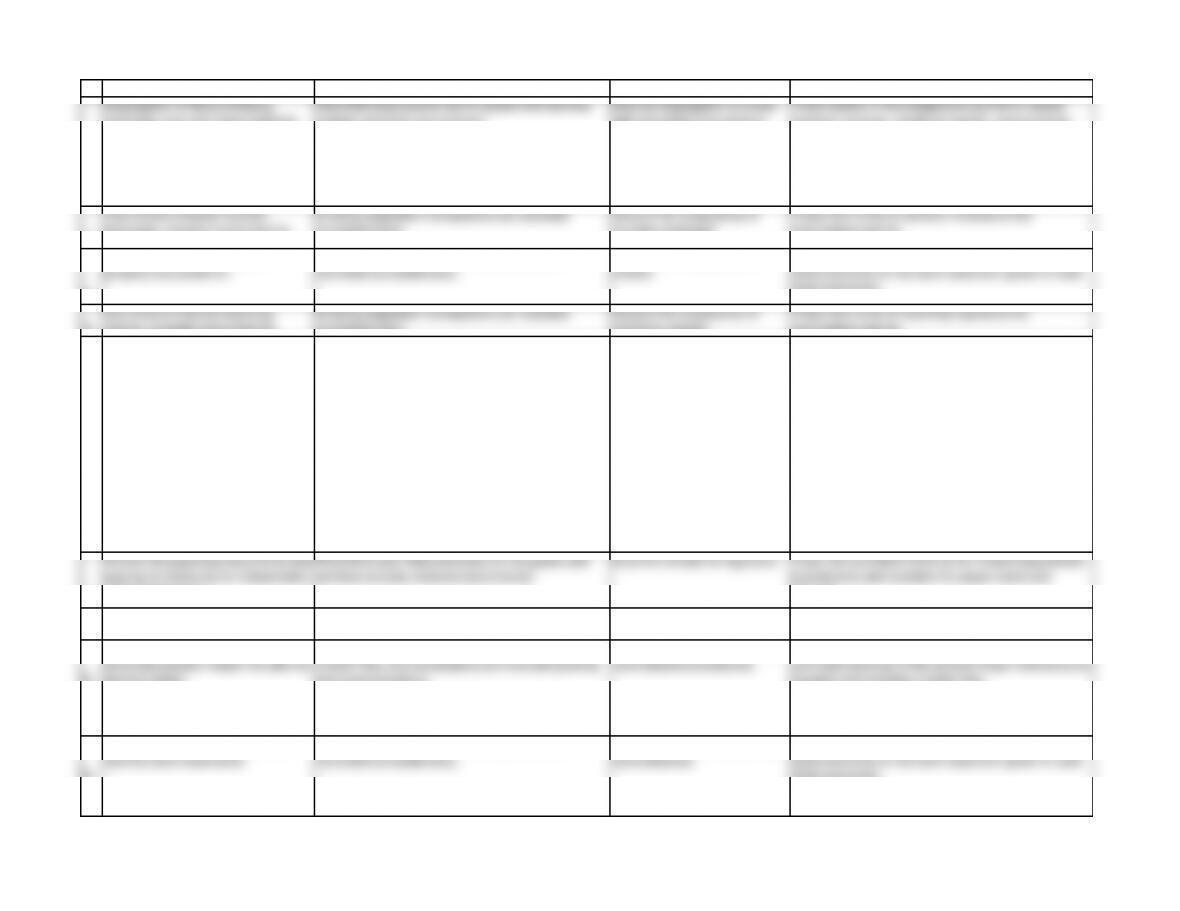

# a. Key Internal Control b. Transaction Related Audit Objectives c. Test of Control d. Substantive Test of Transaction

1.

Segregation of the purchasing,

receiving, and cash disbursements

functions.

Recorded acquisitions are for goods and services

actually received (occurrence).

Discuss segregation of duties

with personnel and observe

activities.

Trace entries in the acquisitions journal to related

vendors’ invoices, receiving reports, and purchase

orders.

Recorded cash disbursements are for goods and

services actually received (occurrence).

2.

Use of prenumbered voucher

packages, properly accounted for.

Existing acquisition transactions are recorded

(completeness).

Account for a sequence of

voucher packages.

Trace from a file of vendors’ invoices to the

acquisitions journal.

3.

Use of prenumbered checks,

properly accounted for.

Existing cash disbursement transactions are

recorded (completeness).

Account for a sequence of

checks.

Reconcile recorded cash disbursements with the cash

disbursements on the bank statement (proof of cash

disbursements).

4.

Use of prenumbered receiving

reports, properly accounted for.

Existing acquisition transactions are recorded

(completeness).

Account for a sequence of

receiving reports.

Trace from a file of receiving reports to the

acquisitions journal.

5.

Internal verification of document

package before check preparation.

Recorded acquisitions are for goods and services

actually received (occurrence).

Examine document package

for indication of internal

verification.

Examine supporting documents for propriety and

recompute information on the supporting documents.

Recorded acquisitions are stated at the correct

amounts (accuracy).

Acquisition transactions are properly included in the

master files, and are properly summarized (posting

and summarization).

Acquisitions are properly classified (classification).

Acquisitions are recorded on the correct dates

(timing).

6.

Review of supporting documents and

signing of checks by an independent,

authorized person.

Recorded cash disbursements are for goods and

services actually received (occurrence).

Examine checks for signature.

Trace the cancelled check to the related acquisitions

journal entry and examine for payee name and

amount.

7.

Cancellation of documents prior to

signing of the check.

Recorded acquisitions are for goods and services

actually received (occurrence).

Examine indication of

cancellation.

Examine the acquistions journal for duplicate entries

to a vendor.

8.

Monthly reconciliation of the

accounts payable master file with the

general ledger.

Acquisition transactions are properly included in the

master files, and are properly summarized (posting

and summarization).

Inquire of client about monthly

reconciliation procedures.

Foot acquisitions and cashdisbursements journals

and trace postings to the general ledger and accounts

payable and inventory master files.

Cash disbursement transactions are properly

included in the master file, and are properly

summarized (posting and summarization).

9.

Independent reconciliation of the

monthly bank statements.

Existing cash disbursement transactions are

recorded (completeness).

Examine file of completed bank

reconciliations.

Reconcile recorded cash disbursements with the cash

disbursements on the bank statement (proof of cash

disbursements).

Recorded cash disbursement transactions are

stated at the correct amounts (accuracy).