22–11

22–23 (continued)

procedures.

2. Confirm the balance in notes payable to payees included in

year.

4. Obtain a standard bank confirmation that includes a specific

client does business.

5. Review the minutes of the board of directors.

22–24 In each case, any actual failure to comply would have to be reported in

a footnote to the statements in view of the possible serious consequences of

advancing the maturity date of the loan. The individual audit steps that should

be taken are as follows:

a. Calculate the working capital ratio at the beginning of and through

b. Examine the client’s copies of insurance policies or certificates of

insurance for compliance with the covenant, preparing a schedule

c. Examine vouchers supporting tax payments on all property covered

by the indenture. By reference to the local tax laws and the

d. Vouch the payments to the sinking fund. Confirm bond purchases

and sinking fund balance with trustee. Observe evidence of

22–12

22–25 a. It is desirable to prepare an audit schedule for the permanent file

for the mortgage so that the appropriate information concerning

the mortgage will be conveniently available for future years’

b. The audit of mortgage payable, interest expense, and interest

payable should all be done together since these accounts are

c. The audit procedures that should ordinarily be performed to verify

the issue of the mortgage, the balance in the mortgage and interest

payable, and the balance in the interest expense accounts are:

1. Determine if the mortgage was properly authorized.

2. Obtain the mortgage agreement and schedule the pertinent

payments, interest rate, restrictions, and collateral.

lending institution.

4. Recompute interest payable at the balance sheet date and

the payments made.

5. Test interest expense for reasonableness.

d. Accounting standards require disclosures related to long–term debt.

The terms of the debt agreement are to be disclosed, including

the client’s disclosures are complete and accurate.

