23-11

23–19 (continued)

c.

RECONCILING ITEM

AUDIT PROCEDURE

1. Deposits in transit

Trace to duplicate deposit slip and entry on

cutoff bank statement.

2. Erroneous check

Examine correction notice in August charge

received from bank.

3. Outstanding checks

Obtain cutoff bank statement. Trace

enclosed checks to outstanding check list.

Trace uncleared items to supporting

documentation.

4. Bank service charge

Examine advice returned with July bank

statement.

5. Note payment

Examine cancelled note. Recompute

interest. Check for absence of note on

7/31 bank confirmation.

6. NSF check

Examine advice returned with July bank

statement. Examine other related

evidence from credit manager to

determine if account is uncollectible.

7. Unrecorded check

Examine check returned with July bank

statement. Trace number to absence in

July cash disbursements journal and

recording in August. Examine supporting

documentation. Investigate why

unrecorded.

d. The correct cash balance for the financial statements is $1,950.

23–20 a. In verifying the interbank transfers, the following audit procedures

should be performed:

the balance sheet date (already done).

2. Trace these interbank transfers to the appropriate accoun–

b. For December 2016

Cash in bank $16,000

23-12

23–20 (continued)

Cash in bank 22,000

For January 2017

c. For December 2016

Home office clearing account $28,000

Cash in bank $28,000

For January 2017

Eliminate corresponding entries already made for the

above.

d.

and

e.

