Professional skepticism must be maintained only if the auditor suspects fraud.

Auditors use trends in the accounts receivable turnover ratio to assess the

reasonableness of the company’s credit policies.

Section 404 of the Sarbanes-Oxley Act requires public companies to have an external

auditor attest to their internal control over financial reporting.

Amounts involving fraud are not usually considered qualitative factors affecting the

preliminary materiality judgment.

The auditor’s first course of action when an illegal act is uncovered should be to

immediately notify the appropriate authorities, including but not limited to, law

enforcement and the Securities and Exchange Commission.

When a customer disagrees with the amount shown on an account receivable

confirmation, the auditor should not ask the client to reconcile the difference.

A CPA firm can issue a compilation report even if it is not independent with respect to

the client.

SOC 3 reports are prepared using the Trust Services principles.

Management’s philosophy and operating style influence the risk of material

misstatements in the financial statements.

WebTrust services are performed under the direction of the SSARS.

To test for overstatement cutoff amounts when auditing accounts payable, the auditor

should trace receiving reports issued before year-end to related vendors’ invoices to

make sure they are not recorded as accounts payable.

If a company uses a periodic inventory system, the shipping records are used to update

the inventory quantities.

Realizable value is an essential balance-related audit objective for accounts receivable.

Because of audit risk, some CPA firms now refuse any new clients in certain high-risk

industries.

In monetary unit sampling, the likelihood of high dollar items from the population

being included in the sample is lower than the likelihood for small dollar items.

Securities and contracts will typically be held by the broker-dealer.

Problems commonly encountered in the audit of prepaid insurance are not typical of the

problems found in other prepaid assets.

Relevant assertions have a meaningful bearing on whether the account is fairly stated

and are used to assess the risk of material misstatement and the design and performance

of audit procedures.

The formal name of the Yellow Book is Government Auditing Standards.

A lack of controls over payments to vendors can cause revenue fraud.

Review reports are normally dated as of the client’s balance sheet date.

Significant audit efficiencies can be achieved on many audits when controls are

operating effectively.

The same three defenses available to auditors in common lawsuits by third

partiesnonnegligent performance, lack of duty, and absence of causal connectionare also

available for suits under the Securities Exchange Act of 1934.

Auditors usually design bank confirmations that address the client’s specific

circumstances.

Physical examination is an essential type of evidence used to verify the existence and

count of inventory.

The Sarbanes-Oxley Act includes additional communication requirements for auditors

of public companies.

The receipt of raw materials is a part of the acquisition and payment cycle.

The annual reports of many public companies include a statement about management’s

responsibilities and relationship with the CPA firm.

To determine if the client has rights to the accounts receivable on the trial balance, the

auditor should inquire of management if any receivables are pledged or factored.

When auditing the year-end cash balance, one of the areas of focus is on the accuracy

objective.

Auditing standards require that the auditor presume that there is a risk of fraud in

revenue recognition.

Auditors can state the conclusions drawn from a confidence interval using statistical

inference in different ways.

A lack of independence will override any other scope limitations and requires a

disclaimer of opinion.

If the auditor concludes that the computer upper exception rate (CUER) is 5% at an 8%

sampling risk, this means that the exception rate in the population is no greater than 5%

with an 8% risk of the exception rate exceeding 5%.

When an auditor believes that an illegal act may have occurred, the first step he or she

should take is to gather additional evidence to determine the extent of the illegality and

if there is a direct impact on the financial statements.

Auditors can insist that the changes that they recommend as the result of an operational

audit be implemented by the company.

Members of the AICPA in public practice are prohibited from performing comparative

advertising.

The criterion used by most merchandising and manufacturing clients for determining

when revenue recognition takes place is whether title to the goods has passed.

Which of the following represents the best description of the tolerable exception rate?

A) the highest exception rate the auditor will permit in the control being tested and still

conclude it is operating effectively

B) the highest exception rate the auditor expects to find in the population

C) the number of exceptions found in the sample divided by the sample size

D) the highest estimated exception rate in a population at a given estimated population

exception rate.

