12-21

12–28 (continued)

4. Access the client’s electronic inventory master file and list

slow–moving items or parts.

5. Access the client’s electronic inventory master file and list all

reviewed for possible slow–moving or obsolete items.

6. Enter the audit test–count quantities onto the cards. Match

differences. This will indicate whether the client’s year–end

agreement.

7. Use the adjusted electronic inventory master file and

calculations performed by the client.

8. Use the client’s electronic inventory master file and list all

9. Use the costs per unit on the client’s electronic inventory

master file, and extend and total the dollar value of the

12-22

12–29

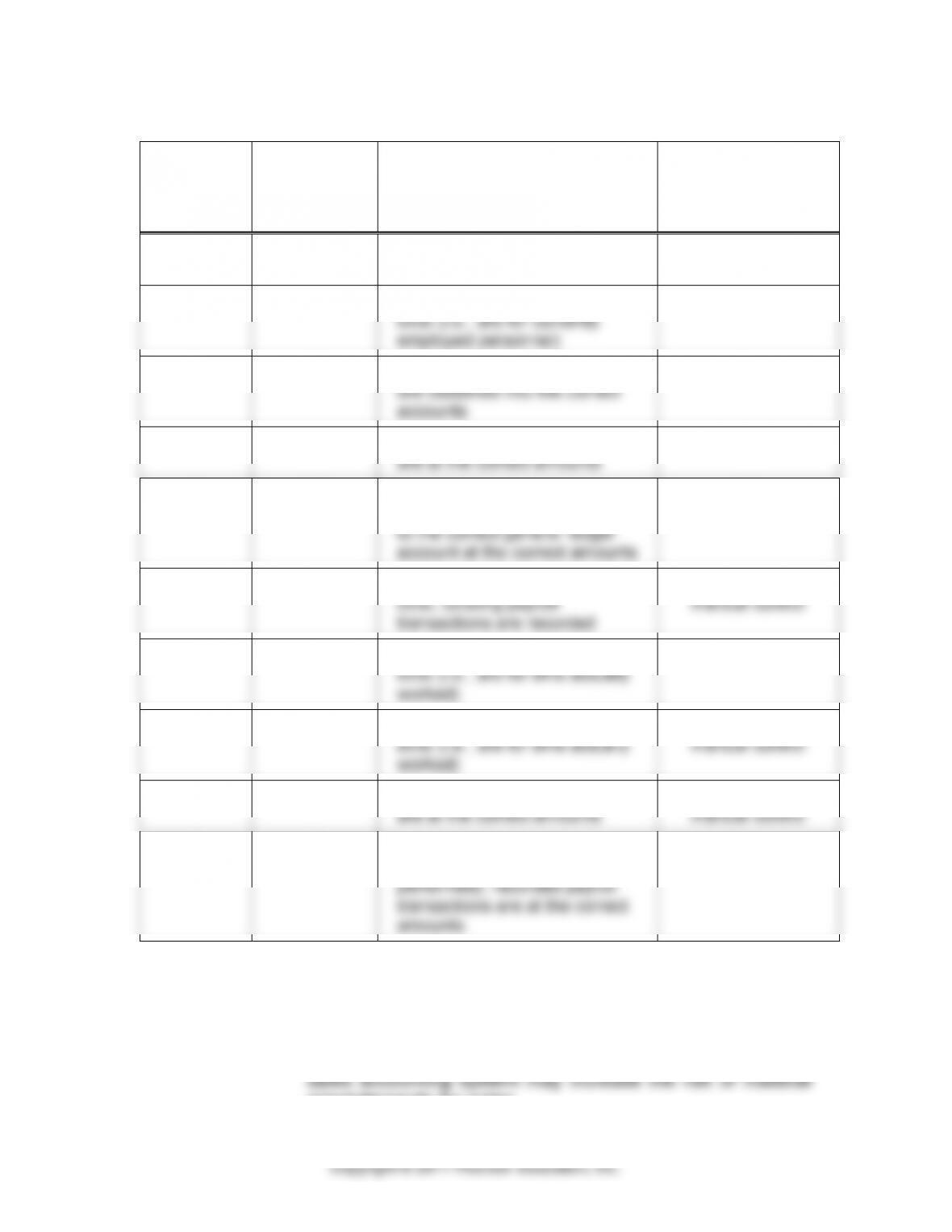

INTERNAL

CONTROL

a.

