9-20

9–39 (continued)

inventory, or could be the result of an acquisition, or they simply

haven’t paid it off. In any case, verifying this balance is a relatively

easy audit procedure.

2016. Federal income taxes payable on the balance sheet is

significantly lower at 12–31–16 than would be expected based on

Sales Whenever there is a drastic increase in business

activity, there is an increased risk of problems. It is possible that

controls will lapse or not be carefully observed. It is possible that

transactions will not be carefully accounted for. Therefore, in a

Cost of Goods Sold and Gross Profit Consistent with the

comments under sales, the auditors must determine why the gross

Pension Cost It appears that the Company exceeded the

contractual amount for additional pension contribution. Yet,

pension cost is a lesser percent of sales in 2016 than in 2015.

9–39 (continued)

d.

ACCEPTABLE

AUDIT RISK

INHERENT

RISK

SUBSTANTIVE

ANALYTICAL

PROCEDURES

Detail tie–in

Existence

Completeness

Accuracy

Classification

Cutoff

Realizable value

Rights

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

Medium

High

High

Medium

See Note 5

See Note 5

See Note 5

See Note 5

See Note 5

High

High

See Note 5

Performance materiality:

Trade accounts receivable $80,000

Allowance for uncollectible

accounts 15,000

Total $95,000

RATIONALE

4. Inherent risk for realizable value is considered high because of the

establishing the allowance for uncollectible accounts.

5. The analytical procedures performed are preliminary only, and

don’t provide substantive evidence. However, they can indicate

9-22

9–39 (continued)

Stanton Enterprises

Worksheet 9–39A

Determination of Materiality and

Allocation to the Accounts

12/31/2016

DETERMINATION OF MATERIALITY:

Income before taxes $8,004,277

Possible adjustments – estimated.

equal same %

of trade accounts

receivable as

prior year.

Increase accounts payable (1,070,000) Reflect same

Adjusted net income before taxes $6,714,277

Note: A key consideration is whether the

Company will be required to make its

additional pension contribution. As more

9-23

9–39 (continued)

Stanton Enterprises

Worksheet 9–39A, cont.

ALLOCATION TO THE ACCOUNTS:

Prelim.

12/31/16

Performance

Materiality

Cash

$243,689

5000

Easy to audit at low cost.

Trade accounts receivable

3,544,009

80000

Large performance materiality (PM) because

account is large and requires extensive sampling

to audit.

Allowance for uncollectible accounts

(120,000)

15000

Fairly large PM because of inherent risk.

Inventories

4,520,902

100000

Large PM because account is large and requires

extensive sampling to audit.

Prepaid expenses

29,500

5000

Easy to audit at low cost.

Total current assets

8,218,100

Property, plant, and equipment, at cost

12,945,255

100000

Small PM as a percent of account balance because

most of balance is unchanged from prior year &

audit of additions is relatively low cost.

Less: accumulated depreciation

(4,382,990)

40000

Fairly low PM due to possible risk of misstatement.

See answers to part c. of HW 9–39 and worksheet

9–39B.

8,562,265

Goodwill

1,200,000

20000

Fairly low PM due to possible risk of misstatement.

See answers to part c. of HW 9–39 and worksheet

9–39B.

Total assets

$17,980,365

Accounts payable

$2,141,552

70000

Large PM because account is large and requires

extensive sampling to audit.

Bank loan payable

150,000

0

Easy to audit at low cost.

Accrued liabilities

723,600

20000

Easy to audit at low cost.

Federal income taxes payable

1,200,000

40000

Fairly low PM due to possible risk of misstatement.

See answers to part c. of HW 9–39 and worksheet

9–39B.

Current portion of long–term

240,000

0

Easy to audit at low cost.

Total current liabilities

4,455,152

Long–term debt

960,000

0

Easy to audit at low cost.

Stockholders’ equity:

Common stock

1,250,000

0

Easy to audit at low cost.

Additional paid–in capital

2,469,921

0

Easy to audit at low cost.

