Determining if the financial instruments included in the schedule of investment activity

at year-end are stated at appropriate amounts in accordance with accounting standards is

the balance-related audit objective of

A) materiality.

B) realizable value.

C) consistency.

D) classification.

When labor is a significant part of inventory, verifying the proper accounting of these

costs should be tested in the

A) inventory and warehousing cycle.

B) payroll and personnel cycle.

C) acquisitions and payments cycle.

D) cash cycle.

When using the cycle approach to segmenting the audit, the reason for treating capital

acquisition and repayment separately from the acquisition of goods and services is that

A) the transactions are related to financing a company rather than to its operations.

B) most capital acquisition and repayment cycle accounts involve few transactions, but

each is often highly material and therefore should be audited extensively.

C) Both A and B are correct.

D) Neither A nor B is correct.

Auditors, as part of completing the audit, will request the client to send a standard

inquiry to the client’s attorney letter to those attorneys the company has been consulting

with during the year under audit regarding legal matters of concern to the company. The

primary reason the auditor requests this information is to

A) determine the range of probable loss for asserted claims.

B) obtain a professional opinion about the expected outcome of existing lawsuits and

the likely amount of the liability, including court costs.

C) obtain an outside opinion of the probability of losses in determining accruals for

contingencies.

D) obtain an outside opinion of the probability of losses in determining the proper

footnote disclosure.

Which of the following should sign checks under conditions of effective internal

control?

