A type of positive confirmation known as a blank confirmation

A) requests the recipient to fill in the amount of the balance.

B) is considered less reliable than the regular positive confirmation.

C) generates as high a response rate as the regular positive confirmation form.

D) is used when the auditor is confirming several small balances.

The management’s responsibility section of the standard unmodified opinion audit

report for a nonpublic company states that the financial statements are

A) the responsibility of the auditor.

B) the responsibility of management.

C) the joint responsibility of management and the auditor.

D) none of the above.

Verifying that an adequate chart of accounts is used is a key internal control for the

transaction-related objective of

A) classification.

B) accuracy.

C) existence.

D) occurrence.

A procedure to test for a cash receipts cutoff error is

A) reconciling the bank statement.

B) performing a four-column proof-of-cash.

C) observing the counting of cash at the balance sheet date.

D) tracing recorded cash receipts to subsequent period bank deposits on the bank

statement.

The most common case in which conditions beyond the client’s and auditor’s control

cause a scope restriction in an engagement is when the

A) auditor is not appointed until after the client’s year-end.

B) client won’t allow the auditor to confirm receivables for fear of offending its

customers.

C) auditor doesn’t have enough staff to satisfactorily audit all of the client’s foreign

subsidiaries.

D) client is going through Chapter 11 bankruptcy.

The auditor is determining that the correct selling price was used for billing and that the

quantity of goods shipped was the same as the quantity billed. She is gathering evidence

about which transaction-related audit objective?

A) existence

B) completeness

C) accuracy

D) cut-off

The auditor is concerned with the audited value rather than the misstatement amount of

each item in the sample when using

A) difference estimation.

B) mean-per-unit estimation.

C) ratio estimation.

D) monetary unit sampling.

When the sample selection is done using probability proportional to size sample

selection (PPS),

A) the actual number of units selected for testing may be more than the computed

sample size.

B) the auditor must use systematic selection, rather than random selection of dollars.

C) population items with a zero recorded balance have no chance of being selected.

D) negative balances must be treated as positive balances.

In order to obtain an understanding of the client’s business, the audit firm will consider

A) inherent and control risk of the client.

B) audit risk to the CPA firm.

C) the client’s business risk and the risk of material misstatements in the financial

statements.

D) the CPA firm’s potential ongoing revenue from the audit client.

Which of the following is required for a firm to designate itself “Member of the

American Institute of Certified Public Accountants” on its letterhead?

A) At least one of the owners must be a member of the AICPA.

B) All CPA owners must be members of the AICPA.

C) The CPA owners whose names appear in the firm name must be members of the

AICPA.

D) A majority of the owners must be members of the AICPA.

Which of the following is a correct statement?

A) The auditor uses the control risk assessment and results of tests of controls to

determine planned detection risk.

B) The auditor links the inherent risk assessments to the balance-related audit

objectives.

C) The audit risk model is used determine the level of audit risk.

D) All of the above are correct statements.

The two major factors affecting acceptable audit risk are

A) inherent risk and the intended uses of the financial statements.

B) control risk and the intended uses of the financial statements.

C) the likely statement users and their intended uses of the statements.

D) the audit firm and the intended uses of the statements

Proper segregation of functional responsibilities calls for separation of

A) authorization, execution, and payment.

B) authorization, recording, and custody.

C) custody, execution, and reporting.

D) authorization, payment, and recording.

Which of the following is a key internal control for the posting and summarization

transaction-related audit objective?

A) Batch totals are compared with computer summary reports.

B) Documents are canceled.

C) Dates are internally verified.

D) The accounts payable master file contents are internally verified.

The provisions of many laws and regulations affect the financial statements

A) directly.

B) only indirectly.

C) both directly and indirectly.

D) materially if direct; immaterially if indirect.

Personnel responsible for performing internal verification procedures must be

independent of those originally responsible for preparing the data.

Which of the following parties is responsible for implementing internal controls to

minimize the likelihood of fraud?

