Substantive analytical procedures performed during the testing phase of the audit

A) are required under generally accepted auditing standards.

B) are always done independently from other audit procedures.

C) are used as a substantive test in support of account balances.

D) do not need to be documented in the working papers.

Inherent risk is often high for an account such as

A) inventory.

B) land.

C) capital stock.

D) notes payable.

In which of the following circumstances would a CPA be ethically bound to refrain

from disclosing any confidential client information?

A) The CPA is issued a summons enforceable by a court order which orders the CPA to

present confidential information.

B) A major stockholder of a client company seeks accounting information from the CPA

after management declined to disclose the requested information.

C) The confidential client information is made available as part of a quality review of

the CPA’s practice by a peer review team authorized by the AICPA.

D) An inquiry by a disciplinary body of a state CPA society requests confidential client

information.

The auditor is performing tests of transactions for individual accounts payable

transactions with vendors. Which document provides more reliable information about

individual transactions with vendors?

A) receiving report

B) vendors’ invoices

C) vendors’ statements

D) purchase orders

Smith Manufacturing Company’s accounts receivable clerk has a friend who is also a

customer of Smith Manufacturing. The accounts receivable clerk has issued fictitious

credit memos to his friend for goods supposedly returned. The most effective procedure

for preventing this activity is to

A) prenumber and account for all credit memorandums.

B) require receiving reports that provide evidence of returned inventory items to

support all credit memorandums before they are approved.

C) have independent sales and accounts receivable departments.

D) mail monthly statements to customers.

When a company maintains its own records of stock transactions and outstanding stock,

internal controls must be adequate to ensure that

A) actual owners are recorded in the bylaws.

B) the correct amount of dividends is paid to stockholders owning the stock on the

dividend record date.

C) the correct amount of dividends is paid to stockholders owning the stock on the

declaration date.

D) actual owners are recorded in the minutes.

The standard inquiry to the client’s attorney should be prepared on

A) plain paper (no letterhead) and be unsigned.

B) lawyer’s stationery and signed by the lawyer.

C) auditor’s stationery and signed by an audit partner.

D) client’s letterhead and signed by a company official.

Which of the following audit procedures would be the most effective in testing for

nonexistent employees?

A) Trace transactions recorded in the payroll journal to the human resources department

to determine employment status.

B) Examine cancelled checks for proper endorsement.

C) Recalculate net pay.

D) Reconcile the disbursements in the payroll journal with the disbursements on the

payroll bank statement.

Dracule Industries is a privately owned business that sells medical product and devices

to hospitals, clinics and the public. Certain changes have occurred in Dracule Industries

during the year undergoing the audit. Harker needs to evaluate the effect these changes

have on audit risk. Audit risk at the financial statement level is influenced by the risk of

material misstatement; which include factors related to management, the industry and

the entity or a combination thereof. For each of the following changes that have

occurred during the year under audit identify the appropriate audit response for the list

of responses. Each response can be used once, more than once or not at all.

Client changes: 1. An internal audit department has been established. 2. A new

inventory control system has been installed that reduces the access of unauthorized

parties. 3. Inexperienced accounting personnel were hired in the accounting department.

4. Excess cash was used to purchase complex derivatives. 5. Controls over the sales

credit approval process have laxed. 6. New government regulations now apply to

Dracule Industries. 7. Management has become overly aggressive in reaching target

goals. 8. An expert was hired to help determine the value of the ore content in ending

materials inventory. Possible effect on the audit: a. increase the acceptable level of

detection risk. b. decrease the acceptable level of detection risk. c. change has no effect

on the acceptable level of detection risk.

The five steps in applying materiality are listed below in random order.

1. Estimate the combined misstatement.

2. Estimate the total misstatement in the segment.

3. Set materiality for the financial statements as a whole.

4. Determine performance materiality.

5. Compare combined estimate with preliminary judgment about materiality.

The first three steps in correct sequence would be

A) 1, 2, 5

B) 3, 4, 2

C) 2, 1, 5

D) 3, 2, 4

Which of the following accounts would normally not be a part of the acquisition and

payment cycle of prepaid insurance?

A) cash

B) insurance payable

C) insurance expense

D) prepaid insurance

Which one of the following is not a major difference between operational and financial

auditing?