A) treasurer

B) purchasing agent

C) accounts payable clerk

D) person preparing the checks

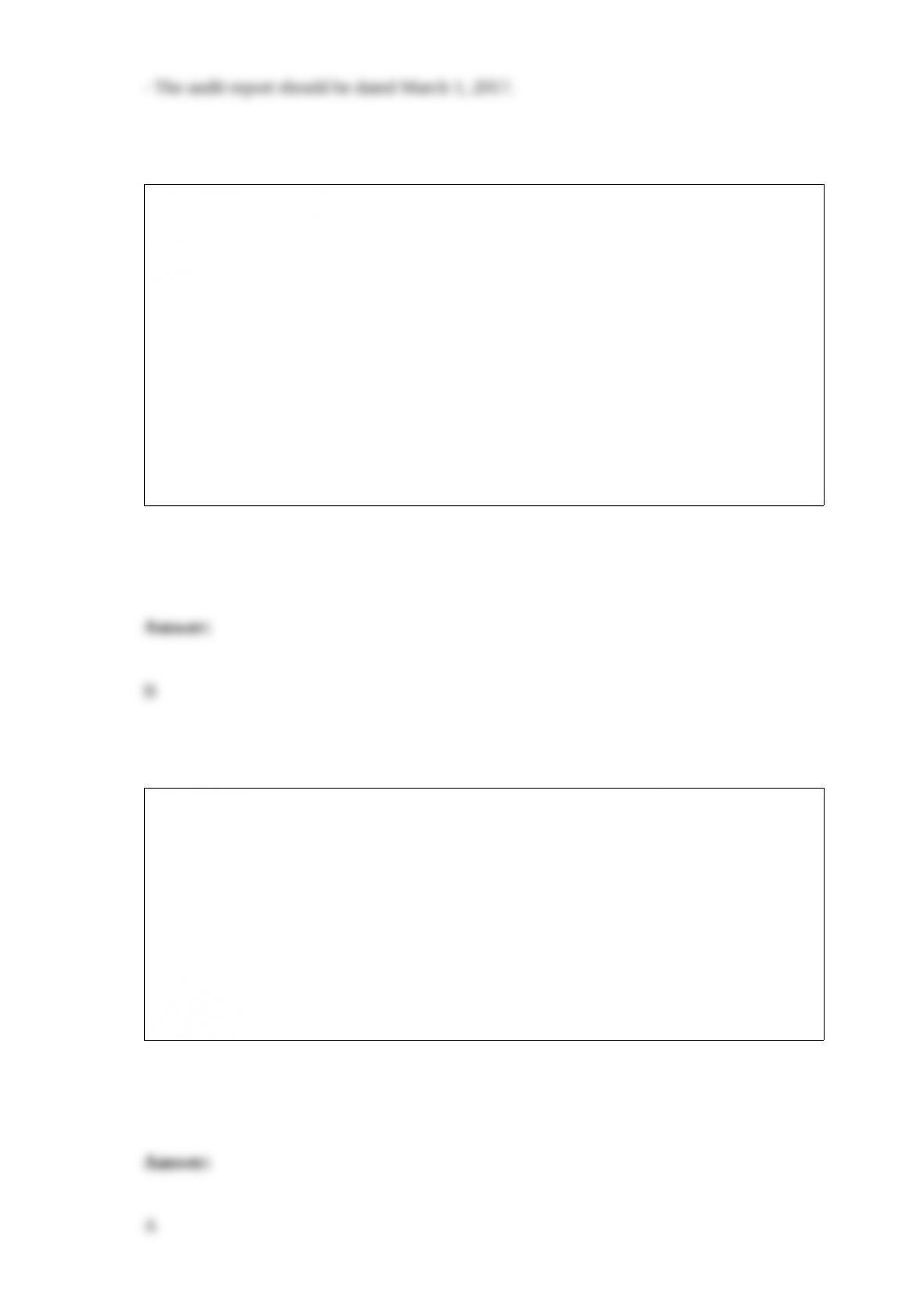

An audit report prepared by Garrett and Brown, CPAs, is provided below. The audit for

the year ended December 31, 2016 was completed on March 1, 2017, and the report

was issued to Javlin Corporation, a private company, on March 13, 2017. List any

deficiencies in this report. Do not rewrite the report.

We have examined the accompanying financial statements of Dalton Corporation as of

December 31, 2016. These financial statements are the responsibility of the company’s

management.

Management’s Responsibility for the Financial Statements:

Management is responsible for the preparation and fair presentation of the financial

statements in accordance with generally accepted auditing standards; this includes the

design, implementation, and maintenance of internal control relevant to the preparation

and fair presentation of financial statements that are free from all misstatement, whether

due to fraud or error.

Auditor’s Responsibility

Our responsibility is to give an opinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted

throughout the world. Those standards require that we plan and perform the audit to

obtain absolute assurance about whether the financial statements are free of

misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts

and disclosures in the financial statements. The procedures selected depend on

management’s judgment, including the assessment of the risks of material misstatement

of the income statement, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the auditor’s preparation

and fair presentation of the financial statements in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of expressing an opinion

on the effectiveness of the entity’s internal control. An audit also includes evaluating the

appropriateness of accounting policies and the accuracy of accounting estimates made

by management, as well as evaluating the overall presentation of the financial

statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to

provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present accurately the

financial position of Javlin Corporation as of December 31, 2016, in conformity with

accounting principles generally accepted in the United States of America.

Garrett and Brown, CPAs

March, 2017

Whenever subsequent events are used to evaluate the amounts included in the

statements, care must be taken to distinguish between conditions that existed at the

balance sheet date and those that come into being after the balance sheet date. The

subsequent information should not be incorporated directly into the statements if the

conditions causing the change in valuation

A) took place before the balance sheet date.

B) did not take place until after the balance sheet date.

C) occurred both before and after the balance sheet date.

D) are reimbursable through insurance policies.

Which of the following normally signs the engagement letter for an audit of a private

company?

A) management

B) board of directors representative

C) audit committee representative

D) corporate treasurer

The audit procedure referred to as proof of cash receipts is particularly useful to test

A) time lags in making deposits.

B) whether all recorded cash receipts have been deposited in the bank.

C) whether there are cash receipts that have not been recorded in the journals.

D) the client’s reconciliation between cash receipts and bank deposits.

