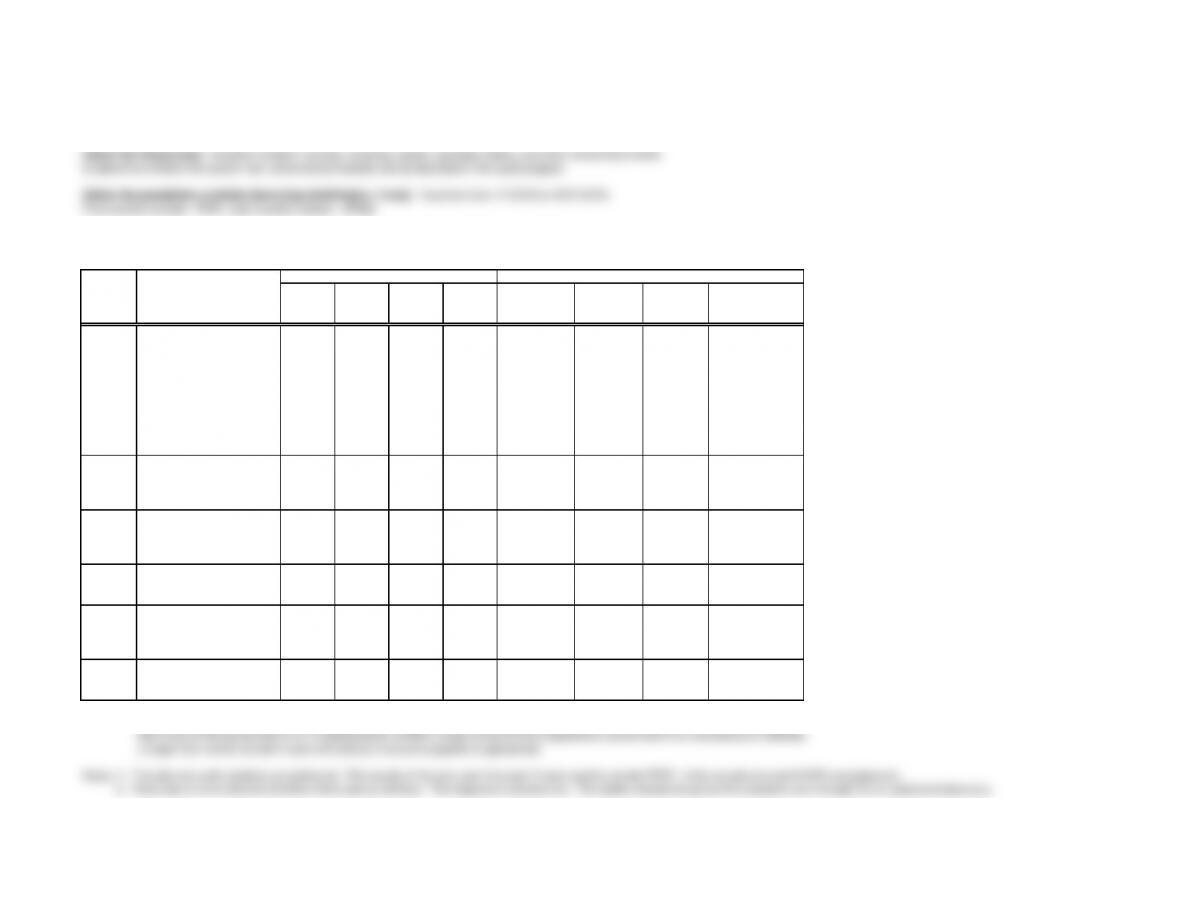

Client: Pinnacle Manufacturing

Audit Area: Tests of Controls and Substantive Test of Transactions–Acquisitions.

Define the Objective(s): Examine vendors’ invoices, receiving reports, purchase orders, and other related documents

to determine whether the system has functioned as intended and as described in the audit program.

Define the population precisely (including stratification, if any): Vouchers from 1/1/2016 to 10/31/2016.

First voucher number – 6734. Last voucher number – 33722.

Define the sampling unit, organization of population items, and random selection procedures:

Voucher number, recorded sequentially in the acquisitions journal; random number function in electronic spreadsheet.

EPER TER ARO

Initial

sample

Size

Sample Size

Number of

Exceptions

SER

Calculated

Sampling Error

(TER-SER)

1.

Evidence of internal

verification of voucher

package including propriety

of purchase, dates, unit

costs, prices, extensions,

footings, account

classification, recording in

journal, and posting and

summarization. (6a, b)

06% 10% 30 30 2 6.7% -0.7%

2.

Prices on vendors’ invoices

conform to approved price

limits established by

management. (6c)

05% 10% 40 40 0 0.0% 5.0%

3.

Price times quantity and

other calculations on the

vendor’s invoice are correct.

(6d)

1% 5% 10% 50 50 0 0.0% 5.0%

4.

Evidence of proper account

classification on vendors’

invoices. (6e)

2% 5% 10% 70 70 0 0.0% 5.0%

5.

