7-1

Chapter 7

Audit Evidence

Concept Checks

P. 192

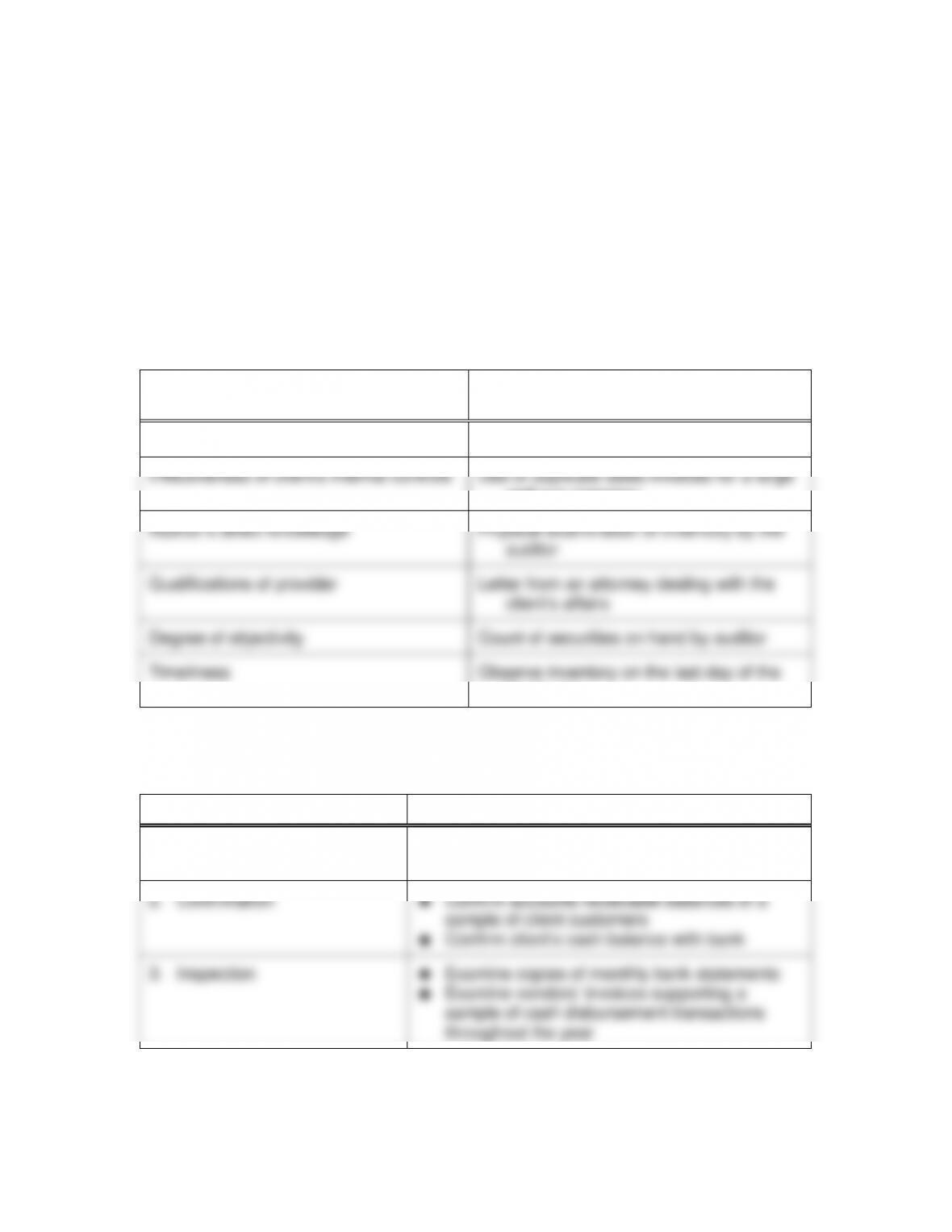

1. Following are six characteristics that determine reliability of evidence and an

example of each.

