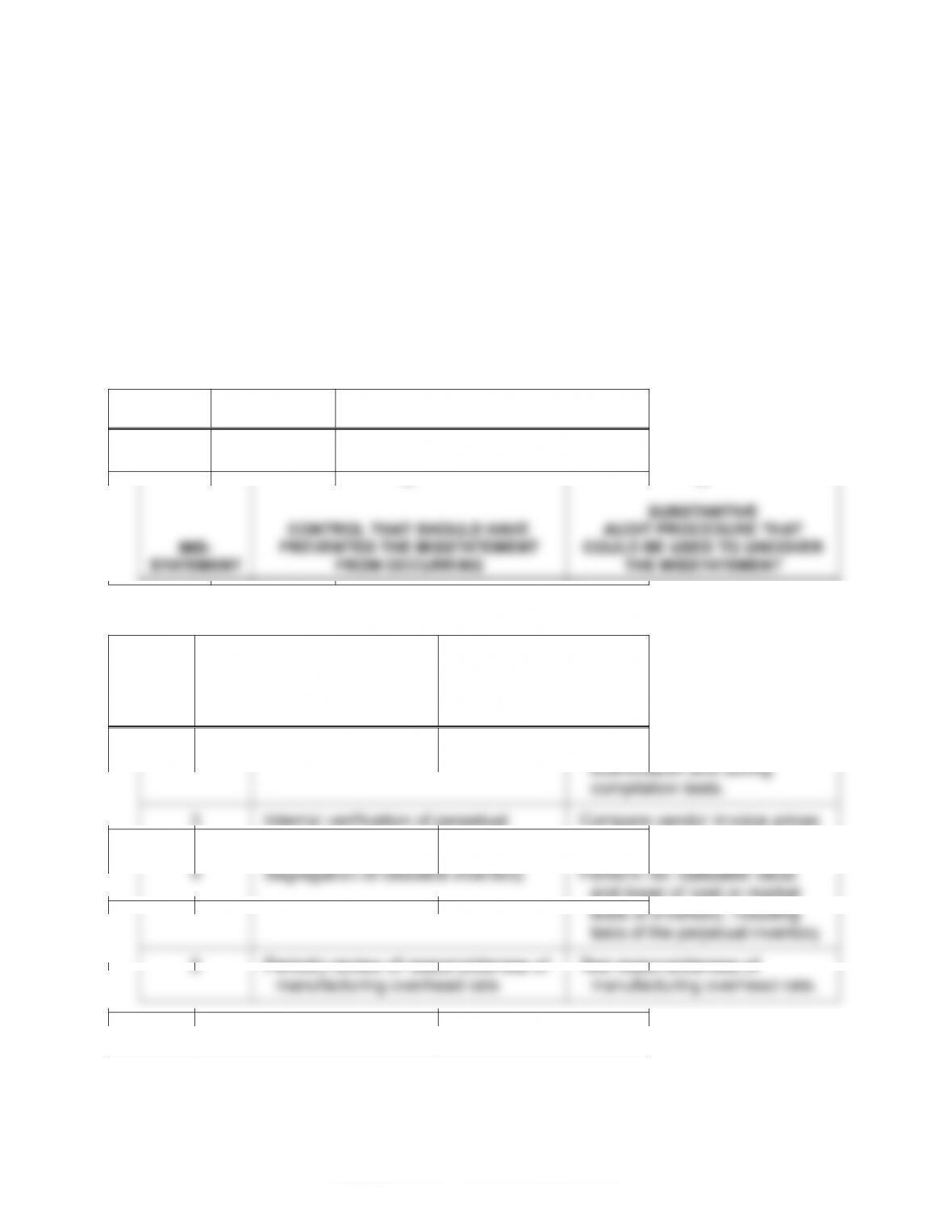

6

Substantive Test

To test that the final inventory was valued at its

proper cost. (Accuracy)

7

Test of Control

To ensure that no raw material was issued

without proper approval. (Existence)

8

Test of Control

or

Substantive Test

To ensure that additions recorded on the finished

goods perpetual records were recorded on the

books as completed production. (Accuracy and

classification)

21-20

MIS-

STATEMENT

a.