A) external auditors

B) audit committee members

C) management

D) Committee of Sponsoring Organizations

For financial statement audits, auditors need to understand controls that are relevant to

the audit in order to

A) identify and assess the risks of material misstatements.

B) perform preliminary analytical procedures.

C) detect fraud.

D) assess inherent risk.

Which of the following accounts is not included in the acquisitions class of

transactions?

A) inventory

B) prepaid expenses

C) sales discounts

D) accounts payable

Which of the following would have the least impact in determining sample size?

A) acceptable risk of overreliance

B) risk of assessing control risk too low

C) tolerable exception rate

D) population size

If no exceptions were found in the substantive tests of transactions,

A) ARIA would stay the same.

B) the sample size would stay the same.

C) ARIA would increase.

D) the sample size would increase.

For compilations, an accountant does which of the following?

A)

B)

C)

D)

Which account is used in the current ratio but not the quick ratio?

A) marketable securities

B) accounts payable

C) accounts receivable

D) inventory

In the audit of the transactions and amounts in the capital acquisition and repayment

cycle, the auditor must take great care in making sure that the significant legal

requirements affecting the financial statements have been properly fulfilled and

A) any violations are reported to the SEC.

B) are adequately disclosed in the financial statements.

C) must issue a disclaimer if they haven’t been fulfilled.

D) any departures from the agreements are made with management’s knowledge and

consent.