A) purpose of the audit

B) distribution of the report

C) testing the effectiveness of internal controls

D) inclusion of nonfinancial areas

A(n) ________ is a supporting schedule that supports a specific amount and is normally

expected to tie the amount recorded in the client’s records to another source of

information.

A) reconciliation of amounts

B) analysis

C) summary of procedures

D) informational document

The dollar amount of some misstatements cannot be accurately measured. For example,

if the client were unwilling to disclose an existing lawsuit, the auditor must estimate the

likely effect on

A) net income.

B) users of the financial statements.

C) the auditor’s exposure to lawsuits.

D) management’s future decisions.

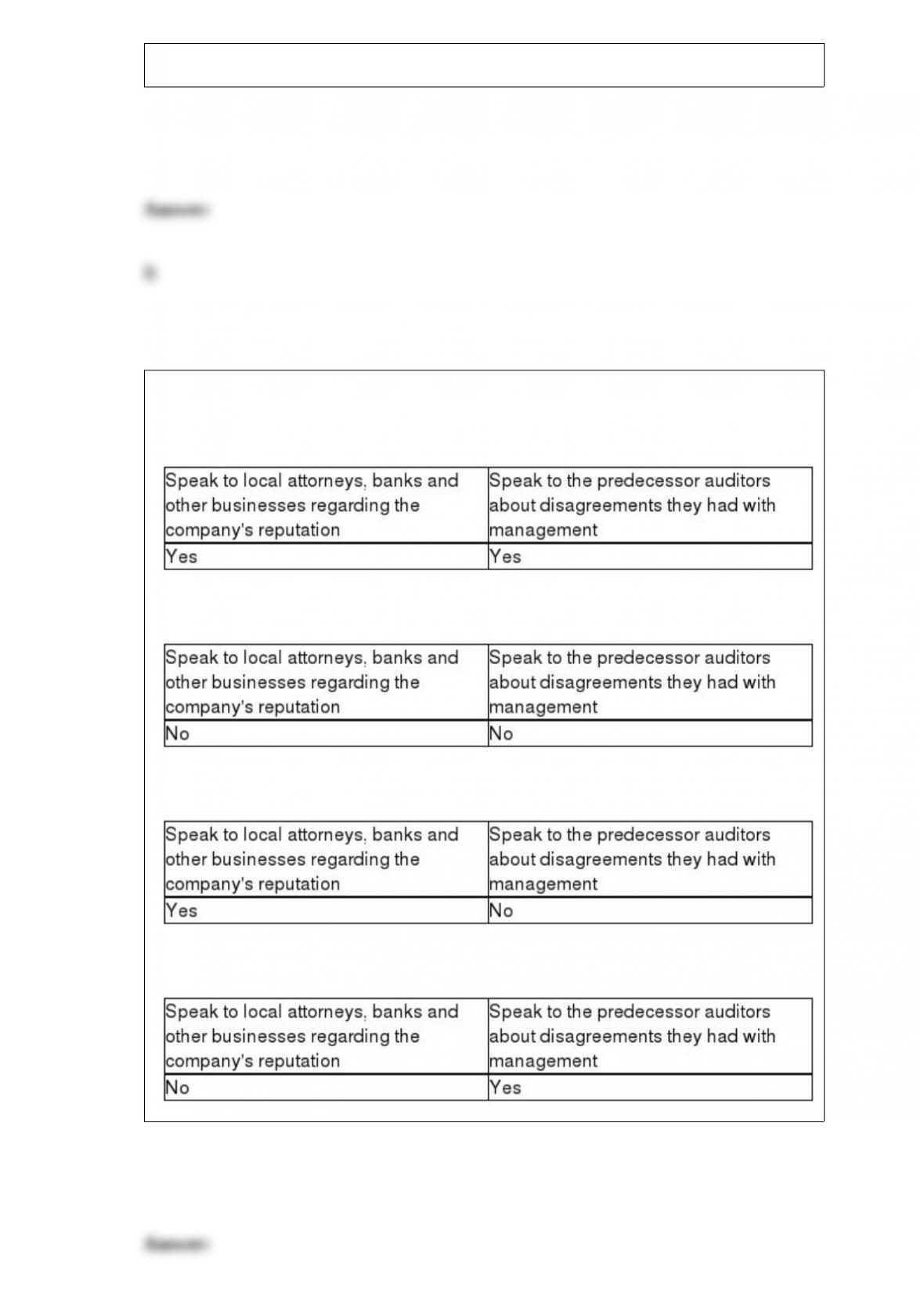

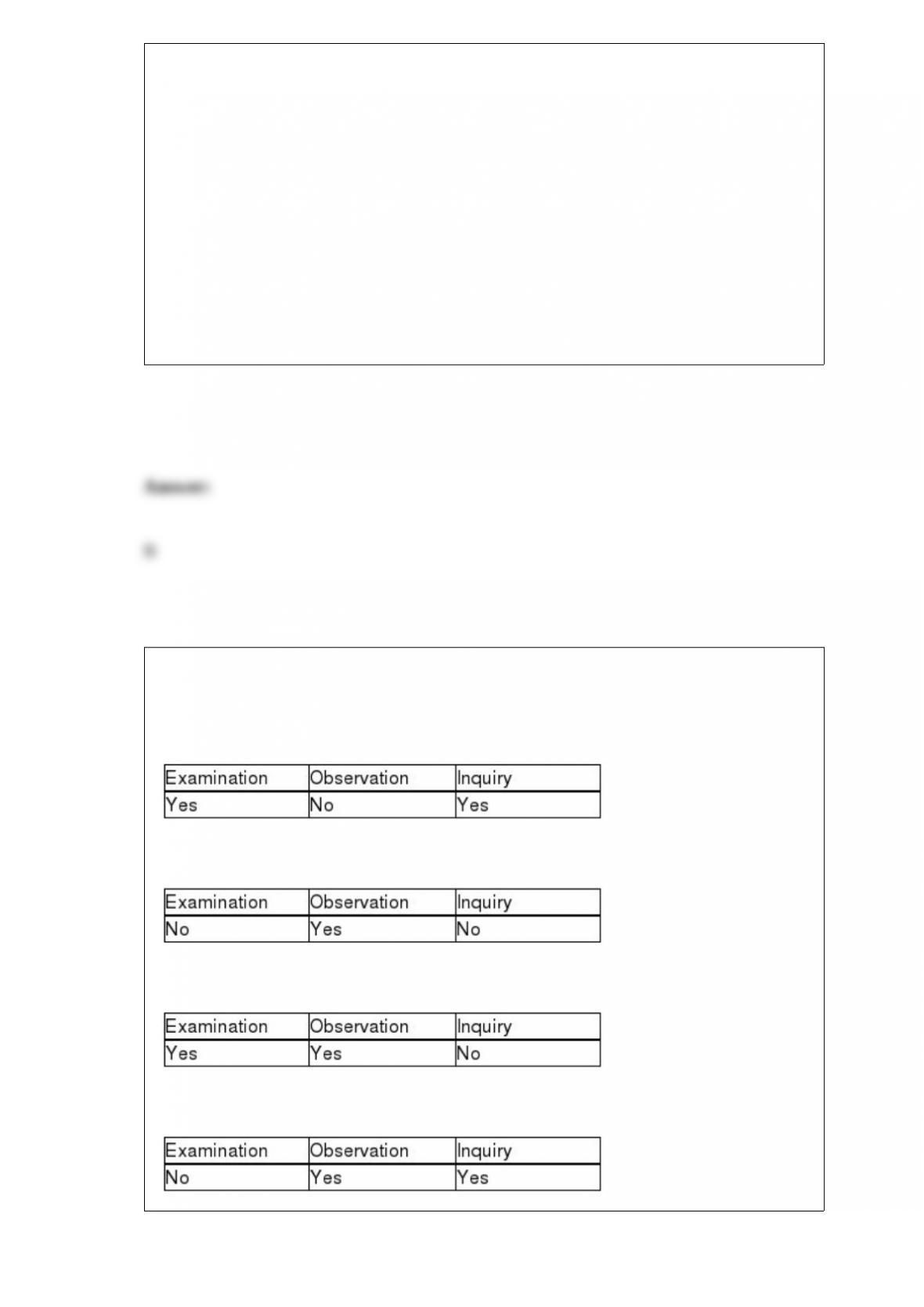

A successor auditor may perform which of the following for a new audit client?

A)

B)

C)

D)

When the auditor sends a confirmation to the broker-dealer, they are testing the

balance-related audit objective of

A) detail tie-in.

B) existence.

C) cutoff.

D) rights.

