A high detection risk equates to a low amount of audit evidence needed.

CPA firms are required to be independent when performing any professional service.

For each significant internal control deficiency identified by the auditor, he or she

should design one or more tests of controls to assess the extent of the deficiency and its

effect on the financial statements.

The auditor’s audit objectives follow and are closely related to management assertions.

Government auditing standards are included in the Yellow Book.

When an auditor relies upon a different CPA firm to perform part of the audit and

chooses to issue a shared opinion, only the auditor’s responsibility paragraph should be

modified.

When verifying the transfer of inventory from one location to another, the audit

objectives with which the auditor is primarily concerned are occurrence of recorded

transfers, completeness of recorded transfers, and accuracy of recorded transfers.

The assessment of control risk does not impact the testing of controls.

Audit assurance is the complement of planned detection risk, that is, one minus planned

detection risk.

The auditor should perform procedures to verify the addresses used for the accounts

receivable confirmations.

Auditors must maintain control of confirmations until they are returned from the

customer.

Companies may purchase marketable securities as a way to temporarily invest excess

cash.

Sampling risk results if the sample accurately represents the population.

Controls that relate to a specific use of the IT system, such as the processing of sales or

cash receipts, are called application controls.

Auditors typically test details of account balances in the audit of payroll.

Examining the minutes of the board of directors’ meetings for proper authorization

ordinarily tests the existence objective for capital stock transactions.

The defense of contributory negligence by a third party is often used by auditors if

charged with a violation of the 1934 Securities Act.

Confirmations are ordinarily used to verify account balances, but may be used to verify

transactions.

Materiality does not depend on the decisions of users who rely on the statements to

make the decisions.

Many of the auditor’s audit procedures in the audit of cash center around the client’s

bank confirmations.

The only way to know with certainty whether a sample is representative is to

subsequently audit the entire population.

A predecessor auditor who has been contacted by a successor auditor for information

about the client does not have to obtain permission from the former client before

providing any confidential information to the successor auditor because the

confidentiality requirement does not extend to former clients.

The broadest interpretation of the right of third-party beneficiaries is the primary user

concept.

The most important benefits of industry comparisons are to aid in understanding the

client’s business and as an indication of the likelihood of financial failure.

The audit procedure “Foot the inventory listing schedules for raw materials,

work-in-process, and finished goods” provides assurance mainly for the accuracy

objective for inventory pricing and compilation.

One criteria used by an external auditor to evaluate published financial statements is

known as generally accepted auditing standards.

The accuracy of a dividend declaration can be audited by recalculating the amount on

the basis of the dividend per share times the number of shares outstanding.

The population standard deviation has a significant effect on the computed precision

interval.

After the auditor is satisfied with the allowance for uncollectible accounts, it is easy to

verify bad debt expense.

The issuance of bonds by the client subsequent to the balance sheet date would require

a footnote disclosure in, but no adjustment to, the financial statements under audit.

Because of the importance of tests of controls and substantive tests of transactions for

acquisitions and cash disbursements, attributes sampling is commonly used when

testing the acquisitions and cash disbursements cycle.

The physical observation of the inventory and the acquisition of raw materials are part

of the inventory and warehousing cycle.

A high inherent risk increases planned detection risk and decreases planned substantive

tests.

A bill of lading is a written contract between the seller and the buyer.

A set of records for each piece of equipment that includes descriptive information, date

of acquisition, original cost, current year depreciation, and accumulated depreciation is

the

A) acquisitions schedule.

B) depreciation schedule.

C) fixed asset master file.

D) file of purchase requisitions.

The following situations involve a possible violation of the AICPA’s Code of

Professional Conduct. For each situation, 1/ determine the applicable rule from the

Code, 2/ decide whether or not the Code has been violated, and 3/ briefly explain how

the situation violates (or does not violate) the Code.

a. Howard Cunningham & Co., CPAs, designates its firm as “Members of the American

Institute of Certified Public Accountants.” All of the partners of the firm are CPAs.