A five-step approach can be used to identify deficiencies, significant deficiencies, and

material weaknesses. The first step in this approach is

A) identify the absence of key controls.

B) consider the possibility of compensating controls.

C) determine potential misstatements that could result.

D) identify existing controls.

When determining materiality,

A) the preliminary judgment about materiality can be increased, but not decreased

during the audit.

B) auditing standards provide specific materiality guidelines to practitioners.

C) only one benchmark can be used.

D) the application of guidelines requires considerable professional judgment.

The primary audit objectives to focus on when auditing accounts in the capital

acquisition and repayment cycle are

A) accuracy and completeness.

B) accuracy and existence.

C) completeness and valuation.

D) accuracy and valuation.

A review results in a conclusion that represents ________ assurance.

A) limited assurance

B) negative

C) positive

D) unequivocal

Which of the following statements is true?

A) Evidence must be relevant to all of the audit objectives.

B) If evidence is subjective, it cannot be reliable.

C) Evidence obtained directly by the auditor may not be reliable if the auditor lacks the

qualifications to evaluate the evidence.

D) The persuasiveness of evidence can be evaluated after considering its sufficiency.

An example of a physical control is

A) a hash total.

B) a parallel test.

C) the matching of employee fingerprints to a database before access to the system is

allowed.

D) the use of backup generators to prevent data loss during power outages.

When the auditor goes through a population and selects items using nonprobabilistic

selection methods, without regard to their size, source, or other distinguishing

characteristics, it is called

A) block sample selection.

B) haphazard selection.

C) systematic sample selection.

D) statistical selection.

An auditor is determining whether an issuance of notes payable for cash was correctly

recorded. Her best course of action would be to

A) confirm with the bond trustee as to the amount of bonds issued.

B) confirm with the underwriter as to the appropriate market yield on the bonds.

C) trace the cash received from the proceeds to the accounting records.

D) verify that the amount was included in a footnote disclosure.