CONTROL THAT SHOULD HAVE

PREVENTED THE MISSTATEMENT

FROM OCCURRING

b.

SUBSTANTIVE

AUDIT PROCEDURE THAT

COULD BE USED TO UNCOVER

THE MISSTATEMENT

1

Perform independent second counts

on all merchandise. All persons

responsible for inventory tags and

compilation of physical inventory

should be independent of custody

of perpetual inventory records.

Record test counts and trace to

compiled inventory.

2

Use of prenumbered tags and

accounting for numerical sequence.

Account for all prenumbered

tags during the physical

examination and during

compilation tests.

3

Internal verification of perpetual

inventory prices.

Compare vendor invoice prices

to perpetual inventory prices.

4

Segregation of obsolete inventory.

Perform net realizable value

and lower of cost or market

tests of inventory, including

tests of the perpetual inventory.

5

Periodic review of reasonableness of

manufacturing overhead rate.

Test reasonableness of

manufacturing overhead rate.

21-20 (continued)

MIS-

STATEMENT

a.

CONTROL THAT SHOULD HAVE

PREVENTED THE MISSTATEMENT

FROM OCCURRING

b.

SUBSTANTIVE

AUDIT PROCEDURE THAT

COULD BE USED TO UNCOVER

THE MISSTATEMENT

6

Internal verification by another

person.

Examine vendors’ invoices in

support of prices used.

7

Keep a record of the last shipping

report number shipped before the

inventory count.

Examine bills of lading for first

shipments recorded after the

physical inventory to determine

that they were shipped after

year-end.