Dates on entries in

purchases journal agree with

dates on receiving reports.

(6f)

1% 5% 10% 50 50 2 4.0% 1.0%

6.

Evidence of internal

verification of each purchase

voucher. (6g)

06% 10% 30 30 0 0.0% 6.0%

Results: based on the results of the tests, all controls appear effective except for evidence of internal verification. Since there were also

two errors on timing and and error in comparing the vendor’s invoice amount to the acquisitions journal that is not included as an attribute,

a larger than normal sample in year-end testing of accounts payable is appropriate.

Notes: 1. The planned audit variables are judmental. The results of the prior year from part III were used to decide EPER. Initial sample size and CUER are judgments.

2. There was an error discovered where there was no attribute. This happens in practice too. The auditor should not ignore the exception even though it is an unplanned discovery.

Planned Audit

Description of Attributes

Actual Results

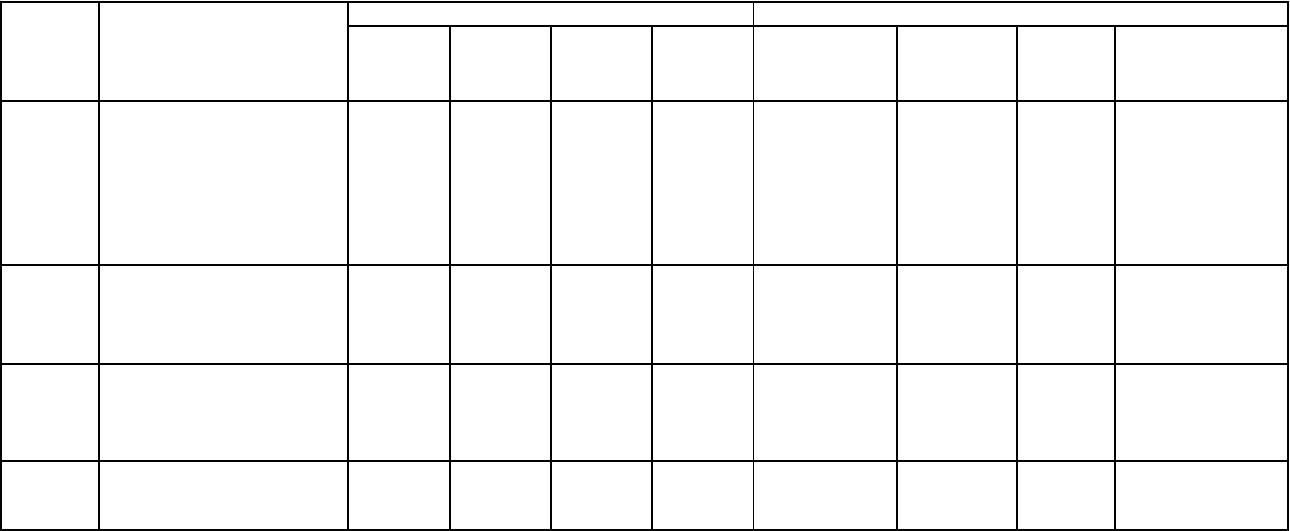

Client: Pinnacle Manufacturing

Audit Area: Tests of Controls and Substantive Test of Transactions–Cash Disbursements

Define the Objective(s): Examine cancelled checks and other related documents

to determine whether the system has functioned as intended and as described in the audit program.

Define the population precisely (including stratification, if any): Cancelled checks from 1/1/2016 to 10/31/2016.

First check number – 12376. Last check number – 37318.

Define the sampling unit, organization of population items, and random selection procedures:

Check number, recorded sequentially in the cash disbursements journal; random number function in electronic spreadsheet.

EPER TER ARO

Initial

sample

Size

Sample Size

Number of

Exceptions

SER

Calculated

Sampling Error

(TER-SER)

1.

Payee, name, amount, and

date on cancelled check

agrees with related

purchases journal and

cash disbursements entry.

(9a)

05% 10% 40

2.

Evidence of signature,

proper endorsement and

cancellation of each check.

(9b)

05% 10% 40

3.

Date on cancelled check

agrees with bank

cancellation date. (9c)

25% 10% 70

4.

Cash discounts are

correct. (9d)

05% 10% 40

Description of Attributes

Planned Audit

Actual Results

Selection of 50 random numbers (largest sample size is 50)

10237 Note: Random numbers in this file change each time the file

11302 is opened. To show numbers in sorted order, students will

11741 need to use the block/values command to set the random number

19804

values after the 50 items are generated with the RANDBETWEEN

23183 command. Next, students should sort the random numbers in

26914 ascending order into a separate column.

27907

14586

27508

22393

20980

20273

8811

15270

27518

32858

18899

30809

14103

21676

28123

18740

30007

23298

9598

9827

20287

14527

28619

28116

22841

31801

20845

8335

24247

17726

11073

21915

16399

24133

12986

31036

9622

28867

29907

14005

19323

11881

29940

9821