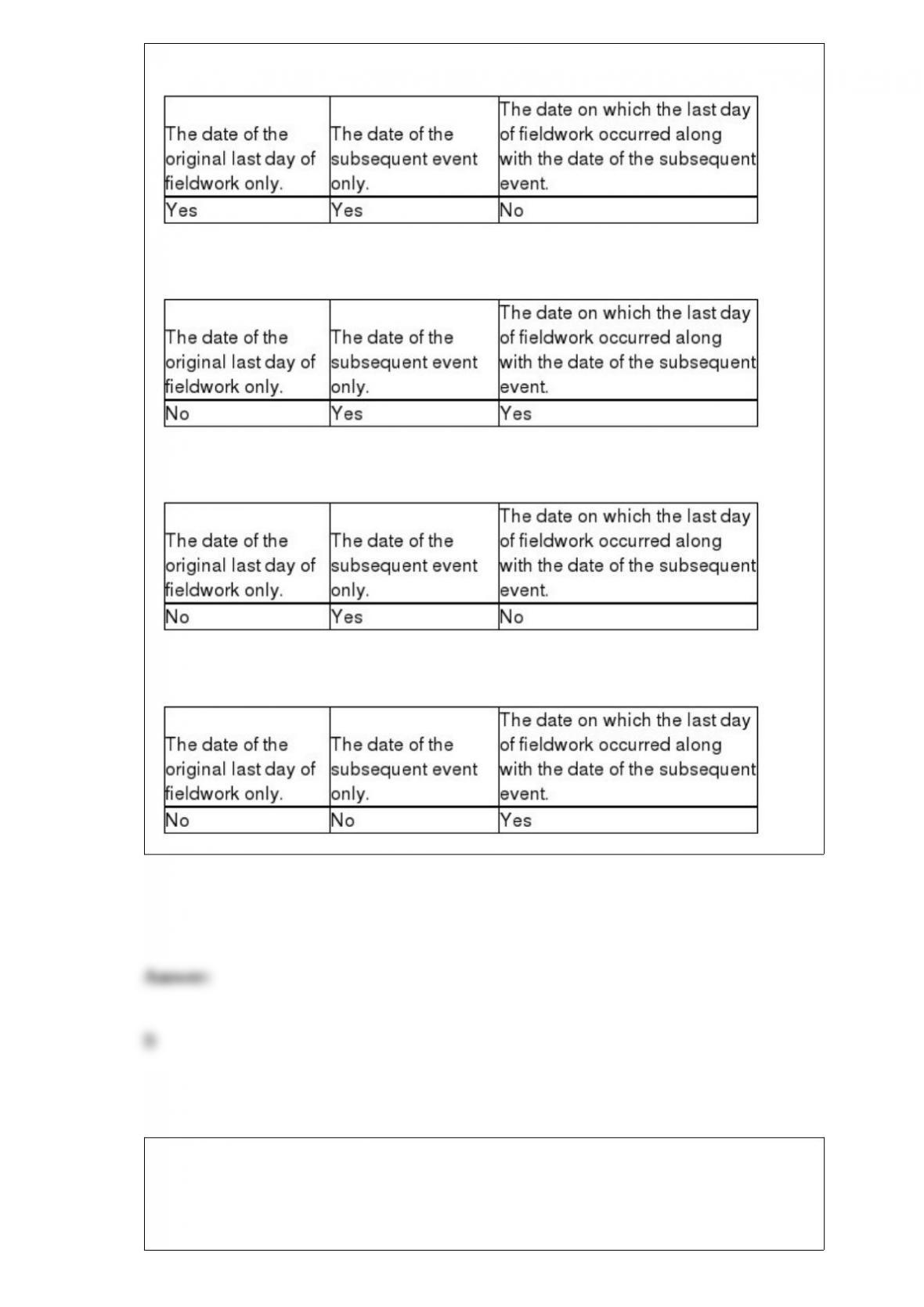

If the auditor determines that a subsequent event that affects the current period financial

statements occurred after fieldwork was completed but before the audit report was

issued, what date(s) may the auditor use on the report?

A)

B)

C)

D)

Attestation standards allow a CPA to perform all but which of the following services for

a forecast or projection?

A) compilation

B) review

C) examination

D) agreed-upon procedures

In determining the reasonableness of the client’s amount for depreciation expense the

auditor is primarily concerned that the client has followed a consistent policy and the

calculations are correct. Which of the following audit objectives best addresses the

above concerns?

A) existence

B) accuracy

C) valuation

D) allocation

Physical examination

A) is a direct means of verifying that an asset really exists.

B) is sufficient evidence to verify that the existing assets are owned by the client.

C) can be used for both tangible assets and documents.

D) is not generally a reliable type of audit evidence.

Which of the following statements is true as it relates to limited liability partnerships?

A) Only senior partners are liable for the partnerships debts.

B) Partners have no liability in a limited liability partnership arrangement.

C) Partners are personally liable for the acts of those under their supervision.

D) All partners must be AICPA members.

Which of the following is an accurate statement regarding the audit of the capital

acquisition and repayment schedule?

A) When internal controls over notes payable are deficient, auditors are required to

confirm the notes payable.

B) As auditors perform tests of details of balances for balance-related audit objectives,

the evidence obtained helps satisfy the notes payable presentation and disclosure

requirements.

C) The normal starting point for the audit of notes payable is a list of fixed asset

acquisitions.

D) The schedule of notes payable and accrued interest must be prepared regardless of

the number of transactions involved.

The auditor has completed her assessment of subsequent events. The proper accounting

for subsequent events that have a direct effect on the financial statements is to

A) adjust the financial statements for the year under audit.

B) disclose in the notes to financial statement the amount of the adjustment.

