8-11

Discussion Questions And Problems

8–29

AUDIT ACTIVITIES

RELATED PLANNING PROCEDURE

1. Review accounting principles unique to

the client’s industry.

(2) Understand the client’s business

and industry

2. Determine the likely users of the

financial statements.

(1) Accept client and perform initial

audit planning

3. Evaluate the appropriate financial

statement measures for determining

amounts likely to be considered material

by users of the financial statements.

(4) Set preliminary judgment of

materiality and performance

materiality

4. Identify whether any specialists are

required for the engagement.

(1) Accept client and perform initial

audit planning

5. Send an engagement letter to the client.

(1) Accept client and perform initial

audit planning

6. Tour the client’s plant and offices.

(2) Understand the client’s business

and industry

7. Specify materiality levels to be used in

testing of accounts receivable.

(4) Set preliminary judgment of

materiality and performance

materiality

8. Compare key ratios for the company to

industry competitors.

(3) Perform preliminary analytical

procedures

9. Review management’s risk

management controls and procedures.

(2) Understand the client’s business

and industry

10. Identify potential related parties that

may require disclosure.

(2) Understand the client’s business

and industry

8–30 a. A related party transaction occurs when one party to a transaction

has the ability to impose contract terms that would not have

occurred if the parties had been unrelated. Accounting standards

conclude that related parties consist of all affiliates of an enterprise,

including (1) its management and their immediate families, (2) its

8-12

8–30 (continued)

b. (1) Related party transaction. Canyon Outdoor has entered into

an operating lease with a company owned by one of the

(2) Not a related party transaction. The fact that Canyon Outdoor

has purchased inventory items for many years from Hessel

Boating Company is a normal business transaction between

(3) Related party transaction. The financing provided by Cameron

Bank and Trust through the assistance of Suzanne may not

(4) Not a related party transaction. Just because the two owners

are neighbors does not mean that either has significant

(5) Not a related party transaction. The declaration and approval

c. When related party transactions or balances are material, the

following disclosures are required:

1. The nature of the relationship or relationships.

2. A description of the transaction for the period reported on,

3. The dollar volume of transactions and the effects of any

in the preceding period.

4. Amounts due from or to related parties, and if not otherwise

8-13

8–30 (continued)

1. Obtain background information about the client in the manner

2. Perform analytical procedures of the nature discussed in

3. Review and understand the client’s legal obligations in the

4. Review the information available in the audit files, such as

5. Discuss the possibility of fraudulent financial reporting with

management.

6. When more than one CPA firm is involved in the audit,

7. Investigate whether material transactions occur close to

8. In all material transactions, evaluate whether the parties are

9. Whenever there are material non–arm’s–length transactions,

each one should be evaluated to determine its nature and

10. When management is indebted to the company in a material

amount, evaluate whether management has the financial ability

evaluate its acceptability and value.

11. Inspect entries in public records concerning the proper

liens.

8–30 (continued)

12. Make inquiries with related parties to determine the possibility

between them.

14. When an independent party, such as an attorney or bank, is

significantly involved in a material transaction, ascertain from

referred to were those from October 21, 2016.