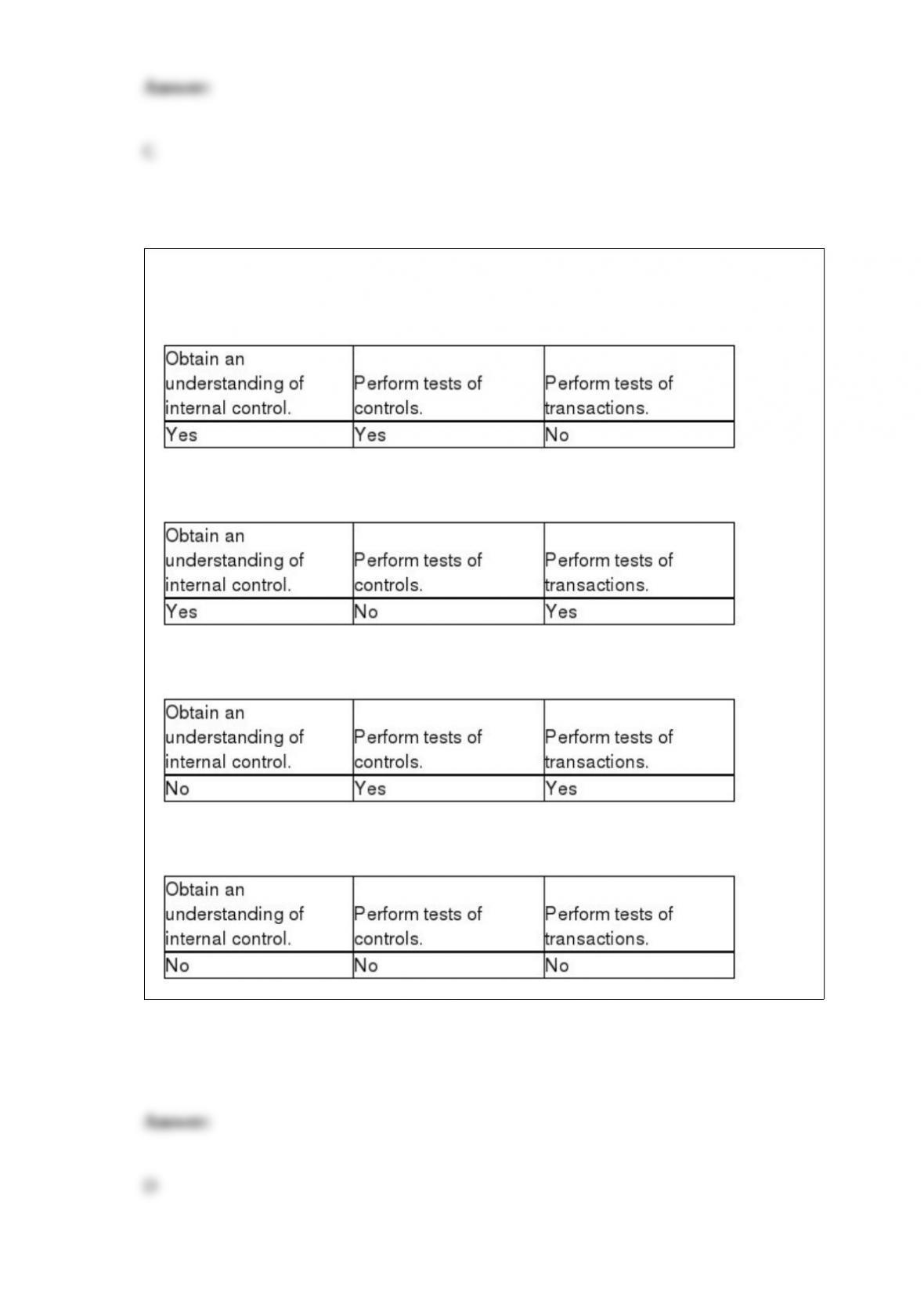

Which of the following is true regarding the relationship between tests of controls and

procedures to obtain an understanding?

A) In obtaining an understanding of internal control, the procedures to obtain an

understanding are applied to all controls identified during that phase.

B) Tests of controls are applied only when the assessed control risk has not been

satisfied by the procedures to obtain an understanding.

C) Procedures to obtain an understanding are performed only on one or a few

transactions.

D) All of the above are correct.

________ is a method of projecting from the sample to the population to estimate the

population misstatement. It assumes that misstatements in the unaudited population are

proportional to the misstatements found in the sample.

A) Mean-per-unit estimation

B) Point estimate

C) Monetary unit

D) Basic precision

The auditor is reviewing the receivables listed on the aged trial balance for notes and

related party receivables. Which balance-related audit objective is he trying to satisfy?

A) detail tie-in

B) existence

C) classification

D) all of the above

An accountant

A) must possess expertise in the accumulation of audit evidence.

B) must decide the number and types of items to test.

C) must have an understanding of the principles and rules that provide the basis for

preparing the accounting information.

D) must be a CPA.

A broad interpretation of the rights of third-party beneficiaries holds that users the

auditor should have been able to foresee as being likely users of financial statements

have the same rights as those with privity of contract. This is known as the concept of

A) foreseen users.

B) foreseeable users.

C) expected users.

D) four-party contracts.

The evaluations of financial information through analysis of plausible relationships

among financial and nonfinancial data is the definition of

A) analytical procedures.

B) tests of transactions.

C) tests of balances.

D) auditing.

When there is uncertainty about a company’s ability to continue as a going concern, the

auditor’s concern is the possibility that the client may not be able to continue its

operations or meet its obligations for a “reasonable period of time.” For this purpose, a

reasonable period of time is considered not to exceed

A) six months from the date of the financial statements.

B) one year from the date of the financial statements.

C) six months from the date of the audit report.

D) one year from the date of the audit report.

The assessment against a defendant of the full loss suffered by a plaintiff regardless of

the extent to which other parties shared in the wrongdoing is called

A) separate and proportionate liability.

B) shared liability.

C) unitary liability.

D) joint and several liability.

To be considered reliable evidence, confirmations must be controlled by

A) the client’s employee responsible for accounts receivable.

B) the external auditor.

C) the client’s internal audit department.

D) the client’s controller or CFO.

Auditor tests of the physical controls over raw materials, work in process, and finished

goods are generally limited to

A) observation and confirmation.

B) observation and inquiry.

C) inquiry and reconciliation.

D) observation and reconciliation.