C) duly note in the audit workpapers that next year’s financial statements need to be

adjusted.

D) make no adjustment of the financial statements for the year under audit.

The most common audit test to verify equipment additions is to

A) examine vendors’ invoices.

B) perform an inventory of the fixed assets.

C) confirm the additions with the vendors.

D) trace the vendor invoices to the cash disbursements journal.

The appropriate and sufficient evidence to be obtained from tests of details must be

decided on an

A) efficiency basis.

B) effectiveness basis.

C) objective-by-objective basis.

D) none of the above

An inventory acquisition is received late in the afternoon of December 31 after the

physical inventory is completed. If the acquisition is included in accounts payable and

purchases, but excluded from inventory, the result

A) is an understatement of net earnings.

B) is an overstatement of net earnings.

C) is an overstatement of working capital.

D) is an overstatement of owner’s equity.

When sales invoices are automatically calculated and posted by a computer, the auditor

may be able to reduce substantive tests of transactions for which, if any, assertion?

A) accuracy

B) existence

C) completeness

D) none of the above

An auditor must inquire about consigned or customer inventory included on the client’s

premises to satisfy the balance-related audit objective of

A) cutoff.

B) classification.

C) rights.

D) completeness.

When there are no perpetual inventory files and inventory is material,

A) an audit cannot be performed, so the auditor must issue a disclaimer.

B) a physical inventory should be taken by the client near the end of the accounting

period.

C) the auditor will have to perform the inventory count and determine valuation.

D) the auditor need not observe inventory counts but must do test counts.

Management’s disclosure of the amount of unfunded pension obligations and the

assumptions underlying these amounts is an example of the ________ assertion.

A) completeness

B) existence

C) accuracy and valuation

D) rights and obligations

Why does the auditor divide the financial statements into segments around the financial

statement cycles?

A) Most auditors are trained to audit cycles as opposed to entire financial statements.

B) The approach aids in the assignment of tasks to different members of the audit team.

C) The cycle approach is required by auditing standards.

D) The cycle approach allows the auditor to detect illegal acts.

When the auditor suspects that fraud may be present, auditing standards require the

auditor to

A) terminate the engagement with sufficient notice given to the client.

B) issue an adverse opinion or a disclaimer of opinion.

C) obtain additional evidence to determine whether material fraud has occurred.

D) re-issue the engagement letter.

An auditor selects a sample from the file of shipping documents to determine whether

invoices were prepared. This test is to satisfy the audit objective of

A) accuracy.

B) existence.

C) control.

D) completeness.

A document sent to each customer showing his or her beginning accounts receivable

balance and the amount and date of each sale, cash payment received, any debit or

credit memo issued, and the ending balance is the

A) accounts receivable subsidiary ledger.

B) monthly statement.

C) remittance advice.

D) sales invoice.

Controls specific to IT include all of the following except for

A) adequately designed input screens.

B) pull-down menu lists.

C) validation tests of input accuracy.

D) separation of duties.

An auditor uses monetary unit sampling with a sampling interval of $20,000 and detects

an item with a recorded amount of $10,000 with an audited value of $4,000. The

projected misstatement of the sample is

A) $12,000.

B) $6,000.

C) $10,000.

D) $3,000.