Retained earnings

8,845,292

NA

Total stockholders’ equity

12,565,213

Total liabilities and stockholders’ equity

$17,980,365

$495,000

(1.5 x $330,000)

9-24

9–39 (continued)

Stanton Enterprises

Worksheet 9-37B

Analysis of Financial Statements

and Audit Planning Worksheet

12/31/2016

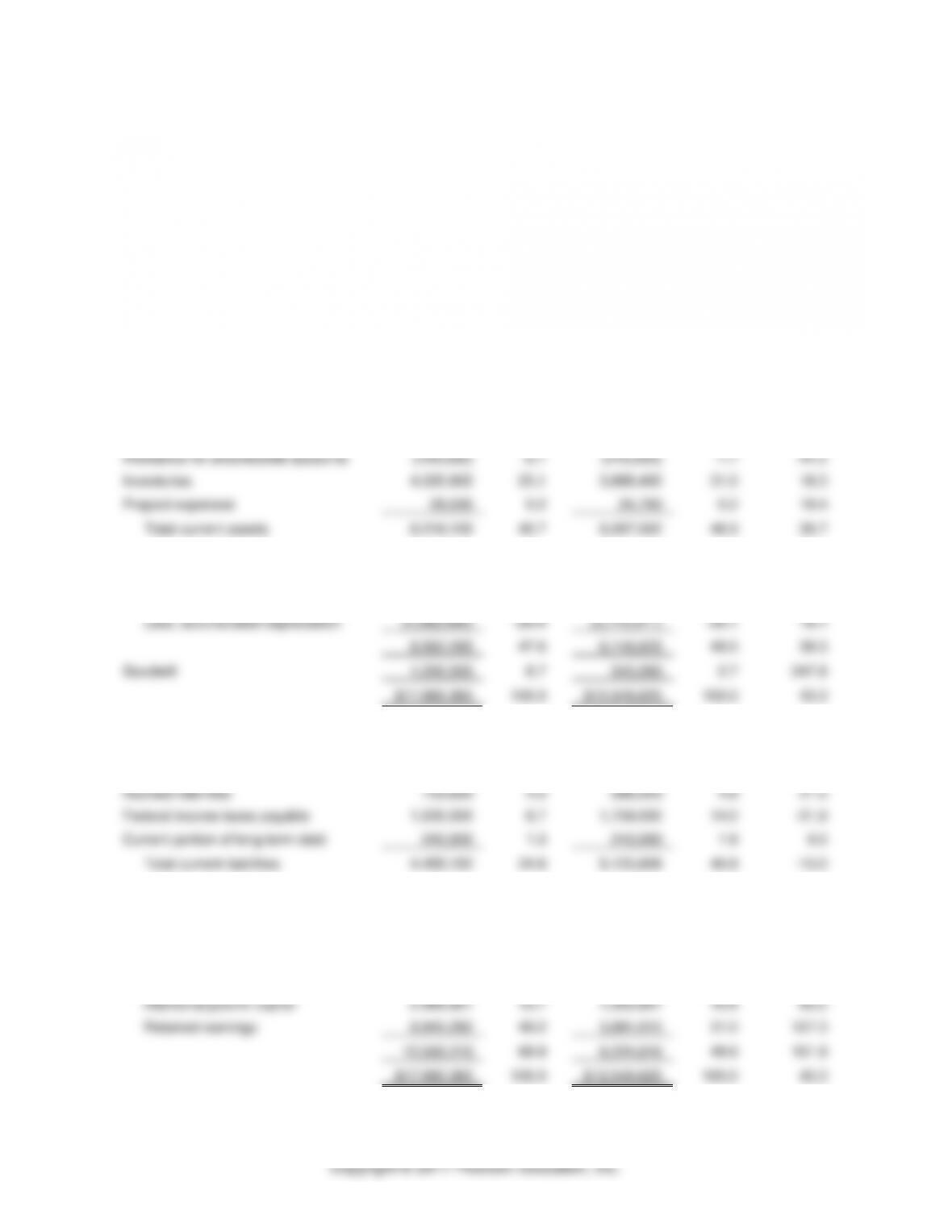

BALANCE SHEET

Preliminary

12/31/16

%

Audited

12/31/15

%

%

Change

Cash

$243,689

1.4

$133,981

1.1

81.9

Trade accounts receivable

3,544,009

19.7

2,224,921

17.7

59.3

Allowance for uncollectible accounts

(120,000)

-0.7

(215,000)

-1.7

-44.2

Inventories

4,520,902

25.1

3,888,400

31.0

16.3

Prepaid expenses

29,500

0.2

24,700

0.2

19.4

Total current assets

8,218,100

45.7

6,057,002

48.3

35.7

Property, plant, and equipment:

At cost

12,945,255

72.0

9,922,534

79.1

30.5

Less, accumulated depreciation

(4,382,990)

-24.4

(3,775,911)