However, one of the partners has recently chosen to allow her membership to lapse

because of personal reasons.

Rule: ________ Violation? Yes No

Explanation:

b. Brad Long, CPA, was traveling from Orlando to Miami, Florida when he was pulled

over by a police officer on suspicion of driving under the influence. He was convicted

in court of driving while under the influence of alcohol. Because of past convictions,

Brad was sentenced to 5 years in prison.

Rule: ________ Violation? Yes No

Explanation:

c. Kelley Brent, CPA, is a partner in a one-office CPA firm that audits Dane, Inc., a

closely held corporation. Kelley’s sister was recently appointed as the chief financial

officer for Dane, Inc.

Rule: ________ Violation? Yes No

Explanation:

d. Sarah Martin, CPA, is a senior auditor in the San Francisco office of Cooper &

Howell, CPAs. Sarah’s father is employed as the controller of Line Electronics, a public

company in Detroit, Michigan. Line Electronics is one of the firm’s audit clients.

Neither Sarah nor the San Francisco office is involved in the audit of Line Electronics.

Rule: ________ Violation? Yes No

Explanation:

e. On August 20, 20×7, Min Lee, CPA and partner, was offered and accepted the

engagement to audit the annual financial statements of Jernigan Corporation for the

year ended December 31, 20×7. Preliminary work began on the audit on September 15,

20×7 and the engagement ended on March 7, 20×8. Jernigan is regulated by the SEC.

Min served as controller of Jernigan Corporation from December 1, 20×2, until April

10, 20×7, at which time she terminated her employment with Jernigan.

Rule: ________ Violation? Yes No

Explanation:

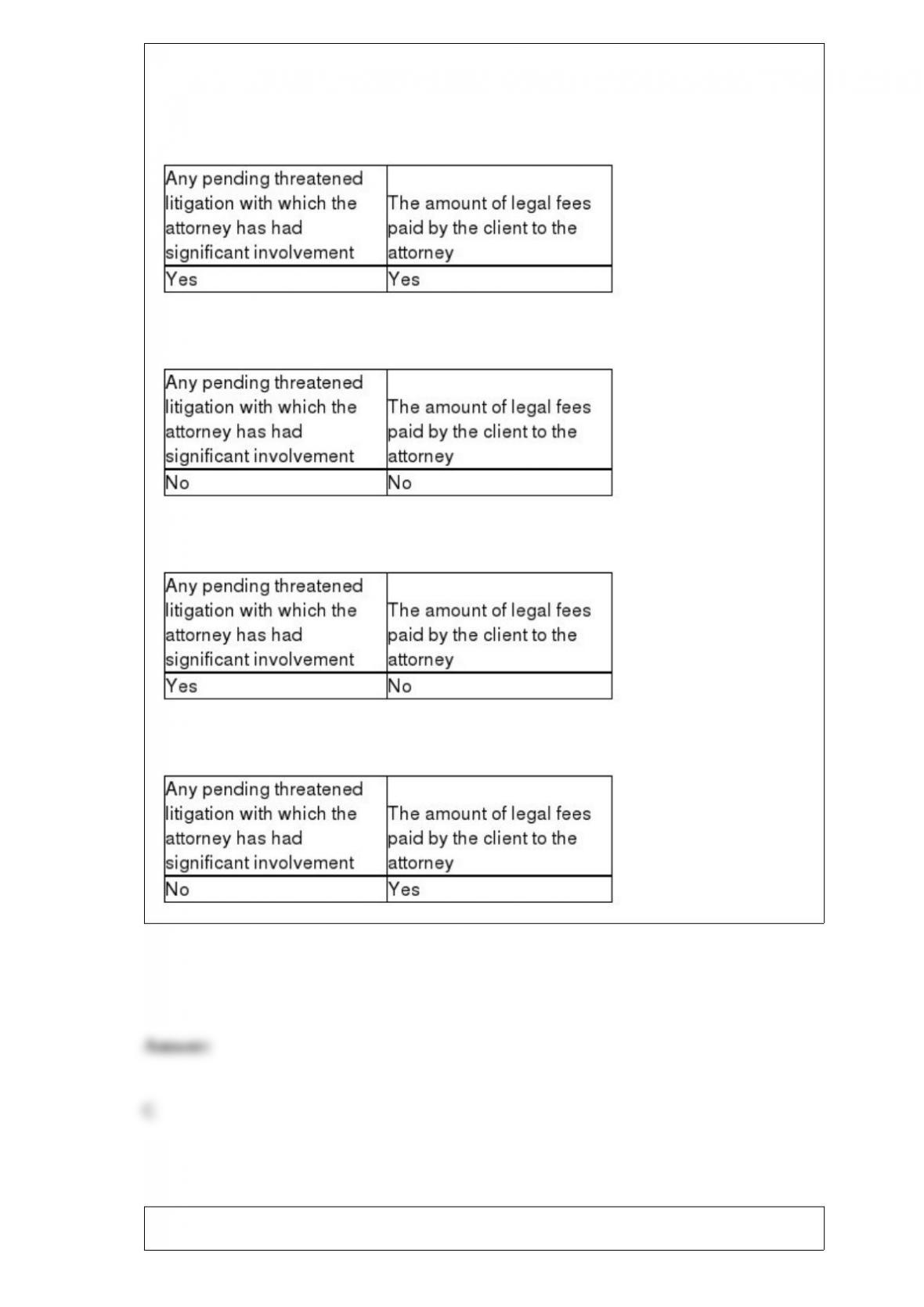

What needs to be included in a standard inquiry to the client’s attorney letter sent to a

client’s legal counsel?

A)

B)

C)

D)

Which of the following is a factor that relates to incentives/pressures to misappropriate

assets?

A) weak internal controls

B) significant personal financial obligations

C) management’s practice of making overly aggressive forecasts

D) anger and fear

Which of the following is most correct when using audit sampling for exception rates?

A) The auditor is concerned with the lowest rate.

B) The auditor is concerned with the highest rate.

C) The auditor is concerned with the average on previous audits.

D) The auditor is not concerned with the exception rate for audits of nonpublic

companies.

Which of the following is the exception rate that the auditor expects to find before

testing?

A) sample exception rate

B) estimated population exception rate

C) computed exception rate

D) tolerable exception rate

The record of the outstanding shares at any given time is maintained in the

A) corporate directory.

B) stock certificate books.

C) schedule of stock owners.

D) shareholders’ capital stock master file.

The detail tie-in objective is not concerned that the details in the account balance

A) agree with related subsidiary ledger amounts.

B) are properly disclosed in accordance with GAAP.

C) foot to the total in the account balance.

D) agree with the total in the general ledger.

Which of the following is an accurate statement regarding the risk assessment process

of phase I of the audit process for the sales and collection cycle?

A) Auditors must perform substantive tests related to assertions deemed to have

significant risks.

B) The auditor must relate control risk for transaction-related audit objectives to

balance-related audit objectives in deciding planned inherent risk.

C) The realizable value balance-related audit objectives are affected by assessed control

risk for classes of transactions.

D) All of the above are accurate statements.

Audit standards require the auditor to consider materiality early in the audit. Which

statement(s) regarding preliminary materiality are true?

I. Preliminary materiality may change during the engagement.

II. Preliminary materiality is the maximum amount by which the auditor believes the

financials could be misstated and still not affect the decisions of reasonable users.

A) I only

B) II only

C) both I and II

D) neither I nor II

It is important for the CPA to consider the competence of the clients’ personnel because

their competence has a direct impact upon the

A) cost/benefit relationship of the system of internal control.

B) achievement of the objectives of internal control.

C) comparison of recorded accountability with assets.

D) timing of the tests to be performed.

The total of the individual account balances in the accounts receivable master file

should equal the

A) total sales for the period.

B) balance of the sales account in the general ledger.

C) total sales less the total cash received for the period.