A major source of cutoff information for sales and purchases of inventory is

A) confirmations from outside parties.

B) the test of details of balances.

C) physical observation.

D) the performance of analytical procedures.

Which of the following is an accurate statement regarding audit risk, audit failure, and

business failure?

A) Audit risk is always avoidable if the audit is conducted in accordance with generally

accepted auditing standards.

B) Because auditors gather evidence on a test basis, and because well-concealed frauds

are difficult to detect, audit risk is unavoidable.

C) Legal precedent makes it easy to determine who has the right to recover losses in the

event of an audit failure.

D) A business failure will always result in an audit failure.

Auditor tests of physical controls over raw materials, work-in-process, and finished

goods are performed by

A)

B)

C)

D)

The reliability of perpetual inventory master files affects the timing and ________ of

the auditor’s physical examination of inventory.

A) cutoff

B) accuracy

C) nature

D) extent

For cash receipts, the occurrence transaction-related audit objective affects which of the

following balance-related audit objectives?

A) existence

B) completeness

C) rights

D) detail tie-in

Which of the following would generally not be a component of the audit of the

acquisition and payment cycle?

A) adequacy of controls over acquisitions of long-lived assets

B) tracing disposals of long-lived assets to the fixed asset master file

C) determining the adequacy of the funds available for capital expenditures

D) reperformance of recorded depreciation expense

A procedure designed to test for monetary misstatements directly affecting the

correctness of financial statement balances is a

A) test of controls.

B) substantive test.

C) test of attributes.

D) monetary unit sampling test.

An auditor is reconciling the amounts included in the long-term debt footnotes to the

information examined and supported in the audit files for long-term debt. Which audit

objective is being satisfied?

A) accuracy and valuation

B) occurrence and rights and obligations

C) completeness

D) classification and understandability

The concept of limited assurance is provided for in which of the following

engagements?

A) audit

B) review

C) compilation

D) agreed-upon procedures

When performing a review service, auditors must make inquiries of management.

Which of the following inquiries are typically made of management?

A) Is each account on the financial statements prepared in conformity with accounting

standards and consistently applied?

B) What unusual or significant transactions occurred this year?

C) Do you have knowledge of an actual or suspected fraud?

D) All of the above are inquiries typically made of management.

Which of the following is true with regards to the various auditing standards?

A) Statements on Auditing Standards (SASs) are issued by the PCAOB.

B) The ASB Clarity Project was intended to make the U.S. auditing standards easier to

read, understand, and apply.

C) The ASB redrafted existing AICPA auditing standards to align them with respective

ISAs.

D) Both B and C are correct.

An adverse opinion is issued when the auditor believes

A) some parts of the financial statements are materially misstated or misleading.

B) the financial statements would be found to be materially misstated if an investigation

were performed.

C) the auditor is not independent.

D) the overall financial statements are so materially misstated that they do not present

fairly the financial position or results of operations and cash flows in conformity with

GAAP.

The tests of details of balances procedure which requires the auditor to trace the totals

of the notes payable list to the general ledger satisfies the audit objective of

A) accuracy.

B) existence.

C) detail tie-in.

D) completeness.

Which of the following is the best reason for management to emphasize fraud

prevention and deterrence?

A) It is often more effective and economical for companies to focus on fraud prevention

and deterrence rather than on fraud detection.

B) Collusion is impossible to detect.

C) The AICPA requires management to implement a fraud prevention program.

D) All of the above are equally valid reasons.

An audit procedure that compares the name, amount, and dates shown on remittance

advices with cash receipts journal entries and with related duplicate deposit slips would

be effective in detecting

A) kiting.

B) lapping.

C) unauthorized write-offs of customers as uncollectible accounts.

D) sales without proper credit authorization.

You are auditing the inventory account and are concerned about the possibility of an

inventory overstatement. What is the best audit procedure to detect damaged inventory?

A) Observe the condition of inventory during the client’s physical count.

B) Compare the condition of inventory from the previous year’s count to the current

year.

C) Compare inventory turnover from the previous year’s inventory to the current year’s

inventory.

D) Reconcile the inventory counts to the cost accounting records.

Which of the following is not one of the four decisions about what evidence to gather

and how much of it to accumulate?

A) which audit procedures to use

B) which accounts must agree to the general ledger

C) when to perform the procedures

D) what sample size to select for a given procedure