11–11

Copyright © 2017 Pearson Education, Inc.

11–25 1. a. Adequate documents and records, and independent checks

on performance.

b. Transactions are recorded on the correct dates (cutoff).

c. Carefully coordinate the physical count of inventory on the

2. a. Adequate documents and records and independent checks

on performance.

when the master file is updated.

3. a. Proper authorization of transactions and adequate

b. Recorded transactions exist (occurrence).

payable.

4. a. Adequate documents and records, physical control over

b. Recorded transactions exist (occurrence).

employees from parking inside the fencing.

2) Require the accounting department to maintain

5. a. Adequate separation of duties.

b. Recorded transactions exist (occurrence).

file.

6. a. Independent checks on performance.

(accuracy).

c. Counts by qualified personnel and independent checks on

7. a. Proper authorization of transactions and activities.

b. Transactions are stated at the correct amounts (accuracy).

11–12

11–25 (continued)

2) Require independent approval of all transactions,

8. a. Adequate documents and records.

b. Recorded transactions exist (occurrence).

c. 1) Require that payments only be made on original

11–26 The criteria for dividing duties is to keep all asset custody duties with

one person (Cooper). Document preparation and recording is done by the other

person (Smith). Singh will perform independent verification. The two most

three as follows:

11–27 A schedule showing the pertinent transaction–related management

assertions and application controls for each type of misstatement is below

and on the following page.

