4-24 (continued)

(a)

POTENTIAL THREATS

TO INDEPENDENCE

(b)

POSSIBLE

SAFEGUARDS?

(c)

RULES OF CONDUCT

VIOLATED?

(d)

APPROPRIATE

ACTION?

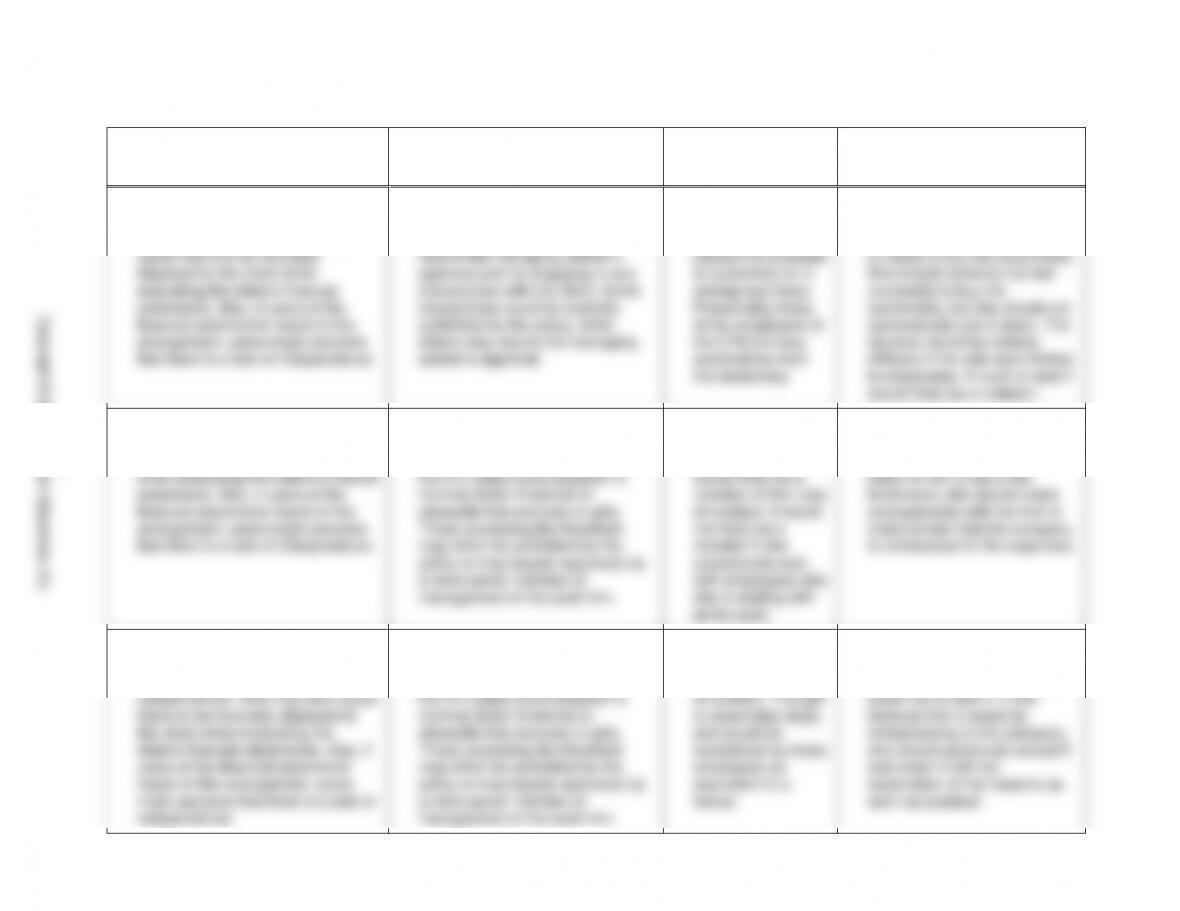

1. The ability to purchase a car at a

substantial discount due to Marie’s

long-standing audit service may

cause Marie to be favorably

disposed to the client when

evaluating the client’s financial

statements. Also, if users of the

financial statements heard of this

arrangement, some might perceive

that there is a lack of independence.