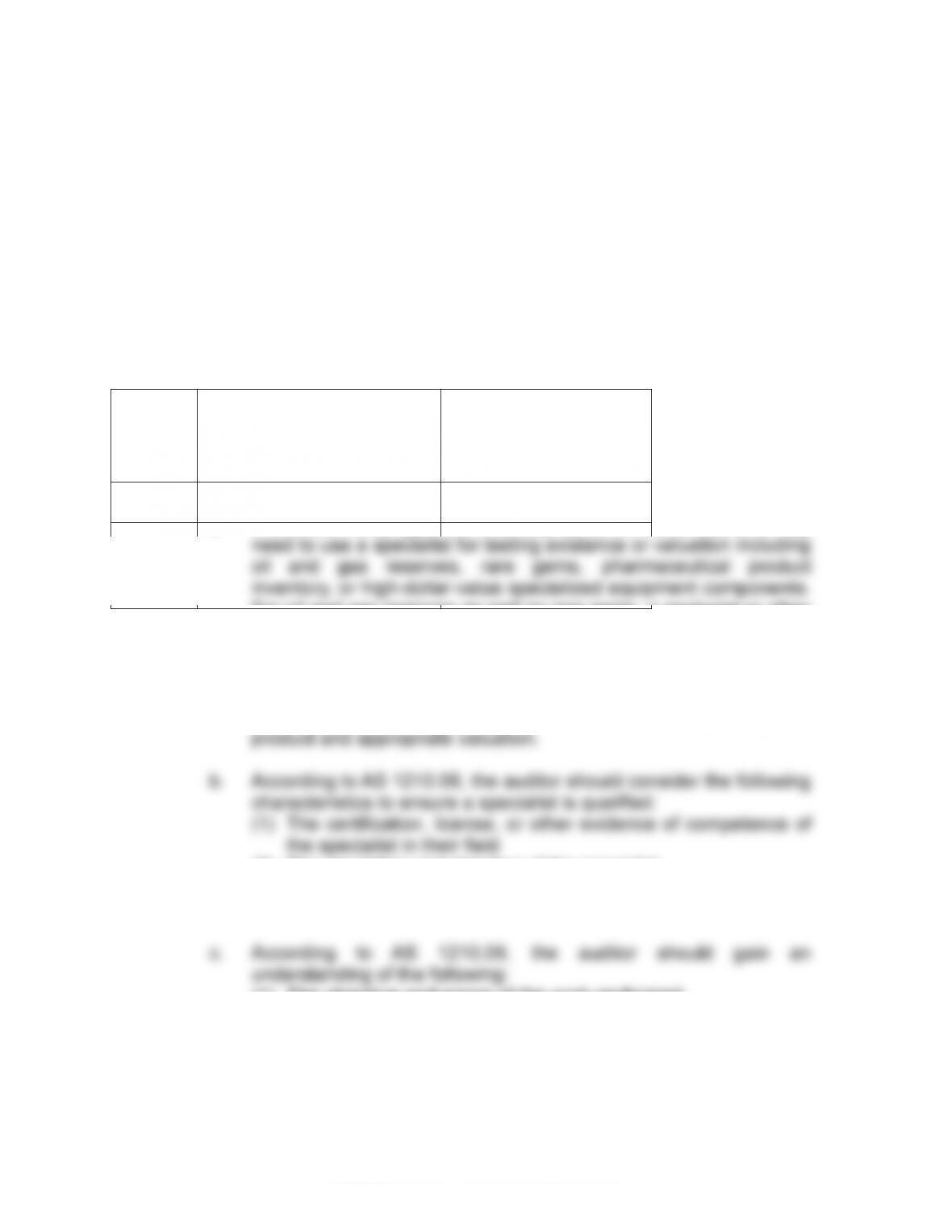

21-21 Note: The PCAOB reorganized their auditing standards effective

December 31, 2016. PCAOB AU Section 336 is identified in the

reorganized standards as AS 1210.

a. There are many types of inventory items for which auditors may

need to use a specialist for testing existence or valuation including

oil and gas reserves, rare gems, pharmaceutical product

b. According to AS 1210.08, the auditor should consider the following

characteristics to ensure a specialist is qualified:

(1) The certification, license, or other evidence of competence of

c. According to AS 1210.09, the auditor should gain an

understanding of the following:

(1) The objective and scope of the work performed

21-14

21-21 (continued)

(4) A comparison of the methods and assumptions to those used

in prior periods, if relevant

d. According to AS 1210.10-1210.11, an auditor may rely on work

performed by a specialist hired by the client; however, in all cases

the auditor should ensure that the specialist can be objective in

21-22 a.

INTERNAL CONTROLS

TESTS OF CONTROLS

1.

Inventory purchases are used

to update the perpetual

Atlanta inventory records.

Trace inventory quantities for a sample of

purchase transactions to the perpetual

inventory records as a part of tests of

controls and substantive tests of

acquisition transactions.

2.

Transfers of inventory are used

to update the Atlanta and local

distribution center perpetual

inventory records.

Trace inventory quantities for a sample of

shipments from Atlanta to local

distribution centers to the perpetual

inventory records.

3.

Inventory sales are used to

update the local distribution

center perpetual inventory

records.

Trace inventory quantities for a sample of

sales transactions to the perpetual

inventory records as a part of tests of

controls and substantive tests of sales

transactions.

4.

Local distribution centers

access to perpetual records is

restricted to processing sales

transactions.

Test the effectiveness of the perpetual

records access restrictions using the CPA

firm’s computer audit specialists.

5.

Quarterly physical inventory is

taken for comparison to and

adjustment of perpetual

records.

Examine local distribution center physical

inventory count records and adjustments

to the perpetual records.

21-15

21-22 (continued)

INTERNAL CONTROLS

TESTS OF CONTROLS

6.

Internal auditors test the

perpetual records

continuously.

Examine internal auditor audit programs

and working papers for their tests of the

perpetual records and the findings.

7.

Internal auditors sample

inventory counts and test

inventory adjustments.

Examine internal auditor audit programs

and working papers for their tests of the

physical observation of inventory and the

findings.

these to use.

counting and do test counts of inventory.

counting at each location.

3. Reduce the sample sizes for test counts inventory.

4. Perform the physical observation of inventory at an interim

date.

21-23 a.

INVENTORY

DESCRIPTION

UNITS

ON

HAND

DOLLARS

NUMBER

OF UNITS

REQUIRING

FLOOR

SPACE

PER UNIT

REQUIRED

SQ.