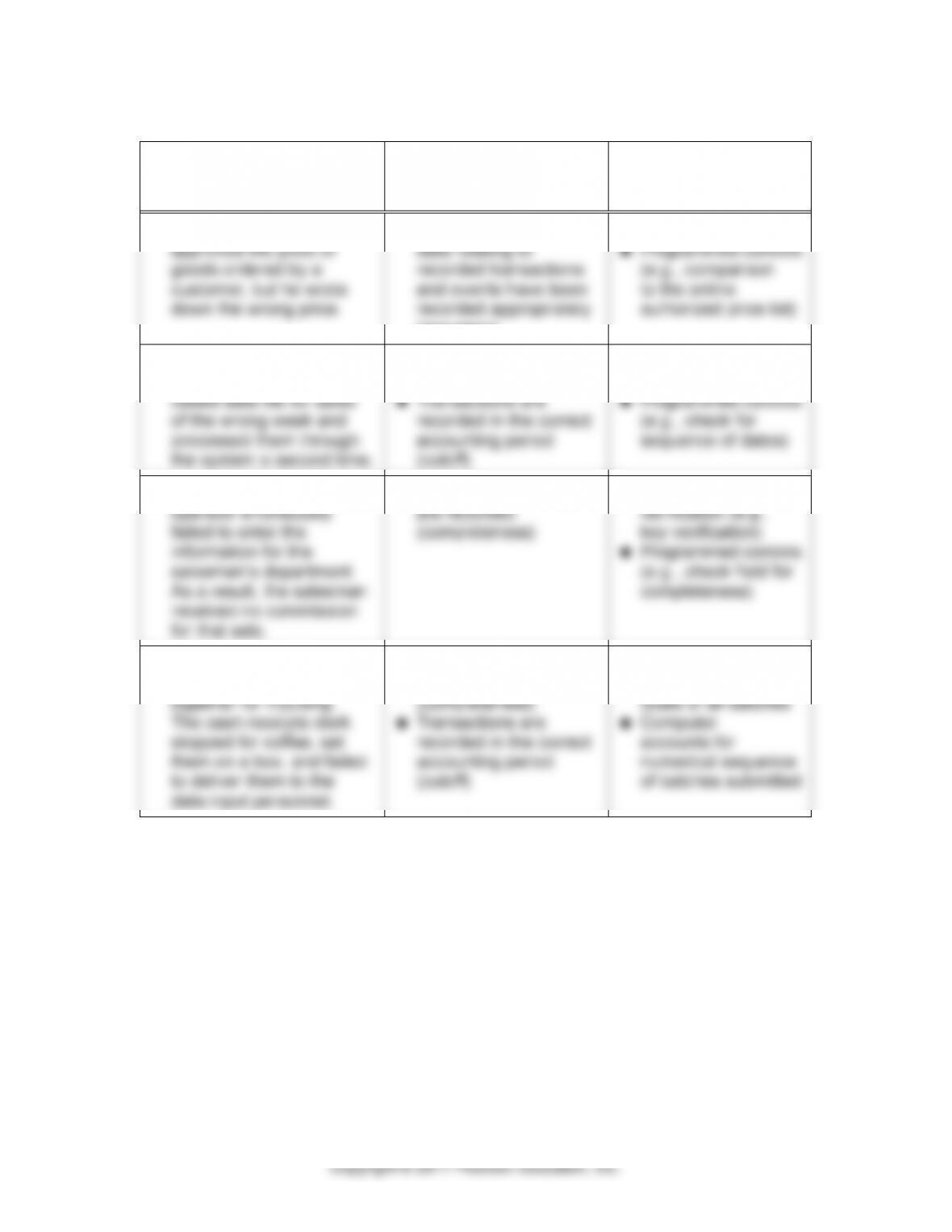

MISSTATEMENT

a.

TRANSACTION–

RELATED ASSERTION

b.

COMPUTER–BASED

CONTROLS

1. A customer number

on a sales invoice was

transposed and, as a

result, charged to the

wrong customer. By the

time the error was found,

the original customer was

no longer in business.

Recorded transactions

exist (occurrence)

Amounts and other

data relating to

recorded transactions

and events have been

recorded appropriately

(accuracy)

Key entry verification

Check digit

Reconciliation to

customer number on

purchase order and

bill of lading

2. A former computer

operator, who is now

a programmer, entered

information for a fictitious

sales return and ran it

through the computer

system at night. When

the money came in, he

took it and deposited it

in his own account.

Recorded transactions

exist (occurrence)

Input security

controls over cash

receipts records

Scheduling of

computer processing

Controls over

access to equipment

Controls over access

to live application

programs

3. A nonexistent part

number was included in

the description of goods

on a shipping document.

Therefore, no charge

was made for those

goods.

Existing transactions

are recorded

(completeness)

Preprocessing

review

Programmed

controls (e.g.,

compare part no. to

parts list master file)

4. A customer order was

filled and shipped to a

former customer that had

already filed bankruptcy.

Recorded transactions

exist (occurrence)

Preprocessing

authorization

Preprocessing

review

Programmed

controls (e.g.,

comparison

to customer file)

11-27 (continued)

MISSTATEMENT

a.

TRANSACTION–

RELATED ASSERTION

b.

COMPUTER–BASED

CONTROLS

5. The sales manager

approved the price of

goods ordered by a

customer, but he wrote

down the wrong price.

Amounts and other

data relating to

recorded transactions

and events have been

recorded appropriately

(accuracy)

Preprocessing review

Programmed controls

(e.g., comparison

to the online

authorized price list)

6. A computer operator

picked up a computer–

based data file for sales

of the wrong week and

processed them through

the system a second time.

Recorded transactions

exist (occurrence)

Transactions are

recorded in the correct

accounting period

(cutoff)

Correct file controls

Cutoff procedures

Programmed controls

(e.g., check for

sequence of dates)

7. For a sale, a data entry

operator erroneously

failed to enter the

information for the

salesman’s department.

As a result, the salesman

received no commission

for that sale.

Existing transactions

are recorded

(completeness)

Conversion

verification (e.g.,

key verification)

Programmed controls

(e.g., check field for

completeness)

8. Several remittance

advices were batched

together for inputting.

The cash receipts clerk

stopped for coffee, set

them on a box, and failed

to deliver them to the

data input personnel.

Existing transactions

are recorded

(completeness)

Transactions are

recorded in the correct

accounting period

(cutoff)

Control totals

reconciled to manual

totals of all batches

Computer

accounts for

numerical sequence

of batches submitted

11–15

11–28

PERSON 1

PERSON 2

PERSON 3

PERSON 4

a. Systems analyst

Programmer

Computer operator

Librarian

Data

control

b. Systems analyst

Programmer

Computer operator

Librarian

Data

control

N/A

c. Systems analyst

Programmer

Data control*

Computer operator

Librarian*

N/A

N/A

* This solution assumes the data control procedures will serve as a check on

the computer operator and will allocate work across both persons.

d. If all five functions were performed by one person, internal control

would certainly be weakened. However, the company would not

necessarily be unauditable, for two reasons: First, there may be

11–29 1. Wilcoxon Sports should strengthen several of its IT general controls.