1. Marie Janes’ firm could establish

policies regarding services

provided by attest clients that

require the managing partner’s

approval prior to engaging in any

transactions with the client. Some

transactions could be explicitly

prohibited by the policy, while

others may require the managing

partner’s approval.

1. Marie Janes has

likely not violated

the rules; the

discount is available

to customers on a

widespread basis.

Presumably many

of the employees of

the CPA firm buy

automobiles from

the dealership.

1. Marie Janes should discuss the

discount with the firm‘s

managing partner if she intends

or wants to buy the automobile.

She should certainly not feel

compelled to buy the

automobile, but she should not

automatically turn it down. The

situation would be entirely

different if the sale were limited

to employees. In such a case it

would likely be a violation.

2. The ability to eat meals on an

ongoing basis may cause Marie to

be favorably disposed to the client

when evaluating the client’s financial

statements. Also, if users of the

financial statements heard of this

arrangement, some might perceive

that there is a lack of independence.

2. Marie Janes’ firm could establish a

policy regarding free services or

gifts provided by clients. Perhaps

the firm policy could establish a

minimal dollar threshold of

allowable free services or gifts.

Those exceeding the threshold

may either be prohibited by the

policy or may require approvals by

a more senior member of

management of the audit firm.

2. If Marie Janes were

to eat there on an

ongoing basis, that

would likely be a

violation of the rules

of conduct. It would

not likely be a

violation if she

occasionally eats

with employees who

she is dealing with

at the audit.

2. Marie Janes should eat

elsewhere if it is practical to do

so, but if the only practical

place for her to eat is the

lunchroom, she should make

arrangements with her firm to

make certain that the company

is reimbursed for the expenses.

3. Gifts from clients might be perceived

as a subtle form of bribe, and thus

may create a lack of appearance of

independence. Gifts may also cause

Marie to be favorably disposed to

the client when evaluating the

client’s financial statements. Also, if

3. Marie Janes’ firm could establish a

policy regarding free services or

gifts provided by clients. Perhaps

the firm policy could establish a

minimal dollar threshold of

allowable free services or gifts.

Those exceeding the threshold

3. Accepting such a

gift is likely to be a

violation of the rules

of conduct. That gift

is reasonably large,

and would be

considered by many

3. Ideally Janes should not accept

the gift and state that since she

is not an employee, she would

prefer not to take it. If she

believes that it would be

embarrassing to the company,

she should graciously accept it

4-11

Copyright © 2017 Pearson Education, Inc.

4-12

audit committee assists and advises the full board of directors, and,

as such, aids the board in fulfilling its responsibility for public

financial reporting.

b. An audit committee member is considered independent if they

than in their capacity as a board member.

c. The functions of an audit committee may include the following:

1. Select the independent auditor; discuss audit fee with the

auditor; review auditor’s engagement letter.

purpose, and general audit procedures).

3. Review the annual financial statements before submission to

the full board of directors for approval.

4. Review the results of the audit including experiences, restrictions,

cooperation received, findings, and recommendations. Consider

attention of the directors or shareholders.

internal controls.

6. Review the company’s accounting, financial, and operating

controls.

7. Review the reports of internal audit staff.

are approved by the board of directors.

9. Review company policies concerning political contributions,

those policies.

10. Review financial statements that are part of prospectuses or

offering circulars; review reports before they are submitted to

regulatory agencies.

11. Review independent auditor’s observations of financial and

accounting personnel.

4-13

4-25 (continued)

12. Participate in the selection and establishment of accounting

policies; review the accounting for specific items or transactions

as well as alternative treatments and their effects.

d. Management is frequently under considerable pressure from

stockholders and the board of directors to maintain high earnings

for the company. In some cases this may in turn motivate management

to put pressure on auditors to permit a violation of accounting

Directors are therefore less likely to put pressure on auditors

to deviate from high professional standards, and the audit committee

can deal with the auditor in a less biased manner than can

management. In addition, the board of directors has a legal

responsibility to review the policies and actions of management.

e. For public companies, the PCAOB’s rules require a CPA firm,

before its selection as the company’s auditor, to describe in writing

and discuss with the audit committee all relationships between the

f. The criticism of audit committees has been made by many smaller

control costs. Therefore if the cost of a smaller audit firm is

significantly less than a large firm, assuming equal quality, the audit

committee would be obligated to use the less expensive firm.