Additionally, the auditor will request the client to include a

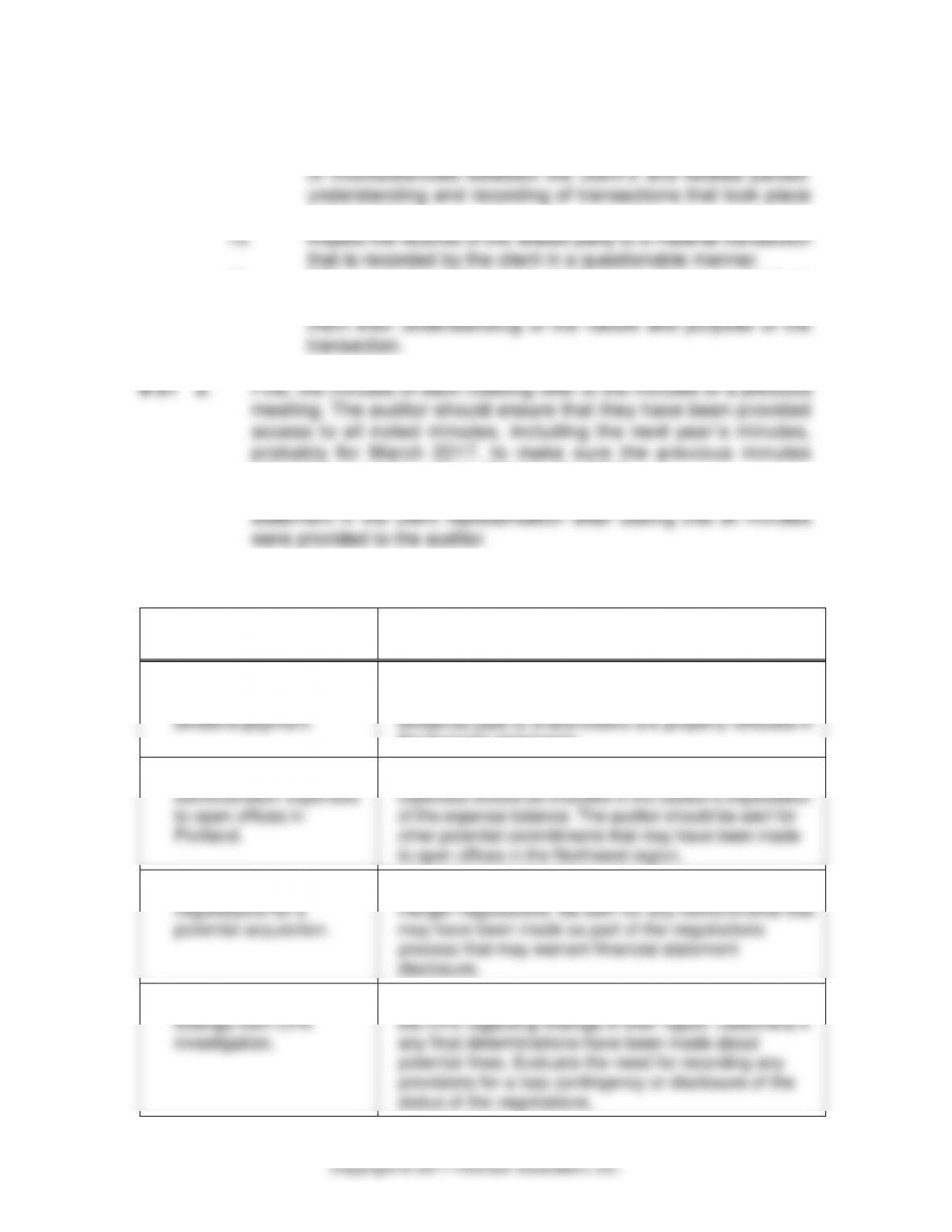

b.

INFORMATION RELEVANT

TO 2016 AUDIT

AUDIT ACTION REQUIRED

March 5:

1. Increase in annual

dividend payment.

Calculate the total dividends and determine that

dividends paid to shareholders are properly reflected in

the financial statements.

2. Approval of additional

administration expenses

to open offices in

Portland.

During analytical procedures, an increase in administrative

expenses should be included in the auditor’s expectation

of the expense balance. The auditor should be alert for

other potential commitments that may have been made

to open offices in the Northwest region.

3. Approval to engage in

negotiations for a

potential acquisition.

Determine the status of any potential acquisition or

merger negotiations. Be alert for any commitments that

may have been made as part of the negotiations

process that may warrant financial statement

disclosure.

4. Potential negative

findings from EPA

investigation.

Evaluate the status of any resolution of negotiations with

the EPA regarding findings in their report. Determine if

any final determinations have been made about

potential fines. Evaluate the need for recording any

provisions for a loss contingency or disclosure of the

status of the negotiations.

8–31 (continued)

INFORMATION RELEVANT

TO 2016 AUDIT

AUDIT ACTION REQUIRED

5. Officers’ bonuses.

Determine whether bonuses were accrued at 12-31-15

and were paid in 2016. Consider the tax implications of

unpaid bonuses to officers.

6. Discussion at the

Audit Committee

and Compensation

Committee.

Determine what, if any, decisions made at either

meeting have any impact on the audit of the financial

statements.

INFORMATION RELEVANT

TO 2016 AUDIT

AUDIT ACTION REQUIRED

October 21:

1. Reduction in sales and

the related cutback in

labor and shipping costs.

During analytical procedures, both the decrease in

revenues and the decreases in labor and shipping

costs should be included in the auditor’s expectation

of the related account balances. The auditor should

be alert to the fact that the drop in operating

performance might create undue incentives and

pressures that could highlight the risk of fraud.

2. Approval of the

acquisition and related

financing.