HOME OFFICE RECORDS

BRANCH ACCOUNT

RECORDS

17,000

No DIT*

No OC**

28,000

No DIT

No OC

16,000

No DIT

No OC

10,000

No DIT

OC

21,000

No DIT

No OC

22,000

No DIT

OC

39,000

No DIT

No OC

* DIT = Deposit in transit

** OC = Outstanding check

23-13

23–21

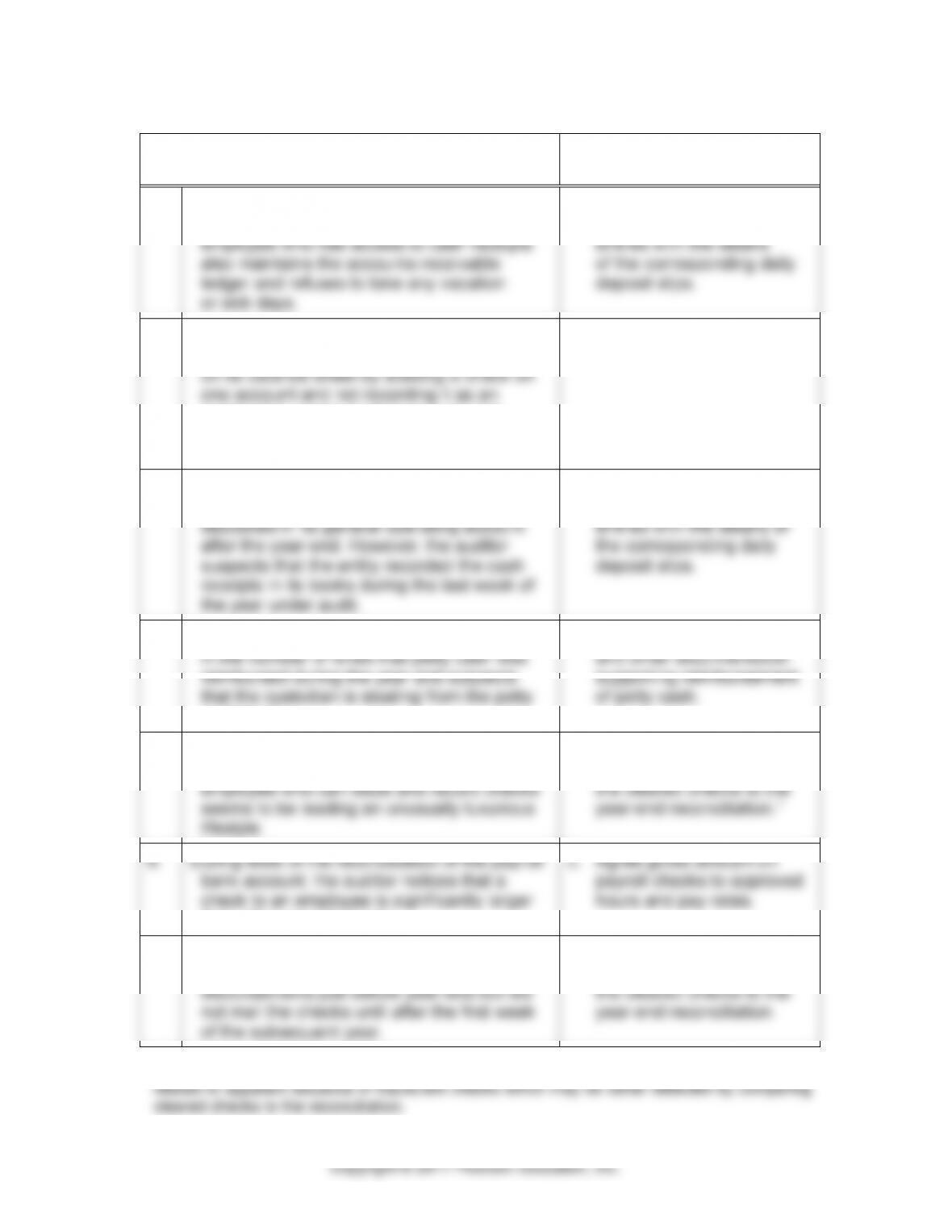

POSSIBLE MISSTATEMENTS

DUE TO ERRORS OR FRAUD

AUDIT PROCEDURE TO

PROVIDE EVIDENCE

1.

The auditor suspects that a lapping scheme

exists because an accounting department

employee who has access to cash receipts

also maintains the accounts receivable

ledger and refuses to take any vacation

or sick days.

a. Compare the details of

the cash receipts journal

entries with the details

of the corresponding daily

deposit slips.

2.

The auditor suspects that the entity is

inappropriately increasing the cash reported

on its balance sheet by drawing a check on

one account and not recording it as an

outstanding check on that account and

simultaneously recording it as a deposit in a

second account.

h. Prepare a bank transfer

schedule.

3.

The entity’s cash receipts of the first few

days of the subsequent year were properly

deposited in its general operating account

after the year–end. However, the auditor

suspects that the entity recorded the cash

receipts in its books during the last week of

the year under audit.

a. Compare the details of

the cash receipts journal

entries with the details of

the corresponding daily

deposit slips.

4.

The auditor noticed a significant increase

in the number of times that petty cash was

reimbursed during the year and suspects

that the custodian is stealing from the petty

cash fund.

e. Examine invoices, receipts,

and other documentation

supporting reimbursement

of petty cash.

5.

The auditor suspects that a kiting scheme

exists because an accounting department

employee who can issue and record checks

seems to be leading an unusually luxurious

lifestyle.

d. Obtain the cutoff bank

statement and compare

the cleared checks to the

year–end reconciliation.1

6.

During tests of the reconciliation of the payroll

bank account, the auditor notices that a

check to an employee is significantly larger

than other payroll checks.

c. Agree gross amount on

payroll checks to approved

hours and pay rates.

7.

The auditor suspects that the controller

wrote several checks and recorded the cash

disbursements just before year–end but did

not mail the checks until after the first week

of the subsequent year.

d. Obtain the cutoff bank

statement and compare

the cleared checks to the

year–end reconciliation.

1 An alternative answer would be to prepare a bank transfer schedule. In this case the kiting is

23-14

23–22 a.