22–26

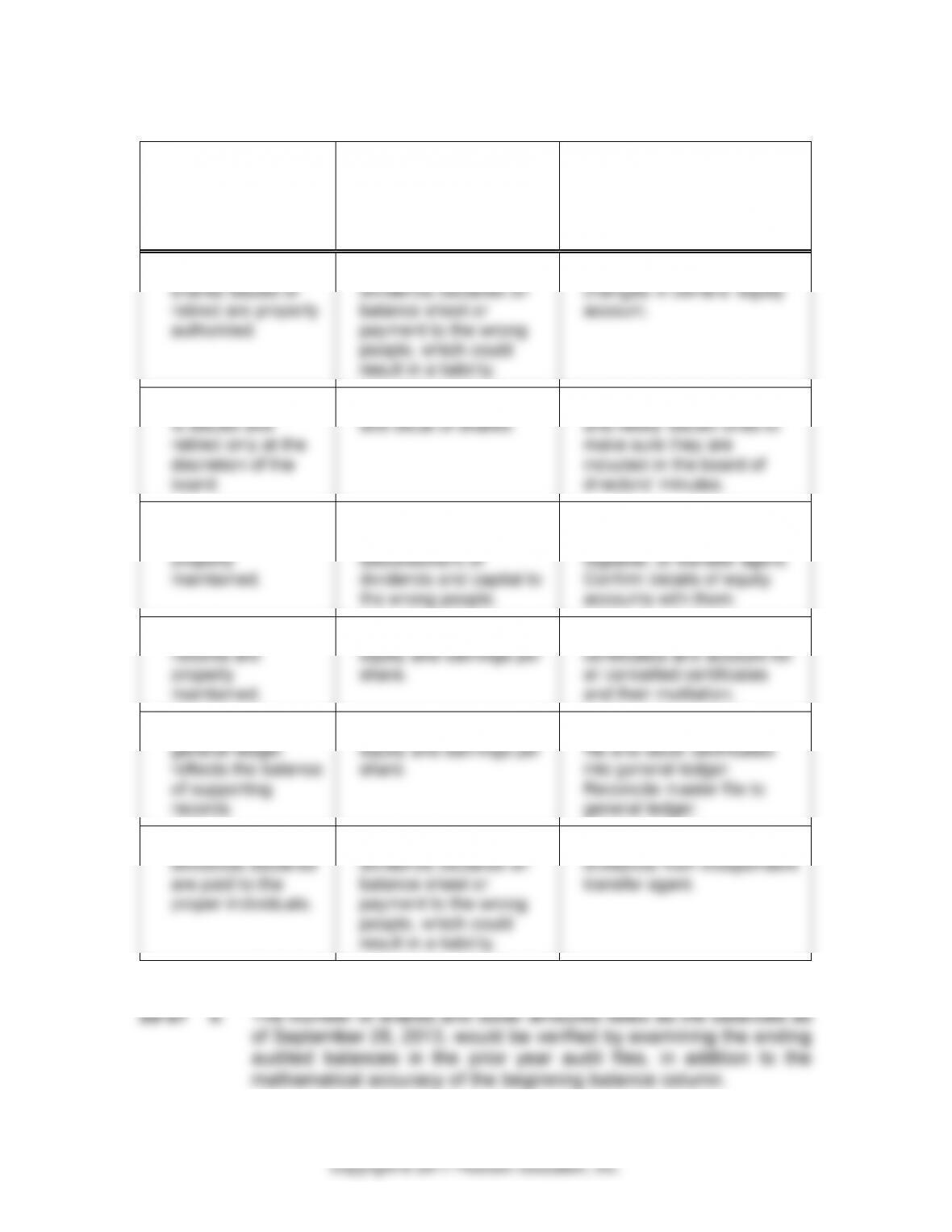

a.

PURPOSE

OF CONTROL

b.

POTENTIAL FINANCIAL

STATEMENT

MISSTATEMENT

c.

AUDIT PROCEDURES

TO DETERMINE

EXISTENCE OF

MATERIAL MISSTATEMENT

1. To insure that all

shares issued or

retired are properly

authorized.

Misstatement of

dividends declared on

balance sheet or

payment to the wrong

people, which could

result in a liability.

Verify authenticity of all

changes in owners’ equity

account.

2. To insure that stock

is issued and

retired only at the

discretion of the

board.

Illegal payments of cash

and issue of shares.

Examine cancelled shares

and newly issued ones to

make sure they are

included in the board of

directors’ minutes.

3. To insure that

records are

properly

maintained.

Misstatement of owners’

equity and the

disbursement of

dividends and capital to

the wrong people.

Determine if company uses

services of an independent

registrar, or transfer agent.

Confirm details of equity

accounts with them.

4. To insure that

records are

properly

maintained.

Misstatement of owners’

equity and earnings per

share.

Account for all unissued

certificates and account for

all cancelled certificates

and their mutilation.

5. To insure that the

general ledger

reflects the balance

of supporting

records.

Misstatement of owners’

equity and earnings per

share.

Trace postings from master

file and stock certificates

into general ledger.

Reconcile master file to

general ledger.

6. To insure that the

dividends declared

are paid to the

proper individuals.

Misstatement of

dividends declared on

balance sheet or

payment to the wrong

people, which could

result in a liability.

Obtain confirmation of paid

dividends from independent

transfer agent.

22–14

22–27 (continued)

entries affecting net earnings are required.

c. The audit procedures that should ordinarily be performed to verify

the repurchase of common stock, share–based compensation, and

common shares issued are described below:

1. Repurchase of common stock: The auditor would examine

The auditor would also examine the cash disbursements

journal and related documentation that supports the

2. Share–based compensation: The auditor would examine

documents that outline the terms of the compensation

committee for evidence of approval of the compensation

plan terms. The auditor would evaluate whether the

amounts reflected as share–based compensation are

transfer agent.

3. Common shares issued: The auditor would examine

minutes of meetings of the board of directors that document

the approval of the decision to issue common shares,

d. The amounts shown as of September 27, 2014, in the Statement of

Shareholders’ Equity should also be included as ending balances in

22–15

22–28

a.

PURPOSE OF

AUDIT PROCEDURES

b.

MISSTATEMENTS THAT

MAY BE UNCOVERED

1. To determine what type of stock

may be issued, under what

circumstances, and its description.

Unauthorized outstanding stock or

improper description of stock.

2. To determine the propriety of

changes in the accounts and to

verify their accuracy.

The issuance or retirement of stock

without proper authorization, improper

valuation, or incorrect dividend

calculations.

3. To determine if there were any

shares issued or retired during year,

or if any certificates are missing.

Unrecorded or unauthorized transactions,

or transactions not handled in a legal

manner.

4. To determine if all retired stock has

been cancelled.

Same as 3.

5. To determine if any stock issues,

retirements, or dividends were

authorized.

Unauthorized or omitted equity

transactions.

6. To verify that earnings per share

has been correctly computed.

Incorrect earnings per share computation.

7. To determine that dividends are

legal and disclosure in the financial

statements is proper.

Illegal payments of dividends and improper

disclosure of the information in the

financial statements.