When dealing with revenue frauds,

A) the most egregious form of revenue fraud involves premature revenue recognition.

B) premature revenue recognition involves recognizing the revenue after the accounting

standards requirements have been met.

C) premature revenue recognition is the same as cutoff errors.

D) side agreements can modify the terms of the sales transaction and should be

analyzed carefully.

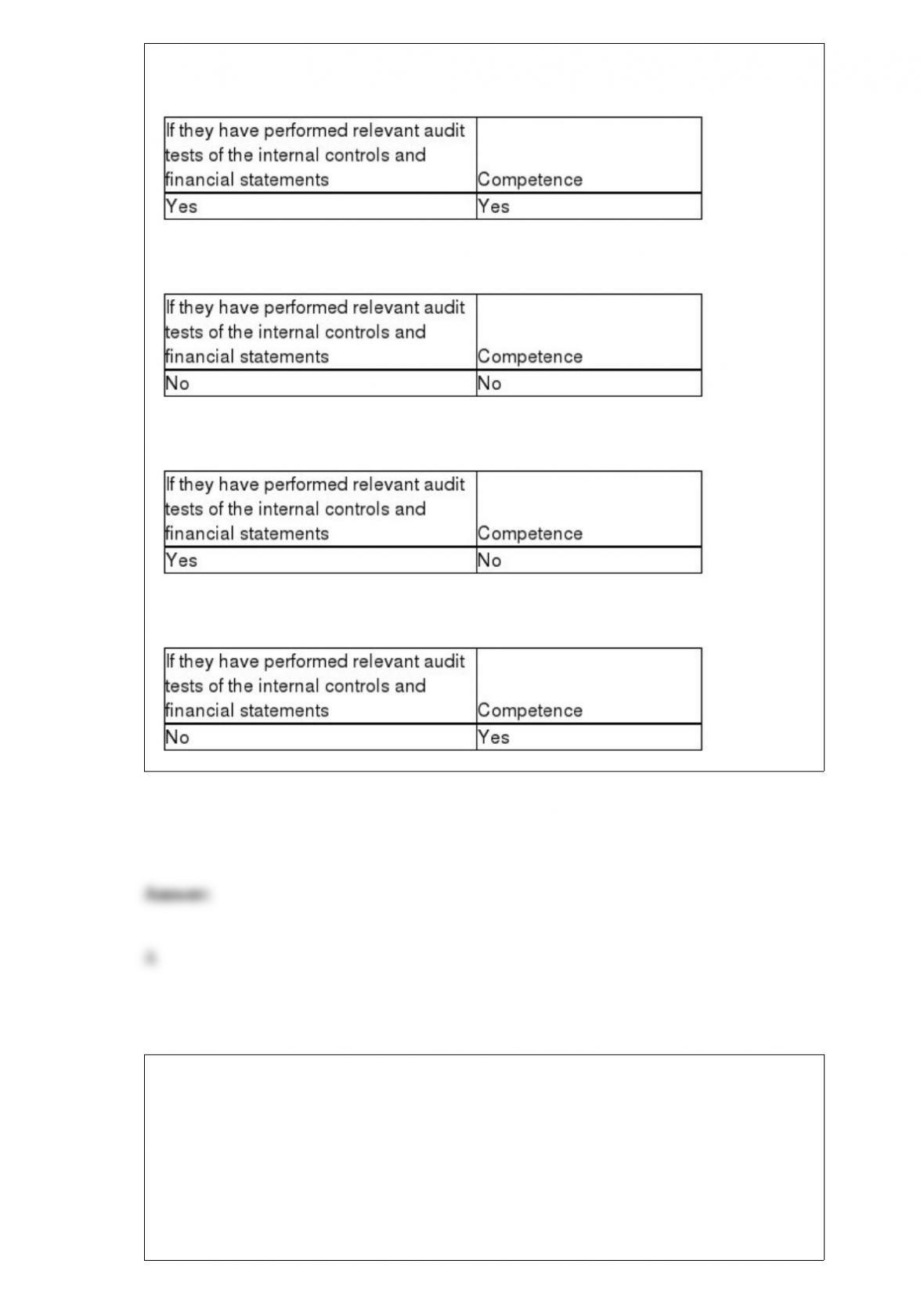

External financial statement auditors must obtain evidence regarding what attributes of

an internal audit department if the external auditors intend to rely on the internal

auditor’s work?

