Both SEC rules and the Sarbanes-Oxley Act prohibit auditors from providing

bookkeeping services to their public company audit clients.

All owners of a CPA firm must be CPAs who are qualified to practice.

Errors are usually more difficult for an auditor to detect than frauds.

An acceptable audit risk assessment of low indicates a risky client requiring more

extensive evidence, assignment of more experienced personnel, and/or a more extensive

review of audit files.

Since the amount of expense report reimbursements is insignificant, auditors can ignore

expense reports for officers and directors.

Audit committee oversight also serves as a deterrent to fraud by senior management.

Many litigation experts believe that a well written engagement letter significantly

reduces the likelihood of adverse legal actions.

The overall objective in the audit of the sales and collection cycle is to evaluate whether

the account balances affected by the cycle are fairly presented in accordance with

accounting standards.

Effectiveness is concerned with whether defined goals are achieved, whereas efficiency

is concerned with whether the goals are achieved with a minimum use of resources.

When an auditor sets a low acceptable audit risk, it means that he wants to be more

certain that the financial statements are not materially misstated.

The transaction-related audit objective that deals with whether recorded transactions

have actually occurred is the completeness objective.

The criteria by which an auditor evaluates the information under audit may vary with

the information being audited.

The auditor performs tests of controls and substantive procedures to obtain assurance

that all audit objectives are achieved for information and amounts included in those

disclosures.

Audit documents are the joint property of the auditor and the audit client.

Separation of duties in the payroll and personnel cycle will prevent overpayments, but

not payments to nonexistent employees.

Current professional auditing standards prohibit external auditors from using internal

auditors for direct assistance on external audits.

The letter of representation is prepared on the CPA firm’s letterhead, addressed to the

client’s chief executive officer, and signed by the audit engagement partner.

Whenever an auditor issues a qualified report, he or she must use the term “except for ”

in the opinion paragraph.

If a sale was for a valid shipment, but the amount of the sales invoice was calculated

incorrectly, the accuracy objective was violated.

The auditor must obtain evidence that the interim financial information agrees or

reconciles with the accounting records for a public company interim review.

The most difficult type of cash embezzlement for the auditor to detect is when the cash

is stolen before it can be recorded in the cash receipts journal.

When auditing acquisitions of property, plant, and equipment, the auditor’s review of

lease and rental agreements most closely relate to the cutoff objective.

Cost accounting systems and controls are the same for all manufacturing companies.

An example of a specific authorization is management setting a policy authorizing the

ordering of inventory when less than a one-week supply is on hand.

The auditor’s understanding of internal control performed as part of risk assessment

procedures provides the basis for the auditor’s initial assessment of control risk.

A CPA firm may use any name as long as it is not misleading.

Parallel testing can be used in combination with pilot testing to test new systems.

There has been an increased emphasis on the use of analytical procedures during an

audit.

The presence of fraud risk factors increases the likelihood of fraud and may suggest that

fraud is being perpetrated.

Audit risk is the risk there will be an audit failure for a given audit engagement.

As society becomes more complex, decision makers are more likely to receive reliable

information.

If a particular internal control is not followed by the client exactly 6% of the time, and

the auditor’s tests of that control find three control violations in a sample of 50, the

sample is considered to be representative.

Tests of the presentation and disclosure-related objectives are generally done as part of

the completion phase of the audit.

Who is responsible for establishing a private company’s internal control?

A) senior management

B) internal auditors

C) FASB

D) audit committee

Which one of the following best describes the auditors responsibilities regarding

appropriate authorizations in the sales/collections cycle?

A) Credit must be authorized before the sale.

B) Goods must be shipped after the authorization

C) Prices must be authorized.

D) All of the above should be of concern to the auditor.

Which of the following would the auditor be most concerned about regarding a

heightened risk of intentional misstatement?

A) Senior management emphasizes that it is very important to beat analyst estimates of

earnings every reporting period.

B) Senior management emphasizes that budgeted amounts for expenses are to be

achieved for each reporting period or explained in the variance analysis report.

C) Senior management emphasizes that job rotation is a worthwhile corporate

objective.

D) Senior management emphasizes that job evaluations are based on performance.

A sample in which every possible combination of items in the population has an equal

chance of constituting the sample is a

A) random sample.

B) statistical sample.

C) judgment sample.

D) representative sample.