22–29 a. The audit program for the audit of Pate Corporation’s capital stock

account would include the following procedures:

1. Examine the articles of incorporation, the bylaws, and the

minutes of the board of directors from the inception of the

corporation to determine the provisions or decisions regarding

the capital stock, such as classes of stock, par value or

22–16

22–29 (continued)

2. Examine the stock certificate stub book and determine

whether the total of the open stubs agrees with the Capital

Stock account in the general ledger. Examine cancelled

stock certificates, which are generally attached to the

corresponding stub.

Information on the stubs regarding the number of

shares, date, etc. for both outstanding and cancelled stock

certificates should be compared with the Capital Stock

account. All certificate numbers should be accounted for

3. Analyze the capital stock account from the corporation’s

inception and verify all entries. Trace all transactions involving

the transfer of cash either to the cash receipts or the cash

disbursements records. If property other than cash was

received in exchange for capital stock, trace the recording

of the property to the proper asset account and consider

the reasonableness of the valuation placed on the property.

Transactions showing the sale of stock at a discount

or premium should be traced to the capital contributed in

excess of par value account. If capital stock has been sold

account are verified. If an entry is not related to capital

stock account entries, as in the case of a write–off of a deficit

as the result of a quasi–reorganization, authorization for

the entry and the supporting material should be examined.

22–17

22–29 (continued)

retained earnings account:

i. Analyze the account from its inception. Consider the

validity of the amounts representing income or loss

that were closed from the profit and loss account.

Amounts representing appraisal increments or writing

of the balance sheet.

ii. Any extraordinary gains or losses carried directly to

reviewed for reasonableness, and authorization for

the entries should be traced to the proper authority.

traced to the minutes of the board of directors for

authorization and traced to the cash account or the

capital stock account. A separate computation should

be made by the CPA of the total amount of dividends

b. In conducting his or her audit, the CPA verifies retained earnings

as he or she does other items on the balance sheet for several

22–18

22–29 (continued)

treatment that may have been contrary to accounting standards;

his or her audit of retained earnings would bring this noncompliance

to his or her attention.

Still another reason for verifying the retained earnings account

from transactions free from any restrictions.

