17-1

Chapter 17

Audit Sampling for

Tests of Details of Balances

Concept Checks

P. 575

1. The steps in nonstatistical sampling for tests of details of balances

and for tests of controls are almost identical, as illustrated in the text.

objectives, tests of controls and substantives tests of transactions are

designed to measure the occurrence rate of an attribute. In contrast,

2. When a population is not considered acceptable, there are several

possible courses of action:

Perform expanded audit tests in specific areas. If an analysis of

the misstatements indicates that most of the misstatements are of

Increase the sample size. When the auditor increases the sample

size, sampling risk is reduced if the rate of misstatements in the

expanded sample, their dollar amount, and their direction are

Adjust the account balance. When the auditor concludes that an

Request the client to correct the population. In some cases the

Refuse to give an unmodified opinion. If the auditor believes the

recorded amount in accounts receivable or any other account is

17-2

P. 583

1. The sampling interval is the book value of the population being

2. The projected misstatement for the item sampled is the percentage

error multiplied by the sampling interval:

($300/$3000) = .10 x $15,000 = $1,500

P. 588

1. Difference estimation is a method for estimating the total

misstatement in a population by multiplying the average misstatement

(the audited value minus the recorded value) in a random sample by

the number of items in the entire population.

estimating the total audited value of the population by multiplying the

arithmetic average, or mean audited value of the sample times the

number of items in the population.

Stratified mean–per–unit estimation is similar to mean–per–unit

The following are examples where each method could be used:

a. Difference estimation can be used in computing the

balance in accounts receivable by using the misstatements

discovered during the confirmation process, where a significant

number of misstatements are found.

employed.

d. Stratified mean–per–unit estimation can be used to determine

17-3

Concept Check, P. 588 (continued)

2. Tolerable misstatement represents performance materiality for an

individual sampling application. It is the amount of misstatement

the auditor believes can be present in an account and the

account balance still be acceptable for audit purposes.

Perform expanded audit tests in specific areas.

Increase the sample size.

In addition, it may be possible to adjust tolerable misstatement

(upward) and remake the decision. The basis for this would be a

Review Questions

17–1 The most important difference between (a) tests of controls and

substantive tests of transactions and (b) tests of details of balances is in what the

auditor wants to measure. In tests of controls and substantive tests of transactions,

the primary concern is testing the effectiveness of internal controls and the rate

17–2 Stratified sampling is a method of sampling in which all the elements

in the total population are divided into two or more subpopulations. Each

In order for an auditor to obtain a stratified sample of 30 items from each

of three strata in the confirmation of accounts receivable, he or she must first

17-4

Copyright © 2017 Pearson Education, Inc.

17–3 ARIA for tests of details of balances is the equivalent of ARO for tests

of controls and substantive tests of transactions. There is an inverse relation

between ARO for tests of controls and ARIA for tests of details of balances. If

internal controls are considered to be effective, control risk can be reduced. A

lower control risk requires a lower ARO, which requires a larger sample size for

testing. If controls are determined to be effective after testing, control risk can

remain low, which permits the auditor to increase ARIA. An increased ARIA

allows the auditor to reduce sample sizes for tests of details of balances.

17–4 The point estimate is an estimate of the total amount of misstatement in

population book value.

The true value of misstatements in the population is the net sum of all

misstatements in the population and can only be determined by a 100% audit.

17–5 The statement illustrates how the misuse of statistical estimation can

appropriate levels of risk and sample size.

17–6 Monetary unit sampling is a method whereby the population is defined

as the individual dollars (or other currency) making up the account balance. A

attributes sampling yet still provides a statistical result expressed in dollars. It

does this by using attribute tables to estimate the total proportion of population

dollars misstated, based on the number of sample dollars misstated.

a. The risk of incorrect acceptance (ARIA) — this is the risk that the

sample supports the conclusion that the recorded account balance

is not materially misstated when it is materially misstated.

b. The risk of incorrect rejection (ARIR) — this is the risk that the sample

17-5

17–7 (continued)

17–8 The preliminary sample size is calculated as follows:

Confidence factor

(10% ARIA, no expected misstatements) 2.31

is in machine–readable form. As the cumulative total exceeds a successive

random number, the item causing this event is identified as containing the

random dollar unit.

When systematic sampling is used, the population total amount is

using the cumulative method described previously.

17–10 Acceptable risk of incorrect acceptance (ARIA) is the risk the auditor is

willing to take of accepting a balance as correct when the true misstatement in

the balance is greater than tolerable misstatement. ARIA is the equivalent term

substantive tests of transactions.

The primary factor affecting the auditor’s decision about ARIA is control

risk in the audit risk model, which is the extent to which the auditor relies on

internal controls. When internal controls are effective, control risk can be

reduced, which permits the auditor to increase ARIA, which in turn reduces the

and ARIA can be increased.

17-6

Copyright © 2017 Pearson Education, Inc.