A)

B)

C)

D)

Why do auditors find MUS appealing?

A) MUS increases the likelihood of selecting a balance of high and low dollar items.

B) MUS is easy to use in the audit environment.

C) MUS provides a nonstatistical, rather than a statistical, conclusion.

D) When misstatements are found, MUS rarely produces bounds in excess of

materiality.

Auditors need to understand the client’s physical inventory count controls before the

count of the inventory begins so that

A) the auditors can accurately count and tag the inventory for the client.

B) the auditors can make constructive suggestions as to the adequacy of the procedures.

C) the client will be informed on exactly what items the auditor intends to test count.

D) the auditor can communicate any weaknesses directly to the audit committee.

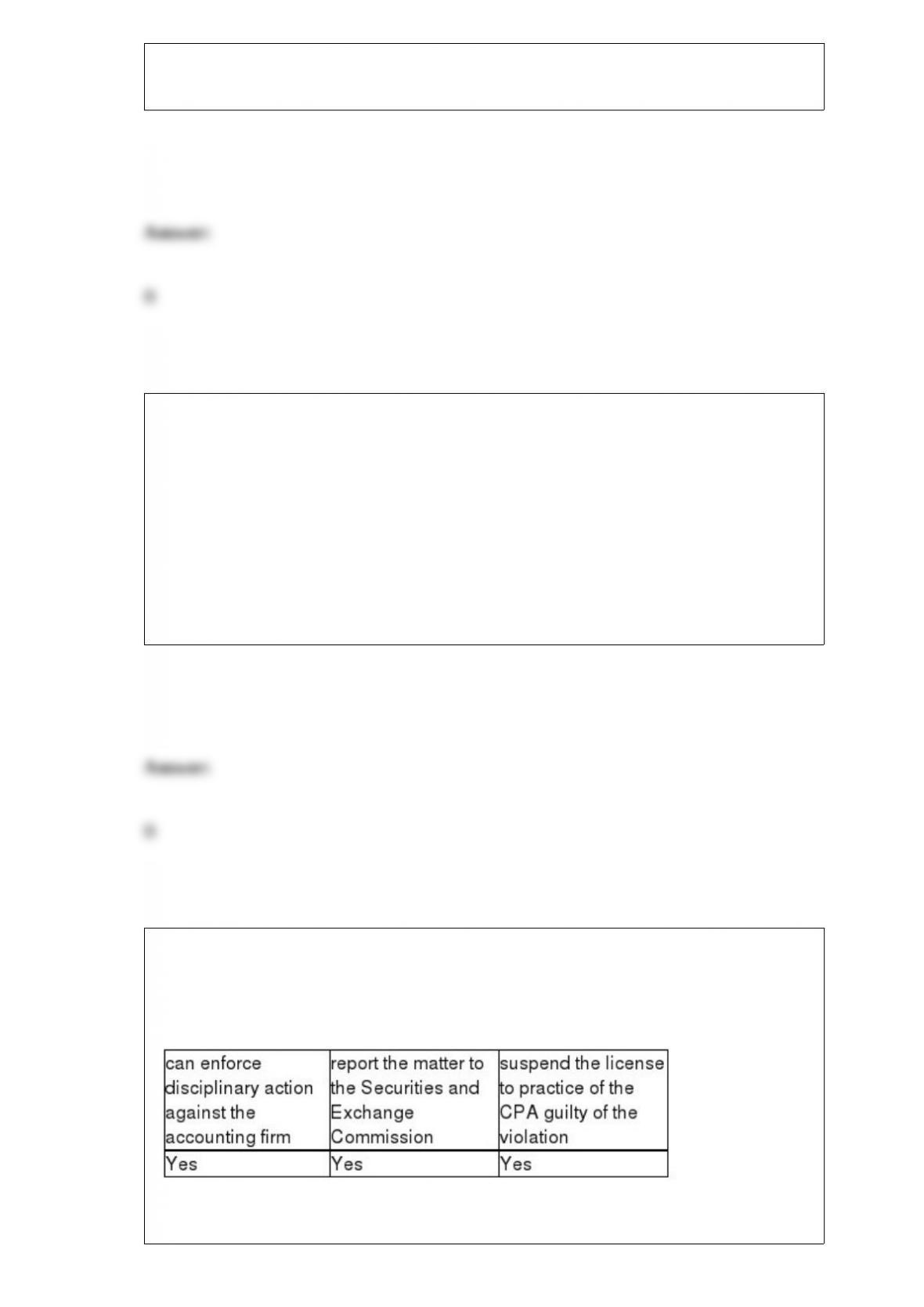

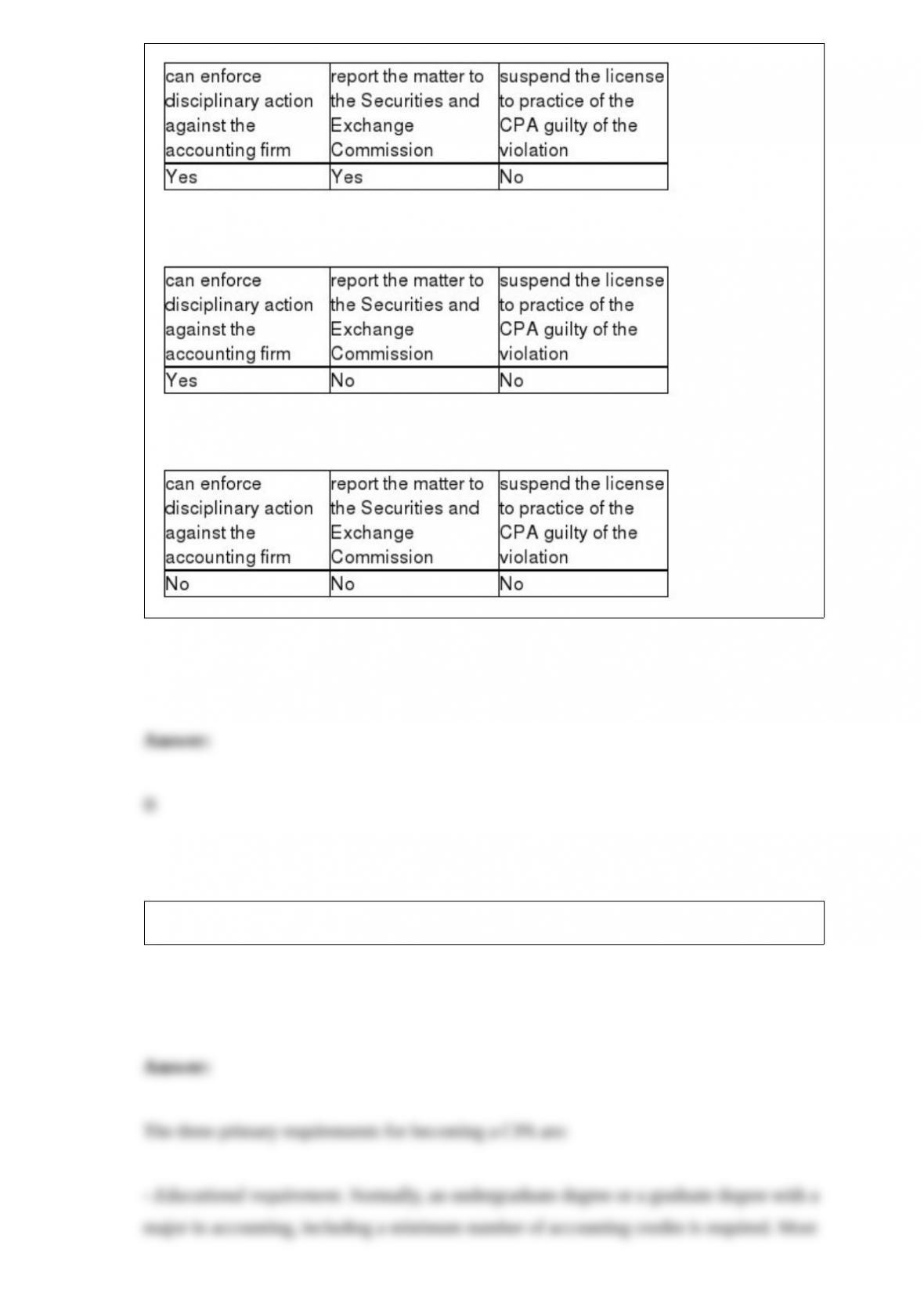

Assume the Public Company Accounting Oversight Board (PCAOB) identifies a

violation during its inspection of a registered accounting firm. The PCAOB

A)

B)

C)

D)

List and discuss the three primary requirements to become a CPA.

One objective of an operational audit is to

A) determine whether the financial statements fairly present the entity’s operations.

B) determine if the auditee is in compliance with GAAP.

C) make recommendations for improving performance.

D) report on the entity’s relative success in attaining profit maximization.