A liability is properly accounted for as an account payable if

A) the amount is known and owed as of the balance sheet date.

B) the amount can be estimated and is owed at the balance sheet date.

C) the amount is known at the balance sheet date and owed by the end of the next fiscal

year.

D) the amount is estimated and owed within 90 days of the balance sheet date.

The purpose of the requirement in having communication between the predecessor and

successor auditors is to

A) allow the predecessor to disclose information which would otherwise be

confidential.

B) help the successor auditor to evaluate whether to accept the engagement.

C) help the client by facilitating the change of auditors.

D) ensure the predecessor collects all unpaid fees prior to a change in auditor.

Which of the following types of receivables would not deserve the special attention of

the auditor?

A) accounts receivables with credit balances

B) accounts that have been outstanding for a long time

C) receivables from related parties

D) each of the above would receive special attention.

When performing planning analytical procedures for a client the auditor detected that

the gross profit percentage had declined by 50% from the previous year to the year

currently under audit. The auditor should

A) investigate the possibility the client may have made an error in their cost of goods

sold computation.

B) assist management in developing greater cost efficiencies in their product line.

C) prepare a going concern opinion for the client.

D) advise the client to have extensive disclosure to alleviate investor concerns.

An auditor traces a sample of electronic time cards before and after the bi-weekly

payroll report and then traces to the payroll master file to determine that payroll

transactions are reported in the correct period. The auditor is gathering evidence for

which audit objective?

A) completeness

B) existence

C) cut-off

D) accuracy

A CPA firm normally uses one or a combination of four defenses when there are legal

claims by clients. Which one of the following is generally not a defense?

A) lack of duty

B) nonnegligent performance

C) contributory negligence

D) foreseeable users

According to the Association of Certified Fraud Examiners, the average company loses

________ percent of its revenues to fraud.

A) one

B) five

C) ten

D) fifteen

Which of the following statements is the most correct regarding errors and fraud?

A) An error is unintentional, whereas fraud is intentional.

B) Frauds occur more often than errors in financial statements.

C) Errors are always fraud and frauds are always errors.

D) Auditors have more responsibility for finding fraud than errors.

An engagement letter sent to a publicly held audit client usually would not include a(n)

A) reference to the auditor’s responsibility for the detection of errors or irregularities.

B) estimation of the time to be spent on the audit work by audit staff and management.

C) statement that management advisory services would be made available upon request.

D) reference to management’s responsibility for the financial statements.

Auditors compare client data with

A) industry data.

B) client-determined expected results.

C) similar prior-period data.

D) all of the above.

When selecting a sample size for substantive tests of balances which factor, other

factors being equal, would result in a larger sample?

A) a decrease in the tolerable misstatement

B) small expected misstatements

C) an increase in the tolerable misstatement

D) an increase in the acceptable risk of incorrect acceptance

Responsibility for the issuance of new notes payable would normally be vested in the

A) board of directors.

B) purchasing department.

C) accounting department.

D) accounts payable department.

The possibility that a business may not be able to repay a bank loan because of an

economic downturn is referred to as

A) materiality risk.

B) information risk.

C) interest rate risk.

D) business risk.