FOOTAGE

TOTAL SQ.

FOOTAGE

REQUIRED

TO STORE

INVENTORY

(Units x Sq ft)

AC Unit – Model 635

1240

$806,000

413.333a

16

6613.33

AC Unit – Model 770

1733

$1,940,960

577.667a

16

9242.67

Furnace – Model 223

1992

$2,589,600

996b

16

15936.00

Furnace – Model 225

2008

$2,761,000

1004b

16

16064.00

Air Handling Ducts

11883

$1,485,400

2970.75c

25

74,268.75

$9,582,960

122,124.75

a 2 pallets of AC units sit on top of 1 pallet that rests on the floor (1240/3 = 413.333; 1733/3 =

577.667).

b 1 furnace can sit on top of the unit that rests on the floor (1992/2 = 996; 2008/2 = 1004) .

c 3 boxes can be stored on top of the box that rests on the floor (11883/4 = 2971) .

21-16

21-23 (continued)

substantive tests to examine the existence of inventory at year

end.

21-24 a. The auditor in this situation should observe the recording of the

b. 1. There is no clear-cut answer to sample size for inventory

counts. The answer to the question depends on additional

factors, such as the randomness of your test counts and

whether the values of the merchandise are relatively stratified.

c. The auditor should determine how this inventory is valued and

after discussion with the client it may be determined to classify

it as obsolete. In all cases, the auditor must specifically identify

the merchandise in the working papers for subsequent

the inventory.

d. One of the important tasks the auditor undertakes during the

observation is to determine that inventory tags are physically

controlled. This assures that the inventory is not understated

21-25

CLIENT

a.

ISSUES

TO CONSIDER

b.

LOCATIONS TO VISIT

c.

POTENTIAL RISKS

OF MATERIAL

MISSTATEMENT

d.