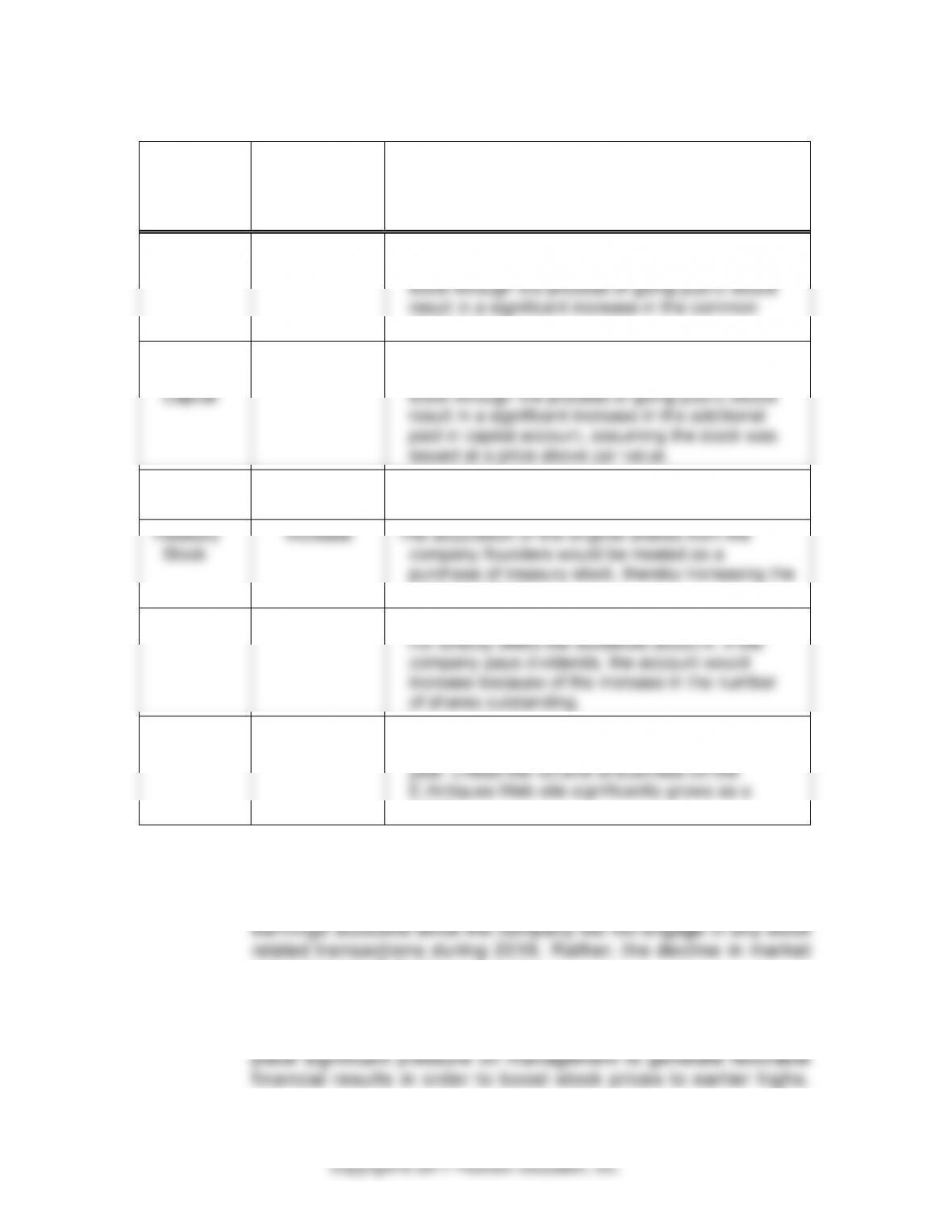

22–30 a.

ACCOUNT

EXPECTED

CHANGE IN

BALANCE

2014 TO 2015

EXPLANATION FOR

EXPECTED CHANGE IN BALANCE

Cash

Increase

While much of the proceeds were used to reduce

debt and purchase hardware and software,

unused proceeds were deposited in company

bank accounts.

Accounts

Receivable

Little Change

The process of becoming publicly held would

likely have minimal impact on accounts

receivable, unless the volume of business on the

E–Antiques Web site significantly grows as a

result of going public.

Property,

Plant, and

Equipment

Increase

Because stock proceeds were used to purchase

hardware and software, the balance in property,

plant, and equipment would be expected to

increase.

Accounts

Payable

Increase

Assuming the purchase of hardware and software

is made on account, the balance in accounts

payable would be expected to increase.

Long–Term

Debt

Decrease

Because stock proceeds were used to pay off

loans, the balance in long–term debt would be

expected to decrease.

22–19

22–30 (continued)

ACCOUNT

EXPECTED

CHANGE IN

BALANCE

2014 TO 2015

EXPLANATION FOR

EXPECTED CHANGE IN BALANCE

Common

Stock

Increase

Despite using stock proceeds to acquire original

shares from company founders, the issuance of

stock through the process of going public would

result in a significant increase in the common

stock account.

Additional

Paid–in

Capital

Increase

Despite using stock proceeds to acquire original

shares from company founders, the issuance of

stock through the process of going public would

result in a significant increase in the additional

paid in capital account, assuming the stock was

issued at a price above par value.

Retained

Earnings

No Change

The transactions associated with going public

would not affect the retained earnings account.

Treasury

Stock

Increase

The acquisition of the original shares from the

company founders would be treated as a

purchase of treasury stock, thereby increasing the

account balance.

Dividends

No Change

The transactions associated with going public would

not directly affect the dividends account. If the

company pays dividends, the account would

increase because of the increase in the number

of shares outstanding.

Revenues

Little Change

The process of becoming publicly held would likely

have minimal impact on revenues for the current

year, unless the volume of business on the

E–Antiques Web site significantly grows as a

result.

b. While the decline in stock market price to $19 per share is not

favorable news for E–Antiques, that decline would have no impact

on the common stock, additional paid–in capital, or retained

value impacts E–Antiques investors.

c. The decline in stock price would likely increase the auditor’s

assessment of business risk and audit risk. The decline is likely to

22–20

22–30 (continued)

22–31 a. The three distinct tiers of the NASDAQ market are The NASDAQ

Global Select Market®, The NASDAQ Global Market®, and The

NASDAQ Capital Market®. The NASDAQ Global Select Market®

has the most stringent listing requirements.

1,250,000 publicly held shares.

c. The four standards for the NASDAQ Global Market® are:

1. Income Standard

2. Equity Standard

3. Market Value Standard

4. Total Assets/Total Revenue Standard

400 round lot shareholders.

d. Securities issuances that require shareholder approval include:

Acquisitions where the issuance equals 20% or more of the

pre–transaction outstanding shares (or 5% or more of the

pre–transaction outstanding shares when a related party

Issuances involving equity compensation.