D) balance of the accounts receivable account in the general ledger.

Which of the following is a continuously updated computerized record of inventory

items purchased, used, sold, and on hand for merchandise, raw materials, and finished

goods?

A) job cost system

B) standard cost records

C) cost accounting records

D) perpetual inventory master file

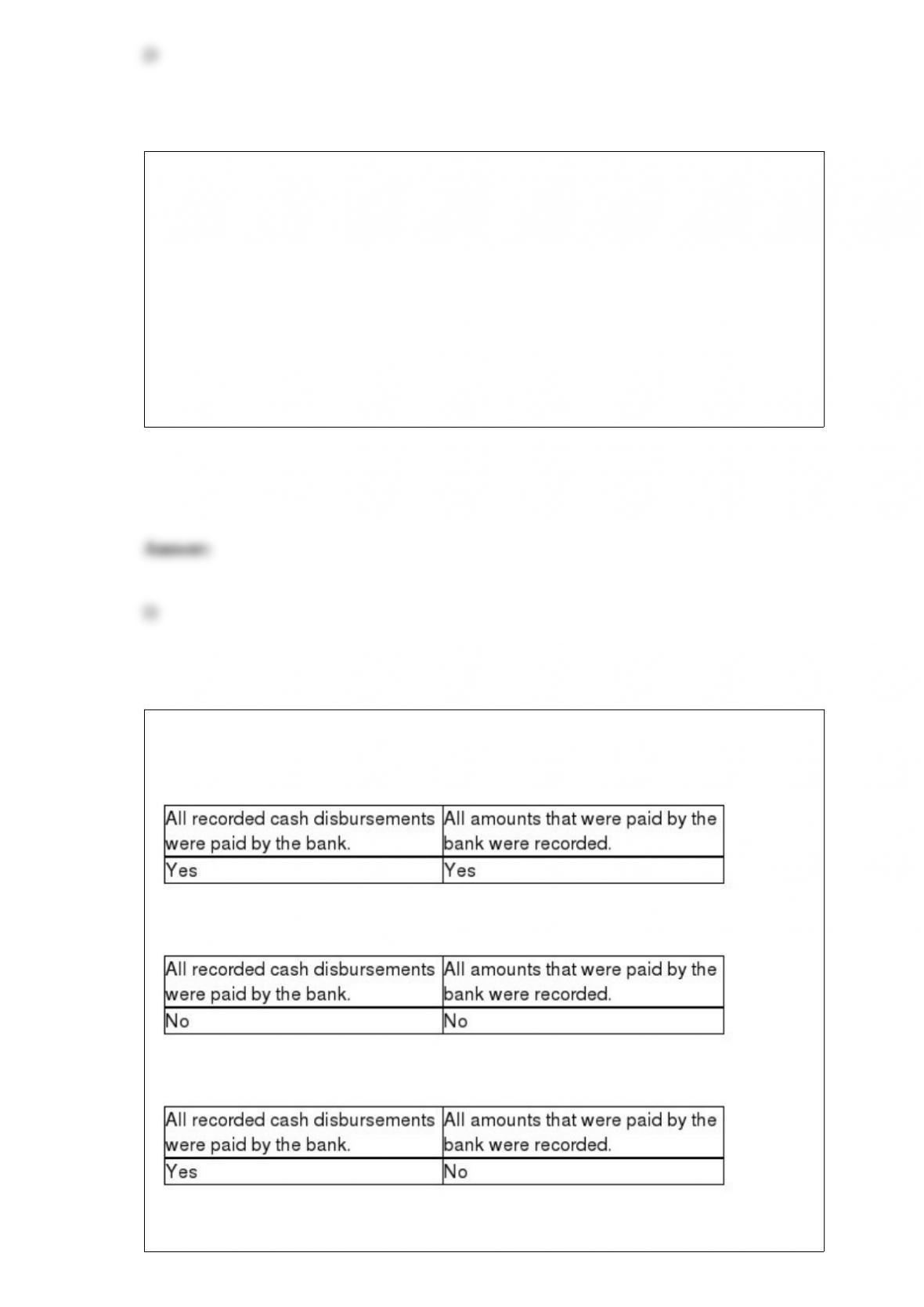

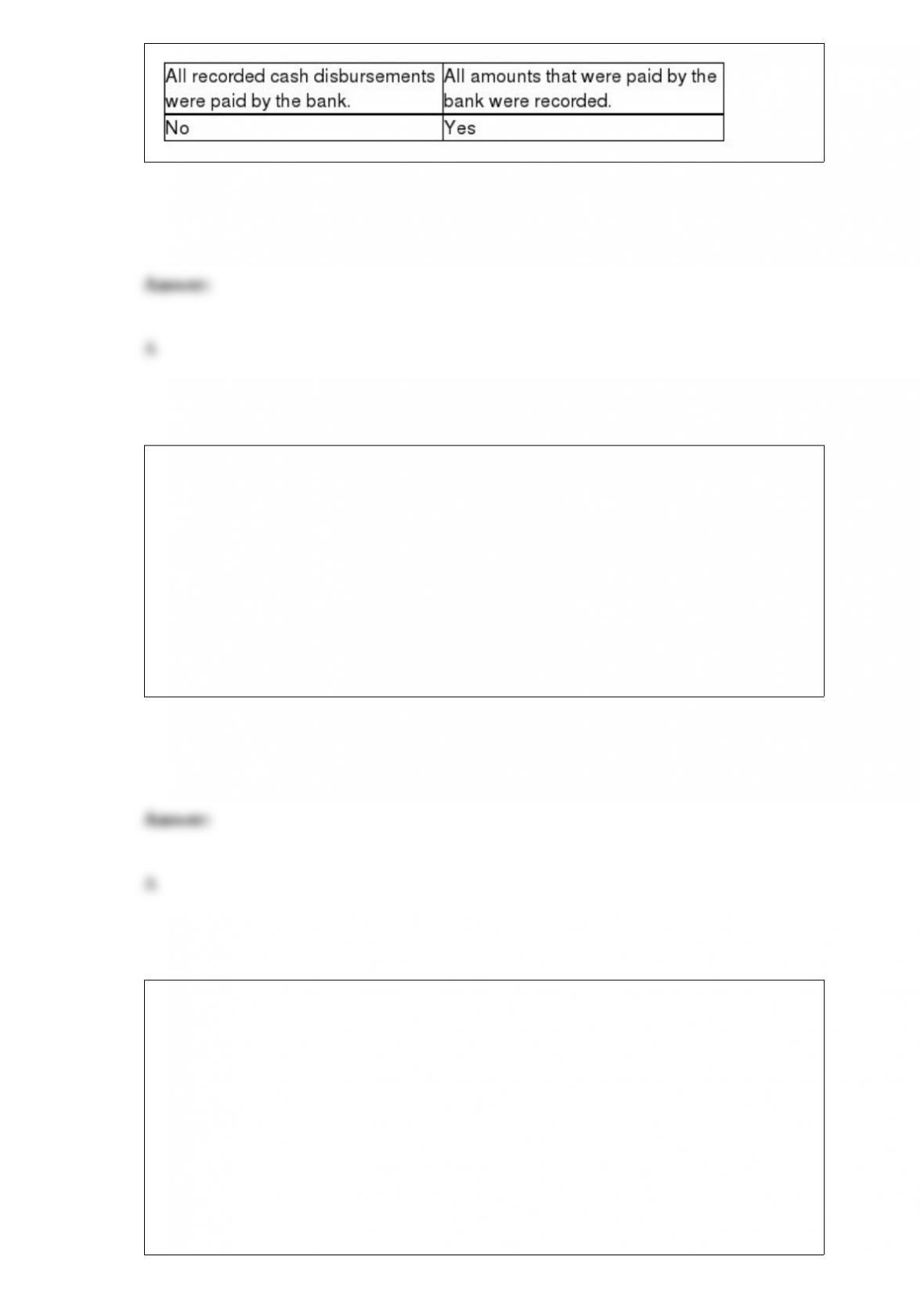

The auditor uses a proof of cash to determine whether

A)

B)

C)

D)

A ________ is a document for communicating the description, quantity, and related

information for goods ordered by a customer.