AUDITOR

RESPONSES

TO RISKS

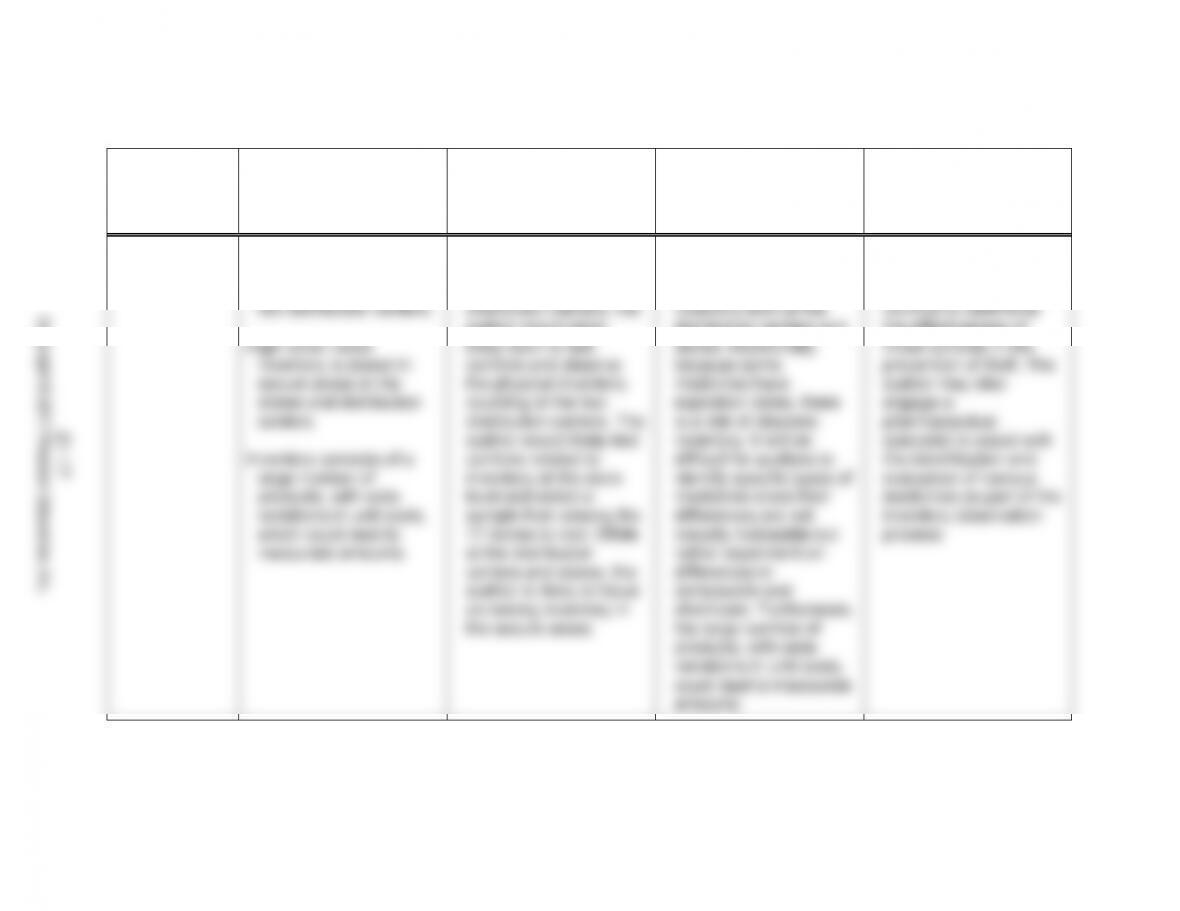

1. Colburn

Pharmacy

A majority of the inventory

amount on the balance

sheet is located at the

two distribution centers.

High dollar value

inventory is stored in

secure areas at the

stores and distribution

centers.

Inventory consists of a

large number of

products, with wide

variations in unit costs,

which could lead to

inaccurate amounts.

Given the significance of

the value of inventory

located in the

distribution centers, the

auditor would most

likely want to test

controls and observe

the physical inventory

counting at the two

distribution centers. The

auditor would likely test

controls related to

inventory at the store

level and select a

sample from among the

77 stores to visit. While

at the distribution

Due to the high cost and

demand for medicines,

there is a risk of theft of

inventory both at the

distribution centers and

stores. Additionally,

because some

medicines have

expiration dates, there

is a risk of obsolete

inventory. It will be

difficult for auditors to

identify specific types of

medicines since their

differences are not

visually noticeable but

rather dependent on

The auditor will likely

focus extensively on

inventory management

controls to determine

the effectiveness of

those controls in the

prevention of theft. The

auditor may also

engage a

pharmaceutical

specialist to assist with

the identification and

evaluation of various

medicines as part of the

inventory observation

process.

21-17

Copyright © 2017 Pearson Education, Inc.

21-25 (continued)

CLIENT

a.

ISSUES

TO CONSIDER

b.

LOCATIONS TO VISIT

c.

POTENTIAL RISKS

OF MATERIAL

MISSTATEMENT

d.