The fact that the programmer was able to access the current live

version of the sales application program suggests that there are

breakdowns in appropriate segregation of duties among IT personnel.

Programmers should be restricted from access to actual software

transactions.

Wilcoxon should consider strengthening its processes for

authorizing and approving software changes. More extensive

procedures should be implemented regarding requests and approvals

for software changes. Only upon the presentation of adequate

change was authorized. Approvals for software changes should

11–16

11–29 (continued)

the sales function.

For larger IT functions, programmers are split into subgroups

with some programmers only authorized to address programming

2. Strengthening IT general controls over program changes, restricting

access to live software versions, and enhancing segregation of

duties will significantly reduce the programmer’s ability to make

unauthorized changes to software as was done at Wilcoxon Sports.

change in software without someone’s knowledge. If the

librarian only accepts revised programs for properly authorized

If programmer functions are separated among programmers

sales application and the operating system software.

11–30

a. The strengths of Hardwood Lumber Company’s computerized accounting

system include the following:

Separate departments for systems programming, applications

programming, operations, and data control.

CHANGE or RUN capabilities.

The computer room is locked and requires a key–card for access

program files.

application software program files.

Data control clerks have no access to software program files.

11–17

11–30 (continued)

Information Systems function:

The Vice President of Information Systems (VP of IS) should report

on a day–to–day basis to senior management (e.g., the president)

The VP of IS should have access to the board of directors and

should be responsible for periodically updating the board on

of IS.

Video monitors should be examined continually. The actual monitors

could be viewed on an ongoing basis by building security guards.

Hardwood should consider taping what the cameras are viewing

for subsequent retrieval in the event of a security breach.

Hardwood may consider purchasing a vendor–developed access

features.

Restrict programmer access to test copies of software programs

for only those programs that have been authorized for program

change. Access to copies of other programs may not be necessary

when those programs have not been authorized for change.

likelihood that a strong systems development process is followed.

Develop a weekly Job Schedule that outlines the order in which

operators should process jobs. The VP of IS should review computer

output to determine that it reconciles to the approved Job Schedule.

11–18

11–30 (continued)

program and data files.

Remove the librarian’s CHANGE rights to program and data files.

Consider purchasing a vendor–developed librarian software package

11–31 a. The COSO report notes that an organization’s technology will

continually evolve as the organization evolves. At the same time,

cyber attackers are continually finding new ways of hacking

b. At the control environment level, management and the board of

directors need to set the tone that cyber security is a priority. The

board of directors needs to be aware of cybersecurity issues.

Regular communication between management and the board

c. The COSO report identifies the following five categories of

perpetrators and motives:

Nation states and spies: foreign nations attempting to steal

national security information or other intellectual property

identity information

Terrorists: individuals or groups attempting to launch

cyberattacks to disrupt infrastructure such as financial

institutions

Hacktivists: individuals attempting to steal and disclose

sell private information

11–31 (continued)

prevent and detect cyberattacks. The report also suggests there

are IT–specific frameworks that organizations can rely on as well,

such as COBIT (Control Objectives for Information and Related

Technology).