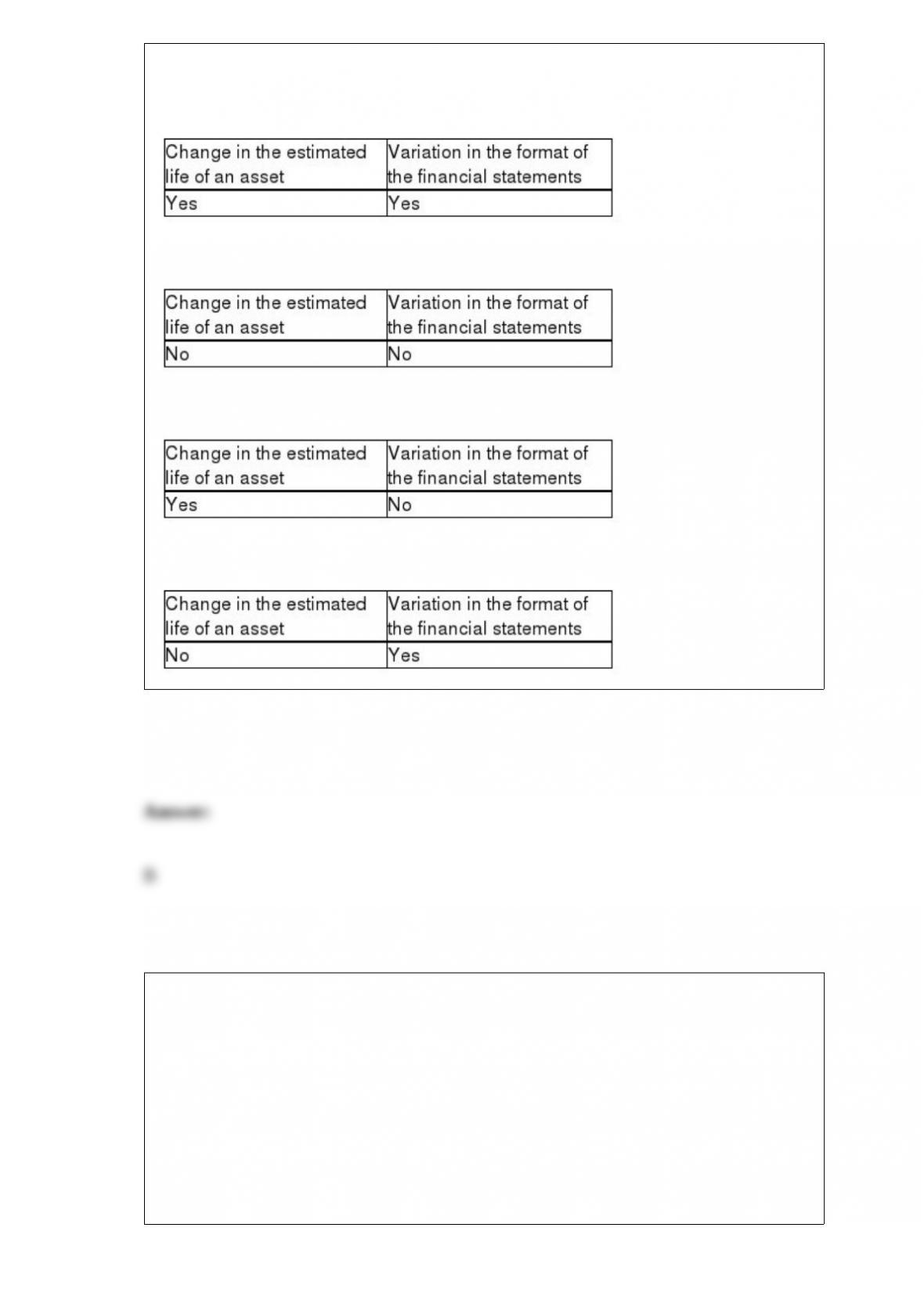

Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

The most commonly used method of statistical sampling for tests of details of balances

is

A) attributes sampling.

B) systematic sampling.

C) discovery sampling.

D) monetary unit sampling.

The audit tests to verify that the client is using an inventory method which is generally

accepted and to verify that physical counts were correctly summarized are performed

during the audit of the

A) acquisition and payments cycle.

B) payroll and personnel cycle.

C) inventory and warehousing cycle.

D) sales and collection cycle.

Cutoff misstatements occur when

A)

B)

C)

D)

Which of the following is not a key control in the acquisition and payment cycle?

A) authorization of purchases

B) authorization of credit

C) timely recording and independent review of transactions

D) authorization of payments

The AICPA principles underlying an audit are organized around four principles. Which

of the following is not one of those principles?

A) fairness

B) responsibilities

C) reporting

D) performance

Which of the following is most correct regarding external auditors use of internal

auditors directly on the audit engagement?

A) discourage

B) prohibit

C) require

D) permit

After a purchase requisition is approved, a ________ must be initiated to purchase the

goods or services.

A) purchase order

B) vendor order

C) call order

D) vendor invoice

All of the following are causes for the addition of an explanatory paragraph under both

AICPA and PCAOB standards except for

A) emphasis of a matter.

B) reports involving other auditors.

C) lack of consistent application of generally accepted accounting principles.

D) auditor agrees with a departure from promulgated accounting principles.

After the balance sheet date but prior to issuance of the auditor’s report the auditor

learns that the client’s facility in a foreign country has been expropriated. Management

refuses to disclose this information in a financial statement footnote or present

pro-forma data as to the effect of the event. The auditor should

A) add a footnote to the financial statements.

B) disclaim an opinion due to the client imposed scope limitation.