-30.1

16.1

8,562,265

47.6

6,146,623

49.0

39.3

Goodwill

1,200,000

6.7

345,000

2.7

247.8

$17,980,365

100.0

$12,548,625

100.0

43.3

Accounts payable

$2,141,552

11.9

$2,526,789

20.1

-15.2

Bank loan payable

150,000

0.8

0

0.0

—

Accrued liabilities

723,600

4.0

598,020

4.8

21.0

Federal income taxes payable

1,200,000

6.7

1,759,000

14.0

-31.8

Current portion of long-term debt

240,000

1.3

240,000

1.9

0.0

Total current liabilities

4,455,152

24.8

5,123,809

40.8

-13.0

Long-term debt

960,000

5.3

1,200,000

9.6

-20.0

Stockholder’s equity:

Common stock

1,250,000

7.0

1,000,000

8.0

25.0

Additional paid-in capital

2,469,921

13.7

1,333,801

10.6

85.2

Retained earnings

8,845,292

49.2

3,891,015

31.0

127.3

12,565,213

69.9

6,224,816

49.6

101.9

$17,980,365

100.0

$12,548,625

100.0

43.3

9-25

9–39 (continued)

Stanton Enterprises

Worksheet 9–39B, cont.

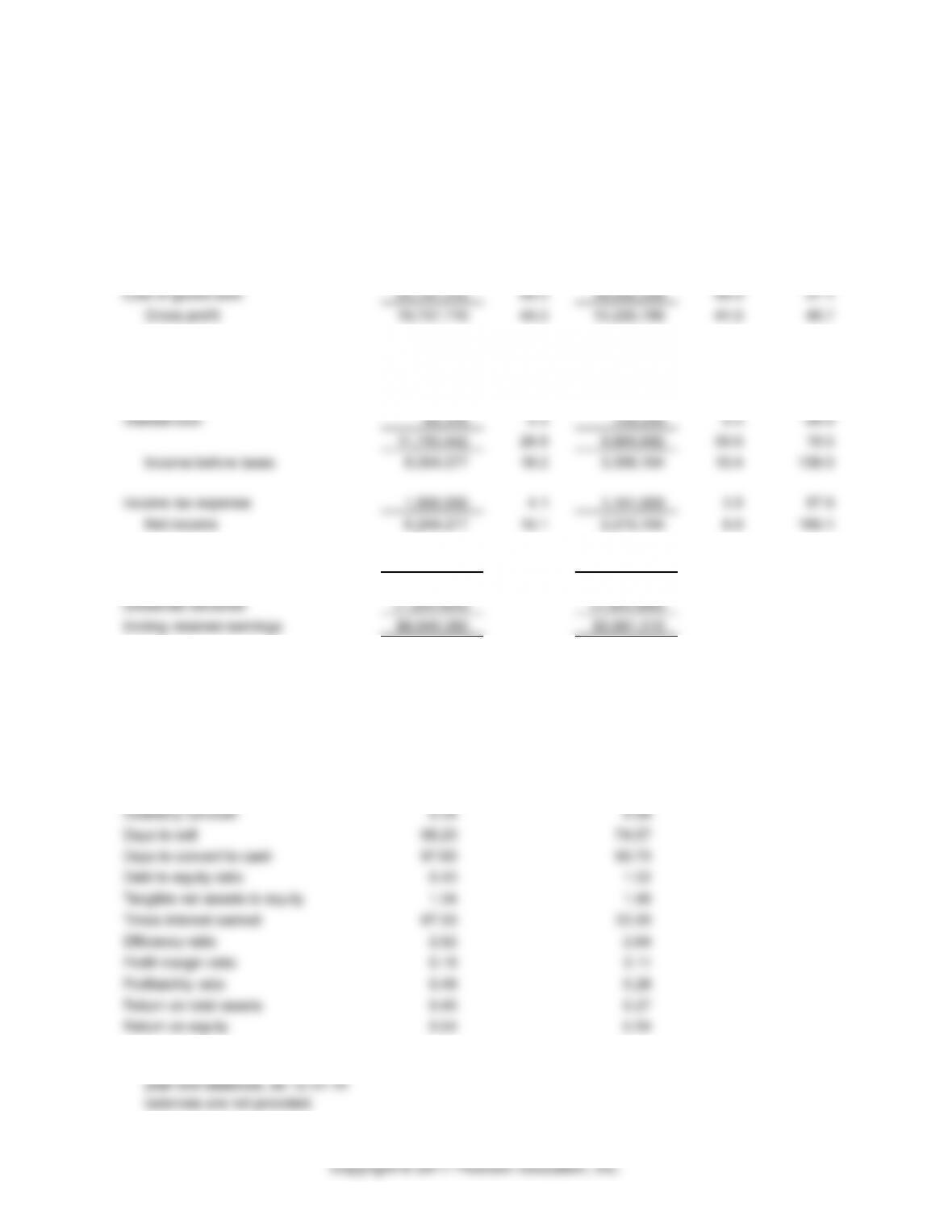

COMBINED STATEMENT OF INCOME

AND RETAINED EARNINGS

Preliminary

12/31/16

%

Audited

12/31/15

%

%

Change

Sales

$43,994,931

100.0

$32,258,015

100.0

36.4

Cost of goods sold

24,197,212

55.0

19,032,229

59.0

27.1

Gross profit

19,797,719

45.0

13,225,786

41.0

49.7

Selling, general, and

administrative expenses

10,592,221

24.1

8,900,432

27.6

19.0

Pension cost

1,117,845

2.5

865,030

2.7

29.2

Interest cost

83,376

0.2

104,220

0.3

–20.0

11,793,442

26.8

9,869,682

30.6

19.5

Income before taxes

8,004,277

18.2

3,356,104

10.4

138.5

Income tax expense

1,800,000

4.1

1,141,000

3.5

57.8

Net income

6,204,277

14.1

2,215,104

6.9

180.1

Beginning retained earnings

3,891,015

2,675,911

10,095,292

4,891,015

Dividends declared

(1,250,000)

(1,000,000)

Ending retained earnings

$8,845,292

$3,891,015

SIGNIFICANT RATIOS

Current ratio

1.84

1.18

Quick ratio

0.82

0.42

Cash ratio

0.05

0.03

Accounts receivable turnover

12.41

14.50

Days to collect

29.40

25.18

Inventory turnover

5.35

4.89

Days to sell

68.20

74.57

Days to convert to cash

97.60

99.75

Debt to equity ratio

0.43

1.02

Tangible net assets to equity

1.34

1.96

Times interest earned

97.00

33.20

Efficiency ratio

2.62

2.64

Profit margin ratio

0.18

0.11

Profitability ratio

0.48

0.28

Return on total assets

0.45

0.27

Return on equity

0.64

0.54

Note: Some ratios are based on

year–end balances, as 12–31–14

balances are not provided.

9-26