FACTOR

DETERMINING RELIABILITY

EXAMPLE OF

RELIABLE EVIDENCE

Independence of provider

Confirmation of a bank balance

Effectiveness of client’s internal controls

Use of duplicate sales invoices for a large

well-run company

Auditor’s direct knowledge

Physical examination of inventory by the

auditor

Qualifications of provider

Letter from an attorney dealing with the

client’s affairs

Degree of objectivity

Count of securities on hand by auditor

Timeliness

Observe inventory on the last day of the

fiscal year

2. The eight types of evidence and examples of each are included in the table

below.

TYPES OF AUDIT EVIDENCE

EXAMPLES

1. Physical examination

Count inventory in warehouse

Examine fixed asset additions

2. Confirmation

Confirm accounts receivable balances of a

sample of client customers

Confirm client’s cash balance with bank

3. Inspection

Examine copies of monthly bank statements

Examine vendors’ invoices supporting a

sample of cash disbursement transactions

throughout the year

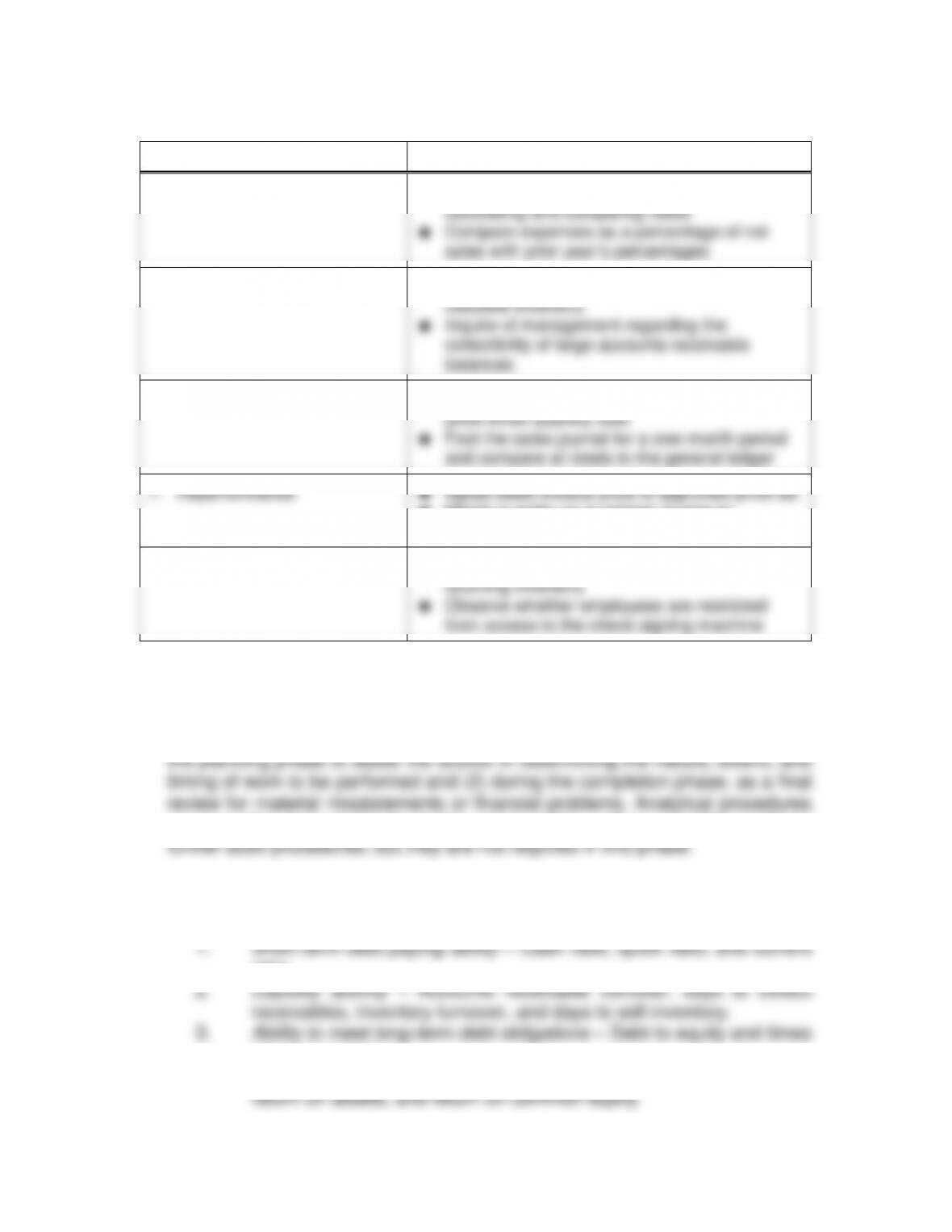

Concept Check, P.192 (continued)

TYPES OF AUDIT EVIDENCE

EXAMPLES

4. Analytical procedures

Evaluate reasonableness of receivables by

calculating and comparing ratios

Compare expenses as a percentage of net

sales with prior year’s percentages

5. Inquiries of the client

Inquire of management whether there is

obsolete inventory

Inquire of management regarding the

collectibility of large accounts receivable

balances

6. Recalculation

Recompute invoice total by multiplying item

price times quantity sold

Foot the sales journal for a one-month period

and compare all totals to the general ledger

7. Reperformance

Agree sales invoice price to approved price list

Match quantity on purchase invoice to

receiving report

8. Observation

Observe client employees in the process of

counting inventory

Observe whether employees are restricted

from access to the check signing machine

P. 199

1. Analytical procedures are required during two phases of the audit: (1) during

are also often done during the testing phase of the audit as part of the auditor’s

2. The four categories of financial ratios and examples of ratios in each

category are as follows:

ratio.

interest earned.

4. Profitability – Earnings per share, gross profit percent, profit margin,

7-3

P. 206

1. The purposes of audit documentation are as follows:

To provide a basis for planning the audit. The auditor may use

To provide a record of the evidence accumulated and the results of