AUDITOR

RESPONSES

TO RISKS

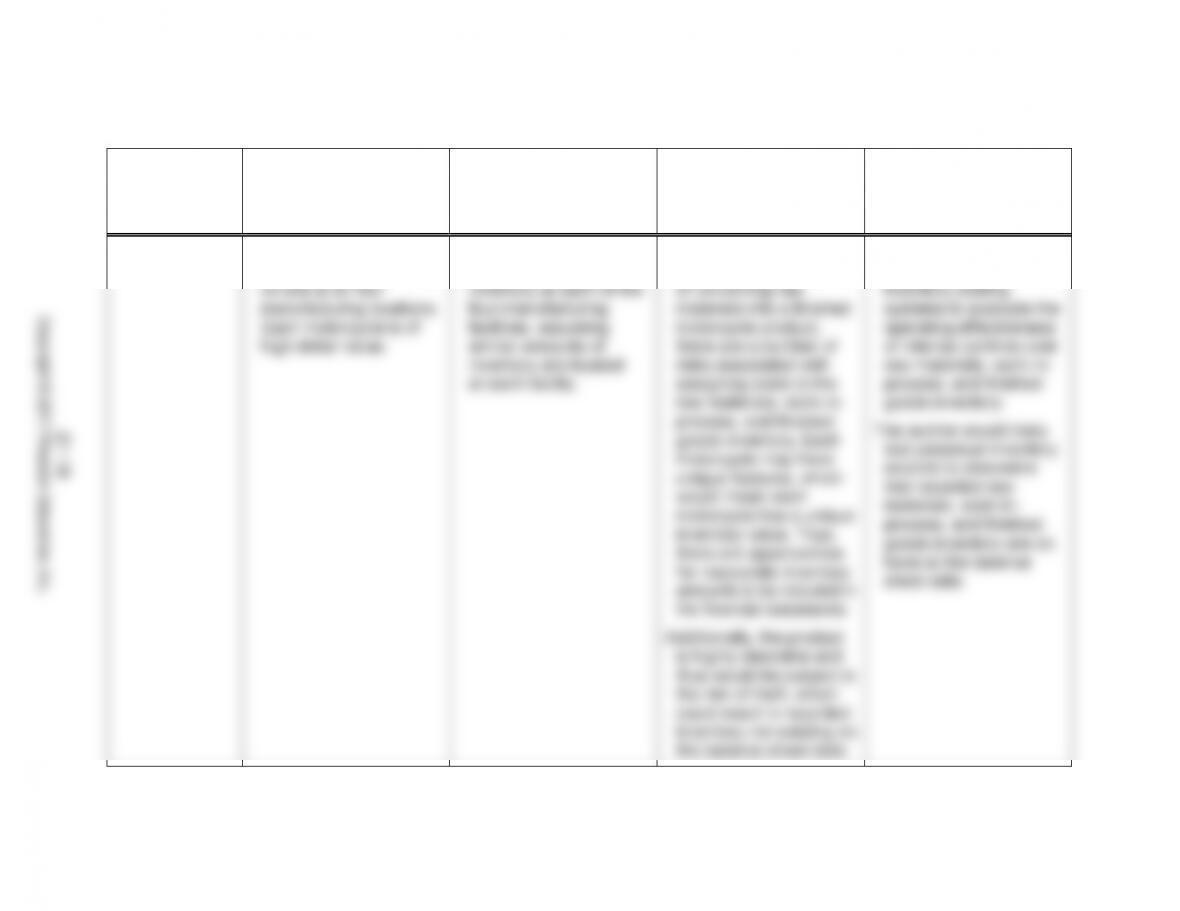

2. Zenith, Inc.

Material amounts of

inventory are most likely

on site at all four

manufacturing locations.

Each motorcycle is of

high dollar value.

Most likely the auditor

would want to inspect

inventory at each of the

four manufacturing

facilities, assuming

similar amounts of

inventory are located

at each facility.

Because of the

manufacturing process

of converting raw

materials into a finished

motorcycle product,

there are a number of

risks associated with

assigning costs to the

raw materials, work-in-

process, and finished

goods inventory. Each

motorcycle may have

unique features, which

would mean each

motorcycle has a unique

inventory value. Thus,

The auditor would want

to extensively test

inventory costing

systems to evaluate the

operating effectiveness

of internal controls over

raw materials, work-in-

process, and finished

goods inventory.

The auditor would likely

test perpetual inventory

records to determine

that recorded raw

materials, work-in-

process, and finished

21-18

Copyright © 2017 Pearson Education, Inc.

21-25 (continued)

CLIENT

a.

ISSUES

TO CONSIDER

b.

LOCATIONS TO VISIT

c.

POTENTIAL RISKS

OF MATERIAL

MISSTATEMENT

d.