■ Case

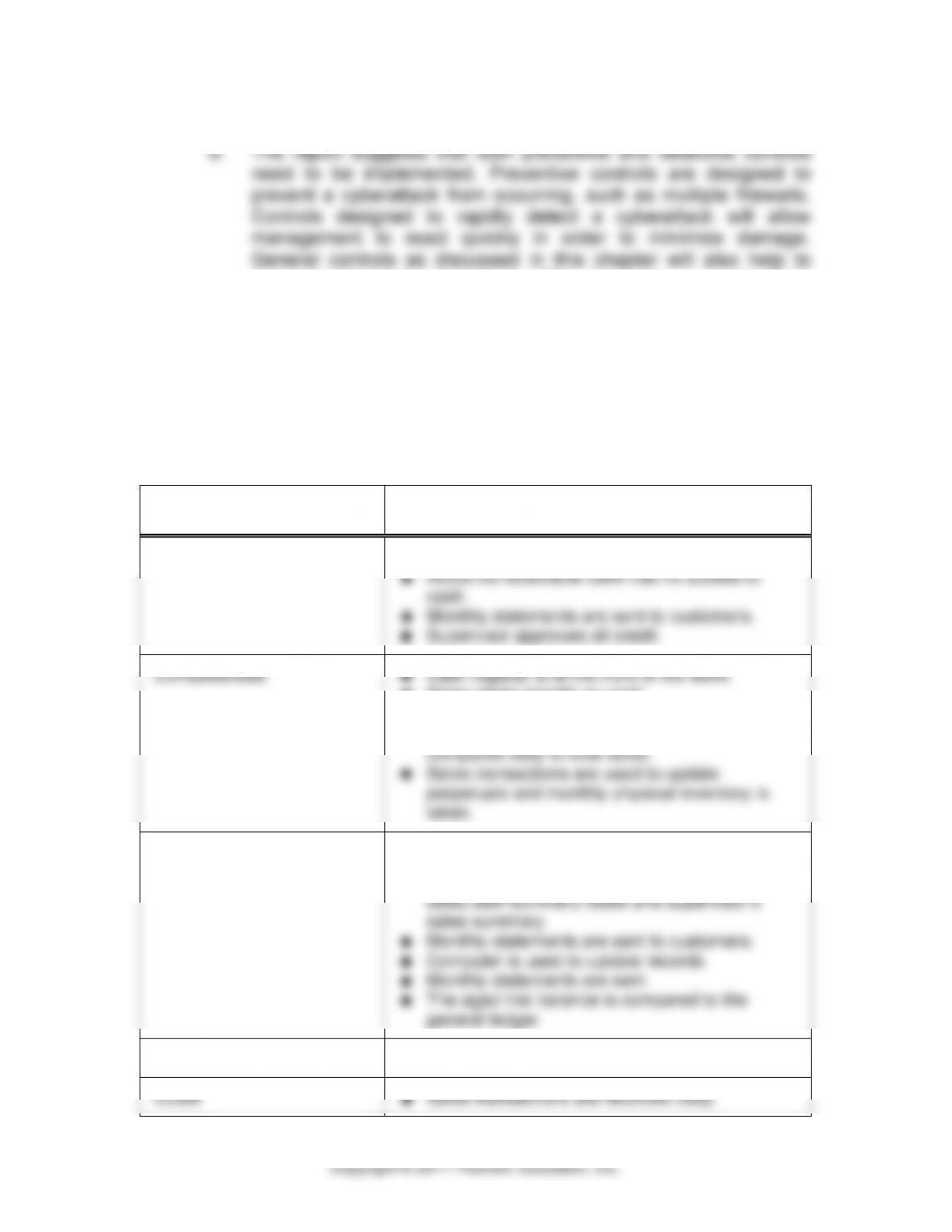

11–32 a. Sales

TRANSACTION–RELATED

ASSERTION

CONTROL

Occurrence

Supervisor approves all invoices.

Accounts receivable clerk has no access to

cash.

Monthly statements are sent to customers.

Supervisor approves all credit.

Completeness

Cash register is at the front of the store.

Sales clerks handle no cash.

Sales clerks summarize daily sales, which

determine their commission. This summary is

compared daily to total sales.

Sales transactions are used to update

perpetuals and monthly physical inventory is

taken.

Accuracy

Owner sets all prices.

Supervisor rechecks all calculations.

Accountant reconciles all computer totals to

sales staff summary totals and supervisor’s

sales summary.

Monthly statements are sent to customers.

Computer is used to update records.

Monthly statements are sent.

The aged trial balance is compared to the

general ledger.

Classification

None

11–20

11–32 (continued)

b. Cash Receipts

TRANSACTION–RELATED

AUDIT OBJECTIVE

CONTROL

Occurrence

Monthly bank reconciliation is prepared.

Accounts receivable clerk compares duplicate

deposit slip from bank to sales and cash receipts

journal.

Completeness

Cash register is used for cash sales.

Cash collected on receivables is prelisted.

Supervisor deposits money in a locked box.

Accuracy

Supervisor recaps cash sales and compares

totals to the cash receipts tapes.

Monthly bank reconciliation prepared.

Accounts receivable clerk compares duplicate

deposit slip from bank to cash sales and cash

receipts journal.

Monthly statements are sent to customers.

Computer is used to update records.

The aged trial balance is compared to the

general ledger.

Classification

None

Cutoff

Cash is deposited daily.

c. Sales and Cash Receipts

Deficiencies

invoices. (Partially offset by control totals used by

comparing sales clerks’ and supervisor’s control totals.)

ledger.

There is a lack of internal verification of all of the