To provide data for deciding the proper type of audit report. Data are

To provide a basis for review by supervisors and partners. These

Audit documentation is used for several purposes, both during the audit

and after the audit is completed. One of the uses is the review by more

experienced personnel. A second is for planning the subsequent year audit. A

third is to demonstrate that the auditor has accumulated sufficient appropriate

2. Audit schedules should include the following:

Name of the client. Enables the auditor to identify the appropriate file

Period covered. Enables the auditor to identify the appropriate year to

Description of the contents. A list of the contents enables the reviewer

to determine whether all important parts of the audit schedule have

Initials of the preparer. Indicates who prepared the audit schedule in

case there are questions by the reviewer or someone who wants

7-4

Concept Check, P.206 (continued)

schedules.

Indexing. Helps in organizing and filing audit schedules. Indexing

Review Questions

guilt of a defendant in a legal case must be proven beyond a reasonable doubt.

This is similar to the concept of sufficient appropriate evidence in an audit

situation. As with a judge or jury, an auditor cannot be completely convinced that

his or her opinion is correct, but rather must obtain a high level of assurance.

7-2 The four major audit evidence decisions that must be made on every audit

are:

1. Which audit procedures to use.

4. When to perform the procedure.

7-3 An audit procedure is the detailed instruction for the collection of a type

of audit evidence that is to be obtained. Because audit procedures are the

7-5

7-4 An audit program for accounts receivable is a list of audit procedures that

statements are correct:

1. The cost of accumulating evidence. It would be extremely costly for

2. Evidence is normally not sufficiently reliable to enable the auditor to

7-6 The two determinants of the persuasiveness of evidence are appropriateness

and sufficiency. Appropriateness refers to the relevance and reliability of evidence,

or the degree to which evidence can be considered believable or worthy of trust.

7-7 The characteristics of a confirmation are:

1. Receipt directly by auditor

2. Written or electronic response

to-day operation of the business.

7-8 Internal documentation is prepared and used within the client’s organization

without ever going to an outside party, such as a customer or vendor.