AUDITOR

RESPONSES

TO RISKS

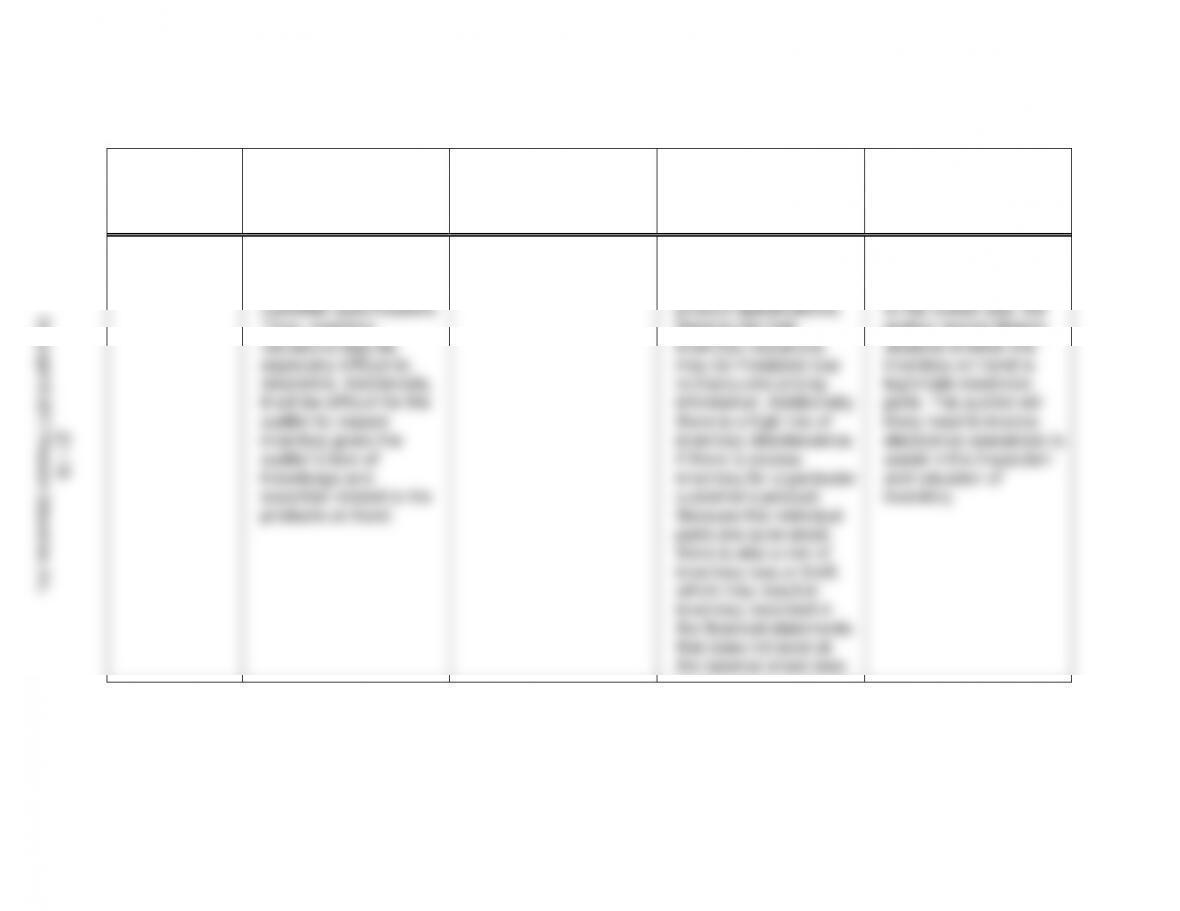

3. Texide

Electronics

Inventory items are

unique, given that they

are dependent on

customer specifications.

Thus, inventory

valuations may be

especially difficult to

determine. Additionally,

it will be difficult for the

auditor to inspect

inventory given the

auditor’s lack of

knowledge and

expertise related to the

products on hand.

All inventory is located

at one manufacturing

facility.

Because the client’s

inventory is customized

to their customers’

product specifications,

there is risk that

inventory valuations

may be misstated due

to inaccurate pricing

information. Additionally,

there is a high risk of

inventory obsolescence,

if there is excess

inventory for a particular

customer’s product.

Because the individual

parts are quite small,

there is also a risk of

inventory loss or theft,

inventory recorded in

Because the interior

components of the

product are not visible

to the human eye, the

auditor cannot directly

observe whether the

inventory on hand is

legitimate electronic

parts. The auditor will

likely need to involve

electronics specialists to

assist in the inspection

and valuation of

inventory.

21-19

Copyright © 2017 Pearson Education, Inc.