4-26 a. Independence is essential for an auditor because users of financial

statements expect an unbiased viewpoint in the CPA’s attestation

to the fairness of the financial statements. If users believe that auditors

4-14

4-26 (continued)

to outsiders such as users of financial statements. Independence of

mind refers to whether the auditor has maintained an attitude of

independence throughout the engagement. For example, an auditor

could possibly maintain an attitude of independence of mind (also

Conduct concerns both.

d. 1. He has violated the Code of Professional Conduct.

Independence rules prohibit any direct ownership by a

partner or shareholder in the office that serves the client or

engagement.

2. Such a small ownership is unlikely to have any impact on a

partner’s objectivity in evaluating the financial statements. It

is unlikely to affect the partner’s independence of mind.

3. Such ownership could affect the appearance of independence

the reputation of the profession.

e.

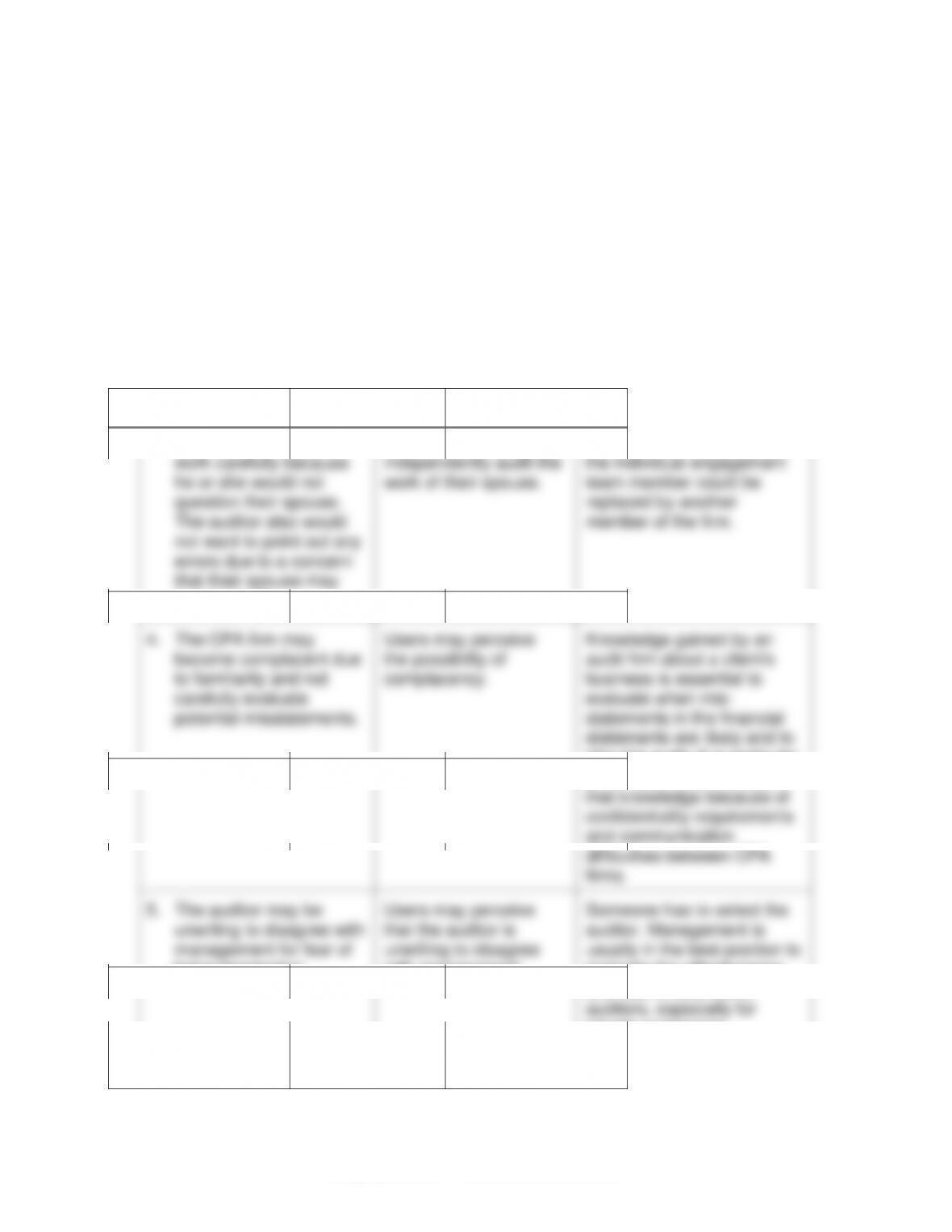

INDEPENDENCE OF MIND

INDEPENDENCE

IN APPEARANCE

SOCIAL CONSEQUENCES

OF PROHIBITING

1. May cause the auditor to

permit misstatements to

enhance personal

wealth.

Users may perceive

that auditors would

permit misstatements to

enhance personal

wealth.

Minor, if any.

4-26 (continued)

INDEPENDENCE OF MIND

INDEPENDENCE

IN APPEARANCE

SOCIAL CONSEQUENCES

OF PROHIBITING

2. Person doing this audit

may not do the audit

work carefully because

he or she did the

bookkeeping.

Users may perceive

that the auditor may not

independently audit his

or her own work.

Some clients find it less

expensive to have

bookkeeping services

performed by an outside

service. It is often less

expensive to have this done

by the auditor, because the

auditor will already be

knowledgeable about the

business.

3. Person doing this audit

may not do the audit

work carefully because

he or she would not

question their spouse.

The auditor also would

not want to point out any

errors due to a concern

that their spouse may

lose their job.

Users may perceive

that the auditor may not