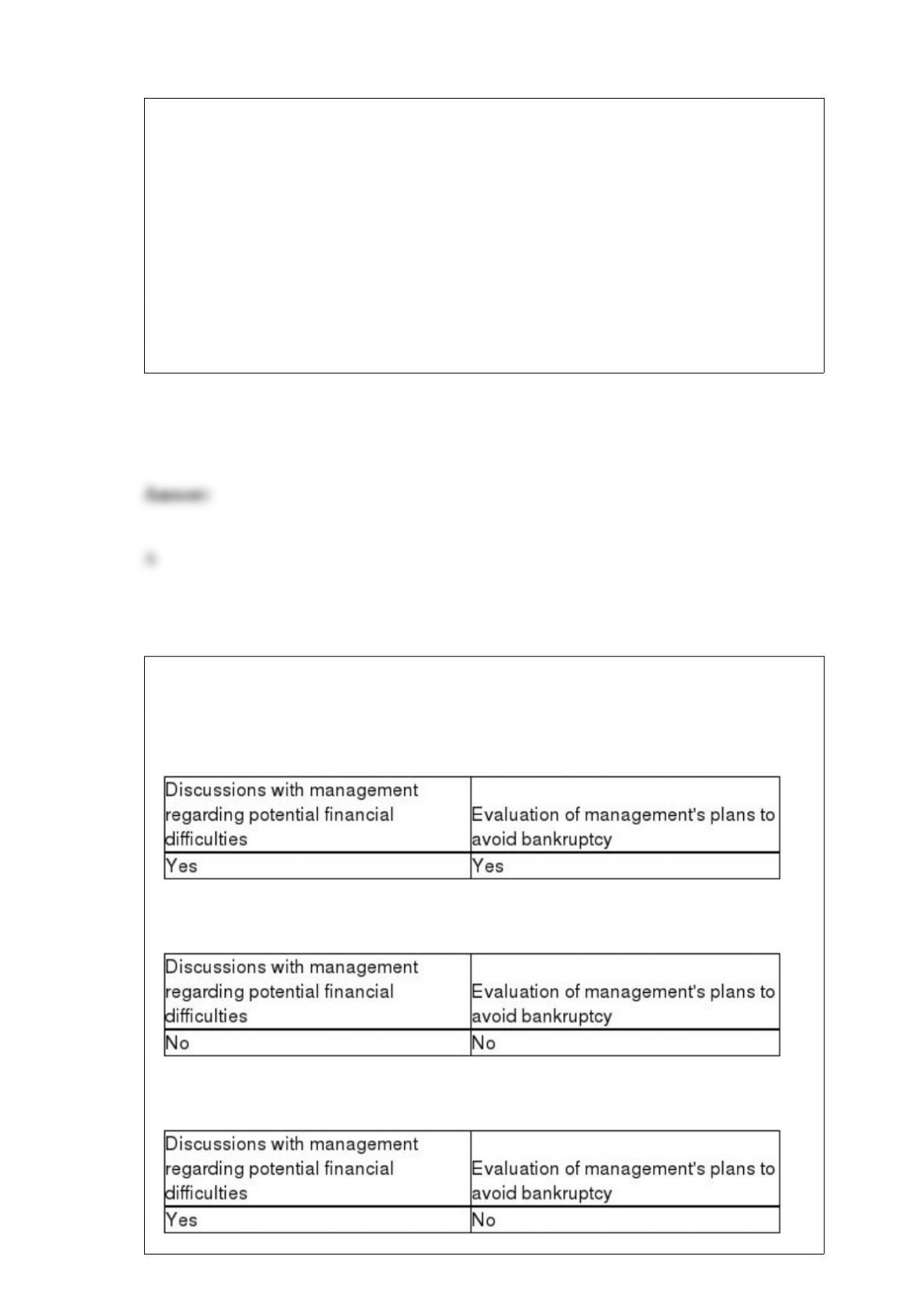

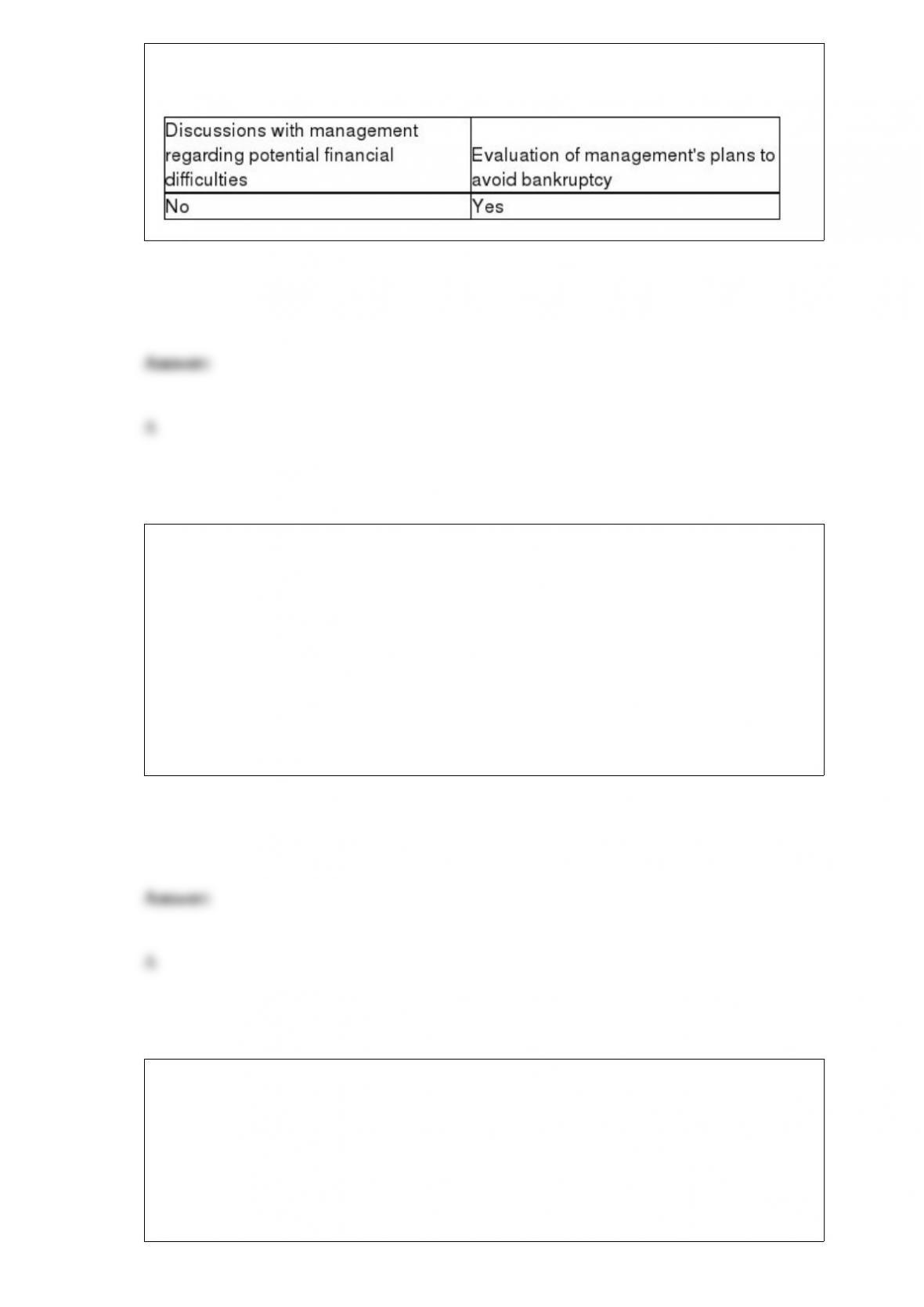

Which of the following procedures and methods are important in assessing a company’s

ability to continue as a going concern?

A)

B)

C)

D)

Actual interest expense is significantly higher than the auditor’s estimate. This would

most likely lead the auditor to conclude that the client has not

A) recorded all long-term interest bearing debt in the accounting records.

B) recorded all interest expense paid or accrued.

C) properly accounted for the discount of bonds payable account.

D) properly recorded interest income.

Fraud occurs when

A) a misstatement is made and there is both knowledge of its falsity and the intent to

deceive.

B) a misstatement is made and there is knowledge of its falsity but no intent to deceive.

C) the auditor lacks even slight care in the performance in performing the audit.

D) the auditor has an absence of reasonable care in the performance of the audit.