A) sales order

B) customer order

C) vendor invoice

D) sales invoice

In what order should the following steps occur?

A. Set preliminary judgment of materiality and performance materiality.

B. Understand the clients business and industry.

C. Perform preliminary analytical procedures.

D. Accept the client and perform initial audit planning.

A) D, B, C, A

B) B, A, C, D

C) B, D, A, C

D) D, C, B, A

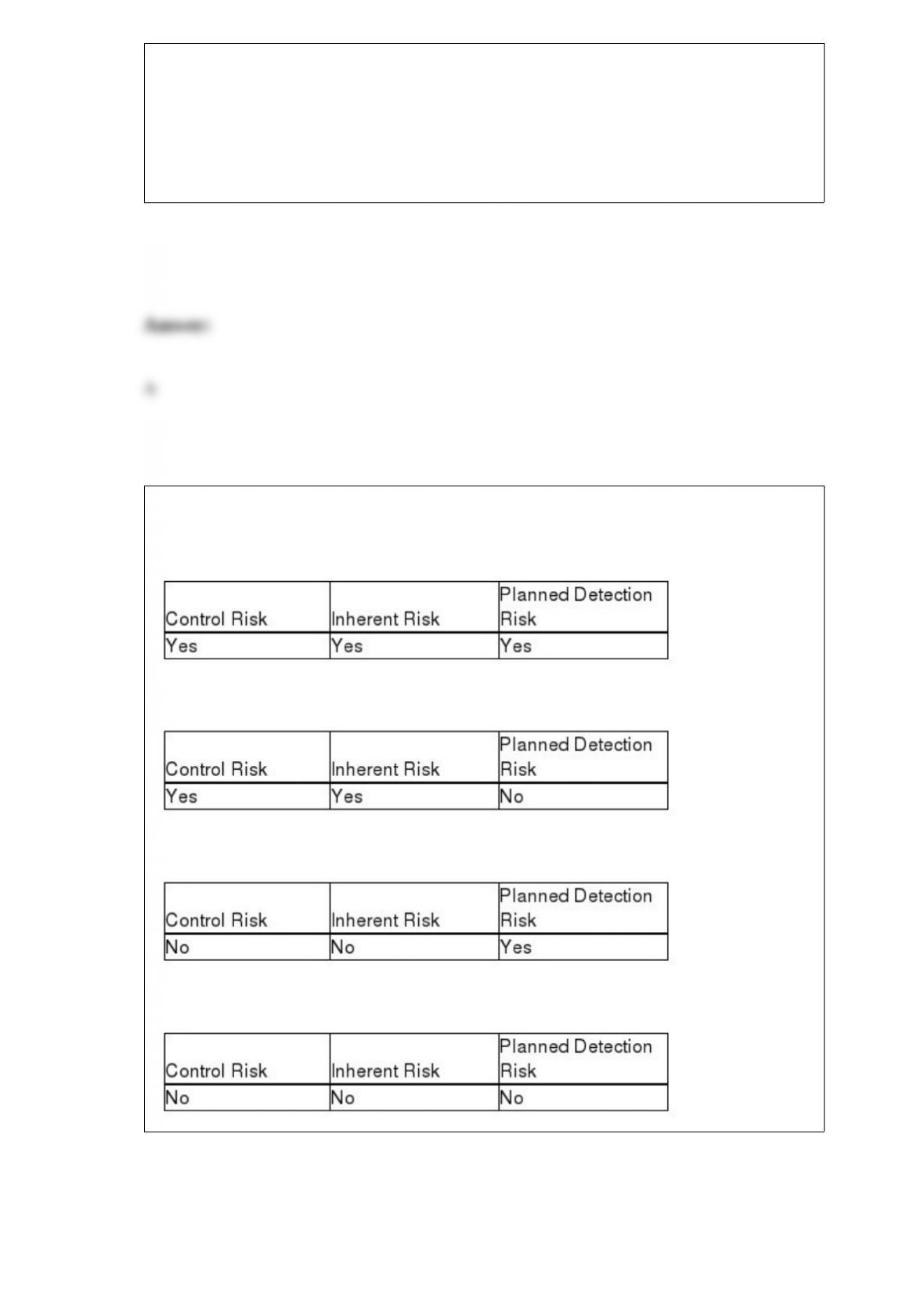

Which of the following risks are used in the audit risk model?

A)

B)

C)

D)

Which of the following is not one of the business functions for the payroll and

personnel cycle?

A) payment of payroll

B) timekeeping and payroll preparation

C) reconciliation of payroll account

D) human resources and employment

Management assertions are

A) directly related to the financial reporting framework used by the company, usually

U.S. GAAP or IFRS.

B) stated in the footnotes to the financial statements.

C) explicitly expressed representations about the financial statements.

D) provided to the auditor in the assertions letter, but are not disclosed on the financial

statements.

Insurance expense for the period is a function of which of the following?

A) the beginning prepaid balance, current premium payments and the ending prepaid

balance

B) the beginning prepaid balance and the current period premium payments

C) the current period premium payments

D) the current period premium payments and the ending prepaid balance

Analytical procedures performed during the planning phase of the audit

A) are used as a substantive test in support of account balances.

B) are used to assist in determining the nature, extent, and timing of audit procedures

C) are used to detect fraud.

D) are mandatory only for public companies.

________ is the degree to which the organization’s objectives are accomplished.

A) Effectiveness

B) Efficiency

C) Goal optimization

D) Performance

A surprise payroll payoff in which employees must pick-up and sign for their pay check

is one means of

A) identifying employees who do not have proper work credentials.

B) establishing a tightly controlled, fraud-free work environment.

C) testing for nonexistent employees.

D) identifying employees who have not submitted proper W-2 forms.

When dealing with the administration of the IT function and the segregation of IT