Examples:

check request form

receiving report

7-6

7-8 (continued)

Examples:

vendor’s invoice

cancelled check

following:

1. Understanding the client’s business and industry

2. Assessment of the entity’s ability to continue as a going concern

procedures, but they are not required in this phase.

7-11 Attention-directing analytical procedures occur when significant, unexpected

differences are found between current year’s unaudited financial data and other

substantive tests.

Substantive analytical procedures are designed to reduce or eliminate

detailed substantive tests. The effectiveness of an analytical procedure in

7-7

7-12 (continued)

assessing the risk of material misstatements.

7-13 Liquidity activity ratios, such as accounts receivable turnover, days to

collect receivables, inventory turnover, and days to sell inventory, provide

information about how long it takes a company to convert less-liquid current

7-14 Audit files are owned by the auditor. They can be used by the client if the

auditor wants to release them after a careful consideration of whether there might

be confidential information in them. The audit files can be subpoenaed by a court

and thereby become the property of the court. They can be released to another

7-15 The Sarbanes–Oxley Act of 2002 requires auditors of public companies to

1. Articles of incorporation

2. Bylaws, bond indentures, and contracts

3. Analysis of accounts that have continuing importance to the auditor

By separating this information from the current year’s audit files, it becomes

7-17 The purpose of an analysis is to show the activity in a general ledger

account during the entire period under audit, tying together the beginning and

ending balances. The trial balance includes the detailed makeup of an ending

7-18 Unanswered questions and exceptions may indicate the potential for

presented.

The audit files can also be subpoenaed by courts as legal evidence.

was done and by whom.

7-20 The purposes of audit engagement management software are to convert

traditional paper-based documentation into electronic files and to organize the

audit documentation, and help manage the engagement. The benefits of

engagement management software are as follows:

The effects of adjusting journal entries are automatically carried

through to the trial balance and financial statements, making last–

minute adjustments easier to make.

package after the audit is completed.

Multiple Choice Questions From CPA Examinations

7-21 a. (2) b. (4) c. (4)

7-22 a. (1) b. (4) c. (2)

7-23 a. (3) b. (3) c. (4)

7-9

7-24 a. (4) b. (2) c. (1)

Discussion Questions And Problems

7-25 a. 1. Internal 7. External 13. Internal

2. Internal 8. External 14. Internal

they are still internal documents.

** Bills of lading are ordinarily signed by the freight company.

the conditions stated on the document.

7-26

1. (4) analytical procedures

2. (5) inquiries of client

3. (3) inspection

4. (2) confirmation

5. (6) recalculation

6. (1) physical examination

7-27

ACCOUNT

NAME

FROM WHOM

CONFIRMED

INFORMATION

TO BE CONFIRMED

CASH IN BANK

All banks in which Star

had deposits during the

year, including those

which may have had an

account that was closed

out during the year.

Name and address of the bank.

The amount on deposit for each

account as of the balance sheet date

plus the name of each account, the

account number, whether or not the

account is subject to withdrawal by

check, and the interest rate if the

account is interest bearing.

The amount for which Star was

directly liable to the bank for loans

as of the balance sheet date plus the

date of the loan, the due date, the

interest rate, the date to which interest

is paid, and description of the liability

and collateral.

If internal controls over cash are

deficient, the auditor may wish to

request that the bank include a list

of authorized signatures with the

confirmation.

TRADE

ACCOUNTS

RECEIVABLE

A representative sample

of debtors at a selected

confirmation date which

may be either at the

balance sheet or an

interim date.

Confirmations should

also be requested for

the following types of

accounts:

Accounts with large

balances;

The confirmation can be either a positive

or negative form of request. The positive

form requests the debtor to directly

notify the auditor whether the

information is correct and, if not correct,

which items are considered incorrect.

The negative form requests a reply only

if the information is incorrect. In both

cases the information should include:

Name and address of the debtor.

Account number (if applicable).

The confirmation “as of” date.