17–11 The statement reflects a misunderstanding of the statistical inference

process. The process is based on the long–run probability that the process will

produce correct results in a predictable proportion of the times it is applied.

Thus, a random sampling process that produces a 90% confidence interval will

produce intervals that do, in fact, contain the true population value 90% of the

time. However, the confidence limits of each interval will not all be the same.

17–12 Basic precision is the upper limit when no misstatements are found in

the sample, and represents the minimum allowance for sampling risk inherent

in the sample. It is calculated by multiplying the sampling interval by the

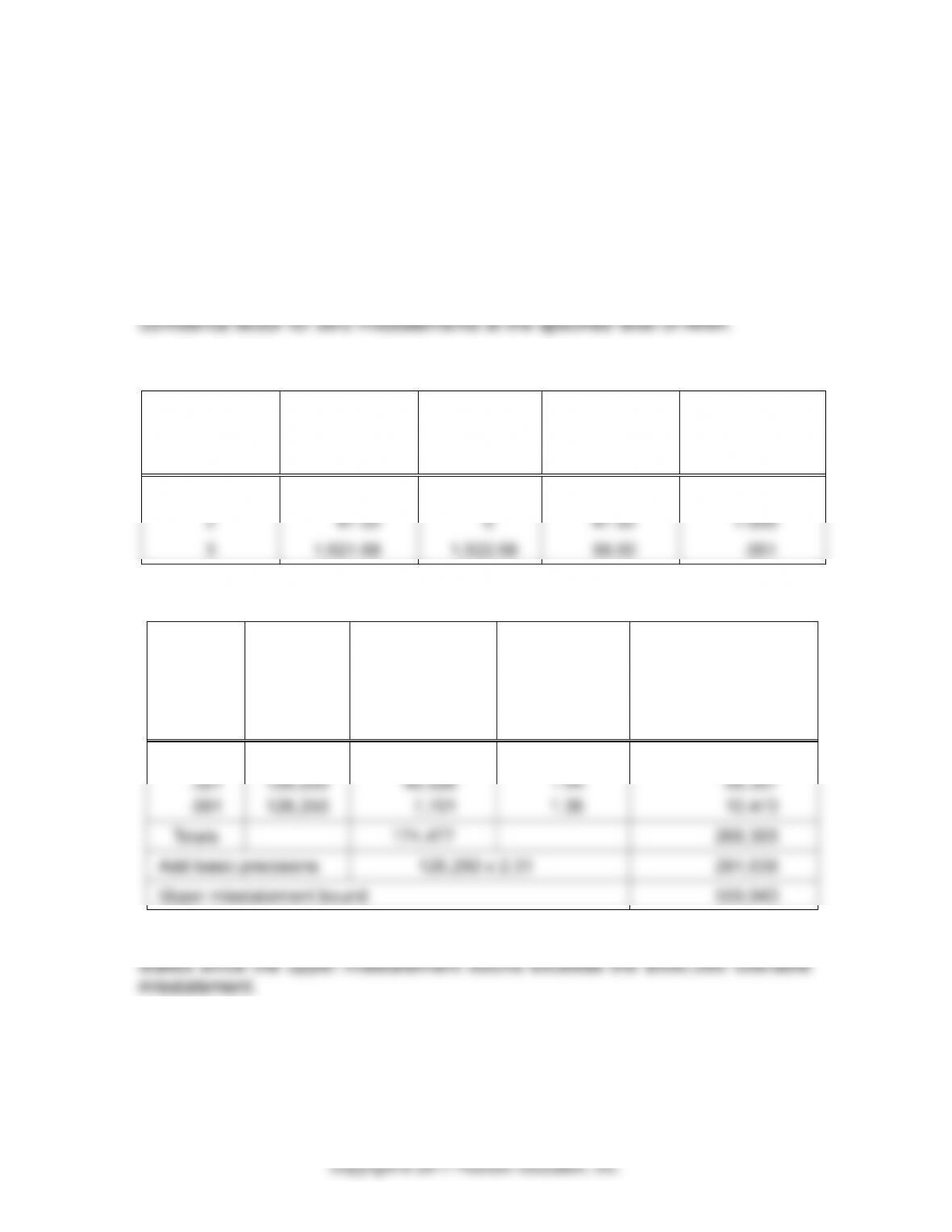

17–13 Misstatement bounds

MISSTATEMENT

RECORDED

VALUE

AUDITED

VALUE

MISSTATEMENT

TAINTING

MISSTATEMENT/

RECORDED

AMOUNT

1

897.16

609.16

288.00

.321

2

47.02

0

47.02

1.000

3

1,621.68

1,522.68

99.00

.061

The calculation of the misstatement bound is given below:

(a)

TAINTING

(b)

SAMPLING

INTERVAL

( c = a x b)

PROJECTED

MISSTATEMENT

(d)