An auditor is gathering evidence on the completeness assertion. To do so, she performs

a test to verify that all goods received by the company have been recorded properly. The

document population for this test would consist of all

A) vendor invoices.

B) purchase orders.

C) receiving reports.

D) cash disbursements for accounts payable.

Internal auditors are expected to add value to the organization through improved

operational effectiveness. In addition, their responsibilities include all the following

except

A) reviewing the reliability and integrity of information.

B) ensuring compliance with the company’s accounting policies.

C) verifying accounting information for external users.

D) ensuring compliance with applicable governmental regulations.

The unqualified opinion audit report for public entities includes the following three

paragraphs:

A) introductory, scope and management’s responsibility.

B) materiality, scope and report.

C) introductory, scope and opinion.

D) scope, fieldwork and conclusion.

The primary source of authoritative literature for doing government audits is the

A) Purple Book.

B) Yellow Book.

C) Green Book.

D) Red Book.

An auditor has the responsibility to actively search for subsequent events that occur

subsequent to the

A) balance sheet date.

B) date of the auditor’s report.

C) balance sheet date, but prior to the audit report.

D) date of the management representation letter.

Which of the following would normally be discovered as part of the audit of the bank

reconciliation?

A) failure to bill a customer

B) failure to include a deposit in transit on the bank reconciliation

C) duplicate payment of a vendor’s invoice

D) payment to an employee for more hours than she worked

All of the following would require an emphasis of matter paragraph except for

A) the existence of material related party transactions.

B) the lack of auditor independence.

C) important events occurring subsequent to the balance sheet date.

D) material uncertainties disclosed in the footnotes.

For the report containing a disclaimer for lack of independence, the disclaimer is in the

A) second or scope paragraph.

B) third or opinion paragraph.

C) first and only paragraph.

D) fourth or explanatory paragraph.

Security controls should require that users enter a(n) ________ before being allowed

access to software and other related data files.

A) echo check

B) parity check

C) self-diagnosis test

D) authorized password

Which of the following is an accurate statement regarding cash?

A) The amount of cash flowing into and out of the cash account is often larger than that

for any other account in the financial statements.

B) The susceptibility of cash to embezzlement is greater than that for other types of

assets.

C) Auditors must verify whether recorded cash in the general ledger correctly reflects

all cash transactions that took place during the year.

D) All of the above are accurate statements.