Integrated Case Application

9–40

PINNACLE MANUFACTURING―PART II

External users’ reliance on financial statements:

1. The company is privately held, but there is a large amount

of debt; therefore, the financial statements will be used

fairly extensively. Also, management is considering

debt financing.

Likelihood of financial difficulties:

1. The solar power engine business revolves around

constantly changing technology, thus making it inherently

Solar–Electro.

3. Item 9 in the planning phase indicates there is a debt

covenant requiring a current ratio above 2.0 and a debt–to–

Management integrity:

No major issue exists that would cause the auditor to question

management integrity, but the auditor should have done extensive

fraudulent financial reporting.

b. Acceptable audit risk is likely to be medium to low because of the

factors listed previously, especially the planned increase in

financing and the potential violation of the debt covenant

9-27

9–40 (continued)

c. Inherent risks are addressed by examining each of the 11 items in

the planning phase.

1. Inherent Risk: No effect on inherent risk.

3. Inherent Risk: There is a potential related party

transaction, which could affect the valuation of the

transaction and may require disclosure as a related party

transaction.

Accounts Affected: Manufacturing equipment, footnote

4. Inherent Risk: This situation involves a nonroutine

of sales

5. Inherent Risk: A receivable outstanding for several months

from a customer making up 15% of the company’s

outstanding accounts receivable balance may indicate a

understatement of the allowance for uncollectible

accounts.

Accounts Affected: Accounts receivable, bad debt

expense, allowance for uncollectible accounts

6. Inherent risk: No effect on inherent risk.

transaction.

Accounts Affected: Repairs and maintenance expense

and accounts payable

8. Inherent Risk: Although this does not directly affect

Accounts Affected: All accounts

9-28

9–40 (continued)

all debt covenants have been met.

Accounts Affected: All accounts

10. Inherent Risk: An ongoing dispute with the Internal

Revenue Service may require an adjustment to income tax

payable

11. Inherent Risk: This situation involves a related party

transaction (Solar–Electro borrowed money from the

Welburn division). Because this transaction was not

statements.

Accounts Affected: Notes payable, notes receivable,

interest expense and interest income