C) provide the information in the report and modify the opinion.

D) issue an unqualified opinion but provide the information in the auditor report.

Controls which provide a means of ensuring that the physical counts are properly

summarized, priced at the same amount as the unit records, correctly extended and

totaled, and included in the general ledger at the proper amount are known as

A) standard cost controls.

B) pricing internal controls.

C) compilation internal controls.

D) count quantity internal controls.

Which of the following is not one of the responsibilities of an auditor under the

principles underlying an audit?

A) possess appropriate competence and capabilities

B) comply with ethical requirements

C) plan work and supervise assistants

D) maintain professional skepticism and exercise professional judgment

Which of the following is not one of the three primary objectives of effective internal

control?

A) reliability of financial reporting

B) efficiency and effectiveness of operations

C) compliance with laws and regulations

D) assurance of elimination of business risk

In many audits, no substantive tests of transactions are made for the ________ assertion

on the grounds that understatement of sales is not a concern.

A) accuracy

B) existence

C) completeness

D) none of the above

Recent academic research on the topic of professional skepticism suggests that there are

six characteristics to skepticism. List and briefly describe each of these characteristics.

There are eight types of audit evidence: physical examination, confirmation, inspection,

observation, inquiries of the client, reperformance, analytical procedures, and

recalculation. For each of the following types of audit tests, indicate the type(s) of

evidence that can be obtained through the test: (1) tests of controls, (2) substantive tests

of transactions, (3) analytical procedures, and (4) tests of details of balances.

In addition to performing analytical procedures that examine the relationship of

inventory account balances with related financial statement accounts, auditor’s will

often use nonfinancial measures in determining the reasonableness of inventory

balances. List below at least two nonfinancial measures that may be useful to auditors.

Auditors will often prepare a proof of cash when the client has material internal control

weaknesses in cash receipts and cash disbursements. The purpose of the proof of cash is

to determine the client’s accounting records for cash are reliable. List below the four

requirements the proof of cash is designed to provide for the auditor.

In the context of the audit of sales, distinguish between the occurrence and

completeness transaction-related audit objectives. State the effect on the sales account

(overstatement or understatement) of a violation of each objective.

Discuss at least 3 steps the AICPA and the accounting profession as a whole can and are

taking to reduce the practitioner’s exposure to lawsuits.

How do auditors determine the extent of testing of internal controls in the acquisition

and payment cycle?

Mathews and Company has $112,000 in an accrued payroll account. The company’s

weekly payroll is $186,700 and the accrual represents 3 days out of 5 working days. If

the auditor has determined that controls are effective over payroll, what additional work

should the auditor perform for this account?

Cutoff misstatements can occur for sales, sales returns, and cash receipts. List below the

threefold approach an auditor performs for each account above to determine the

reasonableness of the cutoff.

Control activities help assure that the necessary actions are taken to address risks to the

achievement of the company’s objectives. List the five types of control activities.

An environmental clean-up lawsuit is pending against your client. What information

about the lawsuit would you as the auditor need in order to determine the proper

accounting treatment?

Discuss the audit procedures performed when testing the detail tie-in objective for

accounts receivable, and explain why this objective is ordinarily tested before any other

objectives for accounts receivable.

There are 14 steps to audit sampling for tests of details of balances, divided into three

sections: plan the sample, select the sample and perform the audit procedures, and

evaluate the results. Discuss 5 of the 9 steps included in the “plan the sample” section

for nonstatistical sampling.

Internal controls over year-end cash balances in the general account can be divided into

two categories. List the two below.

“Failure to bill a customer” is an example of an error that results in the failure to receive

cash, but would not be discovered as part of the audit of the bank reconciliation. State

three other examples of errors or irregularities that result in the improper payment of, or

failure to receive, cash, but that would not be discovered during the audit of the bank

reconciliation. How are these types of misstatements normally uncovered in the audit?

Explain the decision rule used in monetary unit sampling to determine whether the

population is acceptable.

The primary accounting record for property, plant, and equipment accounts is the fixed

asset master file. What is included for each fixed asset in the master file?

Discuss the purposes of (1) substantive tests of transactions, (2) tests of controls, and

(3) tests of details of balances. Give an example of each.

Discuss each of the three types of compilation reports and the circumstances in which

each should be used.

What types of exceptions are auditors most concerned with when evaluating

populations of accounting data?