TYPE OF

CONTROL

b.

TRANSACTION–RELATED

AUDIT OBJECTIVE

c.

OPPORTUNITY TO

RELY ON PRIOR

YEAR TESTING

1

AC

Recorded payroll transactions

exist for valid employees

Yes

2

AC

Recorded payroll transactions

exist (i.e., are for currently

employed personnel)

Yes

3

AC

Recorded payroll transactions

are classified into the correct

accounts

Yes

4

AC

Recorded payroll transactions

are at the correct amounts

Yes

5

AC

Recorded payroll transactions

are summarized and posted

to the correct general ledger

account at the correct amounts

Yes

6

MC

Recorded payroll transactions

exist; existing payroll

transactions are recorded

No, since

manual control

7

AC

Recorded payroll transactions

exist (i.e., are for time actually

worked)

Yes

8

MC

Recorded payroll transactions

exist (i.e., are for time actually

worked)

No, since

manual control

9

MC

Recorded payroll transactions

are at the correct amounts

No, since

manual control

10

AC

Recorded payroll transactions

exist (i.e., for valid work

performed); recorded payroll

transactions are at the correct

amounts

Yes

12–30 a. The following deficiencies in the Parts for Wheels, Inc., online

sales system may lead to material misstatements:

1. Lack of Sales System Interface. The lack of automatic

interface between the online sales ordering system and the

misstatements for sales.

12-23

12–30 (continued)

that sales may be processed or recorded inaccurately.

2. Lack of Inventory System Interface. The lack of automatic

interface between the online sales ordering system and the

inventory accounting records. With manual processing,

there may be some risk that shipments occurred without

completion of a proper bill of lading, which is required to

or are entered more than once. Furthermore, the manual

process of recording inventory transactions increases the

records.

3. Manual Credit Approval. The process of verifying credit

customers. This may lead to an increased risk of collection

problems from credit card receivables.

4. Premature Recording. Currently, sales are entered into the

shipment has occurred. As a result, sales may be recorded

5. Inadequate Tracking of Returns. If systems for tracking and

estimating online sales returns are inadequate, Parts for

shipping costs.

b. Below are suggested changes that could be made to the existing

the online system:

12-24

12–30 (continued)

1. When the accounting department prints submitted orders

should be recorded.

2. Prenumbered bills of lading should be used. All bills of

3. Accounting should match the bills of lading with the accounting

department’s copy of the sales orders before any entries

recording of transactions.

c. For the deficiencies identified in part a, the auditors would be most

concerned about the following transaction–related and balance–

related audit objectives:

1. Lack of Sales System Interface. Auditors would be

concerned about occurrence, completeness, accuracy, and

accuracy, and cutoff of accounts receivable.

2. Lack of Inventory System Interface. Auditors would be

concerned about occurrence, completeness, accuracy, and

completeness, accuracy, and cutoff of inventory.

with realizable value of credit card receivables.

4. Premature recognition. Auditors would be most concerned

receivable.

5. Inadequate Tracking of Returns. The auditor would be

concerned about completeness of sales returns

(occurrence of sales) and shipping costs.

d. Auditors could use generalized audit software in several ways.

First, they could use audit software to match orders made through

the online sales order system to sales recorded manually by

12-25

12–30 (continued)

Audit software could also be used to compare updates to

the inventory system with the sales recorded to ensure all sales

12–31 a. When an organization outsources its information technology functions

to a third party, there are several inherent risks that arise. For First

Community Bank, management is totally reliant on Technology

Solutions’ internal controls designed to protect IT hardware,

Because First Community must transmit transaction related

data between the bank and the Technology Solutions data center,

there is a risk that data may be lost, corrupted, or stolen during the

communication transfer process. Also, like First Community,

b. As noted in the answer to part a., the outsourcing of the IT function

to Technology Solutions means that most of the IT general controls

are now under the direct supervision of management at Technology

c. The use of Technology Solutions is likely to have a significant

effect on the audit of the financial statements of First Community

Bank. Because the bank has outsourced all of the bank’s financial

reporting applications to Technology Solutions, most of the IT–

related controls and underlying applications and data files now

12-26

Copyright © 2017 Pearson Education, Inc.