Examine acquisition documentation and financing

documentation to understand the impact to the

financial statements for recording the acquisition and

the debt transaction. Consider what commitments and

contingencies exist and evaluate the appropriateness

of the recording of the acquisition transaction and

related disclosures.

3. Consideration of a new

incentive stock option

plan.

Determine if the new incentive stock option plan has

been approved. If so, consider accounting treatments

required to reflect any commitments on the part of the

company and evaluate the tax implication of the plan

and need for related disclosure.

4. Identification of

deficiencies in internal

control.

Discuss the deficiencies in internal control with

management and evaluate the impact of any

remediation activities to address the deficiencies.

Evaluate the impact of remediation on the auditor’s

tests of controls and need for substantive procedures.

5. Resolution of the EPA

report findings.

Examine the EPA resolution agreement and determine

if provision has been recorded for the expected costs

to modify the air handling equipment. Consider the

need for any additional disclosures of this resolution.

6. Discussion at the Audit

and Compensation

Committee.

Determine what, if any, decisions made at either

meeting have any impact on the audit of the financial

statements.

8–31 (continued)

c. The auditor should have obtained and read the March minutes,

before completing the 12–31–15 audit. Two items were especially

8–32 a. Gross margin percentage for drug and nondrug sales is as follows:

DRUGS

NONDRUGS

2016

2015

2014

2013

40.6%

42.2%

42.1%

42.3%

32.0%

32.0%

31.9%

31.8%

approximately $82,000 (42.2% – 40.6% x $5,126,000), which appears

b. As the auditor, you cannot accept Adams’ explanation if $82,000

income.

8-33

OBSERVED CHANGE

POSSIBLE EXPLANATION(S)

1. The allowance for obsolete

inventory increased from the

prior year, but the allowance as

a percentage of inventory

decreased from the prior year.

a. Shipments of inventory sold prior to year

end were included in the client’s inventory

counts as of the balance sheet date.

f. The client purchased a large block of

inventory on account close to year end.

2. Long-term debt increased from

the prior year, but total interest

expense decreased as a

percentage of long-term debt.

d. Portions of existing long-term debt were

refinanced at lower interest rates. (Note:

This explanation would not be sufficient by

itself given it does not help explain the

increase in long-term debt).

i. Short-term borrowings were refinanced on a

long-term basis at lower interest rates.

8-33 (continued)