independently audit the

work of their spouse.

Minor, if any, as this should

be relatively infrequent and

the individual engagement

team member could be

replaced by another

member of the firm.

4. The CPA firm may

become complacent due

to familiarity and not

carefully evaluate

potential misstatements.

Users may perceive

the possibility of

complacency.

Knowledge gained by an

audit firm about a client’s

business is essential to

evaluate when mis-

statements in the financial

statements are likely and to

plan the audit. It is costly for

a new audit firm to obtain

that knowledge because of

confidentiality requirements

and communication

difficulties between CPA

firms.

5. The auditor may be

unwilling to disagree with

management for fear of

being terminated.

Users may perceive

that the auditor is

unwilling to disagree

with management.

Someone has to select the

auditor. Management is

usually in the best position to

evaluate the effectiveness

and cost of alternative

auditors, especially for

4-26 (continued)

INDEPENDENCE OF MIND

INDEPENDENCE

IN APPEARANCE

SOCIAL CONSEQUENCES

OF PROHIBITING

6. There may be an

absence of a careful

independent check of

the entries or preparation

of the statements because

they were originally

prepared by the auditor.

Users may believe that

the auditor may not

independently audit his

or her own work or that

of a staff person from

his or her firm.

Many clients lack technical

expertise in accounting.

Having services performed

by the auditor is sometimes

the least costly alternative.

7. The auditor may be

reluctant to criticize or

may not rely on a

valuation estimate that

was originally prepared

by another department

of the audit firm.

Users may perceive

that the auditor is

auditing their own work

and will be reluctant to

criticize or question the

estimates.

A CPA firm gains

considerable knowledge

about a client and its

business during the audit.

Due to this knowledge,

valuation services can often

be provided by the same

CPA firm at a lower cost

than alternative sources

such as other CPA firms or

valuation consultants.