duties

A) in large organizations, management should assign technology issues to outside

consultants.

B) programmers should investigate all security breaches.

C) the board of directors should not get involved in IT decisions since it is a routine

function handled by middle management.

D) in complex environments, management may establish IT steering committees.

Which of the following activities is allowed for a CPA firm’s attestation clients?

A) contingent fees fixed by a court

B) commissions for referring a review client to an insurance agency for insurance

coverage

C) preparation of tax returns for which fees are based upon client refunds

D) each of the above is allowed

A measure of how willing the auditor is to accept that the financial statements may be

materially misstated after the audit is completed and an unqualified opinion has been

issued is the

A) inherent risk.

B) acceptable audit risk.

C) statistical risk.

D) financial risk.

Government Auditing Standards recognize that because of public accountability over

governmental activities the acceptable tolerable misstatement as compared to

commercial businesses may be

A) equal.

B) lower.

C) higher.

D) indeterminable.

Management makes the following assertions about account balances:

A) existence, completeness, classification and cutoff.

B) existence, accuracy, classification and rights and obligations.

C) existence, completeness, valuation and allocation, and rights and obligations.

D) existence, completeness, rights and obligations, and cutoff.

The methods used by a CPA firm to ensure that the firm meets is professional

responsibilities to clients and others is

A) continuing professional education.

B) compliance with generally accepted reporting standards.

C) quality control.

D) peer review.

Which of the following is the best way for an auditor to determine that every name on a

company’s payroll for the Rodgers factory is that of a bona fide employee presently on

the job?

A) Examine personnel records for accuracy and completeness.

B) Examine employees’ names listed on payroll tax returns for agreement with payroll

accounting records.

C) Make a surprise observation of the company’s regular distribution of paychecks.

D) Visit the working areas and confirm with employees their badge or identification

numbers.