12–32 a. 1. Automated control embedded in computer software

2. Manual control whose effectiveness is based significantly

on IT–generated information

3. Automated control embedded in computer software

4. Manual control whose effectiveness is based significantly

auditor determines that no changes have been made to the

automated control, the auditor can rely on prior year audit

tests of the controls as long as the control is tested at least

once every third year audit. If the control mitigates a

year’s audit.

2. The extent of testing of this control could be moderately

reduced in subsequent years if effective controls over

program and master file changes are in place. Such controls

would increase the likelihood that the printout of prices

changed without authorization. However, because this

control is also dependent on manager review of computer

subject to an unauthorized change.

12-27

12–32 (continued)

identifies purchases exceeding $10,000 per vendor functions

accurately. However, because this control is also dependent

5. Because this control is not dependent on technology

12–33 Note: The PCAOB reorganized their auditing standards effective

December 31, 2016. Auditing Standard No. 5 is identified in the

reorganized standards as AS 2201.

a. Paragraph .01 of AS 2201 notes that the integrated audit standard

over financial reporting.

b. According to paragraph .07 of the standard, the auditor’s objective

in an audit of internal control over financial reporting is to express

an opinion on the effectiveness of internal controls over financial

to support the assessment of control risk that is relevant to the

financial statement audit.

c. As discussed in paragraphs .10 through .12 of AS 2201, risk

assessment related to the audit of internal control over financial

performed.

12-28

12–33 (continued)

level controls and then work their way down to significant

accounts and then relevant assertions and audit objectives. Both

quantitative and qualitative factors are important in identifying

significant accounts and relevant assertions.

implied.

12–34 1. Students should have located the Form 10–K for Bob Evans

Farms, Inc., for the year ended April 25, 2014. Instructors may

2. Management’s Annual Report on Internal Control Over Financial

Reporting provides the following answers to the questions in a.

through f.:

a. Management is responsible for establishing and

maintaining adequate internal control over financial

reporting.

financial reporting.

c. Management conducted its assessment of the effectiveness

of internal control over financial reporting based on criteria

established in the COSO Internal Control – Integrated

Framework.

accounting and property, plant, and equipment accounting.

f. Management does not disclose any changes in their report,

but discloses additional information in Item 9A of the form

12-29

12–34 (continued)

3. The report of the independent registered public accounting firm

notes the firm audited internal control over financial reporting in

accordance with the standards of the PCAOB. The auditor’s report

also discusses the material weaknesses identified in

financial statements.

Case

12–35 1. Strengths in lines of reporting from IT to senior management at

Jacobsons:

needs.

Melinda’s boss, the COO, has access to the board of

directors and provides periodic updates about IT issues, if

needed.

may place undue pressure on IT to work on IT related projects

that affect the COO’s areas of responsibility. Thus, other

areas, such as those under the chief financial officer’s control

(e.g., the accounting system), may not receive adequate

IT resources.

board of directors.

There does not appear to be a written IT strategic plan that

sets direction for the IT function.

Recommendations related to the lines of reporting from IT to senior

management:

12-30

12–35 (continued)

annually by the board.

Significant hardware and software changes should be approved

by the board or its IT Steering Committee. Other changes

to application software should also be approved by affected

user departments.

including her strengths:

Melinda is actively involved in the IT function and closely

monitors day–to–day IT activities.

Melinda is experienced in Jacobson’s IT function, having been

employed by the company for 12 years. She has served in

the IT function.

Melinda performs extensive background checks before offering

candidates employment in IT functions.

Melinda has successfully maintained a fairly stable IT staff.

Melinda conducts weekly IT departmental meetings to discuss

issues affecting the performance of the department.

board.

Concerns about current management of the IT function:

Melinda may be over–delegating tasks to IT personnel without

maintaining close accountability for employee actions. For

example, programmers are given extensive leeway in

properly followed.

Melinda spends too much of her time in the systems analyst

role, which leaves little time for her to adequately monitor

all IT tasks.

IT department:

Consider assigning systems analyst responsibilities to a

senior programmer.