Cash Disburse– Cash

9/30/16 Receipts ments 10/31/16

Balance per bank $6,915 $28,792 $27,431 $8,276

Deposits in transit

9/30/16 5,621 (5,621)

10/31/16 996 996

Outstanding checks

9/30/16 (1,811) (1,811)

10/31/16 2,615 (2,615)

b. Adjusting journal entries:

Dr. Cash in bank $ 3,296

Cr. Notes receivable $2,900

Cr. Interest income 396

23–23 a. A substitute check is a special paper copy of the front and back of

an original check, and is specially formatted so it can be processed

b. Because of Check 21 and other check–system improvements,

checks may be processed faster. The majority of consumers do not

receive their canceled checks with their account statements, but

Individuals who do receive canceled checks back in their

23-15

23–23 (continued)

c. No. In general, the law does not require the bank to return original

checks. Many banks destroy original paper checks. Other banks may

store original checks for some period of time and then destroy

23–24 a. Inherent risk is increased by the investment in speculative derivative

financial instruments due to the potential complexity of the derivative

contracts, the complexity of the relevant accounting standards,

increases inherent risk. Exposure to risk is significant because the

financial instruments account represents approximately 15% of

total assets, which is a material amount, and many of the equity

investments are considered high risk stocks.

on the CEO to show a profit from the investment strategy. The use

of a brokerage firm to execute trades lowers the control risk

assuming internal controls at the brokerage firm have been tested

and are considered effective.

review the underlying agreements.

c. It is difficult to test for completeness of derivative contracts as they

often do not involve an exchange of cash up front but represent a

commitment to perform in the future. To test completeness of the

23-16

23–24 (continued)

to the terms and whether there are any side agreements. To search

discussion of derivative contracts that are not recorded. The

auditor would also search following year–end for settlement of any

contracts that should have been recorded at year–end.

management to develop the fair value estimate. If the derivative

instrument is valued by management using a valuation model, the

auditor should obtain evidence by performing procedures such

as assessing the appropriateness of the model used and the

value estimate to transactions subsequent to year–end.

e. It is highly likely the auditor would use a valuation specialist for the

audit of financial instruments when level 3 fair value estimates are

valuation specialist to develop an estimate in order to corroborate

the estimates developed by management or their specialists.

23–25 a. The PCAOB reorganized their auditing standards effective

December 31, 2016. Before the reorganization, the relevant

in the reorganized standards as AS 2502.

23-17

23–25 (continued)

disclosures:

Controls over the process used to determine fair value

measurements, including, for example, controls over data and

the segregation of duties between those committing the entity to

the underlying transactions and those responsible for

undertaking the valuations.

fair value measurements.

The role that information technology has in the process.

The types of accounts or transactions requiring fair value

measurements or disclosures (for example, whether the

accounts arise from the recording of routine and recurring

transactions).

The extent to which the entity’s process relies on a service

organization to provide fair value measurements or the data that

supports the measurement. When an entity uses a service

organization, the auditor considers the requirements of AS

Organization, as amended.

The extent to which the entity engages or employs specialists in

determining fair value measurements and disclosures.

The significant management assumptions used in determining

fair value.

The documentation supporting management’s assumptions.

assumptions, including whether management used available

market information to develop the assumptions.

The process used to monitor changes in management’s

assumptions.

The integrity of change controls and security procedures for

valuation models and relevant information systems, including

approval processes.

the data used in valuation models.

c. According to paragraphs .21 and .22 of AS 2502, when planning to

use the work of a specialist in auditing fair value measurements,

the auditor should consider “whether the specialist’s understanding

23-18

23-25 (continued)

specialist for estimating the fair value of real estate or a complex

report of the specialist.

AS 1210, Using the Work of a Specialist, provides that,

“while the reasonableness of assumptions and the appropriateness

of the methods used and their application are the responsibility of

the specialist, the auditor obtains an understanding of the

procedures as required in AS 1210.”

d. According to paragraph .23 of AS 2502, the auditor’s substantive

tests of the fair value measurements may involve:

(i) testing management’s significant assumptions, the

evaluates whether:

a. Management’s assumptions are reasonable and reflect,

or are not inconsistent with, market information.

appropriate model, if applicable.

c. Management used relevant information that was

reasonably available at the time.

(ii) developing independent fair value estimates for

corroborative purposes. The auditor may make an

management’s assumptions, the auditor evaluates those

23-19

23-25 (continued)

audit evidence regarding management’s fair value

measurements as of the balance-sheet date. In such