INCREMENTAL

CHANGE IN

CONFIDENCE

FACTOR

(e = c x d)

PROJECTED

MISSTATEMENT PLUS

INCREMENTAL

ALLOWANCE FOR

SAMPLING RISK

1.00

.321

.061

126,250

126,250

126,250

126,250

40,526

7,701

1.58

1.44

1.36

199,475

58,357

10.473

Totals

174,477

268,305

Add basic precisions

126,250 x 2.31

291,638

Upper misstatement bound

559,943

Based on this calculation method, the population is not acceptable as

17-7

17–14 The difficulty in determining sample size lies in estimating the number

and amount of misstatements that may be found in the sample. The upper

bound of a monetary unit sample is sensitive to these factors. Thus, sample

17–15 The population standard deviation is a measure of the difference between

the individual values and the mean of the population. It is calculated for all

variables sampling methods but not for monetary unit sampling. For the auditor,

values in the sample.

The required sample size is directly proportional to the square of the

population standard deviation.

1. No determination was made as to whether a random sample of

100 inventory items would be sufficient to generate an acceptable

net amount.

3. Although no misstatement by itself may be material, other material

4. Regardless of the size of individual or net amounts of misstatements

17–17 Difference estimation can be very effective and very efficient where (1)

an audited value and a book value is available for each population item, (2) a

relatively high frequency of misstatements is expected, and (3) a result in the

form of a confidence interval is desired. In those circumstances, difference

17-8

17–18 Examples of audit conclusions resulting from the use of attributes,

Use of attributes sampling in a test of sales transactions for internal

verification:

We have examined a random sample of 100 sales invoices for

indication of internal verification; two exceptions were noted. Based

does not exceed 6.2%.

Use of monetary unit sampling in a test of sales transactions for existence:

We have examined a random sample of 100 dollar units of sales

transactions for existence. All were supported by properly prepared

Use of variables sampling in confirmation of accounts receivable (in the

form of an interval estimate and a hypothesis test):

We have confirmed a random sample of 100 accounts receivable.

We obtained replies or examined satisfactory other evidence for

misstatement is between $20,000 understatement and $40,000

Multiple Choice Questions from CPA Examinations

17–19 a. (4) b. (2) c. (3)

17–22 a. (4) b. (2) c. (1)

17-9

Discussion Questions and Problems

(6,900,000 x 2) / 150,000

b. If poor results were obtained for tests of controls and substantive

tests of transactions for sales, sales returns and allowances, and

cash receipts, the required sample size for tests of details of

acceptable risk of incorrect acceptance (ARIA).

c. A systematic sample can be selected based on the number of

accounts, or the dollar value of the population. To select a systematic

sample based on the number of accounts, the total number of

into two or more samples.

To select a systematic sample based on the dollar value of

the population, the population value is divided by the required sample

size to obtain the appropriate interval. A random number is then

selected between one and the interval as the starting point. The

selected using this method.

d. The direct projection of error for the sample can be computed as

follows:

(1,500/230,000) x 6,900,000 = $45,000 overstatement

The projected error of $45,000 is well below tolerable misstatement

of $150,000 and provides an allowance for sampling risk of $105,000.

Accordingly, the population is deemed to be fairly stated.

17–10

17–24 (see text Web site for Excel solution for part b.- Filename P1724.xls)

a. The following summarizes the confirmation responses:

Recorded

Value

Confirmation

Response

Misstatement

Acct. 147

$ 24,692

$ 22,486

$ 2,206

Pricing error

Acct. 228

183,219

157,216

26,003

Cutoff error

Acct. 278

7,546

5,546

0

Timing difference

Acct. 497

15,319

0

0

Timing difference

Acct. 564

8,397

7,858

539

Error in quantity

shipped

Acct. 653

32,687

19,328

13,359

Cutoff error

Acct. 830

5,286

0

5,286

Cutoff error

Total misstatement

$47,393

b. Estimate of total misstatement (P1724.xls):

Sample

Value

Sample

Misstatements

Book

Value

Projected

Misstatement

Stratum 1

$1,287,643

$26,003

$1,287,643

$ 26,003

Stratum 2

1,349,678

15,565

4,348,268

50,146

Stratum 3

94,637

5,825

947,682

58,331

Totals

$2,731,958

$47,3935

$6,583,593

$134,480

of $134,480 exceeds tolerable misstatement of $100,000 even

before consideration of sampling risk. The auditor is likely to

propose an adjustment for the actual errors detected and increase

17–25 Addressing misstatements involves auditor judgment, and depends on

Sample

Response

Comment

1

b. Record an adjustment for

actual misstatements

The upper bound will be less than tolerable

misstatement after recording an

adjustment for $20,000.

2

c. Expand sample size

Expanding the sample will lower sampling

risk, which may allow the auditor to accept

the sample.

3

d. Request client to fix the

population

The large number of errors and large

projected misstatement suggests it would

be preferable to have the client fix the

population.