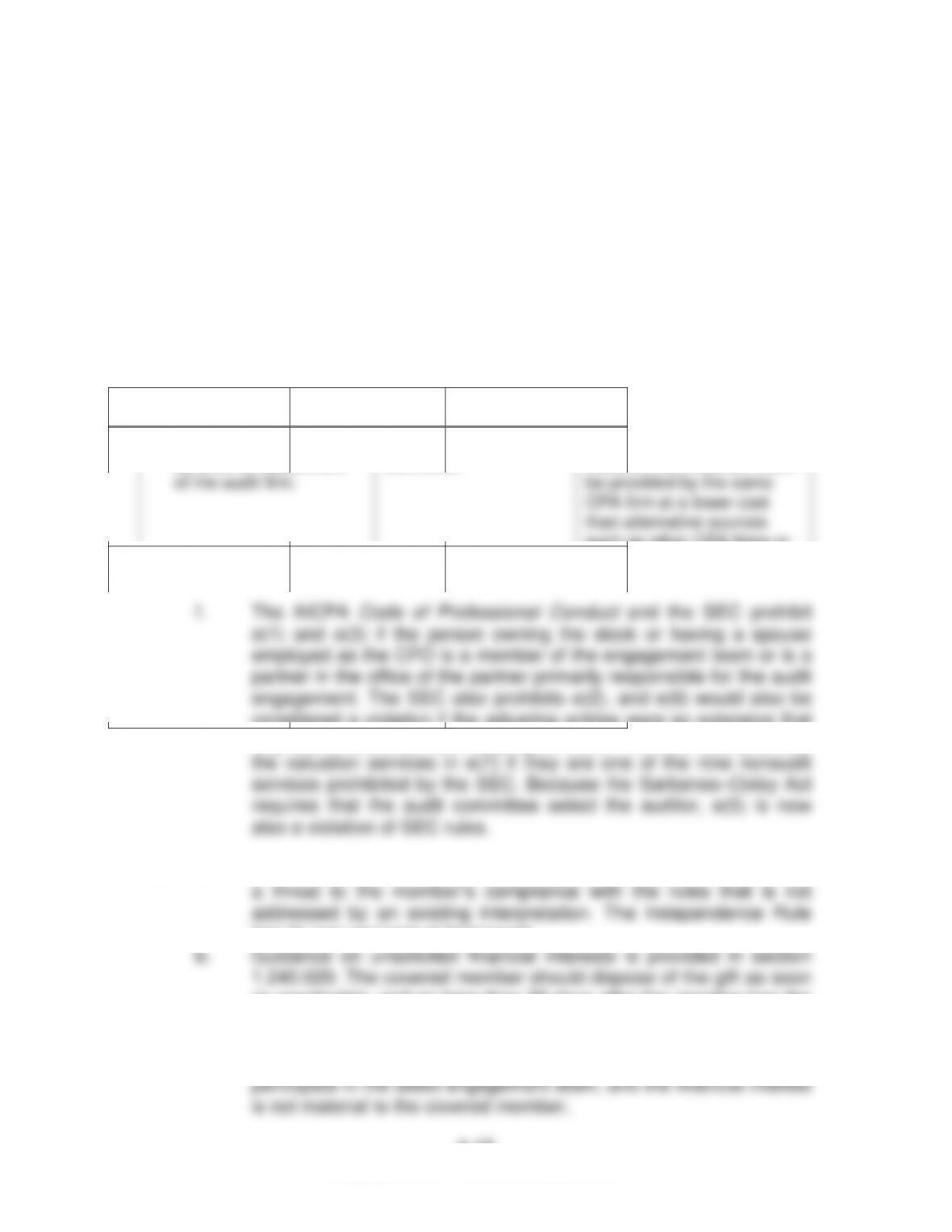

they are, in essence, bookkeeping services. The SEC also prohibits

the valuation services in e(7) if they are one of the nine nonaudit

has its own conceptual framework.

b. Guidance on unsolicited financial interests is provided in section

1.240.020. The covered member should dispose of the gift as soon

as practicable, and no later than 30 days after the member has the

right to dispose of the gift. During the period after the member