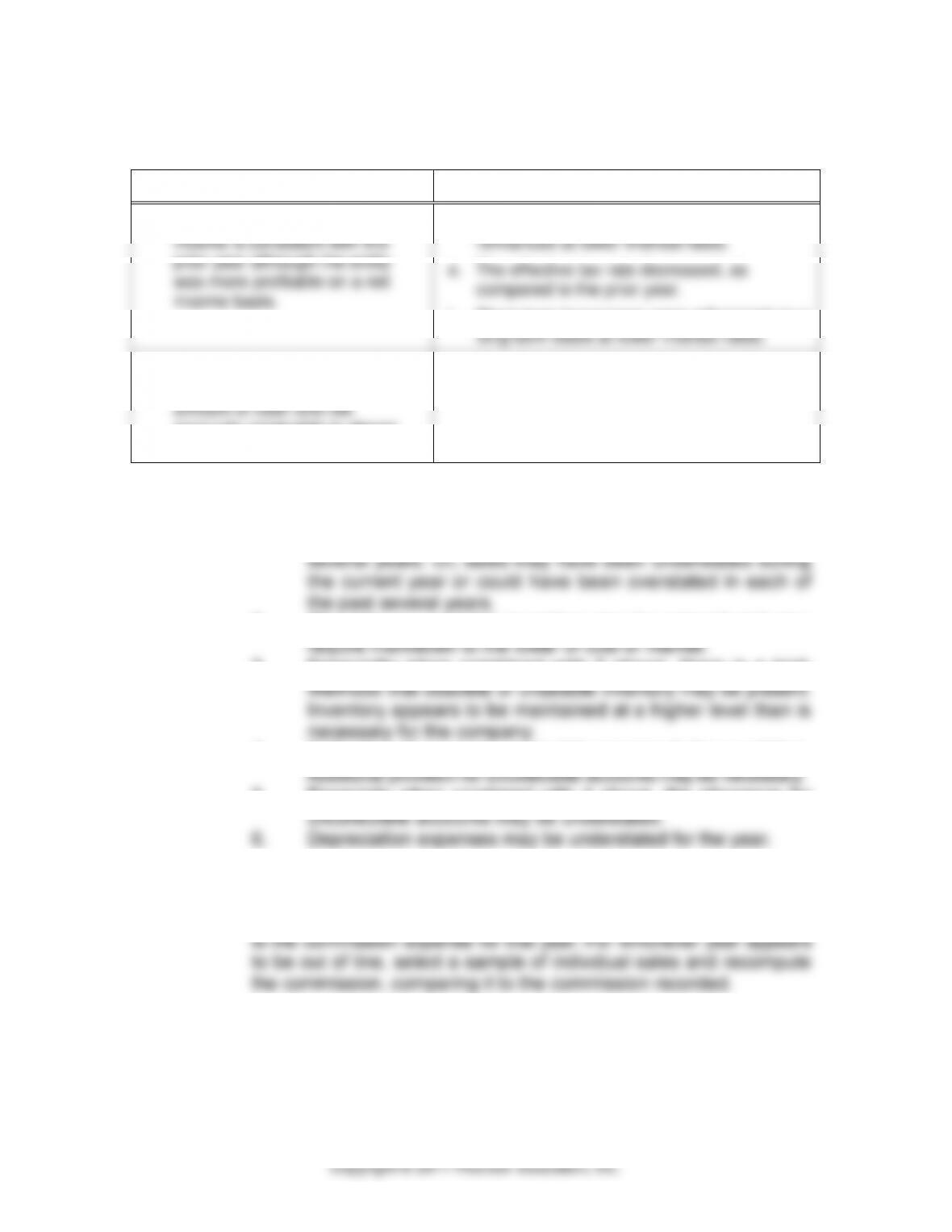

OBSERVED CHANGE

POSSIBLE EXPLANATION(S)

3. The dollar amount of operating

income is consistent with the

prior year although the entity

was more profitable on a net

income basis.

d. Portions of existing long-term debt were

refinanced at lower interest rates.

e. The effective tax rate decreased, as

compared to the prior year.

i. Short-term borrowings were refinanced on a

long-term basis at lower interest rates.

4. The quick ratio decreased from

the prior year, although the

amount of cash and net

accounts receivable is almost

the same as the prior year.

f. The client purchased a large block of

inventory on account close to year end.

8–34 a. 1. Commission expense could be overstated during the current

year or could have been understated during each of the past

2. Obsolete or unsalable inventory may be present and may

3. Especially when combined with 2 above, there is a high

4. Collection of accounts receivable appears to be a problem.

5. Especially when combined with 4 above, the allowance for

b. ITEM 1 – Make an estimated calculation of total commission expense

by multiplying the standard commission rate times commission

sales for each of the last two years. Compare the resulting amount

8-18

8–34 (continued)

to sell, propose that the client mark down the inventory to market

value.

ITEMS 4 AND 5 – Select a sample of the larger and older accounts

additional allowance for uncollectible accounts.

ITEM 6 – Discuss the reason for the reduced depreciation expense

with the client personnel responsible for the fixed assets accounts.

is reasonable for the year.

8–35 a. Target and Kohl’s are similar, but their business descriptions

indicate somewhat different market positioning. Target indicates it

offers customers everyday essentials and fashionable,

b. December is the peak selling month for retailers due to the holiday

shopping season, which is then followed by a brief period with

d. Based on Target’s description as selling at discount prices, it

8-19

Copyright © 2017 Pearson Education, Inc.

8–36 a. The direct projection of error = (misstatements/amount sampled) x

population value.

b. No, the overall financial statements are not acceptable. Including

misstatements.

8–37 a. Ling should consider the overall audit assurance desired,

c. Ling set performance materiality for inventory at a lower amount

because there are concerns about obsolescence and because

d. Performance materiality is the highest for accounts receivable

because the account is large and requires sampling to test the

8-20

of the auditor’s professional judgment.

The illustrative materiality guidelines in Fig 8–6 (p. 238)

STATEMENT

COMPONENT

PERCENT

GUIDELINES

DOLLAR RANGE

(IN MILLIONS)

Earnings from continuing

operations before taxes

Current assets

Current liabilities

Total assets

3 – 6%

3 – 6%

3 – 6%

1 – 3%

$12.5 – $ 25.1

$67.6 – $135.2

$36.5 – $72.9

$38.6 – $115.8

the same amount to each of the balance sheet accounts on the

consolidated statement of financial position. Using a materiality

limit of $12,500,000 before taxes (because it is the most restrictive)

and the same dollar allocation to each account excluding retained

c. Auditors generally use before tax net earnings instead of after tax